A large share of aspiring loan brokers starts in the same place. They understand term loans, lines of credit, maybe equipment financing, but they keep hearing startup founders talk about funding rounds, dilution, runway, and board control as if it's a separate universe.

It isn't. It's a niche. And for the broker who learns it, venture debt for startups can become a highly valuable specialty.

The appeal is obvious. These clients often need expert guidance, they value introductions to the right capital sources, and they can become strong referral partners over time through attorneys, CPAs, consultants, and investor networks. For someone building a home-based brokerage, that creates a compelling path: remote work, relationship-driven deal flow, and a service that business owners indeed need when equity capital is expensive or hard to close.

Table of Contents

- The Hidden Funding Opportunity for VC-Backed Startups

- Understanding Venture Debt Mechanics and Terms

- Identifying the Ideal Client for Venture Debt

- Weighing the Pros and Cons for Your Clients

- A Broker's Playbook for Navigating the Deal Process

- How You Earn Commissions in the Venture Debt Space

- Start Your Journey as a High-Value Broker Today

The Hidden Funding Opportunity for VC-Backed Startups

A consultant might spend years helping small businesses find working capital and still miss what's happening one layer up. A software startup raises a major equity round, starts hiring fast, expands product development, and then needs more capital before the next raise. The founders don't want to sell more ownership too soon. The bank won't underwrite it like a stable cash-flow business. That gap is where venture debt enters.

For a broker, this is more than a startup finance topic. It's a niche with meaningful deal size, strong referral potential, and clients who often need specialized guidance instead of generic lending advice.

The market is large enough to matter. The U.S. venture debt market has grown at an annual rate of 17% since 2014, with deal volume reaching a peak of $38.8 billion in 2021, according to Founderpath's venture debt market overview. That long-term growth matters because it shows this isn't a fringe product. It has become part of how venture-backed companies finance growth.

A trainee broker should also notice what makes these clients different. Many founders aren't trying to replace equity. They're trying to use debt strategically so they can delay dilution, hit milestones, and negotiate the next round from a stronger position. That creates room for a broker who can translate lender language into founder language.

Practical rule: The broker who understands both startup urgency and lender discipline becomes far more useful than the broker who only quotes rates.

Some founders won't raise from venture capital at all, and some will blend debt with other capital paths. A useful perspective on that broader financing environment appears in Fundl on raising capital without VC, especially for brokers who want to understand where venture debt fits inside a wider funding conversation.

Startup funding options also widen beyond venture-backed companies, which is why many brokers study small business funding for startups alongside venture debt. The broker who can spot when a founder is a true venture debt fit, and when they aren't, protects time, credibility, and future referrals.

Understanding Venture Debt Mechanics and Terms

Venture debt is easiest to understand as a funding booster shot attached to an earlier equity raise. It doesn't usually replace that raise. It supplements it.

A founder closes a round, deploys capital, begins scaling, and wants added runway without giving up another chunk of the company. The lender steps in with a structured loan based less on traditional collateral and more on the startup's backing, progress, and ability to raise future capital.

Why founders use it

The basic structure is straightforward. Venture debt is typically a term loan representing 20% to 35% of a startup's most recent equity round, with annual interest rates usually ranging from 8% to 15%, and most deals include warrants for the lender to purchase 0.5% to 2% of the company's equity, as explained in Carta's guide to venture debt financing.

That means if a startup recently closed a $10 million equity round, a broker can often expect venture debt sizing to land in a related band rather than some random number. That alone helps filter conversations quickly.

Founders often get confused by one phrase: non-dilutive. It sounds like debt has no ownership impact. That's not fully accurate. The core capital is debt, not equity, but warrants still give the lender a small equity upside. A broker should explain that early, clearly, and without jargon.

For readers who want a founder-friendly breakdown of how term sheets are discussed in growth-stage settings, venture debt terms for founders adds helpful context.

