A debt schedule is a clear summary of every business debt obligation, showing what the company owes, when payments are due, and how those obligations affect its ability to handle new financing. In practical lending work, it's the document that turns scattered loan statements into a lender-ready picture of repayment capacity.

A lot of new brokers meet this issue on day one. A client wants funding fast, but their debt picture is messy. There's an equipment note from years ago, a revolving line they draw on when cash gets tight, and a short-term advance that never made it onto a formal spreadsheet. The owner knows money is going out every month, but can't say with confidence how much, when, or which payoff dates matter most.

That's where a debt schedule earns its keep. It gives lenders a clean, organized summary of a business's loans, shows exactly how much the business owes, when payments are due, and whether there's room for new debt. For a broker, that matters because clarity wins trust. A well-built debt schedule doesn't feel like accounting homework. It feels like deal preparation.

Many aspiring brokers focus first on lender lists, product types, and commission structures. Those matter. But the brokers who close consistently know how to package a file so an underwriter can review it quickly and say, “This borrower understands the numbers.” That starts with organizing debt properly.

Anyone learning the alternative lending space should also understand how the alternative lending industry really works, because the debt schedule sits right in the middle of that process. It helps the broker advise the client, frame the request, and submit a cleaner file that stands out for the right reasons.

Table of Contents

- Introduction From Chaos to Clarity How a Debt Schedule Unlocks Funding

- What Is a Debt Schedule Really?

- The Anatomy of a Powerful Debt Schedule

- How to Build a Debt Schedule Template and Worked Example

- How Brokers Use Debt Schedules to Get Deals Funded

- Common Pitfalls and Best Practices for Brokers

- Become the Advisor Every Business Needs

Introduction From Chaos to Clarity How a Debt Schedule Unlocks Funding

A contractor applies for growth capital. Revenue looks solid. Deposits are moving through the bank account. The business has real demand. Then the lender asks a simple question: what debt is already in place, and what does the repayment load look like over time?

That's where many files stall.

The owner sends over a few statements, a screenshot from online banking, and a rough guess at monthly payments. Nothing is malicious. It's just disorganized. But underwriters don't approve on good intentions. They approve based on a documented view of obligations, timing, and affordability.

Why this tool changes the conversation

A debt schedule takes that pile of disconnected information and turns it into something useful. It organizes each debt by lender, balance, rate, payment pattern, and maturity. More importantly, it helps the broker answer the question behind the question: can this business take on more financing without creating a problem later?

Practical rule: If a borrower can't clearly explain existing debt, a lender assumes the worst until the file proves otherwise.

That's why the debt schedule is more than a worksheet. It gives structure to the borrower's story. Instead of saying, “They have a few loans,” the broker can show which obligations are short-term, which are secured, which may be refinanced, and where cash flow pressure is likely to show up.

What lenders want to see

A useful debt schedule helps a broker present:

- Current obligations clearly: Every major debt in one place.

- Payment timing: When cash has to leave the business.

- Pressure points: Maturities, heavy payment periods, and likely refinancing needs.

- Capacity for new debt: Whether a new facility fits or creates strain.

A trainee broker should think of this as one of the first credibility tools in the trade. Anyone can forward an application. A professional broker organizes risk before sending the file.

