A new broker usually sees the same pattern within the first few weeks of talking to business owners. The company looks healthy on the surface. Revenue is moving. Customers are recognizable. The owner sounds busy, not desperate.

Then the bank balance tells the full story.

A staffing firm is waiting on invoices from large clients. A distributor shipped product weeks ago but still hasn't collected. A service company is landing work and growing, yet scrambling to make payroll because its customers pay on long terms. That gap between delivery and payment is where accounts receivable lenders become one of the most profitable niches a broker can learn.

This isn't a side product. It's a repeat need in B2B. The broker who understands how to spot trapped receivables, package the file correctly, and place it with the right lender stops sounding like a generalist and starts acting like a specialist. Specialists get trusted faster, close more often, and build stronger referral relationships.

Table of Contents

- The Hidden Cash Flow Crisis in B2B Companies

- Understanding the Two Types of AR Financing

- How Accounts Receivable Lenders Think

- Your Broker Playbook for Placing AR Deals

- Anatomy of a Funded Deal and Your Commission

- Scripts Compliance and Referral Partnerships

- Launch Your AR Lending Business This Month

The Hidden Cash Flow Crisis in B2B Companies

A broker doesn't need to hunt for businesses with no sales. The better opportunity is the business with sales that aren't turning into cash fast enough.

That problem is widespread. In the U.S., 55% of all B2B invoiced sales are overdue, and another survey found 39% of invoices are paid late, according to accounts receivable cash collection statistics. When a company has to wait on its customers, payroll, inventory, fuel, rent, and vendor payments don't wait with it.

What the broker is really solving

The owner usually describes the issue as “cash flow.” A good broker hears something more specific. Cash is trapped in receivables.

That distinction matters. A company with unpaid invoices from viable commercial customers may not need a term loan. It may need access to the value it has already earned. That's why accounts receivable financing works so well for B2B companies operating on longer terms, especially those navigating net 60 payment terms and invoicing strategy.

Practical rule: When a business says revenue is strong but timing is tight, the broker should ask for an aging report before discussing broader loan products.

Strong brokers also notice a second layer. Businesses that struggle with collections often have process issues, not just financing issues. If invoice approvals are slow or paperwork is inconsistent, funding friction increases. For clients trying to tighten their back office, a practical resource like this guide to choosing invoice automation tools can help them reduce avoidable delays before or alongside financing.

Why this niche pays brokers well

AR deals solve immediate pain. Owners feel the problem weekly, sometimes daily. That creates urgency without forcing the broker into hype.

The niche also produces repeat business. Once a company starts financing receivables, the facility can revolve with new invoices, and the broker who structured the first deal often becomes the first call when the business needs another working capital solution. That creates a more durable book of relationships than chasing one-off borrowers who only shop rate.

