A large share of small business conversations ends the same way. The owner needs capital, the bank says no, and the advisor in the room has no funding solution to offer. CPAs see it during tax season. Consultants see it during growth planning. Insurance agents, real estate professionals, bookkeepers, and salespeople hear the same frustration over and over.

That dead end is a business opportunity for a broker who understands unsecured business loans for startups.

This product isn't just another funding option to memorize. It's a practical entry point into alternative lending because it solves a common problem. Early-stage companies often don't own enough hard assets to pledge, but they still need capital for launch costs, hiring, marketing, inventory, and working capital. A broker who can explain the product clearly, pre-qualify the client accurately, and package the file properly becomes valuable fast.

Table of Contents

- The Untapped Opportunity in Startup Funding

- What Unsecured Startup Loans Really Mean

- Decoding Lender Requirements for Your Clients

- Explaining Loan Costs and Risks to Build Trust

- How to Coach Startups for Loan Approval

- Smart Alternatives When Unsecured Loans Are Not a Fit

- Your Broker Playbook for Landing Startup Deals

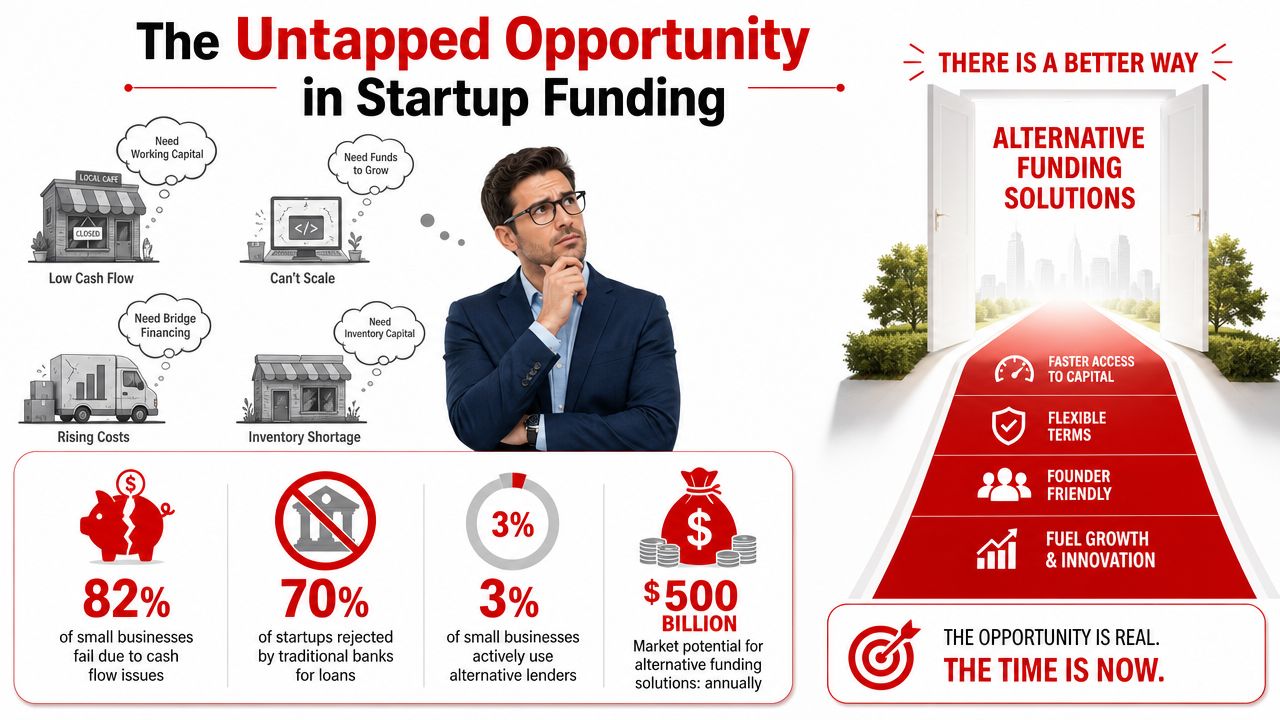

The Untapped Opportunity in Startup Funding

A founder walks out of a bank meeting with a decline letter, then calls the accountant, the consultant, or the agency owner they already trust and asks the crucial question: “Who can get this done?” That call often lands with someone sitting one relationship away from a brokerage business.

