A broker usually meets revenue-based financing for the first time in a familiar situation. A business owner has real sales, a real growth plan, and a real need for capital, but the bank still says no. The company may be growing fast, collecting monthly subscriptions, or processing steady online sales, yet it doesn't own much equipment, real estate, or other hard collateral.

That gap shows up everywhere in modern small business lending. Digital-first companies often look healthy from a revenue perspective while still failing the old underwriting model. For an aspiring broker, that isn't a dead end. It's an opening. The broker who understands what revenue based financing is, when it works, and when it doesn't can step in with a funding solution that fits how these businesses operate.

Table of Contents

- The Modern Funding Gap RBF Was Born to Fill

- What Is Revenue Based Financing at Its Core

- How RBF Mechanics and Repayment Actually Work

- The Advantages and Hidden Risks of RBF

- RBF vs Term Loans vs Equity Financing

- Which Businesses Are a Perfect Fit for RBF

- Your Playbook for Brokering RBF Deals

The Modern Funding Gap RBF Was Born to Fill

A software company lands more customers every month. An e-commerce brand keeps turning inventory and needs cash to reorder faster. A marketing agency with retainers wants working capital to hire before the next wave of contracts hits. These aren't distressed businesses. They're often healthy, but they're hard to place with lenders that prefer collateral, long operating history, or a more conventional balance sheet.

That's the funding gap revenue-based financing was built to fill.

Why traditional lending misses modern businesses

A bank often looks for fixed repayment capacity, hard assets, and a borrower profile that fits a narrow box. Many newer companies don't fit that box even when revenue is consistent. Their strength sits in recurring sales, customer retention, and cash flow velocity, not in trucks, buildings, or heavy equipment.

That creates a practical opportunity for brokers. Instead of asking, "Why was this deal declined?" the better question is, "What product matches this revenue model?"

Practical rule: When a business has predictable top-line performance but weak collateral, a broker should start thinking about cash-flow-based products, not forcing a term loan that was never a fit.

Revenue-based financing is no longer a niche concept. One market estimate put the global market at $6.4 billion in 2023 and projected $178.3 billion by 2033 at a 39.4% CAGR, according to Allied Market Research's revenue-based financing market outlook. That doesn't mean every client needs RBF. It does mean brokers can't afford to ignore it.

Why this matters to a broker's business

For a broker building a home-based advisory business, RBF solves two problems at once.

- It broadens placement options. A declined bank client isn't automatically a lost client.

- It fits growth-focused owners. Many founders care about keeping ownership.

- It supports referral relationships. Accountants, consultants, and agencies regularly meet clients who need capital tied to revenue, not collateral.

A broker who understands this product becomes more than a rate shopper. That broker becomes a translator between the old lending world and the businesses that need funding today.