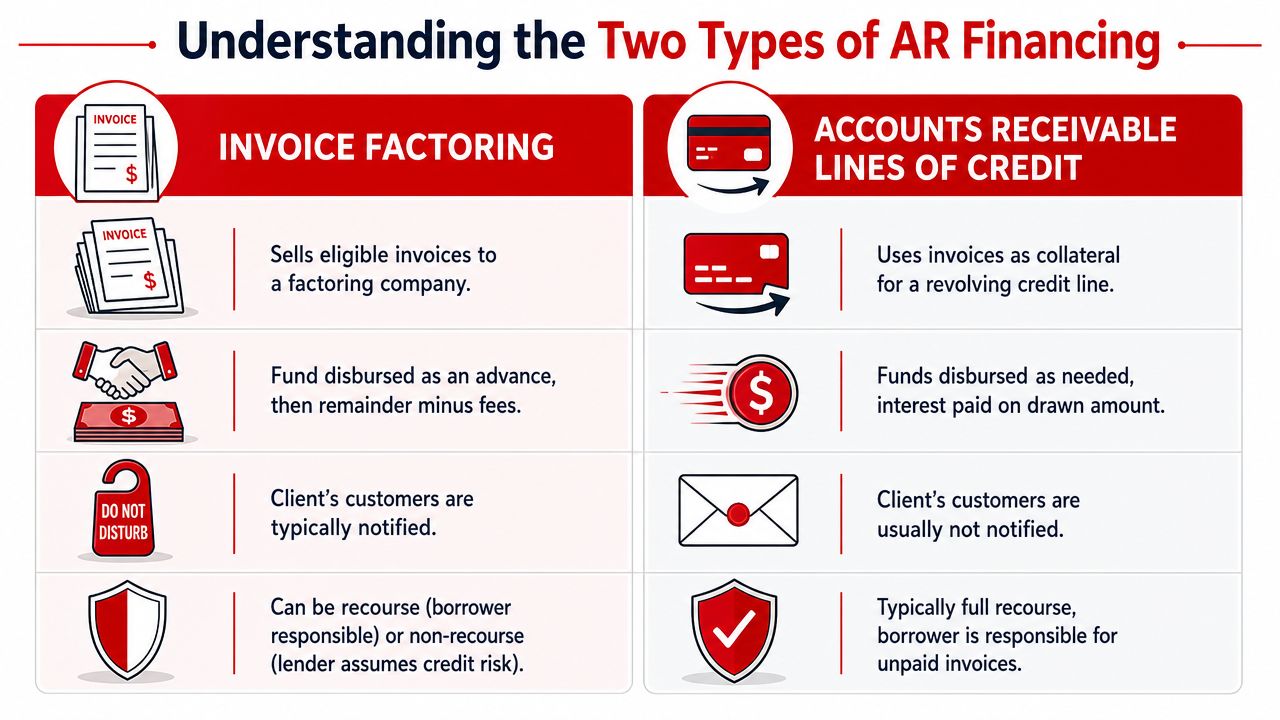

Understanding the Two Types of AR Financing

A broker needs a clean explanation for the two core structures. If that explanation gets muddy, the client gets confused and the lender loses confidence.

Accounts receivable are a large asset class, not some fringe balance-sheet item. Research cited by this overview of accounts receivable financing notes that receivables make up about 12% of total assets for U.S. public firms. That helps explain why lenders build products around them. The same source notes that in factoring, the lender often advances about 80% to 90% of invoice value.

Factoring is a sale of invoices

Factoring is the easier product for a new broker to visualize. The business sells eligible invoices to a factor. The factor advances cash up front, then handles collection and remits the remainder after fees and reserves are reconciled.

A simple analogy helps. Factoring is closer to selling an asset for immediate liquidity. The business trades some control and some economics for speed and access.

Factoring tends to fit borrowers that:

- Need fast liquidity: The company can't wait for long underwriting cycles.

- Can tolerate customer notice: The account debtor is usually instructed to pay the factor.

- Value operations support: Some borrowers want the factor involved in collections and back-office discipline.

- Have weak bankability: The file may still be solid if the customers paying the invoices are credible commercial obligors.

An AR line is a revolving loan against invoices

An accounts receivable line of credit works differently. The borrower keeps the invoices on its books and uses them as collateral for a revolving facility. The company draws against eligible receivables, repays as collections come in, and borrows again as fresh invoices are generated.

This feels more like a secured working capital line than a sale. The client usually keeps more control over customer relationships, collections, and communication.

An AR line often makes more sense when:

- Customer relationships are sensitive: The borrower wants to keep collections in-house.

- Reporting is stronger: The business can produce clean aging, customer data, and regular borrowing base support.

- Management wants flexibility: The company may not need to finance every invoice.

- The business is growing steadily: A revolving structure can scale with invoicing volume.

A broker doesn't need to force one product. The broker needs to match the structure to the borrower's customer base, reporting quality, and tolerance for lender involvement.

The mistake new brokers make is pitching both as if they're interchangeable. They aren't. One is closer to monetizing invoices through sale mechanics. The other is borrowing against those invoices while retaining ownership and more control.

How Accounts Receivable Lenders Think

Most bad submissions fail before underwriting even starts. The file reaches a lender, and within minutes the lender can tell the broker doesn't understand receivables risk.

Why banks often pass

Traditional banks often don't like lending against receivables alone because the collateral can be hard to value cleanly. This discussion of factoring and accounts receivable notes that most banks avoid loans secured solely by accounts receivable for that reason. The same source says typical advances are 60% to 80% of invoice value, depending on invoice quality, customer reliability, and credit history.

That bank hesitation creates room for alternative lenders. But alternative doesn't mean careless. These lenders are disciplined because they aren't relying primarily on the borrower's story. They're relying on the invoices getting paid.

What lenders actually review

A new broker should think like a lender before sending the file out. The lender isn't asking, “Is this owner convincing?” The lender is asking, “Will these customers pay these invoices without drama?”

Here are the issues that drive decisions:

- Invoice quality: Clean invoices tied to completed work are more financeable than invoices with open questions, vague descriptions, or missing backup.

- Aging: Older receivables raise concern quickly. Stale paper often means collection issues, disputes, or customers with stretched payment behavior.

- Customer reliability: A borrower with average financials can still get attention if its account debtors are strong and pay predictably.