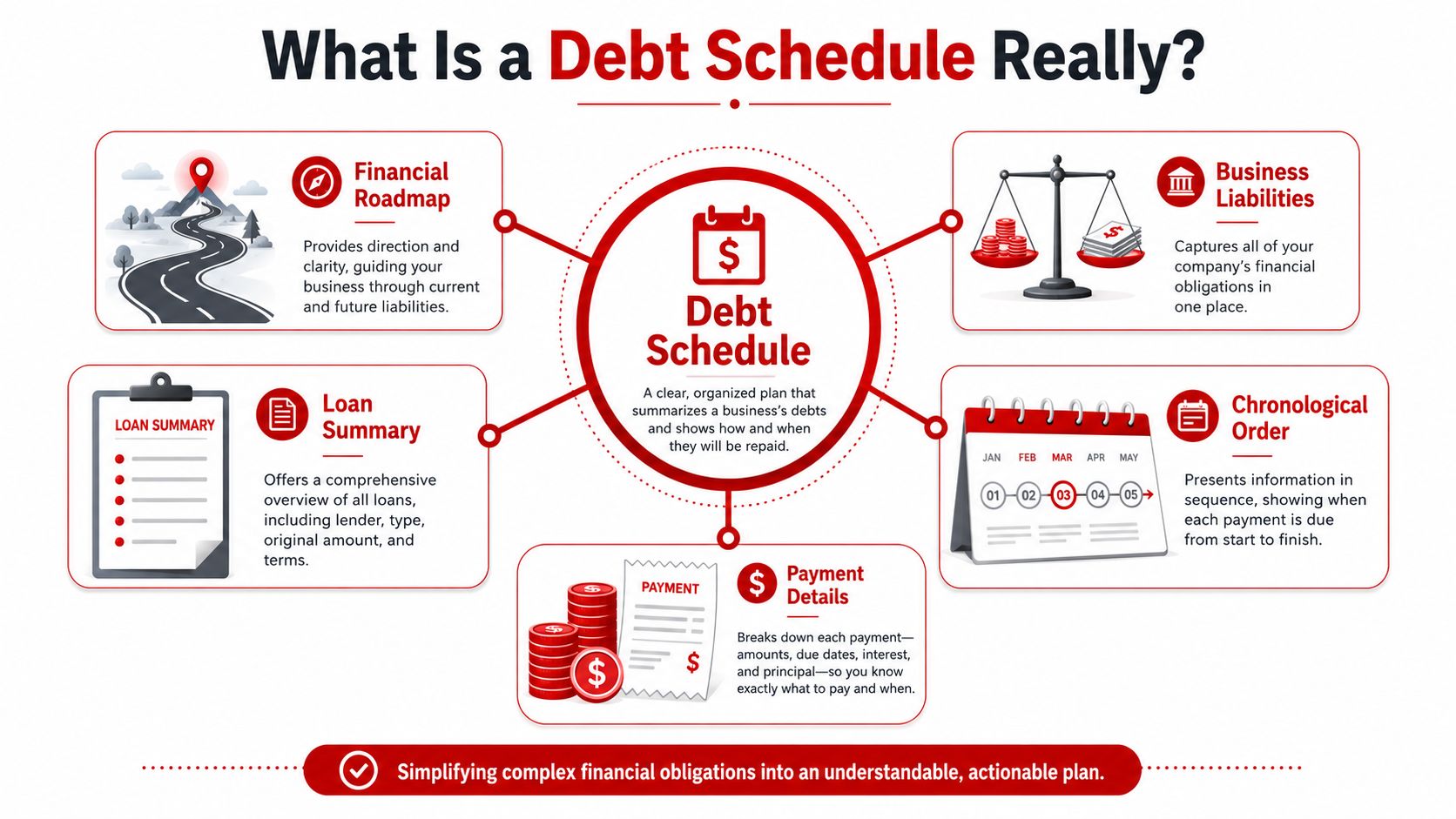

What Is a Debt Schedule Really?

At a practical level, a debt schedule is a business's debt map. It shows where the obligations started, what remains outstanding, how they're being repaid, and when they come due. That's the simple answer to what is a debt schedule.

In formal financial modeling, the definition is tighter. A debt schedule tracks outstanding balances, mandatory principal amortization, and interest expense over time, and it links directly to the three core financial statements. Interest expense flows to the income statement, closing debt balances flow to the balance sheet, and principal repayments flow through financing cash flow, as explained by Wall Street Prep's debt schedule overview.

Why brokers should care about the modeling definition

A new broker doesn't need to build institutional-grade models on every deal. But understanding the mechanics changes how the file is packaged.

A lender isn't just asking for a list of loans. The lender wants a timeline of repayment. That includes how balances roll forward, how interest affects cash flow, and when existing debt will mature. If the broker understands that, the application stops looking like a stack of documents and starts looking like a thought-out credit package.

A schedule also works like a GPS for the deal. It shows the borrower's current position and the route ahead. If a maturity is approaching, that might point to a refinance. If payments are too heavy in the near term, the right structure may be a consolidation or a longer repayment profile instead of stacking another obligation on top.