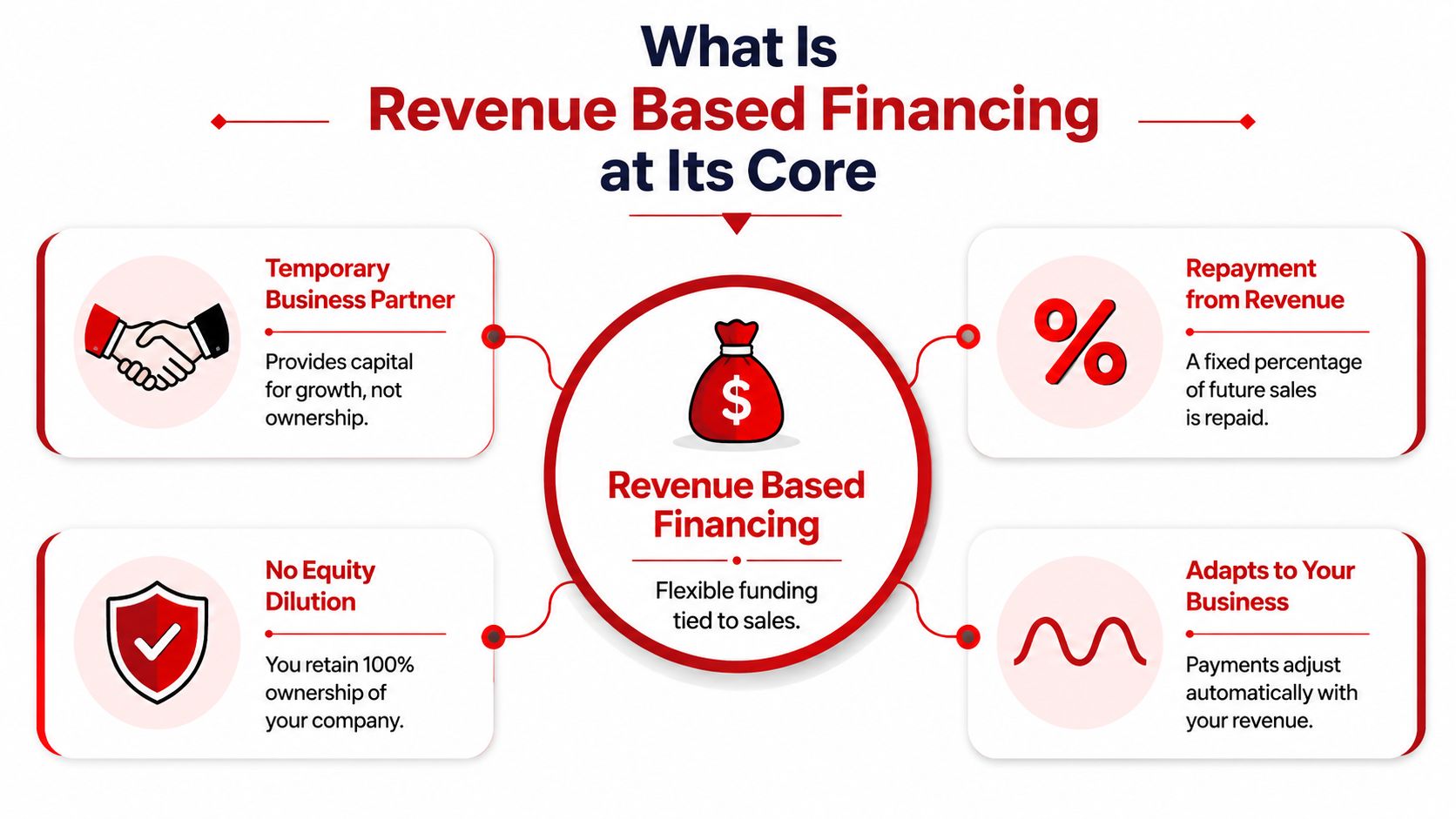

What Is Revenue Based Financing at Its Core

At its simplest, Revenue Based Financing is capital a business receives upfront in exchange for a fixed share of future revenue. The business doesn't give up ownership. It also doesn't make the same fixed payment every month the way it would with a standard amortizing loan.

The easiest way to explain what is revenue based financing to a client is this. It works like a temporary funding partner tied to sales. If revenue rises, repayment moves faster. If revenue slows, repayment shrinks with it.

The plain-English definition brokers should use

A clean broker explanation sounds like this:

A funder gives the business working capital now. In return, the business agrees to remit a percentage of future revenue until a pre-agreed total amount has been repaid.

That framing matters because clients often confuse RBF with either a loan or an investor buy-in. It shares features with both, but it isn't the same as either one.

Here are the core traits that make RBF distinct:

- Repayment comes from revenue. The remittance is tied to sales rather than a fixed installment.

- Ownership stays with the founder. The business isn't selling equity to get the capital.

- The total payoff is defined upfront. The deal ends when the agreed repayment amount is satisfied.

- Cash flow pressure can flex. Strong months move the balance down faster. Softer months reduce the remittance.

For business owners trying to understand revenue sharing more broadly, this guide to business growth with revenue sharing gives useful context around how revenue-linked models operate.

Why this structure resonates with growth companies

RBF tends to make sense faster when the client already understands top-line performance. Brokers who need a simple refresher on that concept can point to this explanation of top-line revenue and what it means for funding conversations.

A founder usually hears two immediate benefits in the RBF structure:

- No dilution. The owner keeps control.

- No rigid fixed payment. The remittance moves with actual business activity.

That doesn't make it cheap money or easy money. It makes it structurally aligned with companies whose sales patterns are more predictable than their month-to-month free cash flow.

How RBF Mechanics and Repayment Actually Work

A founder agrees to the advance in ten minutes, then stalls when the repayment discussion starts. That is where brokers either gain confidence or lose the deal. If you cannot explain how money comes out of the business, the client starts treating RBF like a black box.

The structure usually comes down to two numbers: the revenue share percentage and the repayment cap.

The two levers in a typical RBF deal

In a standard structure, the funder collects an agreed share of revenue until the business repays a preset total amount. That total payoff is often expressed as a multiple of the original advance, as outlined in Drexel's explanation of the rise of revenue-based financing.

Here is the clean way to frame it for a client:

| Deal component | What it means |

|---|---|

| Revenue share | The percentage of sales remitted to the funder |

| Repayment cap | The total amount the business agrees to repay |

| Funding amount | The upfront capital advanced to the business |

Use a simple example. If a business receives $100,000 and agrees to a 1.5x cap, the total repayment is $150,000. If the revenue share is 10%, the company remits 10% of eligible revenue until that $150,000 obligation is satisfied.