For a new broker, startup funding is not a fringe category. It is one of the cleanest entry points into recurring deal flow because early-stage companies ask for help before they understand their options, before they know which lenders fit, and before they present their file properly. The broker who can sort that out becomes valuable fast.

Why this niche is commercially attractive

Startup conversations produce more than one commission opportunity. A client may start with an unsecured working-capital request, come back later for a line increase, then send over a partner or vendor who also needs funding. Good brokers do not treat startup deals as one-off transactions. They build a pipeline around them.

A key advantage is positioning. Banks reject many young companies for thin time in business, limited collateral, inconsistent revenue, or incomplete financials. Alternative lenders may still review those files if the deal is framed correctly and the borrower matches the lender's risk appetite. That gap creates room for a broker with product knowledge and discipline.

Practical rule: If other advisors keep hearing “no” from traditional lenders, a broker can turn that rejected demand into paid placements.

Why advisors become strong brokers

Accountants, consultants, insurance agents, payroll reps, and B2B sales professionals already have the hard asset that matters at the start. They have access to business owners at the moment funding pain shows up. What they usually need is a better grasp of underwriting logic, lender segmentation, and packaging.

That is why learning how the alternative lending industry really works pays off so quickly. Once you understand how lenders price risk, review bank activity, and weigh founder strength against weak business history, startup files stop looking random. They become sortable.

Some founders will still search for early-stage funding through investor networks instead of debt. A broker should understand that path without confusing it with the product being sold. Equity helps companies that need patient capital and can trade ownership for runway. Unsecured business funding fits founders who need speed, want to avoid dilution, and can support repayment. Knowing the difference helps you keep credibility, protect referral relationships, and earn repeat business instead of forcing the wrong deal.

