A lot of people enter the business loan application process thinking the value sits in the form. It doesn't. The value sits in judgment. A weak broker forwards paperwork. A strong broker screens the deal, packages it correctly, matches it to the right lender, manages the file through underwriting, and keeps the client calm when the process gets messy.

That matters because the process is slow, document-heavy, and still more manual than most borrowers expect. Most small businesses spend 24 to 34 hours filling out applications and submitting paperwork, and underwriting alone often runs 24 hours to 3 business days. Nearly 47% of lenders still use highly manual workflows, which is one reason delays keep showing up in ordinary deals (Abrigo on small business lending process data).

For a broker building a remote, referral-driven business, that friction is an opportunity. Business owners don't just need capital. They need someone who can shorten confusion, reduce avoidable mistakes, and give honest direction before a bad application burns time and credibility.

Table of Contents

- Your Role Before the Application Begins

- Assembling a Bulletproof Loan Package

- Strategic Lender Matching for Higher Approvals

- Navigating Underwriting and Managing Timelines

- The Broker's Payday From Offer to Commission

- Handling Denials and Building Client Trust

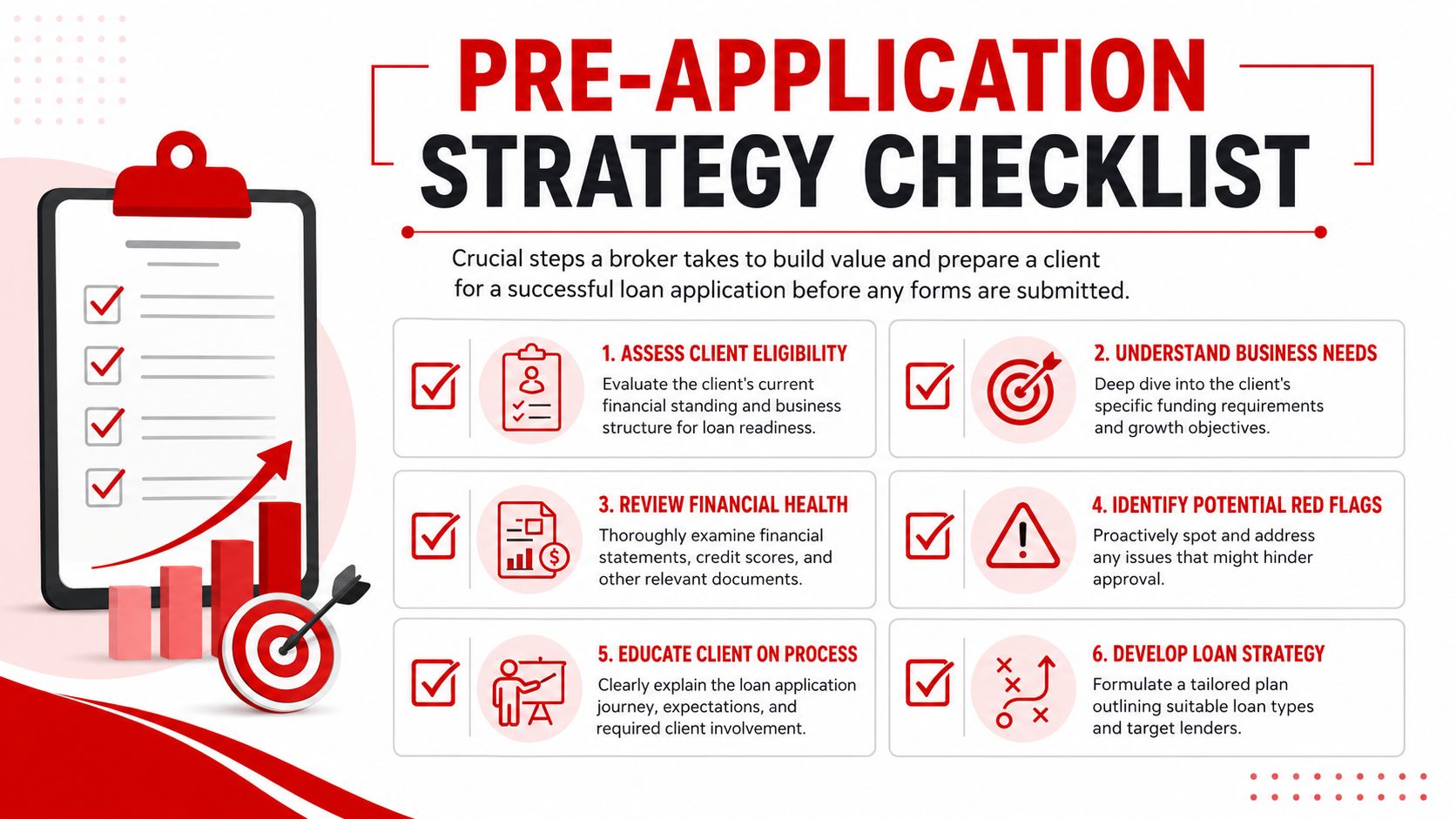

Your Role Before the Application Begins

Start with readiness, not rate shopping

The broker's real job starts before any lender sees the file. At that stage, the client usually wants one answer. “Can this get done?” The better answer is, “That depends on whether the business is ready, whether the request makes sense, and whether the story matches the paper.”

A clean pre-application review should cover more than credit. Revenue consistency matters. Existing debt obligations matter. Deposit behavior matters. The intended use of funds matters. If a client can't explain why they need the money, how it will be used, and how the business will carry the new payment, the problem isn't the lender. The problem is preparation.

Many lenders also expect a breakeven analysis as part of risk review, along with at least two years of personal and business tax returns, profit and loss statements, and bank statements (Wolters Kluwer on what banks review in a loan application). That requirement alone tells a broker what to do early. If the file can't support those basics, the deal needs repositioning before submission.

Practical rule: If the borrower is still guessing on loan amount, use of funds, or document availability, the application isn't ready.

A strong pre-flight review usually includes:

- Business purpose: expansion, payroll support, equipment, inventory, refinance, or short-term working capital

- Repayment logic: where the payment will come from each month

- Financial consistency: whether statements and tax returns tell the same story

- Pressure points: declining deposits, unresolved credit issues, recent cash strain, or missing records

Set expectations before emotion takes over