For a broker, that distinction matters. The client is not just asking, "How much am I getting?" They are asking, "How fast does this come off my top line, and what does that do to cash flow?"

What the client feels month to month

The easiest explanation is the most accurate one. Remittance rises when sales rise. Remittance falls when sales fall. The obligation ends once the agreed total payoff is met.

That creates a very different borrower experience than a fixed installment product.

- In stronger months, more revenue goes to repayment, so the balance burns down faster.

- In softer months, the remittance amount shrinks with sales.

- The payoff timing can move around, which helps businesses with uneven revenue but can make planning harder if the owner expects a fixed end date.

That last point is where newer brokers miss the fundamental trade-off. Flexible remittance helps with volatility, but it can also make forecasting less precise. A disciplined owner will want to see how this payment sits beside payroll, rent, inventory, and current debt. That is why brokers should review the client's full obligation stack, not just the new advance. This guide to reading a debt schedule for funding analysis is a good reference for that step.

Good brokers do not stop at the advance amount. They test whether the repayment method fits the client's revenue pattern and margin profile.

How to explain total cost without confusing the client

Clients often ask for the rate because they are used to term loans. Fair question. The cleaner answer is to walk them through total dollars out, not force the structure into language that does not fit.

Use this sequence:

- Start with the amount advanced

- Show the total amount to be repaid

- Explain the agreed revenue share

- Model a few payoff timelines based on current sales trends

That approach does two things. It keeps the math clear, and it tells the client you know how to structure deals, not just sell them.

For brokers building a book of RBF business, this is the habit that matters most. Explain the mechanics in plain language, tie them to the client's revenue cycle, and show the repayment pressure before the contract goes out. That is how you place better deals and keep referral partners sending you the right clients.

The Advantages and Hidden Risks of RBF

Revenue-based financing is easy to oversell if a broker only talks about flexibility. It's also easy to dismiss if a broker only talks about cost. The right approach is balanced. Good brokers use RBF when the structure fits and avoid it when the revenue profile only looks good on the surface.

Where RBF earns its place

The strongest advantages are practical, not theoretical.

- Ownership stays intact. Founders don't have to give away part of the company.

- Payments move with sales. That matters for businesses with uneven monthly revenue.

- Approvals can move quickly. Many providers use live business data rather than a long traditional underwriting cycle.

- The product fits growth uses. Inventory, marketing, hiring, and working capital often line up well with this type of funding.

For the right business, those benefits are meaningful. A company with strong recurring revenue may prefer flexible revenue remittance over a rigid installment that ignores seasonal swings.

Where brokers need to slow the client down

RBF repayment comes off the top line. That single fact changes everything.

AltCap notes that for thin-margin businesses, daily or weekly withdrawals of up to 8% of revenue can still be painful during a downturn, and in that situation the product can feel more like a variable tax on sales than a cushion, as explained in AltCap's discussion of revenue-based financing trade-offs.

That is the question serious clients ask in real life. What happens in a bad month?

If overhead stays fixed while revenue drops, a flexible remittance can still hurt. Flexible doesn't mean harmless.

The bad-month test

A broker should pressure-test every RBF deal with three simple questions:

- Are margins healthy enough? Revenue alone doesn't pay the bills. Margin matters.

- How volatile are sales? A predictable subscription business behaves very differently from a business with erratic receipts.

- How often is the remittance collected? Daily, weekly, and monthly collections feel very different operationally.

A client may love the idea of no dilution and faster access to capital. That still doesn't make RBF suitable. When margins are thin, overhead is stubborn, and revenue whipsaws, this product can tighten the business instead of helping it.

The broker's reputation grows when bad-fit deals are declined early, not when every lead gets pushed into funding.

RBF vs Term Loans vs Equity Financing

Most owners don't choose funding in a vacuum. They choose among trade-offs. The broker's job is to simplify those trade-offs without flattening the differences.

At a structural level, revenue-based financing sits between traditional debt and equity. It's not as rigid as a term loan, and it doesn't require ownership dilution like equity. But that middle ground only helps when the client's business model supports it.

The fastest way to frame the choice

Capchase explains that unlike a term loan with a fixed amortization schedule, RBF repayment flexes with sales, and total repayment caps often fall in the 1.4x to 2.5x range of principal in some implementations, which is what creates the funder's return without a stated interest rate in the usual sense, according to Capchase's breakdown of revenue-based financing structure.

That difference drives the comparison below.

| Funding type | Best fit | Main strength | Main trade-off |

|---|---|---|---|

| Revenue-based financing | Predictable revenue businesses that want non-dilutive capital | Flexible repayment tied to sales | Can pressure margin because repayment comes from revenue |

| Term loan | Businesses that qualify for conventional debt and can handle fixed payments | Clear amortization and often lower-cost structure | Less flexible when revenue dips |

| Equity financing | Businesses pursuing long-term growth and willing to trade ownership for capital | No direct repayment schedule | Loss of ownership and control |

How brokers should guide the decision

A term loan often wins when the business has strong documentation, stable cash flow, and the ability to support fixed debt service. Brokers who evaluate that path should understand basic debt service coverage ratio calculation and how lenders use it.