The debt schedule as a lender communication tool

Underwriters appreciate documents that reduce guesswork. A clean debt schedule tells them the broker has done the first layer of analysis already.

That's one reason many brokers also study how loan amortization schedules work in practice. The details in amortization patterns help explain why two loans with similar balances can create very different monthly pressure on the business.

For aspiring brokers, that's the difference between order taking and advisory work. A broker who understands debt structure can review a file, spot weak points, and guide the borrower before the lender has to ask.

There's also a broader industry reason this skill matters. Debt schedules are used widely in business finance to assess maturity obligations, liquidity, and borrowing capacity, and Financial Edge notes that U.S. household debt reached $18.8 trillion in the first quarter of 2026 after rising by $18 billion or 0.1% from the prior quarter. Business borrowers face the same basic challenge. Debt has to be tracked on a schedule, not by memory.

Anyone working with newer business owners can also benefit from reviewing business loan fundamentals and financing basics, because most borrowers don't arrive with their obligations organized.

The Anatomy of a Powerful Debt Schedule

A weak debt schedule is just a list. A powerful one answers lender questions before they're asked.

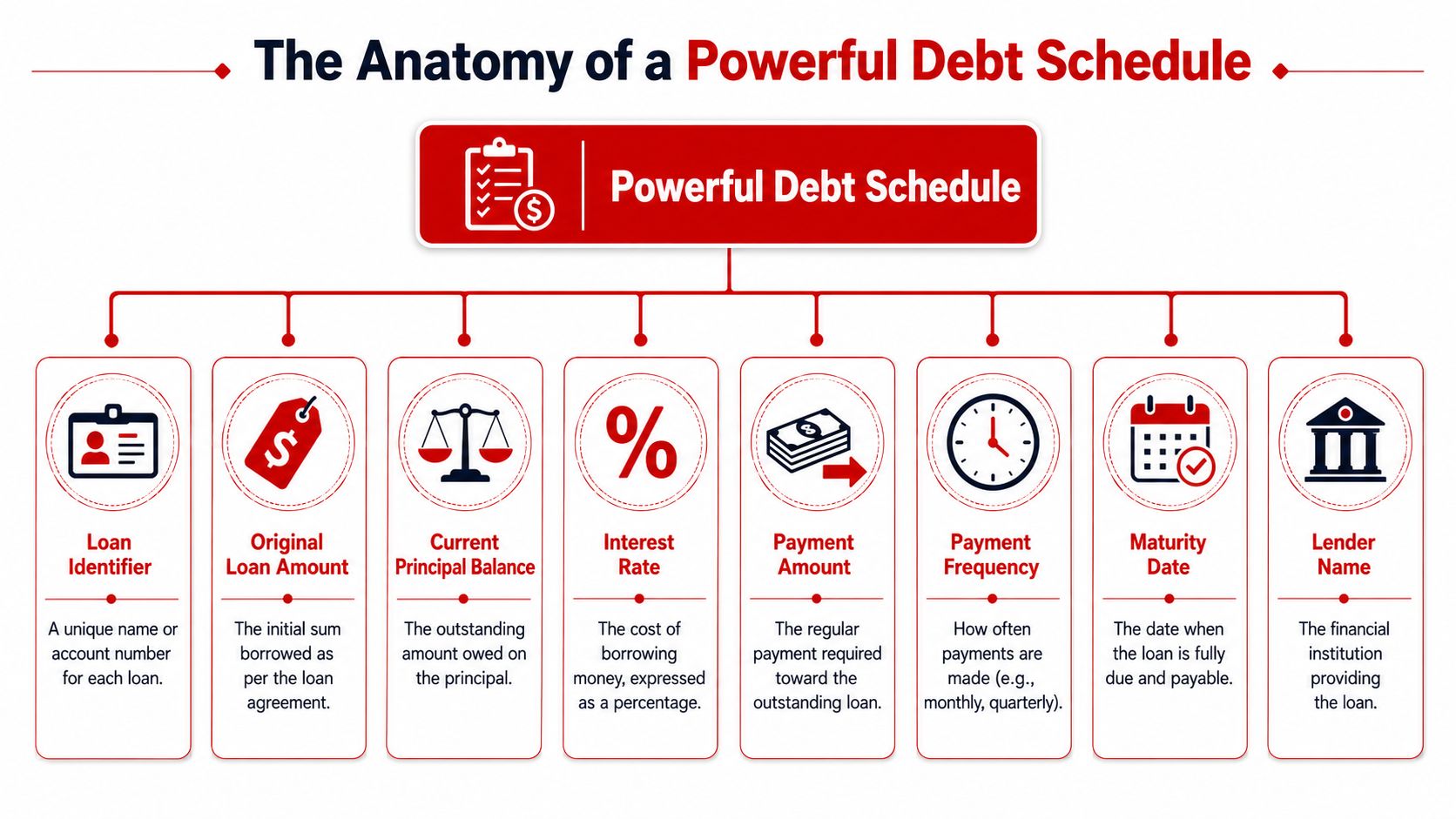

The most useful schedules capture more than a balance. They typically include lender name, origination date, current balance, interest rate, payment frequency, collateral, and maturity date for each obligation, because those fields let finance teams forecast debt service and compare it to expected cash generation, as outlined in SoFi's explanation of a business debt schedule.

The fields that actually matter

Here's what belongs on a broker-ready debt schedule and why each item matters:

- Lender name: This shows who holds the obligation today. It helps the broker identify the type of creditor involved and whether payoff procedures are likely to be simple or more document-heavy.

- Loan type: Term loan, line of credit, equipment note, lease, or advance. Structure matters because repayment behavior differs by product.

- Origination date: This gives context. A debt taken recently can signal a borrower still stabilizing. Older debt may suggest seasoning and payment history.

- Original amount: This helps lenders understand the size of the obligation at closing and how much has been paid down.

- Current balance: This is the amount still outstanding. It's one of the first figures an underwriter scans.

- Interest rate: Fixed and variable debt create different planning issues. Even when the payment is affordable today, rate movement can change future pressure.

