Most advice on how to start a mortgage lending company is too shallow. It makes the process sound like a checklist problem. Form the entity, get licensed, set up software, start originating.

That advice gets people in trouble.

The hard part usually isn't learning the steps. The hard part is surviving the capital drain, the licensing friction, and the slow march from setup to funded volume. For many founders, the smarter move isn't to build a direct mortgage operation first. It's to enter lending through a broker model that's faster to launch, lighter on overhead, and far easier to run from home.

For entrepreneurs who want a practical path into lending, especially those who value flexibility, referral income, and remote work, the better question isn't just how to start a mortgage lending company. It's which lending business model makes sense for the founder's capital, experience, and timeline.

Table of Contents

- The Reality of Starting a Mortgage Lending Company

- A Leaner Path The Business Loan Broker Model

- Your Blueprint for Launching a Business Loan Brokerage

- Building Your Referral Engine Without Cold Calling

- Essential Technology for a Modern Remote Brokerage

- From Launch to Scale Your Path Forward

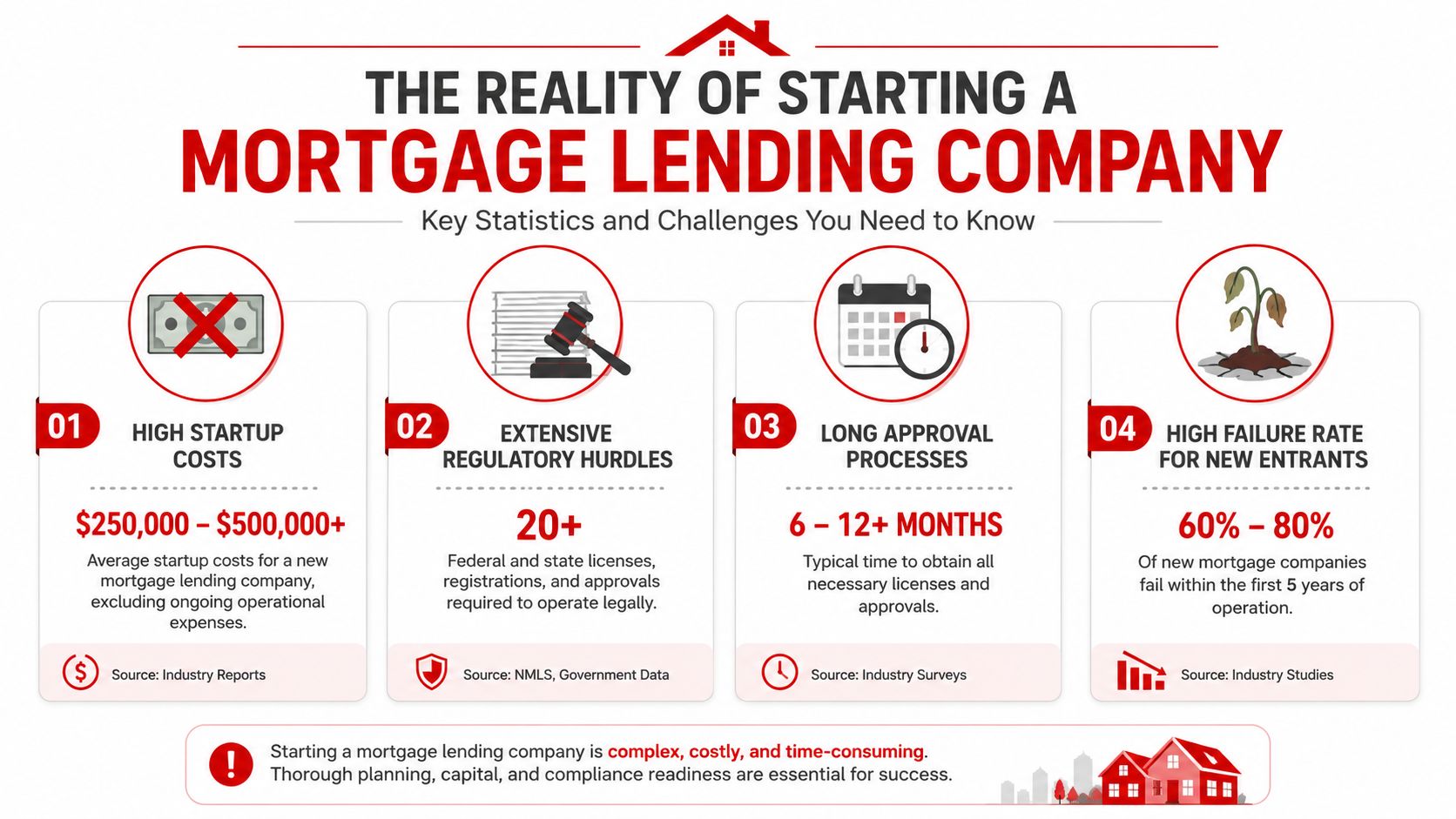

The Reality of Starting a Mortgage Lending Company

Starting a mortgage lending company sounds ambitious. In practice, it is one of the hardest ways to enter lending.

A direct lender is not just selling loans. The founder is building a regulated operation with licensing, compliance controls, documented policies, reporting processes, funding relationships, and enough cash to survive a slow start. That burden hits before the business produces predictable revenue.

The market is bigger and tougher than most founders expect

Scale works against inexperienced entrants.

Back in 2024, analysts at the National Community Reinvestment Coalition found that the home-purchase market was heavily concentrated, with a small group of lenders producing a disproportionate share of total volume, based on its analysis of top home-purchase lenders in 2024. Use that as historical context, not as a current 2026 snapshot.

The practical takeaway is simple. New founders are not entering a wide-open market. They are stepping into a field where established operators already have capital, referral channels, investor relationships, and tested systems.