- Concentration: If one customer represents too much of the pool, the lender's risk rises sharply.

- Dilution: Credits, offsets, returns, and disputes can reduce what looks collectible on paper.

- Industry friction: Staffing, transportation, distribution, manufacturing, and B2B services can all work, but each comes with its own documentation and collection patterns.

The borrower is the applicant. The customer is the repayment source. That single idea changes how AR deals should be screened.

A broker who wants to improve submissions should learn to read supporting financials, not just collect them. For brokers who need help sharpening that lens, working alongside or learning from experienced Financial Analysts can improve how they review aging trends, customer exposure, and reporting quality before a file reaches a lender.

There is also a subtle distinction between cash flow underwriting and receivables underwriting. A term lender may care heavily about ratios such as debt service coverage ratio calculation. An AR lender cares more about collateral behavior. Both matter in commercial finance, but they don't sit in the same seat.

The lender's silent questions

Underwriters often don't say these questions out loud early in the process, but they're there:

| Lender question | Why it matters |

|---|---|

| Are the invoices legitimate and earned? | Unperformed work or incomplete delivery weakens collateral. |

| Do customers pay consistently? | Payment history often tells more than the borrower's pitch. |

| Are there disputes or offsets? | A disputed invoice isn't dependable collateral. |

| Is the aging report clean and current? | Sloppy reporting usually points to operational weakness. |

| Will the pool keep replenishing? | Lenders prefer collateral that refreshes through ongoing sales. |

When a broker can answer those questions before submission, approval odds improve and turnaround usually gets smoother.

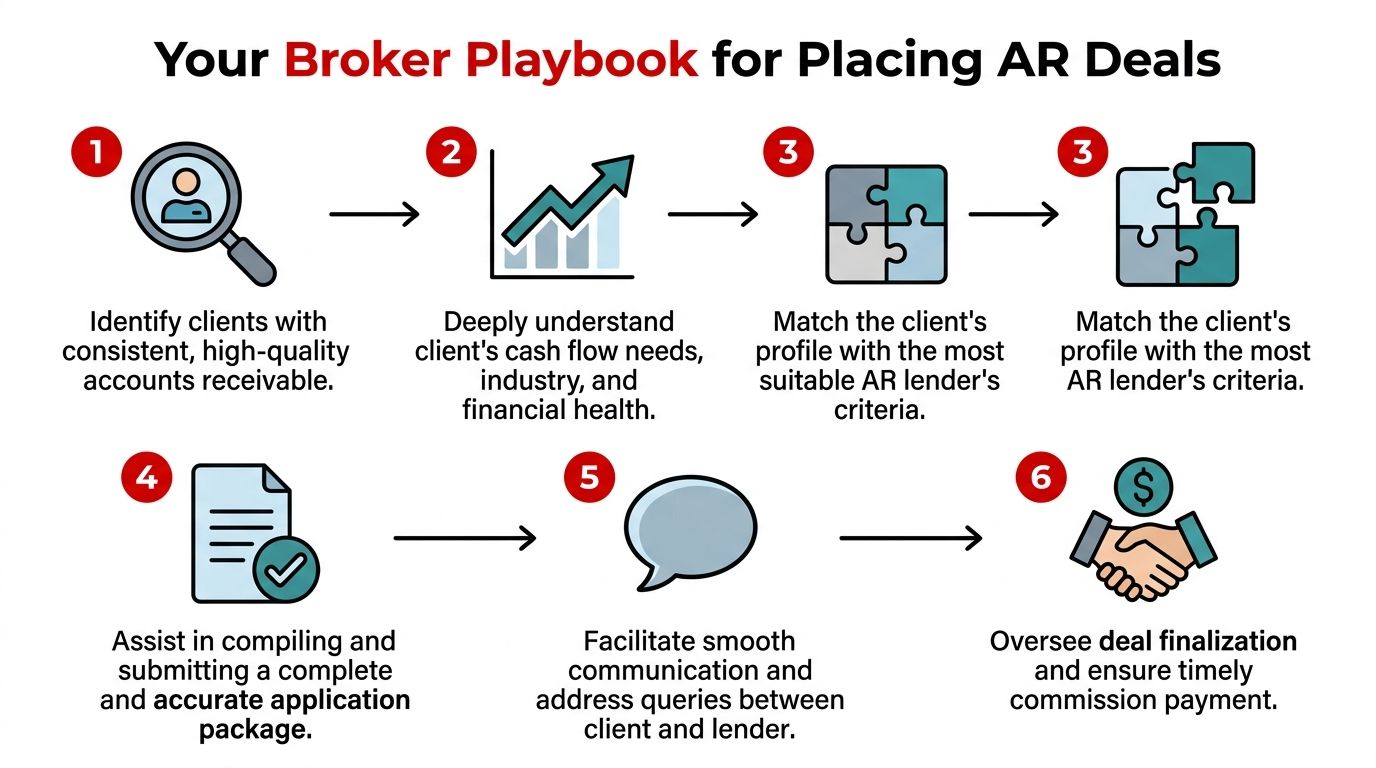

Your Broker Playbook for Placing AR Deals

A profitable AR practice doesn't come from blasting applications to every lender in a contact list. It comes from running the same disciplined process every time.