- Payment amount and frequency: Monthly, weekly, or another pattern. Cash flow stress often hides in timing, not just total dollars.

- Maturity date: This reveals when principal is due or when refinancing may be needed.

- Collateral: This shows which assets are already pledged and what flexibility remains for new secured financing.

What underwriters read between the lines

An underwriter doesn't review these columns in isolation. The schedule tells a story about financial discipline.

If maturities bunch up in a short period, refinancing risk goes up. If collateral is already tied to several facilities, the next lender may need a different structure. If payment frequency is aggressive, the borrower may need relief even when headline revenue looks healthy.

A clean debt schedule tells the lender that the borrower's obligations are knowable, manageable, and being monitored.

That's why presentation matters. One page that clearly lays out the debt stack usually does more for credibility than ten pages of scattered statements.

How strong formatting helps the file move

A broker doesn't need a fancy model. Clean layout is enough:

| Field | Why a lender cares |

|---|---|

| Lender | Identifies the creditor and payoff source |

| Balance | Shows current exposure |

| Rate | Signals cost of debt and possible volatility |

| Payment frequency | Shows how often cash leaves the business |

| Maturity | Highlights refinance timing |

| Collateral | Reveals secured asset constraints |

Brokers who want to sharpen the bigger-picture connection between debt schedules and statement analysis often review frameworks like Steingard Financial's insights for three-statement models. Not because every small business deal needs a full model, but because strong packaging starts with understanding how debt touches cash flow.

How to Build a Debt Schedule Template and Worked Example

Most brokers don't need specialized software to build a usable debt schedule. A spreadsheet is enough if the structure is right and the inputs are verified. The goal is clarity, not complexity.

A good template starts with one row per obligation. Each row should describe a single debt facility, not a mix of products rolled together. If the borrower has two separate term loans with the same lender, list them separately. Lenders care about individual terms, not blended guesses.

A simple template that works

A practical starting table looks like this:

| Lender | Loan Type | Origination Date | Original Amount | Current Balance | Interest Rate | Monthly Payment | Maturity Date |

|---|---|---|---|---|---|---|---|

That structure won't answer every advanced credit question, but it will organize the core items most lenders need first. From there, a broker can add columns for collateral, payment frequency, payoff amount, or notes about variable rates.