Practical rule: Treat mortgage lending as an operations-heavy financial business. Sales matter, but infrastructure decides whether the business survives.

Licensing is not a formality

A lot of startup content treats licensing like paperwork you knock out on the way to launch. That advice gets people in trouble.

The smarter sequence is to choose the business structure first, map the state requirements, complete the required education and testing, and build your compliance process before you originate a single file. In mortgage lending, the license type changes the burden. So does the state.

That distinction matters because broker, lender, and loan originator paths are not interchangeable. They carry different approval standards, background checks, surety bond rules, sponsorship requirements, and operating limits. Founders who are still comparing models should review these licensing considerations for working without a license as a business loan broker before they commit to the wrong structure.

Here is the short version:

| Path | What changes |

|---|---|

| Mortgage broker | Lower operating burden than direct lending in many states, but still regulated and state-specific |

| Mortgage lender | Higher compliance load, stronger capital requirements, and more operational exposure |

| Loan originator | Personal licensing, testing, and employer sponsorship may apply |

Cash flow breaks more founders than paperwork

This is the part people underestimate.

The startup bill is not limited to filing fees and licenses. You also need money for payroll, systems, marketing, legal setup, insurance, and enough reserve cash to carry the business while closings are still inconsistent. A mortgage operation can look legitimate long before it becomes financially stable.

That is why new founders fail in predictable ways:

- They hire before revenue is steady. Payroll arrives whether loans close or not.

- They buy systems before defining the workflow. The tools are in place, but nobody uses them well.

- They chase volume before tightening compliance. More files create more errors.

- They confuse approval with readiness. A license gives permission to operate. It does not create a functioning business.

Can a mortgage lending company work? Yes.

Is it the right first move for someone who wants to build a profitable lending business without taking on heavy fixed costs and regulatory drag from day one? Usually not.