Equity tends to fit a very different conversation. The owner isn't just buying capital. The owner is taking on partners.

RBF tends to fit when the owner values control, needs speed, and has revenue patterns that support a top-line remittance better than a fixed monthly debt obligation.

The product choice shouldn't start with what can get approved. It should start with what the business can carry without breaking its cash flow.

Which Businesses Are a Perfect Fit for RBF

Not every business with sales is a fit for revenue-based financing. To quickly distinguish themselves, a strong broker does not ask only whether a client needs money. The broker asks whether the company's revenue profile, margins, and data trail match the lenders that are active in this space.

The business models lenders tend to like

Recent market coverage shows that RBF providers increasingly target software and recurring-revenue firms, often sizing advances relative to ARR or MRR and using direct data connections through bank, Stripe, or Xero-style integrations to make decisions in days, according to Uncapped's review of how revenue-based finance is being underwritten.

That tells a broker a lot about present-day fit.

The strongest candidates often share these traits:

- Recurring or repeatable revenue. Subscription businesses, retainers, and repeat-purchase models are easier to underwrite.

- Clean digital records. Lenders like businesses that can connect revenue and banking data directly.

- Solid gross margin. Top-line remittance is much easier to carry when margin isn't compressed.

- A clear use of funds. Inventory, marketing, growth hires, and expansion working capital usually make more sense than plugging chronic losses.

The red flags that should change the recommendation

A business may look busy and still be a poor RBF candidate.

Watch for these issues:

- Revenue is inconsistent. If sales swing hard with no pattern, repayment becomes harder to model.

- Margins are too thin. A revenue share can squeeze operations fast.

- Books are messy. If statements don't tell a clean story, underwriting slows or falls apart.

- The business needs long-term restructuring, not growth capital. RBF isn't a rescue product.

Some businesses that don't fit RBF may still fit adjacent products. For example, companies waiting on customer invoices may be better served through options discussed in this guide to accounts receivable lenders and cash-flow-based funding paths.

A broker's quick qualification lens

Before sending a file out, a broker should ask:

- Does the company have revenue that can be tracked cleanly?

- Is the revenue predictable enough to support a remittance model?

- Are margins strong enough to survive payment off the top line?

- Is the owner trying to preserve equity?

- Is the use of funds tied to growth rather than survival?

If the answers are mostly yes, RBF deserves a serious look. If the answers are mixed, the broker should widen the product search instead of forcing the fit.

Your Playbook for Brokering RBF Deals

A broker doesn't get paid for knowing definitions. A broker gets paid for turning product knowledge into funded deals that help clients. Revenue-based financing can do that well when the process is disciplined.

Step one through step three

Start with the intake. The broker should understand the client's revenue pattern, margin profile, current obligations, and exact use of funds. If the client can't explain where the capital will go, the deal usually isn't ready.

Then gather clean documentation. Bank statements, revenue reports, processor activity, and financials need to line up. RBF underwriting often depends on data visibility, so missing or inconsistent records can kill momentum.

Next, educate the client before offers arrive. Explain the revenue share, the cap, and how collections affect cash flow. If a client only hears "flexible payments" and never hears "paid from top-line revenue," the broker hasn't done the job.

Step four through step six

After that, it's a matching and negotiation exercise.

- Match the file to the right lenders. Not every provider wants the same revenue profile.

- Compare structure, not just approval. The remittance method and total payoff matter more than a flashy advance.

- Set expectations after funding. Clients need to know how repayment timing affects operations.

For brokers building a referral-driven business, process compounds. Accountants, consultants, agencies, and fractional finance professionals all meet businesses that need capital but don't fit a bank box. For firms that want a practical framework for prospecting and outreach, ReachLabs.ai's B2B strategies offer useful ideas on building consistent lead flow.

One structured way to learn how to source, package, and place these deals is through Business Lending Blueprint, which trains brokers to work through alternative lending products with a lender network and process guidance.

A broker's edge isn't access to one product. It's the ability to identify fit fast, explain trade-offs clearly, and place the client with the right capital solution.

A broker who can do that with revenue-based financing isn't just learning a funding product. That broker is building a durable advisory business around a real need in the market.

Business owners are looking for funding guidance that matches how their companies run, and brokers who understand products like revenue-based financing are in a strong position to help. To learn how to build a remote, referral-driven business loan brokerage and work deals across alternative lending products, watch the free training or schedule a strategy session with Business Lending Blueprint.