Typical venture debt terms at a glance

Venture debt also shares some DNA with subordinated and structured capital, which is why understanding mezzanine capital definition can sharpen a broker's ability to explain hybrid financing logic.

| Term | Typical Range / Structure |

|---|---|

| Loan size | 20% to 35% of the most recent equity round |

| Interest rate | 8% to 15% annually |

| Warrant coverage | 0.5% to 2% of company equity |

| Loan term | Usually 2 to 4 years |

| Payment structure | Often starts with an interest-only period before principal repayment |

A new broker doesn't need to memorize every term sheet variation on day one. The broker needs to understand the pattern.

- Sizing follows the raise: Lenders often anchor the debt amount to the latest equity round.

- Pricing reflects risk: These companies may be growing quickly but still lack the stable cash flow a conventional bank wants.

- Warrants align upside: The lender takes loan risk and wants a small share of future success.

- Repayment structure buys time: Early interest-only periods give the startup room to deploy capital before heavier repayment starts.

Founders usually don't need a lecture on capital structure. They need a broker who can say, in plain language, what the debt does, what it costs, and what it could help them avoid.

Identifying the Ideal Client for Venture Debt

Not every startup should take venture debt. Some shouldn't touch it at all.

That's where many inexperienced brokers go wrong. They hear “startup” and “funding need” and assume there's a match. In reality, lenders look for a narrow profile. The broker who understands that profile can pre-qualify fast, avoid weak submissions, and protect lender relationships.

What lenders want to see

The clearest starting point comes from SVB's overview of venture debt qualifications. Lenders typically want a startup that has raised at least $4M in a single equity round, has backing from reputable venture capital firms, and maintains 12+ months of organic cash runway. They also underwrite based on the borrower's ability to raise future capital, not just current cash flow.

That last point is the one new brokers often miss.

Traditional small business lending often asks, “Can this company repay from operations today?” Venture debt often asks, “Will this company remain financeable, supported, and investable long enough to refinance, raise again, or grow into the obligation?” That's a different underwriting mindset.

How a broker should pre-qualify

A practical screen usually starts with five questions:

- Equity support: Has the company already closed a meaningful institutional round?

- Investor quality: Are recognized venture investors backing the company?

- Runway position: Does the startup have enough organic runway before adding debt?

- Use of proceeds: Can management explain exactly how the debt helps reach the next milestone?

- Future raise logic: Is there a credible story for the next round or another repayment path?

A broker should listen closely to how the founder answers. Strong candidates usually sound focused. They know what milestone the debt supports, what progress they've made since the last raise, and why now is the right time to take on debt.

Broker lens: The ideal client doesn't just need cash. The ideal client can explain how debt helps create a stronger next financing event.

Weak candidates tend to show one or more problems. The cap table may be shaky. The investor base may be thin. The runway may already be tight. Or management may want debt because they don't want dilution, without a realistic plan to service the obligation.

The broker's job isn't to force a fit. It's to spot one.

