A broker gets a file, matches the borrower to a lender, and expects a smooth approval. Then the decline comes back with language that sounds technical but expensive: insufficient repayment capacity. The client is frustrated, the lender goes quiet, and the commission disappears.

Most of the time, that surprise isn't a surprise at all. It traces back to the debt service coverage ratio calculation. Brokers who can read DSCR the way an underwriter reads it stop submitting hopeful deals and start submitting financeable ones. That shift matters because funded files don't come from enthusiasm alone. They come from anticipating the lender's math before the lender ever opens the package.

For brokers building a remote, referral-driven business, DSCR becomes part of the operating system. It helps qualify faster, spot salvageable deals, and explain borrower weaknesses without guesswork. It also helps brokers understand how the alternative lending industry really works because approvals usually hinge on risk, structure, and repayment capacity, not just a borrower's story.

Table of Contents

- The Billion-Dollar Number That Gets Deals Funded

- What Is DSCR and How Do Lenders Use It

- How to Perform a Debt Service Coverage Ratio Calculation

- Lender Adjustments That Change the Final Number

- What Is a Good DSCR and How to Interpret the Result

- How Brokers Can Help Clients Improve Their DSCR

- Become the Go-To Funding Expert for Businesses

The Billion-Dollar Number That Gets Deals Funded

A new broker often thinks a deal died because the lender was picky. A seasoned broker usually knows the file was weak before it was submitted.

That difference shows up in one number: DSCR. It sounds like accounting. In practice, it's approval language. Lenders use it to decide whether cash flow can carry the debt, and brokers who understand it can tell early whether a file belongs with a conservative lender, a flexible lender, or back on the borrower's desk for cleanup.

A borrower can have a strong business story and still fail this test. Revenue may look healthy. Deposits may be steady. The owner may be confident. But if the debt service coverage ratio calculation shows thin repayment capacity, the underwriter sees risk, not opportunity.

Practical rule: Brokers get paid for funded deals, not for submitted files. DSCR helps separate those two outcomes.

This is why top brokers don't treat DSCR as a checkbox. They use it as a screening tool, a positioning tool, and sometimes a rescue tool. Before a lender raises an objection, the broker should already know where the objection is likely to come from. If the ratio is borderline, the broker can prepare context, adjust the request, or move the file to a lender that underwrites the structure more sensibly.

The broker who masters DSCR starts sounding different on borrower calls. Instead of saying, “Let's see what the lender says,” that broker says, “This payment load is the issue, and here's how to improve the file before submission.” Clients notice that. Lenders notice it too.