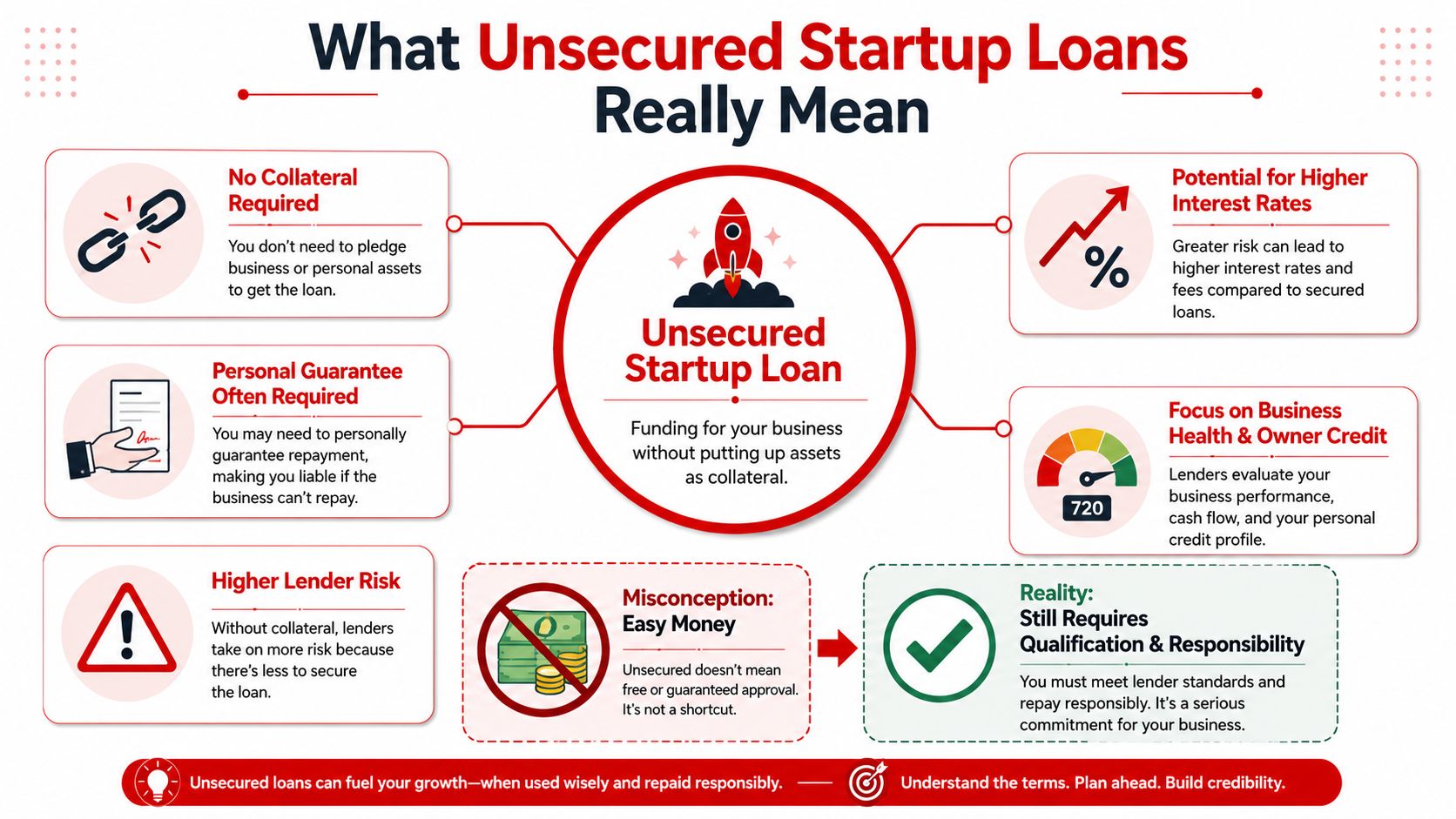

What Unsecured Startup Loans Really Mean

Most new brokers hear the word unsecured and assume it means low-friction funding with minimal downside for the borrower. That's not how lenders see it. In startup lending, unsecured usually means there's no specific hard asset pledged as collateral. It does not mean the founder has nothing at stake.

The better way to explain it to a trainee broker is simple. The lender is often backing the jockey, not the horse. The startup may be thin on assets, but the owner's credit profile, operating habits, business experience, and willingness to stand behind the obligation still matter.

What unsecured actually signals

A lender making an unsecured offer is accepting more recovery risk if the deal fails. Because of that, the lender usually looks harder at the founder and the company's ability to repay.

According to AMP Advance's guide to unsecured business funding, most search content treats unsecured as the main decision point, but lenders still commonly rely on a personal guarantee, credit score, revenue, and bank-statement underwriting. That misunderstanding creates a major opening for brokers. A broker who explains the underlying approval logic sounds credible immediately.

Unsecured doesn't mean consequence-free. It means the lender's protection shifts away from hard collateral and toward the borrower's promise, profile, and cash flow.

The conversation brokers need to lead

Clients often hear “no collateral” and stop asking better questions. A broker needs to move the discussion to key issues:

- What is personally at risk if the business defaults

- What documents support repayment ability

- How lender confidence gets built without equipment, real estate, or inventory

- Whether a blanket lien or personal guarantee is involved

Trust is gained through honest dealings. A broker who glosses over personal liability may get a signature, but won't build a lasting referral business. A broker who explains the paperwork plainly tends to keep the client, even when the answer is no.

For some startup owners, debt won't be the only path. It helps to understand adjacent capital strategies, including Credit for Startups' guide to non-dilutive funding, because borrowers often compare grants, cards, revenue-based capital, and unsecured loans in the same decision cycle. The broker's role is to clarify where unsecured debt fits and where it doesn't.