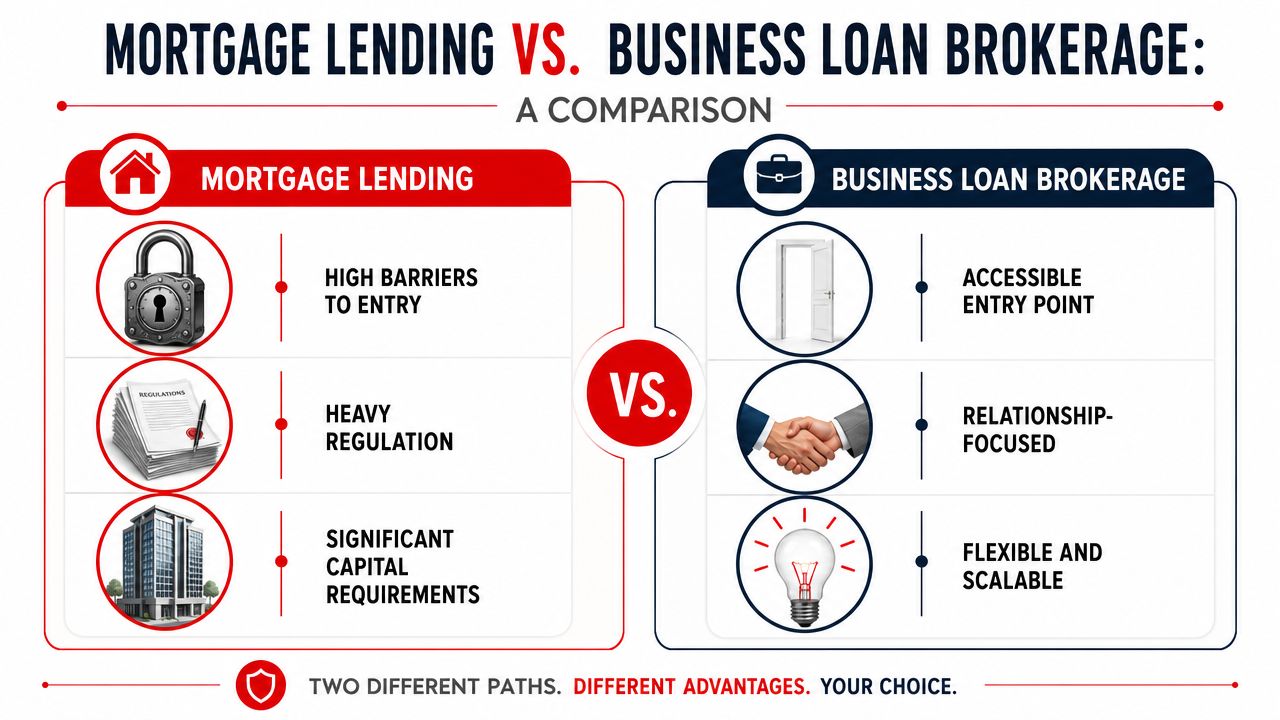

A Leaner Path The Business Loan Broker Model

The better entry point for most founders is simpler. Become a business loan broker first.

That choice changes almost everything. It lowers fixed overhead, reduces operational drag, and lets the founder focus on what creates revenue: finding qualified borrowers, structuring deals, and building referral channels.

The structure matters more than the idea

A lot of people say they want to “start a lending company” when what they really want is a profitable business in the lending space. Those aren't the same thing.

A direct lender has to carry a larger compliance and capital burden. A broker sits in the middle, connects borrowers to funding sources, and earns commissions for creating the match. That model is often the more rational starting point because the founder isn't trying to build the entire machine on day one.

According to this overview of mortgage broker licensing differences by state, the business model chosen, broker, lender, or loan originator, dramatically changes startup requirements, fees, bond obligations, and experience prerequisites. In many markets, the broker model is the more capital-efficient and faster-to-revenue option.

Why the broker model fits more founders

A business loan brokerage is attractive for a simple reason. It aligns with how many modern entrepreneurs want to work.

- Remote-first: it can be run from a home office.

- Relationship-driven: referral partners can generate repeat deal flow.

- Flexible: the founder can start narrow, then expand products later.

- Scalable: one person can begin lean, then add support once volume justifies it.

This is also a cleaner fit for people coming from sales, consulting, tax, banking, insurance, real estate, or client service backgrounds. Those people already understand trust, follow-up, and lead management. They usually don't need a giant operation. They need a reliable process and access to funding partners.

The smartest founders don't ask which model sounds bigger. They ask which model gets to stable revenue with the least drag.

What this looks like in practice

A business loan broker typically works with business owners who need capital for operations, growth, equipment, expansion, working capital, or short-term cash flow gaps. Instead of funding the deal directly, the broker pre-screens the client, gathers the file, identifies fit, and places the request with an appropriate lender.

That creates several advantages over the direct mortgage path:

| Category | Direct mortgage path | Business loan broker path |

|---|---|---|

| Capital pressure | Higher | Lower |

| Operational burden | Heavier | Lighter |

| Speed to launch | Slower | Faster |

| Lifestyle flexibility | More constrained | More remote-friendly |

This isn't about cutting corners. It's about choosing a business model that matches reality.