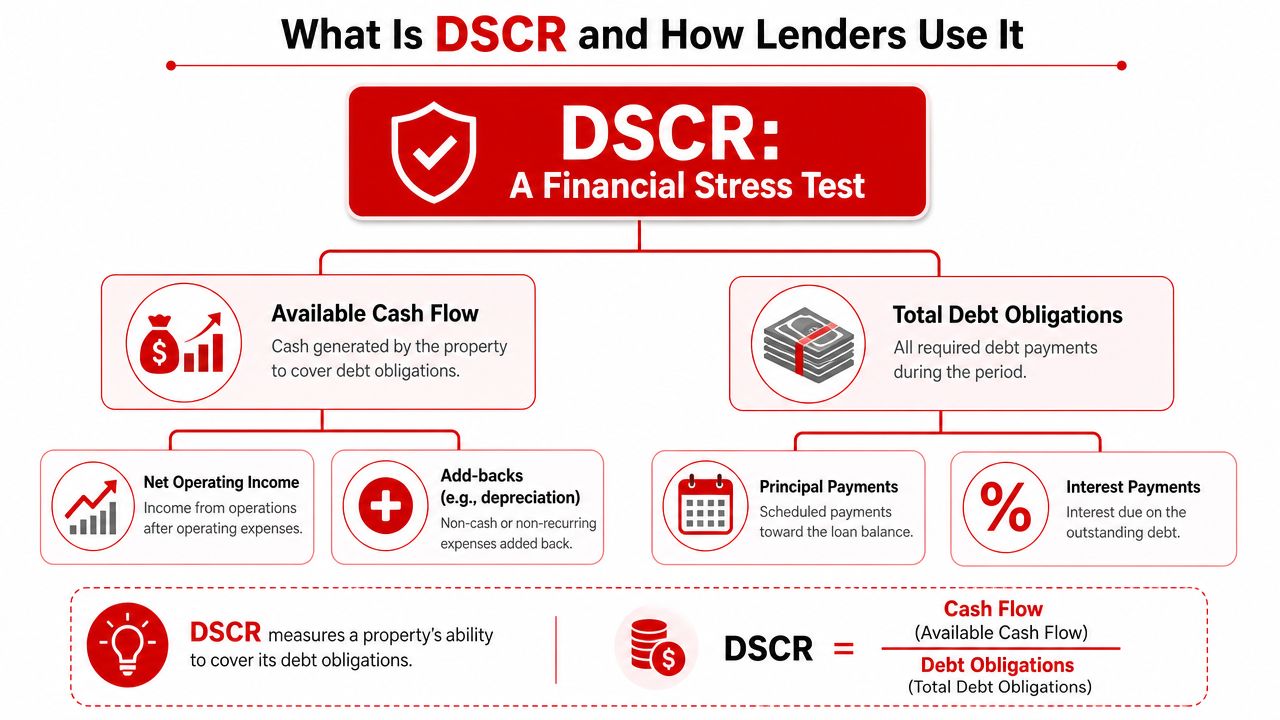

What Is DSCR and How Do Lenders Use It

DSCR is a cash flow test. It asks a simple question: does the borrower generate enough income to cover debt payments with a cushion?

The core formula is net operating income or EBITDA divided by total debt service, and debt service includes principal and interest, as outlined in Chase's explanation of how to calculate DSCR. That same source gives a real estate example of $450,000 of NOI and $250,000 of debt service, producing a 1.8 DSCR, or $1.80 of income for every $1.00 of debt service.

Available cash flow

For an operating business, lenders often focus on EBITDA. For an income-producing property, they often focus on NOI. That distinction matters because the numerator changes the story.

If a broker uses property-style NOI for an operating company, the file can be understated. If a broker uses business-style add-backs too aggressively on a property file, the file can be overstated. Good brokers know which version fits the deal before they start quoting terms.

Total debt obligations

The denominator is where many newer brokers make mistakes. Debt service isn't just the proposed new payment looked at in isolation. Lenders are trying to understand the borrower's ability to carry required obligations, and principal and interest sit at the center of that review.

Lenders don't care whether a payment feels manageable to the borrower. They care whether the documented cash flow supports the required debt load.

This is why DSCR is often the first fast read in underwriting. It compresses a borrower's repayment strength into one ratio. A lender can look at it and immediately tell whether there's room for stress, seasonality, or mistakes.

Why brokers should care early

A broker should calculate DSCR before shopping the file. That prevents two common problems:

- Misplaced submissions: Sending a thin-cushion file to a lender that wants strong repayment capacity.

- Weak borrower expectations: Telling a client the deal looks good when the numbers say otherwise.

- Lost credibility: Asking underwriters for exceptions on files that were never supportable.

A good broker uses DSCR as an early filter, not a post-decline explanation.

How to Perform a Debt Service Coverage Ratio Calculation

A practical debt service coverage ratio calculation starts with clean documents. For most business-purpose files, that means recent profit and loss statements, balance sheet support, business tax returns when available, and a current list of debt obligations. For property deals, it means reliable income and expense figures tied to the asset itself.

The broker's job isn't to create a heroic number. It's to calculate a defensible one.