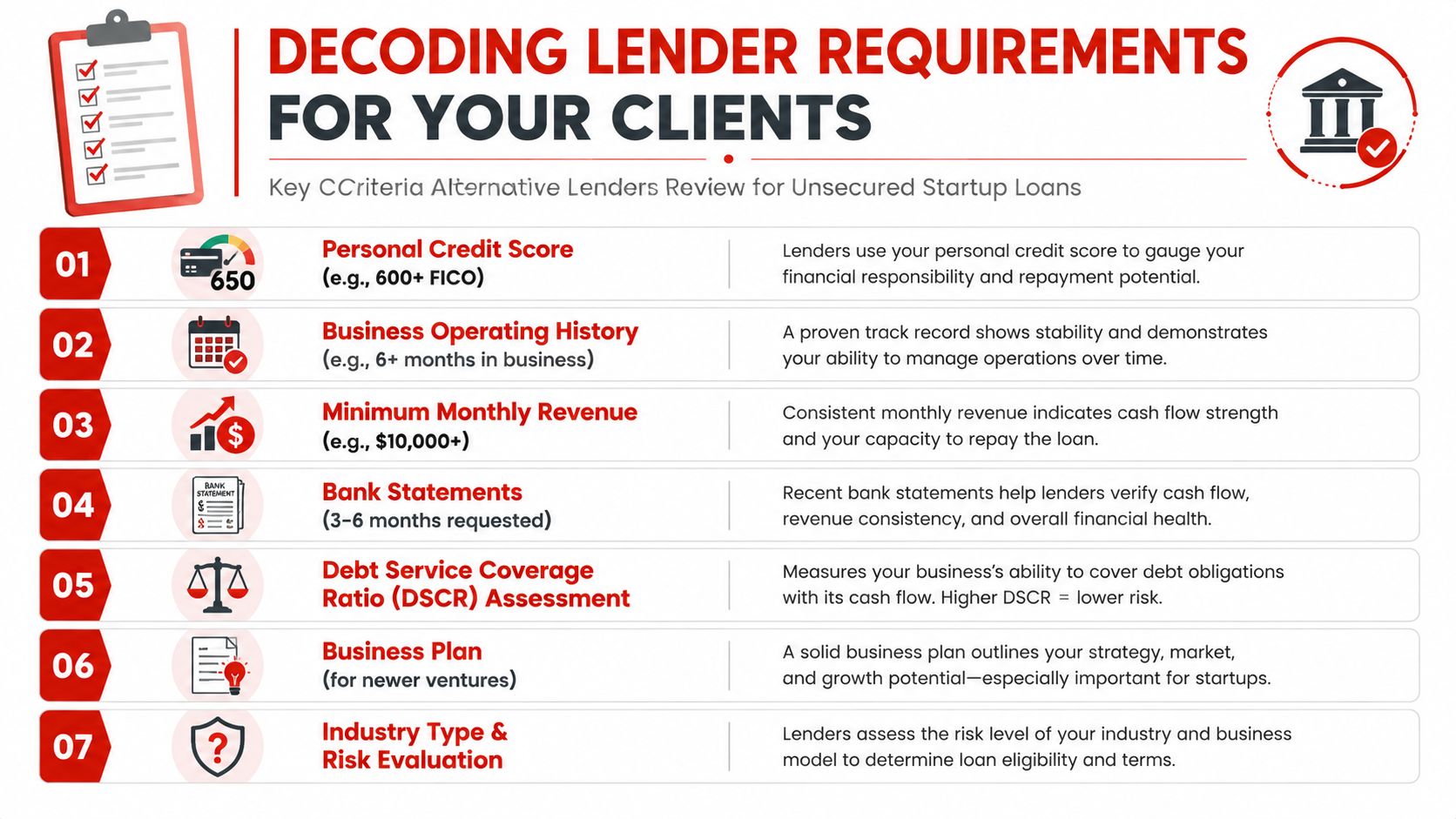

Decoding Lender Requirements for Your Clients

A trainee broker's real job starts before submission. The strongest brokers pre-qualify aggressively, collect the right documents early, and kill weak files before they waste lender attention. For unsecured business loans for startups, underwriting usually centers on three things: credit, capacity, and character.