A founder who starts as a broker can learn deal structure, borrower qualification, lender guidelines, and referral development without taking on the full weight of a direct lending platform. That's a strategic advantage, not a compromise.

Your Blueprint for Launching a Business Loan Brokerage

Skip the early obsession with branding. A brokerage gets traction from process, lender fit, and disciplined intake. The founders who treat this like a real operating business from day one usually get to revenue faster and waste less time fixing preventable mistakes.

Start with a documented business model

A broker model works best when the setup order is clear. Define the market first. Then document your offer, intake standards, workflow, and compliance requirements before you start bringing in applications. Guidance from the U.S. Small Business Administration on writing a business plan before launch supports that sequence, and it fits brokerage far better than the capital-heavy direct lending route.

Write down the rules of the business.

A founder should document:

Target client profile

Choose a borrower type you can understand and serve well. Contractors, e-commerce companies, medical practices, restaurants, and professional service firms all borrow for different reasons and qualify under different standards.Deal filters

Set minimum standards for time in business, revenue profile, use of funds, and document readiness. Clear filters protect your time and keep bad-fit files out of the pipeline.Offer set

Start narrow. Working capital, equipment financing, term loans, or lines of credit are enough to begin. Breadth sounds impressive, but focus closes deals.Intake workflow

Decide what happens from first contact to submission. That includes your pre-screen questions, required documents, follow-up cadence, and handoff points.

If you want a more structured walkthrough, review this guide on becoming a loan broker and starting a lending business.

Build lender access before marketing hard

You do not have a brokerage until you can place deals.

Start with a small lender panel that matches the files you plan to bring in. A huge list is not the goal. You need enough coverage to handle clean borrowers, borrowers with uneven cash flow, and borrowers who fall outside bank credit standards without sending every file everywhere.

Use a practical screen for lender relationships:

- Product fit: choose funding partners that match the borrower profiles you want.

- Submission clarity: work with lenders that state document requirements and approval standards clearly.

- Turn times: favor partners that give predictable updates and realistic timelines.

- Broker support: choose groups that help resolve stipulations instead of going silent mid-file.

That discipline matters. Bad lender fit creates rework, stalls deals, and burns referral trust.

Create a clean workflow from day one

New brokers usually struggle because their process is loose. They chase every lead, collect incomplete files, and submit deals before they are ready. That creates friction at every step.

Use a simple operating sequence:

| Stage | What happens |

|---|---|

| Inquiry | Prospect comes in through referral, content, or direct outreach |

| Pre-screen | Basic fit is checked before a full document request |

| File build | Statements, business details, and support documents are collected and organized |

| Placement | File is sent to the funding source that fits the deal |

| Follow-through | Conditions, updates, and closing steps are managed until funding |

A good workflow also makes growth easier later, especially when you start scaling your referral programs. Referral volume only helps if your intake and follow-up can handle it without turning into chaos.

For founders who do not want to build the entire system from scratch, Business Lending Blueprint provides training, lender access, and process guidance for launching and operating a business loan brokerage. It does not do the work for you. It shortens the learning curve and helps you avoid expensive beginner mistakes.

Building Your Referral Engine Without Cold Calling

The brokers who last don't spend every week hunting strangers. They build a referral engine that keeps bringing the right prospects into the pipeline.

That's not theory. It's how a lean brokerage stays efficient.

The best brokers build channels not campaigns

Industry guidance for brokerage success emphasizes referral infrastructure. Building relationships with real estate agents, builders, and financial advisors, supported by a CRM, is a key part of durable growth, according to this guidance on standardizing intake and partnerships in lending.

In the business lending world, the equivalent partners often include:

- CPAs and tax professionals: they see cash flow problems early.

- Consultants and agencies: their clients often need growth capital.

- Bankers with declined borrowers: they can't fund every deal, but they know who still needs help.

- Commercial real estate and equipment professionals: financing conversations happen naturally around larger purchases.

A strong broker doesn't walk into those relationships asking for favors. The broker shows up with a clear value proposition. Fast response, honest qualification, clean communication, and reliable follow-through.

A referral partner will keep sending deals only if the broker protects that relationship like an asset.

A simple partnership rhythm that compounds

A practical referral engine usually starts with a small handful of partners. One CPA, one consultant, one banker contact, one local business service provider. The broker checks in consistently, shares what kinds of files are a fit, follows up fast, and reports outcomes cleanly.