Start with the right income number

For an operating business, begin with the income statement and work toward EBITDA. For a real estate asset, start with property income and operating expenses to determine NOI. The formula may look simple, but the source documents drive the credibility of the result.

| Metric | Operating Business (EBITDA) | Real Estate Investment (NOI) |

|---|---|---|

| Primary income base | Earnings from the business operation | Income generated by the property |

| Common source document | Profit and loss statement | Property operating statement or rent and expense records |

| Focus of review | Ongoing business cash generation | Property-level operating performance |

| Typical broker concern | Whether earnings reflect true recurring operations | Whether property income and expenses are normalized |

| Key risk | Owner compensation or one-time items distorting performance | Expense omissions or unstable rental income distorting performance |

For brokers working with companies that are already carrying several obligations, a working knowledge of debt management for growing companies helps frame why reducing payment pressure can be just as important as improving revenue. That context matters when a borrower asks whether the problem is “income” or “too much monthly debt.”

Build the debt service denominator carefully

The denominator should reflect required debt payments, not rough estimates scribbled into a notes field. A proper debt schedule is therefore critical. A broker who knows how to build and read one will catch payment burdens that a borrower forgets to mention, especially when multiple loans, renewals, or equipment notes are involved.

A clear primer on that process sits in this guide on what a debt schedule is.

Use a simple sequence:

- Pull the income figure that fits the deal type. EBITDA for operating businesses. NOI for property deals.

- List every required debt obligation that the lender is likely to consider in annual terms.

- Convert the payment burden into a consistent period so the numerator and denominator match.

- Divide income by debt service and review whether the ratio leaves room for lender scrutiny.

Use a simple broker worksheet

A broker doesn't need a fancy model to do strong pre-underwriting. A simple worksheet is usually enough if it's organized.

Include these fields:

- Borrower entity and deal purpose: Clarifies whether the file should be analyzed as a business, a property, or a hybrid.

- Income basis used: Mark whether the ratio uses EBITDA or NOI. That avoids confusion later.

- Existing debt payments: Capture required obligations consistently.

- Proposed new debt payment: Add it only after the broker understands whether the lender underwrites current debt, proposed debt, or a refinance structure.

- Notes on adjustments: Keep a short written explanation for anything unusual.

The cleanest DSCR worksheet wins. Underwriters trust files that make the math easy to follow.

A service business example is straightforward in concept. The broker takes recurring operating earnings from the profit and loss statement, checks whether the debt schedule shows payment strain, annualizes the required obligations, and then divides the earnings figure by that annual debt service total. If the ratio looks thin, the broker should stop there and ask whether the request amount, term, or lender target needs to change.

A property example is different. The broker uses property-level operating income and expenses to arrive at NOI, then compares that number against the annual debt obligation tied to the transaction structure. If the asset itself can't support the payment load, the borrower's confidence won't save the file.

The biggest mistake is treating both deal types the same way. Operating business DSCR and property DSCR may share a formula, but they don't share the same underwriting logic.