According to Bankrate's overview of unsecured business loans, unsecured startup loans are underwritten primarily on cash-flow capacity and borrower creditworthiness, not pledged collateral. In practice, lenders commonly require a personal guarantee, a 650+ credit score, business experience, and evidence that projected monthly income exceeds loan payments by at least 1.25×.

Credit is often the first screen

For a startup, the owner's personal credit tells the lender how the borrower has handled obligation, discipline, and repayment under pressure. It's rarely the only issue, but it often determines whether the file gets serious review.

That doesn't mean perfect credit is required in every case. It means the broker needs to know whether the credit profile is supportable. A thin file, recent derogatories, or unstable usage patterns can weaken the package fast, especially when the business itself doesn't have a long operating history.

Capacity gets proved on paper

Capacity means the lender believes the company can make the payment. In a newer business, that proof may come from current bank activity, signed contracts, invoices, a launch plan, or financial projections that are realistic.

A useful underwriting discipline is to review the client's expected payment burden against projected inflow before submission. Brokers who understand debt service coverage ratio calculation can spot whether a file is directionally financeable or whether the projections are too thin to survive credit review.

A startup projection doesn't need to be fancy. It needs to be believable, consistent, and supported by the story in the file.

Character shows up in the founder's background

A founder with relevant industry experience usually presents better than someone chasing a random idea with no operational history. Lenders want to know who is steering the business, how they make decisions, and whether they understand the market they're entering.

That means a broker should gather more than forms. The file usually gets stronger when it includes:

- A concise owner background that explains industry experience and prior results

- A one-page business summary that shows the use of funds and revenue model

- Bank statements that line up with the stated story

- Basic projections tied to realistic assumptions

- A clean explanation of any red flags before underwriting asks

A messy package makes even decent borrowers look weak. A clean package makes a startup easier to trust.