According to this explanation of accounts receivable financing structures, AR lenders underwrite the underlying obligor, not just the borrower. It also notes that many programs require invoices to be relatively recent, often under 90 days old, and may fund through a borrowing base that refreshes as new eligible invoices are generated. That tells the broker exactly what to look for before the first application goes out.

Start with the right prospect

Not every business with invoices is a fit. The best early targets are B2B companies that invoice commercial clients consistently and can document completed work or delivered product.

Useful questions on the first call include:

- Who pays the invoices? The broker needs to know whether the customers are businesses, government entities, or another type of payer.

- How old are the receivables? Fresh paper usually gets better attention than older balances.

- Are there recurring invoices or one-time projects? Revolving facilities work best when new invoices keep coming.

- Any disputes, offsets, or retention issues? These can kill eligibility fast.

- How concentrated is the customer base? One dominant payer can limit lender appetite.

- Does the owner want confidentiality or doesn't that matter? That answer helps separate line structures from factoring candidates.

A lot of wasted time disappears when the broker asks these questions first instead of after documents arrive.

Build the file before sending it out

The broker's real work starts after the prospect says yes. This niche rewards preparation.

The submission package usually works better when it includes:

- Current AR aging: This is the heartbeat of the deal.

- Customer list with balances: Lenders want to see who owes what.

- Sample invoices and backup: Proof of delivery, timesheets, signed acknowledgments, or purchase support often matter.

- Business bank statements: These help confirm operating behavior and collections.

- Basic company financials: Even when collateral drives the decision, the lender still wants context.

- Explanation of any anomalies: Credits, slow accounts, concentration, or unusual payment cycles should be explained up front.

If the borrower's internal paperwork is messy, the broker should slow down before shopping the file. The same goes for agreements with customers. When clients ask how to tighten documentation flow on their side, practical operations resources like how to automate contract management can help them reduce errors that later become underwriting objections.

A thin file creates questions. A clean file creates options.

Control the process through funding

Once the package is ready, the broker still shouldn't send it everywhere. Match the file to lenders that like the profile. A factoring-oriented lender and a collateral-line lender may look at the same borrower very differently.

During underwriting, the broker should stay close to four pressure points:

- Expectation setting: Tell the borrower what the lender is likely to ask for next.

- Speed: AR facilities can move quickly, but only if requests are answered quickly.

- Narrative: If there are older receivables, customer concentration, or timing quirks, frame them clearly instead of letting the underwriter guess.

- Product fit: If the borrower resists customer notice, don't push the file toward a structure that requires it.

The broker also needs to know when not to force AR financing. If the receivables are weak, disputed, or too irregular, another product may be better. Learning to pivot matters, especially for brokers who also place products like merchant cash advance offers and related funding solutions.

A disciplined process protects reputation. Lenders remember brokers who submit complete, honest files. So do referral partners.

Anatomy of a Funded Deal and Your Commission

A broker should understand the cash mechanics well enough to explain them without sounding scripted. The cleanest way to learn is to walk through one sample deal.

Assume a business has $100,000 in eligible receivables. The lender approves an 85% advance rate, which falls within the common market range described earlier in the article. The lender advances $85,000 up front and holds the remaining $15,000 as a reserve until the invoices are collected and final charges are reconciled.

Sample deal breakdown

| Metric | Amount | Description |

|---|---|---|

| Eligible receivables | $100,000 | Invoices the lender accepts into the facility |

| Advance rate | 85% | Percentage funded at closing |

| Initial advance | $85,000 | Cash provided to the client up front |

| Reserve held back | $15,000 | Amount retained pending collection and settlement |

| Fees | Varies by lender and file quality | Deducted based on the agreement |

| Final rebate | Reserve minus fees and adjustments | Released after customer payment and reconciliation |

The broker should explain one thing carefully. The reserve is not the borrower's profit. It's a holdback. Once the customer pays, the lender settles the account, deducts agreed charges, and remits the remaining balance.