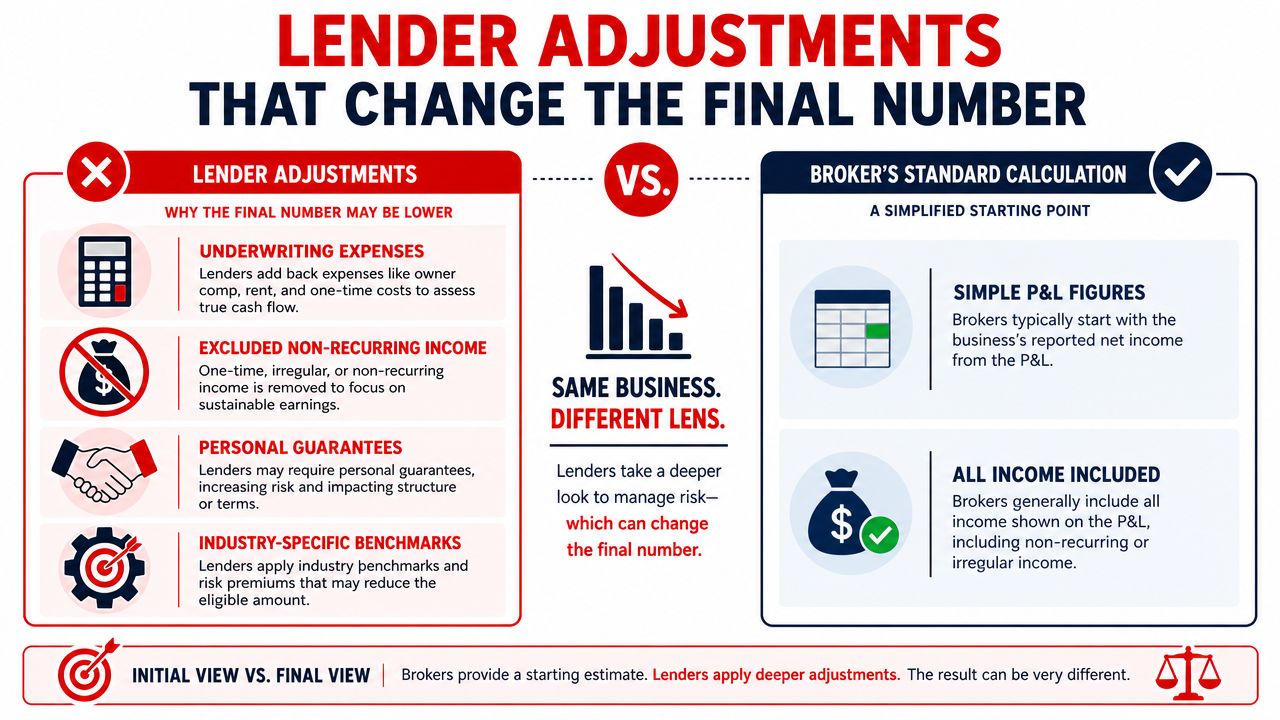

Lender Adjustments That Change the Final Number

The broker's first calculation is rarely the lender's final calculation. That gap explains why some files look strong in conversation and weak in underwriting.

Lenders adjust because they're not trying to accept the borrower's version of reality. They're trying to build a conservative view of repayment. That means some income gets reduced, some expenses get added back differently than expected, and some debt service gets modeled according to rules the broker didn't assume.

Why broker math and lender math differ

A lender may reject a one-time income item that the borrower considered normal. Another lender may question whether an expense is nonrecurring. In project-style underwriting, the metric may move away from accounting earnings and toward a more accurate cash measure. As noted in Fannie Mae guidance on annualized debt service rules for different loan structures, DSCR treatment becomes more technical with interest-only loans, ARMs, amortizing debt, supplemental mortgages, and subordinate debt. In project finance, lenders may use CFADS instead of EBITDA, reducing cash flow by items like maintenance capex to get closer to actual cash available for debt service.

That's why brokers should be careful with “add-backs.” Some are legitimate. Some are optimistic. A lender will usually know the difference.

Common friction points include:

- Nonrecurring expenses: These may be added back if they're documented clearly and established as one-time.

- Owner-related costs: Some compensation or discretionary spending may be adjusted, but only when the lender accepts the rationale.

- Maintenance or capital needs: Cash-heavy operations may face tougher treatment if future upkeep is likely to pressure repayment.

- Income quality: Revenue that looks real on a statement may still be discounted if it appears unstable or unsupported.

Loan structure can rewrite the denominator

Many broker projections fall apart because a non-standard structure can alter debt service treatment even when the borrower's financial profile hasn't changed.

An interest-only period lowers required principal during that phase. A variable-rate loan may force the underwriter to look at debt service differently than a plain fixed-rate amortizing structure. Subordinate debt can complicate repayment capacity even if the borrower insists it won't be a problem.

A broker who understands this can place the file better. When short-term products are part of the capital stack, it helps to know where those structures fit in the broader lending environment, especially when reviewing options tied to finding the best short-term lenders.

Underwriting is rarely about the formula alone. It's about which version of the formula the lender believes fits the structure.

That's the broker's edge. Not memorizing acronyms. Knowing where the lender is likely to tighten the math before the file gets priced.

What Is a Good DSCR and How to Interpret the Result

A ratio only matters if the broker knows how to read it as a decision. A DSCR can be mathematically correct and still commercially weak.

A widely used benchmark is 1.2 to 1.25, meaning the borrower generates 20% to 25% more income than required debt payments, according to Commerce Bank's discussion of DSCR thresholds. That source notes many lenders look for no lower than 1.2, and related lender guidance often frames 1.25 as a strong target.