Most borrower frustration comes from surprise. That's why expectation-setting is part of the business loan application process, not a side conversation.

Clients should know that even good files can slow down when underwriters ask for clarification, ownership docs, updated statements, or explanations for unusual activity. They should also know that not every lender evaluates risk the same way. The right move is often to explain the path before discussing outcomes.

For brokers who want fewer misunderstandings and more long-term trust, this kind of client expectation management framework is worth building into every intake.

Borrowers rarely get upset about a tough process when they were prepared for it upfront. They get upset when the broker promised a shortcut that never existed.

That's how a one-time transaction becomes a referral relationship. The broker doesn't sell hope. The broker gives clarity.

Assembling a Bulletproof Loan Package

Think like an underwriter

Underwriters don't reward effort. They reward clarity. A package gets traction when the decision-maker can see the business quickly, understand the request, and verify the numbers without chasing missing pieces.

That means the broker should build the file like a case, not like a stack of attachments. Every document needs a job. Tax returns confirm history. Bank statements support cash movement. Profit and loss statements frame performance. A short written summary explains what the business does, why capital is needed now, and why repayment is realistic.

Sloppy files create avoidable resistance. So do mislabeled PDFs, mixed date ranges, password-protected statements sent without notice, and duplicate uploads. When a file has multiple owners, guarantors, leases, statements, and legal records, brokers often save time by using processes similar to offline PDF merging for legal teams so the package stays organized before submission.

The Ultimate Business Loan Documentation Checklist

| Document Category | Specific Items | Broker's Pro-Tip |

|---|---|---|

| Business financials | Profit and loss statements, bank statements, balance sheet if available | Match statement periods across documents so the lender doesn't question inconsistencies |

| Tax records | Personal and business tax returns | Review for extensions, missing schedules, and entities that don't line up with the application |

| Ownership and legal | Formation docs, operating agreement, business license, voided check if needed | Make sure signer authority is obvious before closing starts |

| Debt and obligations | Business debt schedule, current loan statements, lease obligations | Note any recent payoffs or restructures so old liabilities don't look active |

| Use of funds | Written summary of how capital will be deployed | Tie the request to a business purpose, not a vague desire for “working capital” |

| Performance narrative | Brief business overview and explanation of strengths or anomalies | Address irregular deposits or one-time events before the underwriter asks |

A lender-ready package usually follows a simple order:

- Application and summary first: give the underwriter context before they hit the raw documents.