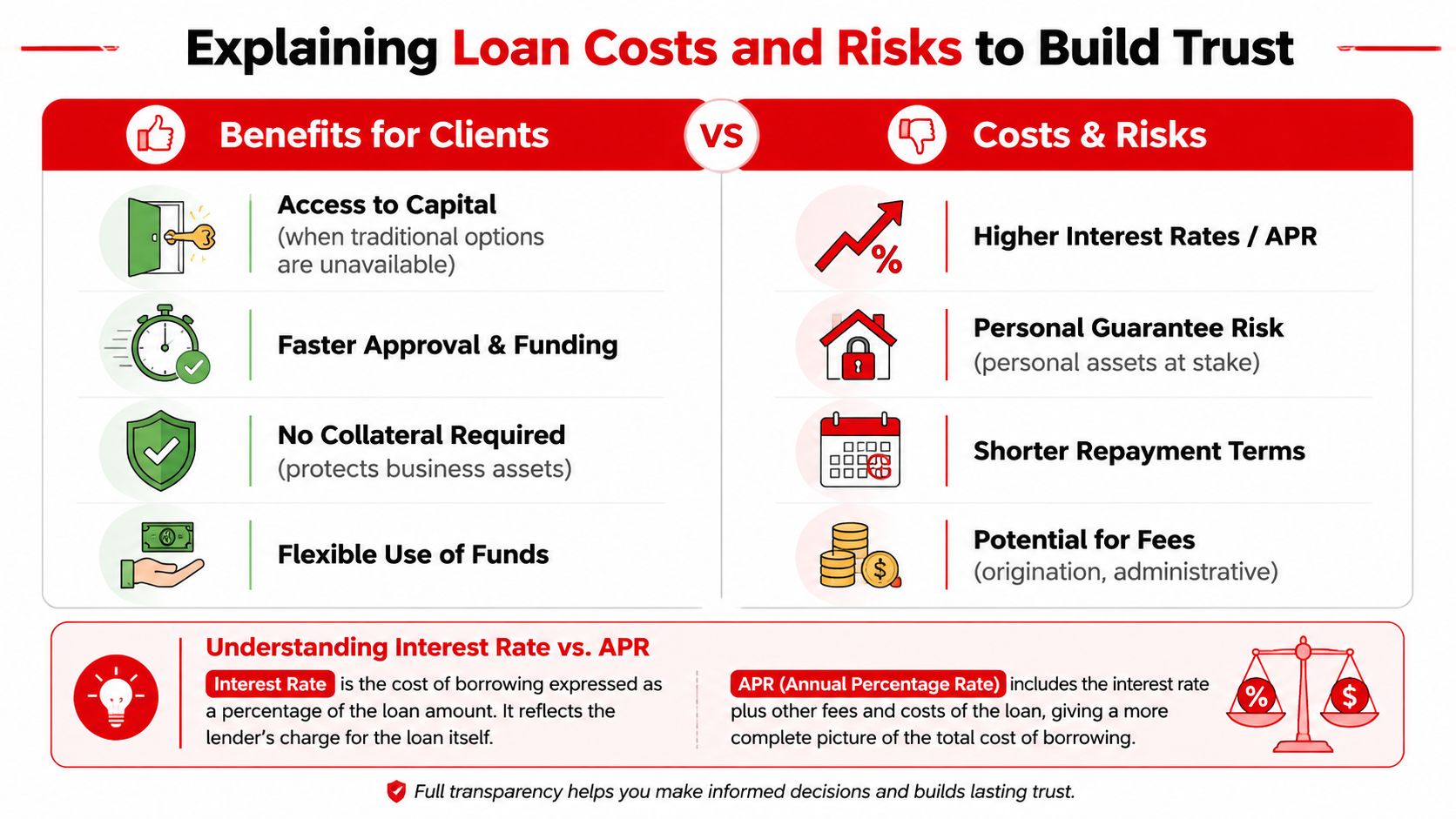

Explaining Loan Costs and Risks to Build Trust

A founder asks for $75,000, likes the speed, and says the payment “should be fine.” That is the moment a broker either earns trust or creates a future chargeback problem.

Cost conversations are where startup deals get won cleanly. They are also where weak brokers lose control of the file. If the borrower feels rushed past pricing, fees, or guarantee language, the deal becomes fragile even if it funds. A broker who explains the downside clearly usually gets fewer surprises at docs, fewer panicked calls after funding, and better referral value from the account.

Unsecured startup loans usually carry more pricing pressure than asset-backed products. The lender has no specific collateral cushion, so the structure often comes with higher rates, shorter terms, tighter payment cycles, and lower starting limits. That does not make the product bad. It defines the product.

How to explain the real cost of the money

Good brokers do not defend pricing. They translate it.

A founder needs to understand three things. First, what the payment is. Second, how often it hits. Third, what the business has to produce for the debt to stay manageable. If those three points are clear, the borrower can make an adult decision and the broker can stand behind the recommendation.

This is also where sloppy presentation kills trust. Quoting only the approval amount is amateur work. Brokers should walk the client through total repayment, fees, payment frequency, and how existing obligations affect cash flow. A clean review of the company's business debt schedule and current obligations helps frame the new payment in context instead of presenting it like free money.

A practical comparison helps:

| Consideration | Unsecured startup loan | Secured business loan |

|---|---|---|

| Collateral | Usually no specific hard asset pledged | Asset support is usually central |

| Underwriting emphasis | Personal credit, business story, repayment strength | Asset value plus repayment strength |

| Typical pressure point | Pricing, term length, payment frequency | Collateral exposure and documentation |

| Broker's job | Set expectations early and test affordability | Explain asset risk and lender controls |

Guarantees need plain English

Personal guarantees should be explained before the borrower reaches final documents. Not after.

