A newer broker often sits across from a business owner who is excited, persuasive, and completely certain the project will work. The owner wants funding fast. The broker wants the file approved. The problem is that confidence doesn't repay a lender, and enthusiasm doesn't protect a broker's reputation.

That's where disciplined deal screening changes everything. A broker who understands how to find profitability index can move the conversation away from hopeful storytelling and toward decision-grade analysis. Instead of asking whether a project sounds good, the broker asks whether the project creates enough present-value benefit relative to the capital required.

That shift matters. It helps a broker qualify deals more intelligently, frame stronger funding narratives, and become more useful to referral partners who care about quality, not just volume.

Table of Contents

- Beyond Gut Feelings The Broker's Secret Weapon for Vetting Deals

- What Is the Profitability Index and Why It Matters to You

- How to Calculate the Profitability Index a Step by Step Guide

- Profitability Index in Action A Real-World Broker Example

- Interpreting the PI How to Make the Right Call

- Turn Financial Insights into a Thriving Broker Business

Beyond Gut Feelings The Broker's Secret Weapon for Vetting Deals

A business owner comes in convinced a new expansion, equipment purchase, or location buildout will pay off. The story is polished. The urgency is real. The numbers, however, are thin. Many brokers move straight to packaging the file and hoping a lender fills in the gaps.

The stronger move is different. A disciplined broker pauses and asks a harder question: does the project justify the capital being requested?

That's where the profitability index, or PI, becomes useful. It gives a broker a practical screen for whether a proposed use of funds appears economically sound after accounting for the time value of money. That last part matters. Plenty of projects look attractive when someone totals up future inflows and ignores timing. Far fewer hold up when those inflows are discounted properly.

What separates a broker from a paper pusher

A paper pusher says, “Let's submit it and see what happens.”

A trusted advisor says:

- Clarify the use of funds: What exactly is the client buying or building?

- Tie funding to cash generation: Which future cash flows are expected to come from this project?

- Test the economics: Does the project appear to create value once timing and required investment are considered?

That process changes the client conversation. It also changes the broker's pipeline quality. Better-screened deals are easier to explain, easier to position, and easier to defend.

Practical rule: A broker earns more trust when the analysis gets sharper before the application goes out, not after the lender starts asking questions.

This is also why adjacent analytical disciplines matter. Anyone working with project assumptions, property performance, or market-driven forecasts can benefit from structured frameworks like this guide to real estate data analytics, because the core habit is the same: translate a business idea into measurable decision inputs.

Why this matters for commissions

A broker doesn't need every owner to have perfect spreadsheets. A broker does need a repeatable way to spot which opportunities deserve time and which ones need more work before they touch a lender.

That's a key edge. PI helps a broker protect credibility, improve deal selection, and build the kind of advisory reputation that leads to repeat clients and stronger referral relationships.

What Is the Profitability Index and Why It Matters to You

A borrower walks in asking for capital to open a second location, buy equipment, or expand inventory. The numbers sound promising, the owner is confident, and the story is easy to like. Your job is to decide whether the project earns the capital it needs.

That is where the profitability index earns its place in a broker's toolkit.

The profitability index measures how much present-value return a project is expected to produce for each dollar of upfront investment. In plain terms, it helps you judge whether the expected future cash generated by a project justifies the capital going in today.

For brokers, that matters because good deals are not just fundable. They are defendable. A client may be excited about growth, but lenders still want to see that borrowed money is tied to a project with a reasonable economic case behind it.

The practical meaning of PI for a broker

PI gives you a cleaner way to screen opportunity quality before you spend time packaging the file. It helps answer a simple business question: if this borrower puts capital into this project, is the expected payoff strong enough relative to the cost?

That changes how you evaluate requests for expansion capital, equipment financing, tenant improvements, or a new product launch. Instead of relying on enthusiasm or headline revenue, you can connect projected cash generation to capital efficiency. That is also why brokers should understand basics like top-line revenue, while remembering that revenue by itself does not prove an investment deserves financing.

A strong broker uses PI to improve three parts of the job:

- Deal screening: Filter out projects with weak economics before they reach a lender.

- Client advising: Push borrowers to clarify assumptions, timing, and expected returns.

- Commission quality: Spend more time on opportunities that are easier to place and more likely to close.

That last point matters. The fastest way to waste a month in this business is to chase a loan request built on vague projections and thin logic.

Why PI matters beyond theory

Lenders care about repayment capacity. Borrowers care about growth and return. Brokers sit between those interests, and PI helps translate the borrower's plan into a capital-allocation decision that makes sense to both sides.

Used well, PI sharpens your questions. What cash flow is this project expected to produce? How long will it take to show up? Is the upfront investment realistic? Are the assumptions strong enough to survive lender scrutiny?