- Financial support second: statements, tax returns, and operating records should back the summary.

- Explanations last: include concise notes for anything that may trigger questions.

The easiest file to approve is the file that answers the underwriter's first five questions before they ask them.

A good broker also prepares the client for document discipline. Files should be named clearly, dated correctly, and stored in a way that makes resubmission easy if another lender needs the same package. That matters because one of the fastest ways to lose momentum is rebuilding a file from scratch each time.

For a deeper breakdown of what lenders commonly ask for, this guide to commercial loan requirements helps frame the difference between “submitted” and “fundable.” Those are not the same thing.

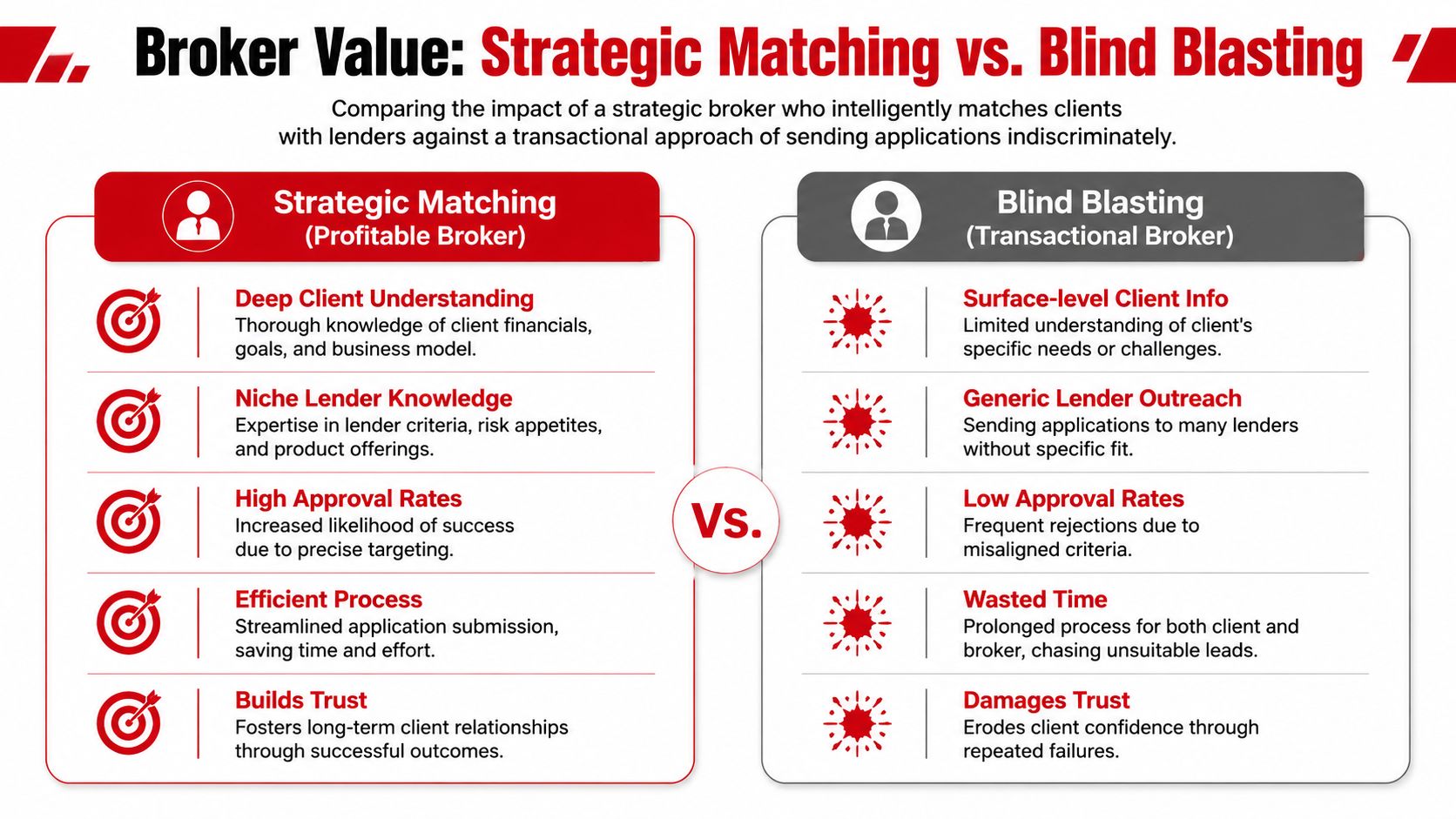

Strategic Lender Matching for Higher Approvals

Why matching beats volume

Most new brokers think more submissions create more opportunities. Usually, they create more denials. Sending one file everywhere doesn't make the deal stronger. It signals that the broker doesn't understand lender fit.

A broker's services are valuable. Alternative lenders matter because many borrowers don't fit the narrow box of a traditional bank. Non-bank lenders show an approval rating of nearly 25%, which statistically doubles the chances of success for small businesses compared to traditional bank applications (Capital Bank on business loan approval differences).

That doesn't mean every alternative product is right. It means the market rewards informed placement. A broker who understands lender appetite can save a borrower from the wrong application path and save the file from unnecessary declines.

What a smart match actually looks like

The strongest lender match starts with the profile, not the product. A broker should ask:

- What does the business need? Short-term flexibility, fixed repayment, equipment-specific financing, or a larger structured facility.

- What does the file support today? Stable deposits, cleaner tax returns, stronger collateral, or a narrower ask.

- What kind of lender fits the risk? Conservative, industry-specific, cash-flow driven, collateral-driven, or speed-focused.

A practical matching process often looks like this:

| Borrower Situation | Weak Broker Move | Strong Broker Move |

|---|---|---|

| Client wants fast capital but has uneven documentation | Blast to multiple lenders and hope one bites | Tighten the package and target lenders that can work with the file as it stands |

| Client asks for more than the business can support | Submit the full ask without pushback | Reset the amount to something defensible |

| Client has a solid business but doesn't fit a bank box | Keep retrying bank-style channels | Shift to an alternative lender with a better fit |