Founders new to business lending often hear “unsecured” and assume “no personal risk.” That misunderstanding creates fallout. If the agreement includes a guarantee, say it directly. The owner is backing the debt. If the business struggles, the liability may not stay inside the business entity.

Use plain language:

- Explain why the guarantee exists. The lender wants owner support because no specific asset is pledged.

- Explain what that means in practice. The founder may still be responsible if the business cannot repay.

- Explain the decision point. If the owner is not comfortable with that obligation, the product is a poor fit.

That conversation protects the client and the broker.

Trust grows when the borrower can see the payment working

Expensive money can still be smart money. The key question is whether the capital solves a defined problem fast enough to justify the cost.

A startup using funds to cover a timed inventory buy, launch a signed contract, bridge receivables, or open a location with a clear revenue path may be using the product correctly. A startup borrowing at premium pricing for a vague growth plan usually creates stress, not momentum. Brokers who know the difference keep their pipelines healthier.

This is one place where operational habits matter. If a founder cannot explain spending discipline, the risk goes up fast. Encourage them to learn expense tracking with Snyp or use another simple system before they take on new debt. Better expense visibility makes repayment conversations more grounded and renewals easier to place later.

Borrowers will accept expensive capital when they understand the use, the cost, and the risk before they sign.

That is how brokers build repeat business. Clear cost framing leads to stronger retention, cleaner referrals, and fewer deals that should never have been submitted.

How to Coach Startups for Loan Approval

A founder gets on a call and says, “I need $75,000 fast.” New brokers often treat that as a submission cue. It is usually a coaching cue.

Startup unsecured deals are won before the file reaches underwriting. The broker who helps shape the story, clean up the documents, and tighten the borrower's answers gives the lender a file that feels financeable instead of rushed. That difference affects approvals, client trust, and your close rate.

As noted earlier, a large share of small businesses still end up underfunded or unfunded. That is why preparation is not extra service. It is part of the product.

What a broker should fix before submission

Start with the gaps that cause lenders to hesitate. In early-stage files, the problem is rarely just credit. It is usually weak explanation.

Founders often cannot clearly state three things: what the money will do, how quickly it will produce a result, and what cash flow will make the payment. If those answers are vague on your call, they will be a problem in underwriting.

A practical coaching sequence looks like this:

Review personal credit early

Most startup lenders underwrite the owner as much as the business. Pull the issue list out early. Late payments, high revolving utilization, reporting errors, and recent inquiries all deserve attention before the file is packaged.Build a simple cash flow case

The borrower does not need a polished investor deck. They need a believable monthly picture. Show expected revenue, fixed expenses, owner pay, and the proposed loan payment. If the payment only works in a best-case month, the deal is weak.Tighten the business summary

A one-page summary should cover the business model, the owner's relevant experience, the use of funds, and the expected return from the capital. Lenders do not need hype. They need a clean reason to say yes.

What makes a file easier to approve

Lenders respond well to consistency. If bank statements show one story, the application shows another, and the borrower explains a third on the verification call, the file gets harder to place.

Coach the founder to match every part of the package. Revenue claims should line up with deposits. Ownership percentages should match formation documents. Existing obligations should be disclosed the first time, not after an underwriter finds them. I tell trainees this all the time. A messy file can still get approved, but it usually prices worse, moves slower, or dies in stipulations.

For founders who need cleaner records, point them toward basic operating discipline. A simple resource to learn expense tracking with Snyp can help them document spending more clearly, which makes underwriting easier and future renewals easier to position.