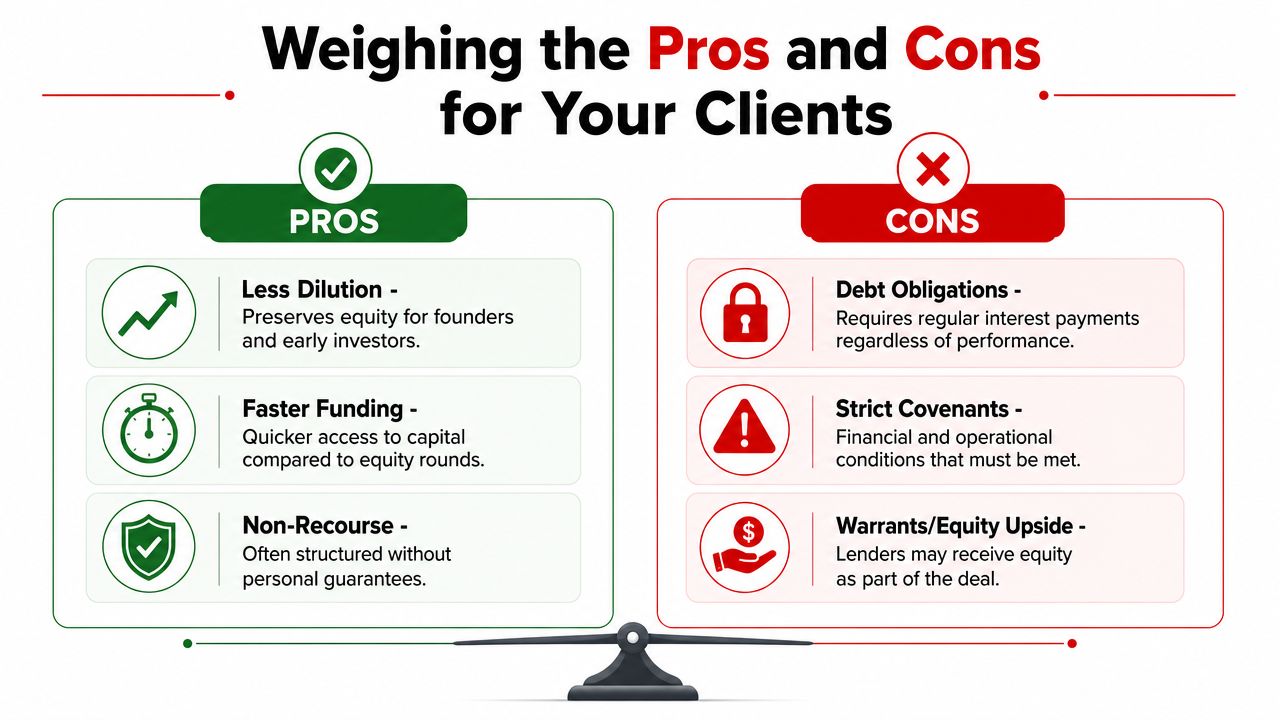

Weighing the Pros and Cons for Your Clients

Good brokers don't pitch venture debt as magic. They frame it as a strategic tool with tradeoffs.

That balanced posture builds trust fast, especially with founders who've already heard simplistic claims about “cheap non-dilutive capital.” Venture debt can be valuable, but only if the startup has enough traction, planning, and discipline to use it well.

Where venture debt helps

The main attraction is control over dilution. A founder can add capital without immediately selling more shares, reshaping board dynamics, or reopening valuation debates before the company is ready.

It can also buy time. Extra runway can help management reach a product milestone, revenue milestone, hiring target, or market expansion point before the next equity process starts. In the right case, debt gives the company negotiating room.

There's also speed and focus. Debt discussions can center on structure, investor support, and milestones, rather than reopening every strategic debate that often appears in a full equity raise. For brokers serving startup clients, that creates a concrete advisory role.

Some founders compare venture debt with other non-bank or flexible capital options before deciding. For example, ClaimKit's R&D financing insights can help frame how specialized financing supports growth when companies are balancing cash needs against future value creation.

Where deals go sideways

The cost can be more serious than founders expect. In high-interest environments, the effective annual cost of venture debt, including PIK interest and warrants, can exceed 12–15%, according to Customers Bank's discussion of startup venture debt. A broker should make sure the client weighs that cost against the benefit of extending runway.

That's where real advisory value shows up. A founder may focus on “no new dilution today” and underweight fixed repayment obligations, covenant pressure, fees, and warrant impact.

A broker should also help the founder compare venture debt with adjacent capital products. Some companies may be better served by structures tied more directly to recurring revenue or operating performance, which is why understanding what is revenue-based financing can sharpen the recommendation.

- Best-case use: Debt funds a clear path to a near-term milestone that improves the next financing outcome.

- Risky use: Debt covers a weak business model, masks a fundraising problem, or postpones hard decisions.

- Broker value: Strong brokers don't just place capital. They pressure-test fit, structure, and timing.

Venture debt is most helpful when it solves a timing problem. It becomes dangerous when it tries to solve a viability problem.