| Client has mixed strengths and weaknesses | Lead with the weakness | Position the strength first and explain the weakness directly |

A lender match isn't about finding someone willing to say yes to anything. It's about finding the lender whose risk model matches the file in front of them.

Profitable brokers build lender knowledge the same way good recruiters build hiring intuition. They learn what each capital source likes, what gets a fast decline, what documentation matters most, and which businesses belong somewhere else. That knowledge compounds into faster approvals, cleaner communication, and stronger referral trust.

Navigating Underwriting and Managing Timelines

A file can look clean at submission and still stall for a week once underwriting gets involved. New brokers read that as lender delay. Experienced brokers read it as a file that raised questions the package did not answer upfront.

Underwriting is a credibility check. The lender is testing whether the story told in the application holds up against bank statements, tax returns, entity records, existing debt, and the requested payment structure. Silence during this stage usually means the file is being reviewed, compared, and stress-tested, not ignored.

From a broker's perspective, the job changes here. Before submission, the main work is packaging and lender fit. After submission, the main work is controlling friction and keeping the borrower from creating new problems with rushed or incomplete responses.

The slowdowns are predictable:

- Signer issues: ownership percentages, guarantors, or entity documents do not line up

- Stale documents: the lender wants more recent statements or updated receivables

- Cash flow questions: transfers, large deposits, or seasonal drops need a plain-English explanation

- Debt discrepancies: obligations on the credit profile do not match what the client disclosed

- Unsupported ask: the requested amount or payment stretches the business more than the file can defend

Good brokers do not just relay stipulations. They translate them.

If an underwriter asks for updated statements, the client should know whether the lender is checking current revenue, looking for declining balances, or verifying that a recent dip has recovered. If repayment capacity becomes the pressure point, the broker should be fluent enough to explain a debt service coverage ratio calculation in simple terms and reset the conversation around what the business can carry.

A simple cadence keeps files alive:

- Acknowledge the lender request fast.

- Tell the client exactly what to send, in the format the lender expects.

- Review everything before it goes back out.

- Package explanations with the documents instead of waiting for the next question.

- Update the client before they ask for an update.