That rhythm creates trust because the partner knows three things:

- The broker responds

- The broker doesn't waste client time

- The broker can explain what happened

One useful next step is to formalize the process with simple tracking and a repeatable partner experience. Teams that want to organize scaling your referral programs can use those principles to keep introductions from getting lost as the network expands.

A founder who wants to see how relationship-based deal flow can develop through networking can study this example of funding generated through a networking-driven approach.

What to track so referrals keep flowing

A referral engine works better when the broker measures behaviors, not vanity.

Useful items to track include:

| What to track | Why it matters |

|---|---|

| Active referral partners | shows whether the network is growing or shrinking |

| Introductions received | reveals who is actually producing |

| Qualified files | separates real opportunities from noise |

| Funding outcomes | helps the broker identify which channels fit best |

| Response time | directly affects partner confidence |

Cold calling can still produce conversations. It just rarely produces the kind of stable business that referral ecosystems create. A brokerage built on relationships is calmer, more credible, and easier to scale.

Essential Technology for a Modern Remote Brokerage

A remote brokerage doesn't need a bloated tech stack. It needs a functional one.

Too many new brokers buy software based on features they'll never use. The better move is to install a small set of systems that handle communication, document flow, follow-up, and visibility across the pipeline.

The minimum stack that actually matters

A modern brokerage usually needs four categories of technology.

- CRM system: this is the core record of every lead, referral partner, file, and follow-up task.

- Secure document collection: borrowers need a simple way to submit sensitive records without turning email into chaos.

- Internal workflow tracking: every file should have visible status, next steps, and assigned actions.

- Communication system: calls, email, and reminders need to be logged in one place whenever possible.

For founders building a lean online presence, virtual office and online business setup ideas can help shape the operational side of a home-based brokerage.

Keep the system simple enough to use

The best stack is the one the broker touches every day.

A useful rule is to design technology around the questions that come up constantly. Where is this file? What is missing? Who referred this client? Who needs a follow-up today? If the system answers those questions fast, it's doing its job.

For intake-heavy operations, it also helps to study ways to streamline form collection and borrower onboarding. Teams that want cleaner submission workflows can explore Orbit AI for finance for ideas on how financial service forms can be organized more efficiently.

Complexity doesn't make a brokerage look bigger. It makes response time worse.

A remote brokerage wins when the founder can open the dashboard, see every active file, and move the day forward without chasing information across five different places.

From Launch to Scale Your Path Forward

Those searching for how to start a mortgage lending company don't need a mortgage company. They need a realistic path into lending.

That distinction matters because the wrong model creates drag before revenue shows up. The right model creates momentum. A lean brokerage does that better for most founders, especially those starting from home, building part time, or transitioning out of another profession.

Scale comes from repetition not complexity

A brokerage scales well when it repeats a simple cycle. Attract the right clients. Pre-screen cleanly. Place deals with the right lenders. communicate clearly. Keep referral partners informed. Repeat.

That doesn't look flashy. It works.

As the brokerage matures, the founder can expand carefully. More referral partners. Better intake systems. A support hire. Broader funding products. Eventually, a small team. The mistake is trying to do all of that at once.

The opportunity is real if the model is right

The market is active enough to support disciplined operators. The U.S. Loan Brokers industry included over 18,800 businesses in 2026 and generated about $9.1 billion in revenue, according to the CFPB HMDA summary page referenced in the verified industry data. That doesn't guarantee success. It does confirm that brokering financing is a real business category, not a side-hustle fantasy.

The founders who build durable firms usually have three traits:

- They choose a model they can sustain

- They build systems before chasing scale

- They grow through partnerships, not random activity

For anyone thinking long term, it also helps to study broader ideas around growth models for community organizations because the strongest brokerages often grow through repeatable relationship systems, not one-off promotions.

A smart path forward is simple. Skip the ego of launching the biggest structure first. Start with the model that gets to revenue faster, keeps overhead lower, and allows the founder to learn the lending business by doing real deals.

Business Lending Blueprint shows aspiring brokers how to launch and scale a home-based business loan brokerage with training, lender access, and a referral-driven model built for remote work. To take the next step, watch the free training at Business Lending Blueprint or schedule a strategy session to see whether the broker model fits the business goals, background, and timeline.