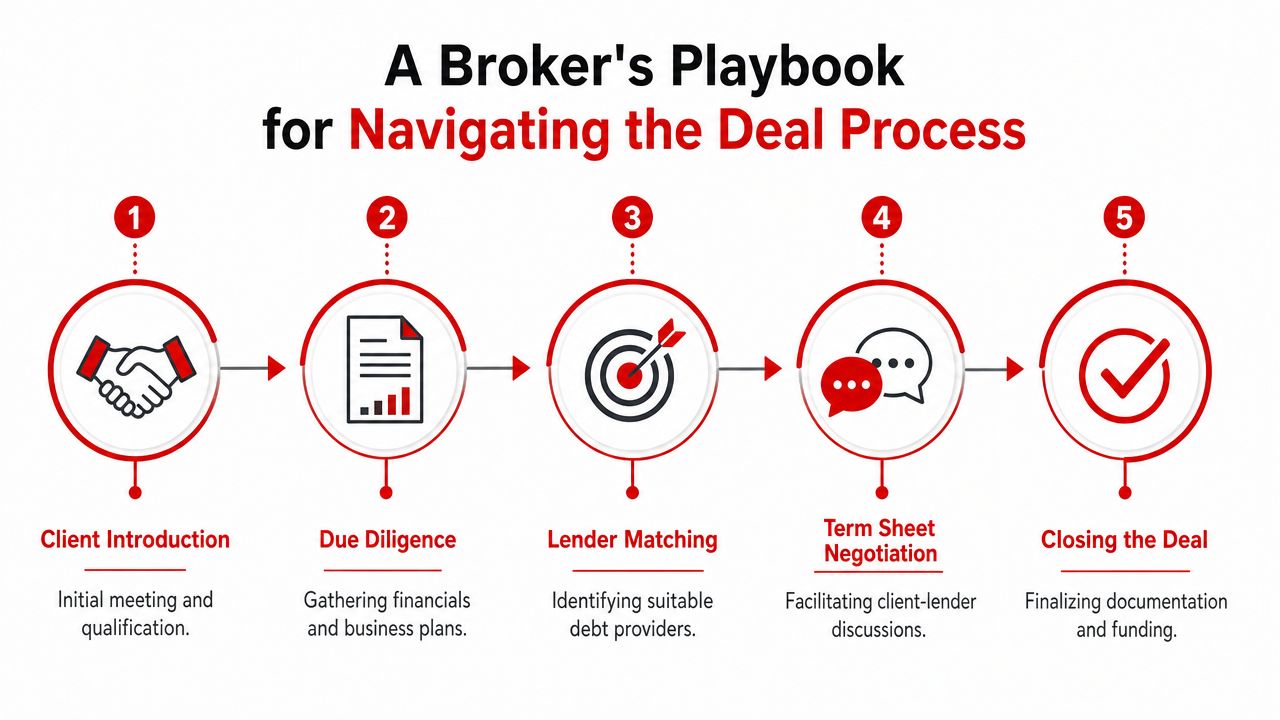

A Broker's Playbook for Navigating the Deal Process

Most venture debt deals feel complex only until the broker understands the sequence. Once the workflow is clear, the process becomes manageable and repeatable.

The strongest brokers rarely chase these opportunities through random outreach. They build a referral web around the people already close to the startup. That includes venture investors, startup attorneys, fractional CFOs, CPAs, and strategic consultants. These relationships matter because venture debt is usually introduced when a company is already in an active financing conversation.

How the process usually unfolds

A practical workflow often looks like this:

Initial qualification

The broker checks recent equity history, investor backing, runway, and use of proceeds.Package preparation

The broker gathers the story behind the numbers. Lenders want financials, but they also want context. What milestone is the company chasing, and why does the debt improve the odds?Lender matching

Not every lender likes the same stage, sector, or risk profile. Broker judgment matters here.Term sheet review

At this stage, confusion spikes. Founders often focus on the headline rate and miss other economic or structural terms.Closing coordination

Legal, diligence, and document follow-through become the broker's discipline test.

A broker who wants broader context on how technology is changing capital access can also study digital lending platforms to better understand where automation helps and where specialized advisory work still matters most.

Where broker value is highest

Timing is one of the most overlooked levers. Many founders assume they should take debt immediately after an equity round. But JPMorgan's guidance on venture debt timing notes that taking it 6–9 months later, after some revenue traction has been proven, can yield 15–20% better terms because the startup has partially de-risked the next capital raise.