Documents that deserve extra attention

A lot of startup declines start with support documents that look incomplete, inconsistent, or rushed. Pay close attention to:

- Bank statements that support the revenue story and show stable account behavior

- A current list of debts so monthly obligations are visible before underwriting asks

- Ownership and formation documents that match the application exactly

- A documented debt schedule that shows balances, payments, and terms. This guide on what a debt schedule is gives a useful framework for building one

Strong files get better attention. They help you act like a broker who improves approvals, not a middleman who forwards paperwork. That is how startup deals turn into repeat clients, referral partners, and a healthier commission pipeline.

Smart Alternatives When Unsecured Loans Are Not a Fit

Good brokers don't cling to one product. They pivot. When unsecured business loans for startups aren't a match, the conversation should move toward the funding structure that fits the client's profile and risk tolerance.

Three common pivots

Secured financing fits borrowers who do have assets and are willing to pledge them. If the founder owns equipment, vehicles, real estate, or other acceptable collateral, a secured structure may produce a more workable offer.

Revenue-based financing often fits companies with active sales but uneven margins. If the business generates ongoing receivables or card-based revenue, a repayment structure tied more closely to revenue can be easier to position than a traditional startup term loan.

Invoice financing works when the business is waiting on customer payments. In B2B settings, that can be a better answer than asking a young company to qualify on projected future strength alone. Brokers who want to understand that niche more thoroughly can review this guide to accounts receivable lenders.

The broker's value isn't product loyalty. It's matching the borrower to the right capital structure.

How to pivot without losing the client

The wording matters. If a broker says, “You don't qualify,” the conversation often ends. If the broker says, “This product isn't the best fit, but there's another route worth exploring,” the relationship usually stays alive.

That shift does two things. It protects trust, and it protects pipeline. Many borrowers who aren't right for unsecured startup funding today can become strong candidates for another product now, or for unsecured financing later after the business matures.

Your Broker Playbook for Landing Startup Deals

A new LLC gets referred to you on Tuesday. The founder has six months of operating history, decent personal credit, no real collateral, and a launch window that cannot slip. If you know how to screen that file fast, set expectations clearly, and route it to the right lender profile, you can turn a hard conversation into a funded deal and a long-term referral source.

That is a significant opportunity in startup funding for brokers. Founders rarely know which product fits, what underwriters will question, or how to present a thin file in the best possible light. The broker who can do that work consistently gets paid, even when the first option does not close.

Startup deals usually come from people who hear about the cash need before a lender ever does. Referral partnerships beat cold prospecting here because the client arrives warmer and the advisor already trusts your process. Good sources include:

- CPAs and bookkeepers who spot cash gaps, tax pressure, and growth plans early

- Business attorneys involved in formations, partner agreements, and early operating issues

- Consultants and agencies working with owners who need capital to hire, market, or fulfill demand

- Insurance and real estate professionals who stay close to business owners during expansion decisions

The brokers who earn repeat commissions in this niche are not usually the loudest. They are the ones who avoid wasting lender appetite on weak files, give referral partners honest feedback, and keep borrowers from being surprised halfway through underwriting.

Four skills matter most:

- Pre-qualify with discipline. Check personal credit, time in business, cash flow pattern, use of funds, and any recent negatives before you submit.

- Control expectations early. Explain personal guarantees, pricing range, documentation, and likely objections before the borrower gets emotionally attached to one outcome.

- Package the file cleanly. A short, accurate summary and organized documents can move a startup file faster than a long sales pitch ever will.

- Protect the referral relationship. Update partners promptly, explain declines without blaming the client, and show them you know how to handle edge cases.

Training helps, especially for new brokers who need a repeatable process for lender matching, submissions, and referral outreach. Business Lending Blueprint teaches how a business loan brokerage can be built around lender relationships and a referral-driven operating model.

As noted earlier, demand for unsecured business lending is substantial. For a broker, that does not mean every startup gets approved. It means the market is large enough to support specialization. If you become the person local advisors call when a young business needs capital, unsecured startup loans stop being an occasional product and start becoming a dependable source of commissions.