That means the borrower shouldn't look only at the advance rate. The borrower also needs to understand reserve mechanics, recourse terms, customer notice, collateral eligibility, and how disputes affect funding availability.

Where the broker gets paid

Broker compensation depends on the lender agreement and structure. Some lenders pay on funded volume. Some pay on facility size. Some tie compensation to usage, renewals, or ongoing performance.

The practical lesson is this: the broker earns by placing a workable deal, not by quoting the highest theoretical advance.

If a broker can't explain reserve flow and lender fees in plain language, the client will lose confidence before documents are signed.

A useful habit is building a short written summary for the client after approval. That summary should list the advance, reserve, collection flow, and the borrower's responsibilities. It also helps to keep the client's broader obligations organized, especially when AR financing sits alongside other liabilities. A simple review of what a debt schedule is and how to use one can make those conversations cleaner.

Scripts Compliance and Referral Partnerships

AR financing becomes a real business when the broker stops relying on random inbound leads and starts building repeat referral channels.

CPAs, bookkeepers, fractional CFOs, payroll providers, and consultants often see the problem before the owner asks for financing. They notice rising receivables, delayed collections, and working capital stress inside the financials. A broker who can speak clearly about receivables becomes useful to them fast.

A simple partner script

This kind of outreach works because it's specific:

“A lot of B2B companies don't have a revenue problem. They have a timing problem because cash is tied up in unpaid invoices. When a client has strong receivables but strained working capital, there's often a financeable solution before they miss payroll or slow growth. If you'd like, a quick review of the aging report can show whether it's worth a conversation.”

That script avoids hype. It also avoids pretending every company is a fit.

A second version works well for warm introductions:

- For CPAs: “If a client is profitable on paper but cash-poor because customers pay slowly, there may be a receivables facility that fits better than a broad cash flow loan.”

- For bookkeepers: “If the aging report keeps getting heavier while payroll pressure rises, send the file early. Early is easier than urgent.”

- For fractional CFOs: “If the business needs a working capital bridge tied directly to invoices, a lender match can often be evaluated quickly when reporting is clean.”

Compliance habits that protect the broker

This business rewards clarity and punishes loose language.

The broker should:

- Describe the role accurately: The broker is arranging financing, not giving legal or tax advice.

- Avoid promising approvals: No file is approved until the lender says so.

- Explain material terms carefully: Customer notice, recourse, reserves, and fees should never come as a surprise.

- Use lender documents correctly: Side promises and off-email explanations create trouble later.

- Document communications: A clean paper trail protects everyone.

Clients don't mind complexity as much as they mind surprise. Most problems in brokerage come from poor expectation setting, not from the product itself.

The referral relationships worth building

The best partners are professionals who already see the books and hear the owner's concerns. They don't need a lecture on what invoices are. They need confidence that the broker can handle the deal professionally.

That trust builds when the broker:

- Responds fast

- Screens with integrity

- Doesn't force bad files

- Keeps partners updated

- Closes cleanly

A referral source who sends one good AR deal and sees it handled well often sends more. That's how a home-based brokerage stops feeling like side work and starts behaving like a business.

Launch Your AR Lending Business This Month

Accounts receivable financing is one of the clearest specialist lanes in commercial brokerage. The pain is real, the use case is easy to understand, and the broker who learns the underwriting logic can create value quickly for B2B owners.

It also has an advantage many new brokers miss. This product isn't only about speeding up cash. It can improve discipline around billing, collections, and customer quality. MIT Sloan research found that after a firm begins using accounts receivable financing, payment delays from customers fall sharply, as noted in this MIT Sloan discussion on receivables financing. That gives the broker a stronger message than “here's more capital.” The message becomes “here's a facility that may also improve how cash gets collected.”

That matters in any economy. Businesses still invoice. Customers still pay on terms. Owners still need to bridge the gap between earned revenue and available cash.

For the broker, that creates a practical path to a remote, referral-driven business. Learn how to identify the right files. Learn how lenders think. Build clean submissions. Stay honest about fit. Then repeat that process through accountants, advisors, and other referral partners who already serve B2B owners.

The brokers who do that don't need to chase every financing trend. They build around a recurring commercial problem and become known for solving it.

Business Lending Blueprint shows people how to build exactly that kind of referral-driven business loan brokerage from home. If this article made the accounts receivable niche click, the next step is to watch the free training at Business Lending Blueprint or schedule a strategy session to map out how to start placing deals, build lender relationships, and create a recession-resistant brokerage with a practical system.

Authored using Outrank tool