That last point matters more than new brokers realize.

Borrowers rarely get upset because underwriting asked for one more item. They get upset when nobody explains why the item matters, what happens next, or whether the deal is still on track. A broker who manages perception well can hold a file together even when the lender asks for more than expected. A broker who goes quiet loses trust fast, even on an approvable deal.

The trade-off is straightforward. Pushing the lender every few hours can annoy the credit team and buy you nothing. Letting a file sit untouched can kill urgency and invite second thoughts from the borrower. The right move is controlled pressure. Clear responses, clean follow-up, and realistic timeline resets.

That is how brokers protect approvals. It is also how they build the kind of client experience that turns one funded deal into repeat business and referrals.

The Broker's Payday From Offer to Commission

The offer is not the finish line

A file gets approved. The client feels relief. New brokers sometimes relax too early.

The file still has to close.

That means the broker now has to help the client read the offer correctly. Not just the headline amount. The structure, payment rhythm, conditions before funding, signer requirements, and any final items that must be cleared before money moves. A funded deal is usually the result of calm hand-holding at this exact stage.

One borrower may need help comparing whether the offer solves the cash need they described at intake. Another may need to understand why a lower amount with cleaner execution is better than chasing a larger approval that drags. A good broker doesn't pressure. A good broker interprets.

How the commission gets earned

Here's the clean version. Business loan brokers typically earn commission fees ranging from 1% to 3% of the total loan amount, with some complex deals reaching up to 5% or more. These fees are paid by the lender upon successful closing, not by the borrower upfront.

That structure matters for two reasons. First, the commission follows value. The broker only gets paid when the deal funds. Second, it forces discipline. Files that were screened well, packaged well, and matched well are much more likely to make it across the finish line.

A typical close often unfolds like this:

- Offer received: broker reviews terms before sending anything to the client

- Client discussion: questions get answered in plain language

- Conditions cleared: final statements, signatures, or entity docs are delivered

- Funding confirmed: broker verifies that proceeds landed

- Relationship extended: broker asks for introductions while the win is still fresh

The referral ask lands best right after a funding, when the client still remembers who made the process easier.

For brokers building a home-based lending business, the model starts to click. One funded deal can lead to accountants, consultants, insurance agents, payroll contacts, and business owners inside the same network. The commission is one payday. The relationship can produce many.

Anyone curious about the earning mechanics behind funded deals can review this overview of business loan broker salary and commission structure. The short version is simple. Brokers don't get paid for activity. They get paid for funded outcomes.