Those are brokerage questions, not classroom questions.

This perspective also shows up outside business lending. Investors comparing real estate opportunities often evaluate expected return against the capital tied up in each option. A consumer-facing piece like Invexa on French investment property reflects the same discipline. Capital should go where it is likely to produce the best value relative to what is committed.

A broker adds more value when the financing request is tied to a sound investment decision, not just a loan amount.

PI helps turn that standard into a repeatable habit. It gives you a disciplined way to judge whether a project deserves serious attention, needs better assumptions, or should be passed over before it drains time, credibility, and pipeline space.

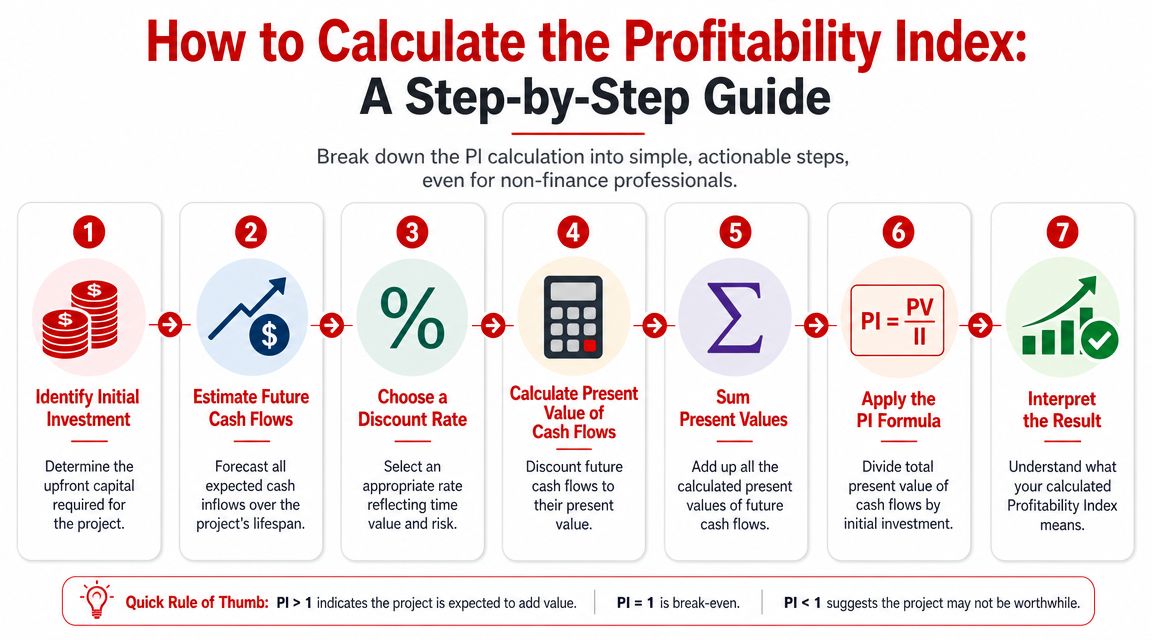

How to Calculate the Profitability Index a Step by Step Guide

A broker who can calculate PI quickly has an edge. You can sort promising requests from weak ones before you spend hours packaging a file that never should have made it that far.

The math is straightforward. Calculate the present value of the project's future cash flows, then divide that total by the initial investment. You can also express it as: PI = (NPV + initial investment) ÷ initial investment. The hard part is not the formula. The hard part is getting inputs you would trust if your own commission depended on the deal closing and performing.

Start with the initial investment and real cash flows

Begin with the full upfront cost. For a borrower, that may include equipment, installation, buildout, software, permits, delivery, or working capital tied directly to the project. New brokers often understate this number because the client mentions only the purchase price. That creates a distorted PI before the analysis even starts.

Then estimate future free cash flows. Free cash flow is what remains after the project's operating costs and other direct cash demands are covered. Revenue alone does not belong in the model. If a client says a new machine will add $20,000 a month in sales, the next question is obvious. How much of that becomes usable cash?

A practical review usually focuses on three questions:

- What new cash is coming in: Added collections, margin improvement, or cost savings tied to the project

- What new cash is going out: Labor, maintenance, supplies, marketing, insurance, or other project-specific costs

- When the cash arrives: Earlier cash flows carry more value than later ones

Existing debt matters here too. A project can look attractive on paper and still strain the borrower if current loan payments are already tight. That is why it helps to understand the borrower's obligations through a debt schedule and payment timeline.

Choose a discount rate that matches the deal

The discount rate converts future cash into today's dollars. It reflects required return and deal risk.