Worked example for Citywide Plumbing

Consider a hypothetical borrower called Citywide Plumbing. The company has three obligations:

- An equipment loan used to finance service vehicles or machinery

- A line of credit used for short-term working capital

- A merchant cash advance taken during a temporary cash squeeze

The broker builds the schedule by asking for the latest statement or payoff information on each one. Then the broker fills in the rows. No guesswork. No rounding from memory if actual statements are available.

| Lender | Loan Type | Origination Date | Original Amount | Current Balance | Interest Rate | Monthly Payment | Maturity Date |

|---|---|---|---|---|---|---|---|

| Lender A | Equipment Loan | [from statement] | [from statement] | [from statement] | [from agreement] | [from statement] | [from agreement] |

| Lender B | Line of Credit | [from statement] | [credit limit or original draw, as applicable] | [from statement] | [current rate] | [current required payment] | [renewal or maturity date] |

| Lender C | Merchant Cash Advance | [from contract] | [advance amount] | [estimated payoff or current balance if available] | [if expressed as rate, list it; if not, note payment terms separately] | [current required payment equivalent] | [expected payoff date] |

This example is intentionally plain. That's what works. Brokers lose time when they overdesign the file before getting clean inputs.

How to build it step by step

Collect the source documents

Ask for the most recent statements, loan notes, and payoff letters if available. A debt schedule built from memory usually creates cleanup work later.Separate each obligation

Don't combine debts because they feel similar. A line of credit and an equipment note behave differently, even if the balances are close.Enter the contractual details

Fill in lender, product type, rate, payment amount, and maturity using the documents in hand.Add a notes column if needed

This is useful for variable-rate debt, seasonal payment patterns, or obligations with unusual payoff rules.Review the schedule against bank activity

If a payment appears in statements but not in the debt schedule, something is missing.

Working standard: If a broker can't trace a listed debt back to a statement, contract, or payoff document, it shouldn't be treated as final.

What makes the template lender-ready

A lender-ready schedule is current, readable, and consistent. Dates follow one format. Balances are updated to the same period. Product names are clear. If the borrower's records are messy, the broker should note assumptions instead of disguising them.

That discipline matters because the schedule often becomes the basis for a broader funding recommendation. If the borrower's short-term debt load is heavier than expected, the right move may be refinance, consolidation, or a different product altogether. The schedule gives the broker the evidence to make that call.

How Brokers Use Debt Schedules to Get Deals Funded

A debt schedule is one of the fastest ways to separate a broker from a file sender. It tells the lender that the package has already been screened for clarity, timing, and basic repayment logic.

That matters in alternative lending, where speed counts but sloppy packaging still gets punished. If the underwriter has to reconstruct the borrower's liabilities from scattered statements, the file slows down. If the broker provides a clean schedule up front, the lender can move more quickly to the key question: does this request make sense?

What the debt schedule does inside the deal

In financial modeling, a debt schedule rolls balances forward across periods by linking principal amortization, interest expense, and maturity timing, so one period's ending debt becomes the next period's beginning debt. Hyperbots explains that this structure is central in leveraged finance because it shows whether a company can service multiple tranches based on seniority and repayment terms.

A broker can apply the same thinking on a smaller business file.

The schedule helps answer questions such as:

- Can the borrower realistically support another payment?

- Is an upcoming maturity creating urgency?

- Would refinancing improve cash flow structure instead of adding strain?

- Are there secured obligations that limit collateral options for the next lender?

How strong brokers use it strategically

Strong brokers don't attach the schedule as an afterthought. They use it to frame the request.

If a borrower has expensive short-term debt, the broker can show how a different facility may simplify the debt stack. If the business has several obligations with uneven payment timing, the broker can present the new request as a way to smooth cash demands rather than increase pressure. That creates a cleaner credit story.

A debt schedule also helps with lender matching. Not every funder wants the same profile. Some are more comfortable with refinancing scenarios. Others prefer straightforward growth capital requests with limited existing debt complexity. The schedule helps the broker decide where the file belongs before the application goes out.

Underwriters rarely complain about getting too much organized information. They do complain about having to assemble the picture themselves.

Why this improves broker credibility

When a broker submits a package that includes a current debt schedule, the message is clear. This file has been reviewed. The borrower has been coached. The request is grounded in actual obligations, not optimism.