That single insight can separate a transactional broker from a strategic one.

The broker also adds value by slowing the founder down at the right moment. A rushed deal can hide covenant issues, unrealistic draw expectations, or misalignment between debt maturity and the likely next financing event.

Field note: The best term sheet isn't always the one with the lowest quoted rate. It's the one the client can live with if growth takes longer than expected.

A clean process helps:

- Set expectations early: Founders should know what documents lenders will request and why.

- Translate lender questions: Startup operators often answer strategically when the lender needs an underwriting answer.

- Track friction points: Delays usually appear around diligence, legal review, and unclear use of proceeds.

- Stay close to referrals: The broker who communicates well earns the next introduction.

How You Earn Commissions in the Venture Debt Space

This niche attracts brokers for a simple reason. The loan sizes are large enough that even one funded transaction can matter.

Compensation usually comes from origination economics tied to the funded loan amount. The exact structure depends on the lender relationship, the deal, and the broker's agreement, so a broker should discuss compensation with precision and document it properly. What matters operationally is that venture debt deals tend to justify meaningful advisory work because the capital itself is substantial and the client expects hands-on guidance.

Why these deals are attractive to brokers

A broker isn't just forwarding an application. The broker is shaping the fit, preparing the narrative, managing expectations, and guiding the client through a specialized process. That makes venture debt one of the clearer examples of where expertise creates value.

It also fits a strong business model for someone building a remote brokerage:

- Relationship-driven deal flow: Referrals from attorneys, CPAs, and consultants can compound over time.

- Low physical overhead: The work can be done from a home office with calls, document review, and lender coordination.

- Higher-value positioning: Specialized knowledge can separate a broker from generalists chasing commodity deals.

- Repeat introductions: One well-served founder can lead to investor, advisor, and peer referrals.

This is especially attractive for professionals already serving businesses in adjacent roles. A CPA, consultant, insurance professional, or agency owner may already know companies that need capital introductions. Adding lending knowledge can turn those conversations into a new revenue stream without requiring a complete career reset.

How to build repeatable deal flow

The better long-term play isn't to hunt random founders one by one. It's to become known in a small network as the broker who understands difficult growth-stage funding situations.

That means building credibility with:

- Venture-side advisors: They often hear about funding gaps before lenders do.

- Transactional professionals: Attorneys and finance professionals see the company's structure up close.

- Growth consultants: They hear when hiring, expansion, or product plans are running ahead of available cash.

- Past clients: A founder who trusts a broker often sends the next introduction.

A business built this way can be flexible, remote, and scalable. It doesn't rely on hype. It relies on becoming useful to people who regularly encounter financing needs and want a dependable specialist to send those deals to.

Start Your Journey as a High-Value Broker Today

Venture debt for startups sits at an interesting intersection. It's complex enough that many brokers avoid it, but practical enough that a trained broker can learn to identify the right clients, structure conversations correctly, and guide deals with confidence.

That creates an opening for the person who wants more than commodity lead chasing.

A broker who understands this niche can serve founders who care a great deal about dilution, timing, runway, and control. That broker can also build valuable referral relationships with the professionals around those founders. For someone looking for a recession-resistant, home-based business, that combination is powerful. The work is remote-friendly, relationship-based, and scalable through repeatable systems.

Opportunity isn't limited to one product. Venture debt is one specialized lane inside a broader lending business. Once a broker learns how to evaluate fit, communicate clearly, and manage capital introductions professionally, those skills transfer across many forms of alternative business finance.

That's why training matters. The person entering this industry doesn't need to guess through lender criteria, client conversations, referral strategy, or deal structure. A proven blueprint can shorten the learning curve and help a new broker build a real business around solving funding problems for business owners.

Business Lending Blueprint teaches everyday people how to build a profitable, home-based business by becoming a business loan broker. It doesn't provide loans. It provides the training, systems, mentorship, and lender access that help brokers serve clients across alternative funding products, including startup financing. Readers who want a flexible, scalable, referral-driven business should watch the free training or schedule a strategy session with Business Lending Blueprint.