Read DSCR like a credit decision

A few practical interpretations help:

- Below 1.0: Cash flow doesn't cover debt service. That's a major warning sign for most lenders.

- At 1.0: The borrower is covering required payments exactly, with no room for disruption.

- Around the common underwriting range: The file starts to look more workable because there's visible cushion.

- Well above minimum expectations: The borrower usually has more flexibility in lender conversations, assuming the quality of earnings is solid.

A good DSCR isn't “high.” A good DSCR is lender-appropriate for the deal type, structure, and risk profile.

The same ratio can mean different things

In this scenario, brokers separate themselves from order-takers. A number that works in one lane may fail in another. Real estate underwriting may focus on property-level support. An operating company lender may focus on enterprise cash flow. A portfolio lender may interpret the same ratio differently depending on cross-collateral support.

That means brokers shouldn't tell borrowers that one threshold guarantees approval. The ratio is a signal, not a promise.

A smarter approach is to ask three questions:

- What kind of income is supporting the file?

- How stable is that income under scrutiny?

- Which lender category is likely to accept this level of cushion?

When brokers interpret DSCR this way, they stop chasing generic approvals and start matching deals to the right credit box.

How Brokers Can Help Clients Improve Their DSCR

A weak DSCR doesn't always mean a dead deal. It often means the file needs restructuring, better documentation, or different timing.

That's where a broker creates real value. Instead of delivering a rejection, the broker can explain what's suppressing the ratio and what can be corrected before the next submission. Clients remember that level of guidance because few others in the market provide such support.

Fix the denominator first

Improving DSCR is often easier when the debt side is addressed before the income side.

Consider these moves:

- Reduce overlapping payments: Small obligations with heavy required payments can drag a file down more than borrowers realize.

- Consolidate where appropriate: A cleaner structure can improve affordability and simplify the underwriter's view.

- Adjust timing: Waiting until a short-term obligation is paid off can materially strengthen repayment capacity.

- Right-size the request: Asking for less or changing the structure may move a file from marginal to workable.

These are practical conversations. They also position the broker as an advisor rather than a messenger.

Document the numerator properly

Some files look weak because the broker didn't document the income story well. If a borrower had a one-time expense, unusual disruption, or owner-related cost that won't continue, that issue needs support, not wishful commentary.

Useful broker actions include:

- Identify legitimate add-backs: Only use items that can be explained and supported cleanly.

- Prepare a credit memo: Give the underwriter a short, factual explanation of anything unusual in the statements.

- Show contract visibility carefully: If future work supports stability, present it as context, not as guaranteed income.

- Clean up supporting records: Messy financials create lender skepticism even when the business is sound.

A borrower's broader business credit profile can also influence lender comfort. When that's part of the issue, brokers may want clients to review resources on how to improve DUN and Bradstreet ratings as part of a more complete funding-readiness plan.

The best brokers don't just hunt approvals. They improve files until approval becomes more likely.

That mindset builds trust, increases resubmission quality, and turns one transaction into a referral relationship.

Become the Go-To Funding Expert for Businesses

Brokers who understand debt service coverage ratio calculation operate differently. They prequalify faster, explain declines more clearly, and place deals with more precision. That leads to better lender relationships and a stronger chance of getting paid on funded files instead of wasting time on weak submissions.

This skill also compounds. Once a broker can diagnose repayment capacity, other parts of deal analysis start making more sense. Borrowers begin to rely on that guidance, especially when they're trying to get funding-ready. For added client education, material on preparing for a business loan in 2026 can help frame what lenders typically want to see before an application goes out.

A home-based brokerage grows when clients trust the broker's judgment, not just access to lenders. DSCR is one of the clearest ways to earn that trust.

Business Lending Blueprint shows aspiring and established brokers how to build a real business in commercial and alternative lending. If the goal is to understand deal structure, lender fit, borrower positioning, and the systems that lead to more funded files, watch the free training from Business Lending Blueprint or schedule a strategy session to see how the model works.

Generated with the Outrank tool