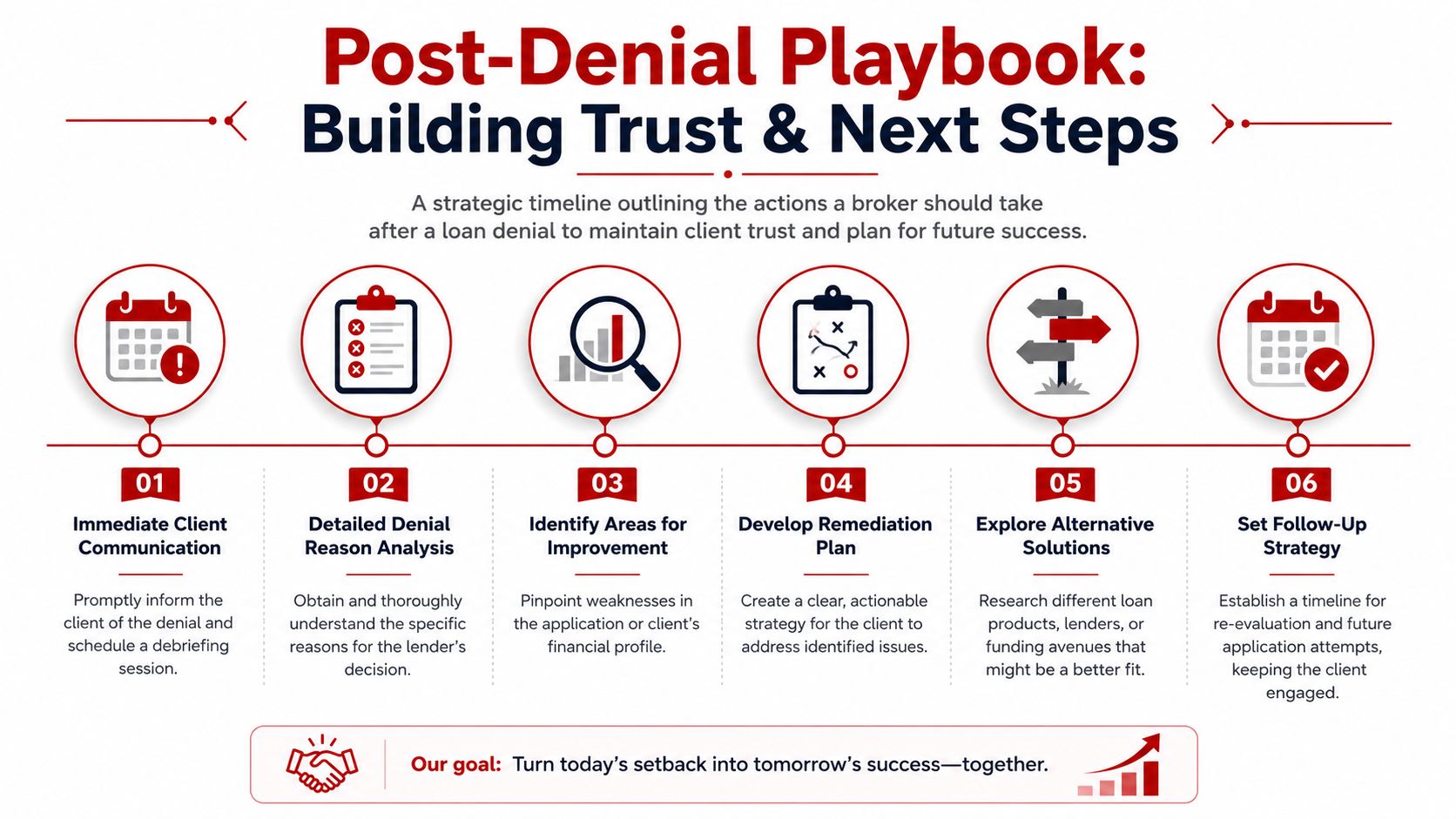

Handling Denials and Building Client Trust

A denial is not the end of the relationship

A lot of brokers treat a denial like a dead lead. That's amateur thinking. Denials often create the strongest long-term clients, because the borrower discovers whether the broker was a transaction chaser or a real advisor.

A rejection usually means one of three things. The timing was wrong, the file was weak, or the lender fit was off. None of those automatically means the business is unfundable forever. It means the next move has to be deliberate.

Over 50% of entrepreneurs who are denied successfully reapply after making targeted improvements, and one useful recovery pattern is waiting 3 to 6 months, showing steady deposit behavior, and returning with an organized folder of updated documents (American Fidelity Bank on what to do after a business loan denial).

The recovery plan clients actually need

Generic advice doesn't help here. “Improve your credit” is not a plan. A useful denial response gives the client a sequence.

A broker should walk the client through:

- Denial reason: document weakness, unstable cash flow, amount requested, timing, or lender mismatch

- What can be corrected now: reporting errors, missing records, outdated statements, messy explanations

- What must improve over time: deposit consistency, cleaner account activity, stronger financial presentation

- When to re-engage: not emotionally, but when the file is materially better

That last point matters. Reapplying too quickly with the same weaknesses usually produces the same answer.

The denial meeting should end with a checklist and a date, not with vague encouragement.

A practical follow-up cadence might include a document refresh, statement review, and a lender strategy reset once the business has established more stable patterns. If the original ask was too aggressive, the next structure may need to be smaller or aimed at a different product. If the problem was documentation quality, the next file should be cleaner than the first one by a mile.

Such instances foster trust. The broker who stays engaged after a no often becomes the first call when the business is ready again. More than that, the borrower remembers who told the truth.

Business Lending Blueprint teaches people how to build a profitable, home-based business as a business loan broker by mastering exactly this kind of process work. It doesn't provide loans. It provides training, systems, and mentorship for people who want to help business owners secure funding through alternative lenders while building a flexible, referral-driven business of their own. To see how the model works, watch the free training from Business Lending Blueprint or schedule a strategy session.