That creates trust, and trust leads to more productive conversations with funding partners. It also improves the client relationship. Business owners don't always know how their existing debt stack looks from a lender's side. The broker who can explain it earns advisory authority.

Readers who want to see how professionals think through packaging and positioning can review funding strategies from an experienced business loan broker. The common thread is simple. Better-prepared files create better funding conversations.

Common Pitfalls and Best Practices for Brokers

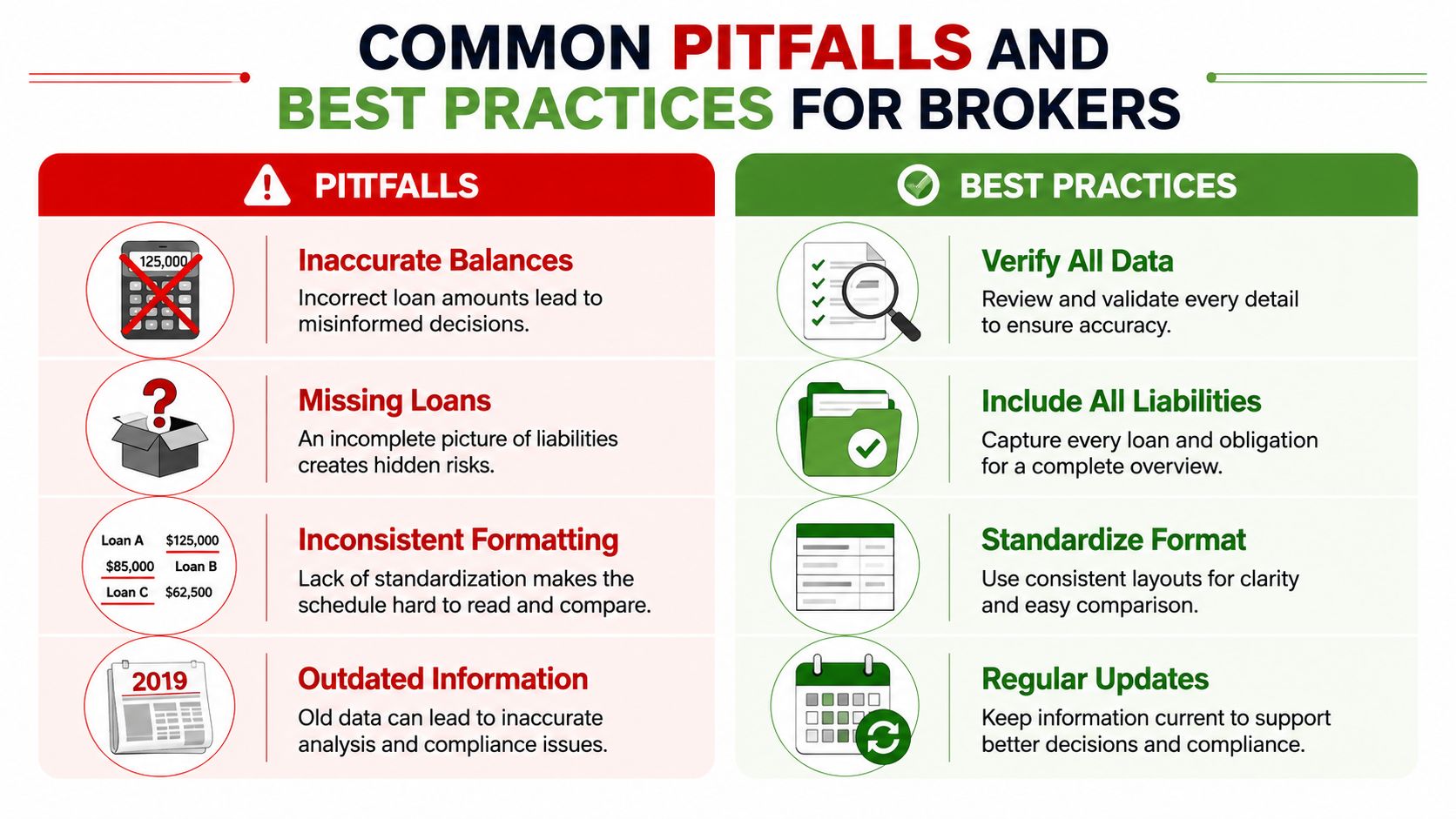

A broker pulls statements, builds a clean-looking debt schedule, and sends the file out fast. Two hours later, the underwriter finds a daily debit position that was never listed and a term loan balance that changed after a recent payoff request. The problem is no longer just missing data. The broker has made the lender question the rest of the package.

That is why this section matters in real production. A debt schedule is one of the fastest ways to show a funding partner that you run a tight process, and one of the fastest ways to lose credibility if you do not.

Pitfalls that weaken the file

These mistakes show up all the time in alternative lending:

- Stale balances: Old statements create avoidable problems, especially on products with frequent payments or recent draws.

- Incomplete debt stacks: Borrowers often leave out equipment loans, merchant advances, partner notes, tax plans, or secured lines that still affect repayment capacity.

- Messy naming conventions: If one item is labeled "Loan 1" and another is labeled by servicer name, the underwriter has to stop and decode the file.

- Missing payment frequency: Monthly, weekly, and daily obligations hit cash flow very differently. A balance alone does not show the pressure.

- No collateral notes: If UCCs, blanket liens, or equipment positions already exist, structure and lender fit can change fast.

- Ignoring contingent obligations: Guarantees, settlement agreements, and deferred payables may not sit neatly in a standard loan list, but they still matter.

Small errors create larger consequences. They lead to follow-up requests, slower responses, weaker lender confidence, and in some cases a decline that had nothing to do with the client's actual business performance.

Best practices that make brokers more reliable

Good brokers treat the debt schedule as part of deal strategy, not paperwork.

- Build from source documents: Use statements, payoff letters, portals, and signed notes instead of borrower memory.

- Date every data point: If a balance is current as of a specific day, say so.

- Break out each facility separately: One lender, three products, should appear as three entries if the terms differ.

- Show payment structure clearly: Include payment amount, frequency, maturity, and whether the rate or payment can change.

- Use comments with purpose: Note renewals in process, disputed balances, recent consolidations, and anything unusual an underwriter would ask about anyway.

- Refresh the schedule before submission: A file that sat for even a week can be wrong in this market.

I also tell new brokers to reconcile the debt schedule against bank statements before they send the package. If the schedule shows three active obligations but the bank account shows five recurring debits to lenders, the file is not ready.

The debt schedule should answer questions before the underwriter asks them.

A practical quality check before submission

Use a short review pass before the file goes out:

| Checkpoint | What to confirm |

|---|---|

| Completeness | Every known lender obligation, lease, note, and payment plan is listed |

| Accuracy | Balances match current statements, payoff figures, or portal data |

| Cash flow impact | Payment amount and frequency reflect how money actually leaves the account |

| Security | Collateral positions, liens, or guarantees are disclosed clearly |

| Consistency | Dates, lender names, and categories follow one format |

| Notes | Exceptions, assumptions, and recent changes are explained |

This habit helps close more than the current deal. A broker who keeps clean debt records can spot refinance opportunities, prepare clients for renewals, and step into the advisor role instead of acting like a form filler. That is part of what separates a hobbyist from someone serious about building a business loan broker practice that earns repeat business and lender trust.

Become the Advisor Every Business Needs

A debt schedule looks simple on the surface. In practice, it's one of the most useful tools a broker can master. It organizes liabilities, highlights pressure points, and helps lenders evaluate whether a new request fits the borrower's current reality.

That's why the brokers who understand debt schedules tend to earn more trust from both sides of the transaction. Clients see someone who can create clarity. Lenders see someone who submits cleaner files. Over time, that reputation matters more than flashy marketing.

For anyone building a remote brokerage, this is the kind of skill that compounds. It helps with better conversations, better deal packaging, and better long-term relationships with business owners who need ongoing access to capital.

Anyone serious about building that skill set can explore what it takes to become a business loan broker and start developing the practical habits that lead to repeatable funding results.

Business Lending Blueprint shows aspiring brokers how to build a real business loan brokerage from home, serve business owners with practical funding solutions, and grow through referral relationships instead of hype. To learn the model, watch the free training at Business Lending Blueprint or schedule a strategy session to see whether this business fits your goals.

Generated with the Outrank tool