Set it too low and weak projects start looking acceptable. Set it too high and you can reject opportunities that would have served the client well and produced a financeable transaction. This is a key trade-off in brokerage. A conservative rate protects against rosy forecasts, but it can also make growth investments look worse than they are.

Use a rate that fits the financing context and the borrower's risk profile. If the client is entering a new market, relying on unproven demand, or layering on debt in a tight cash position, the analysis should reflect that risk.

A polished spreadsheet does not fix a soft discount rate. It only hides the problem better.

Run the formula in the right order

Once the cash flows are forecast, discount each period back to present value. Add those discounted amounts together. Divide that total by the initial investment.

A simple worksheet looks like this:

| Item | What goes in |

|---|---|

| Initial investment | Total upfront project outlay |

| Future cash flows | Period-by-period free cash flow estimates |

| Discount rate | Required return based on risk and financing context |

| Present value total | Sum of discounted future cash flows |

| PI | Present value total divided by initial investment |

This process gives you a usable screening ratio. If you broker multiple requests in a week, that matters. PI helps you decide which files deserve serious attention, which ones need better assumptions, and which ones are unlikely to hold up under lender review.

Avoid the mistakes that make PI misleading

Most bad PI analyses fail for predictable reasons.

- Using sales instead of free cash flow: Higher revenue does not always produce more cash.

- Skipping the discounting step: Undiscounted inflows make distant returns look stronger than they are.

- Leaving out part of the upfront cost: Installation, training, and working capital often get missed.

- Treating PI as the only decision metric: PI shows value per dollar invested, but it does not tell you everything about total value or financing fit.

- Ignoring scale: A smaller project can post a higher PI while generating less total profit than a larger alternative.

Good brokers do not use PI to decorate a pitch. They use it to pressure-test assumptions before they put their name on a deal.

If the forecast is guessed, the PI is guessed too.

That is the standard to keep in mind. The formula is simple enough for any broker to learn quickly. Judgment is what turns it into a tool that helps clients make better capital decisions and helps you spend your time on deals that can close.

Profitability Index in Action A Real-World Broker Example

A broker rarely gets handed a polished capital-budgeting model. More often, the client has a clear need, a rough expected upside, and a lender timeline that feels tighter than it should. That's where a practical PI worksheet earns its keep.

The client request

Consider a fictional print shop called Creative Canvas Prints. The owner wants a term loan to buy a new large-format printer. The case sounds sensible. The current machine is slower, turnaround times are slipping, and the owner believes the upgrade will support more orders and better margins.

The broker's job isn't to nod along. The broker's job is to translate that story into a funding case.

That means gathering four inputs:

- The upfront cost: What total capital is required to acquire and install the printer?

- The expected future cash flows: What additional free cash flow should the new machine generate?

- The timing: When should those cash flows realistically arrive?

- The discount rate: What required return should be used to convert those future amounts into present value?

Here is the kind of worksheet view that makes the conversation easier to manage.

How the broker uses the worksheet

The worksheet doesn't need to impress anyone visually. It needs to do three things well.

First, it separates incremental project cash flow from general business revenue. If the owner claims the new printer will boost sales, the broker asks which cash flows come specifically from faster output, better job mix, lower outsourcing costs, or reduced waste.

Second, it forces timing discipline. A lot of owners speak in annual upside, but lenders and brokers often need a more precise operating picture. If the shop also has outstanding invoices or seasonal swings, the file may benefit from discussing funding options commonly used by accounts receivable lenders, especially when working capital pressure affects how quickly the equipment investment pays off.

Third, it tests whether the present value of expected future cash flows appears strong enough relative to the initial outlay. If the ratio is weak, the broker has choices. The deal might need restructuring. The assumptions might need cleaning up. Or the owner may need to delay the project.

The broker's value isn't in forcing every deal forward. The value is in showing the client which version of the deal is actually defensible.

What the lender conversation sounds like

When the broker has done the work, the lender conversation improves immediately. Instead of saying, “The owner feels this equipment will help,” the broker can say that the owner mapped projected cash generation by period, applied a discount rate, and evaluated the project against the upfront investment.

That doesn't guarantee approval. It does something more important. It changes the broker's position from messenger to analyst.

A lender may still challenge assumptions. Good. That's the right kind of conversation. The broker who can explain the logic behind the cash flow forecast, the timing, and the investment case has a much better chance of being taken seriously.

Why this example matters

Most brokers never formalize this step. They rely on borrower confidence, basic bank statements, and lender appetite. That can produce occasional wins, but it doesn't build a durable advisory business.

A broker who uses PI in situations like this develops sharper instincts. Some projects deserve aggressive pursuit. Some need revised loan terms. Some shouldn't be financed at all. Learning to tell the difference is where long-term broker growth starts.

Interpreting the PI How to Make the Right Call

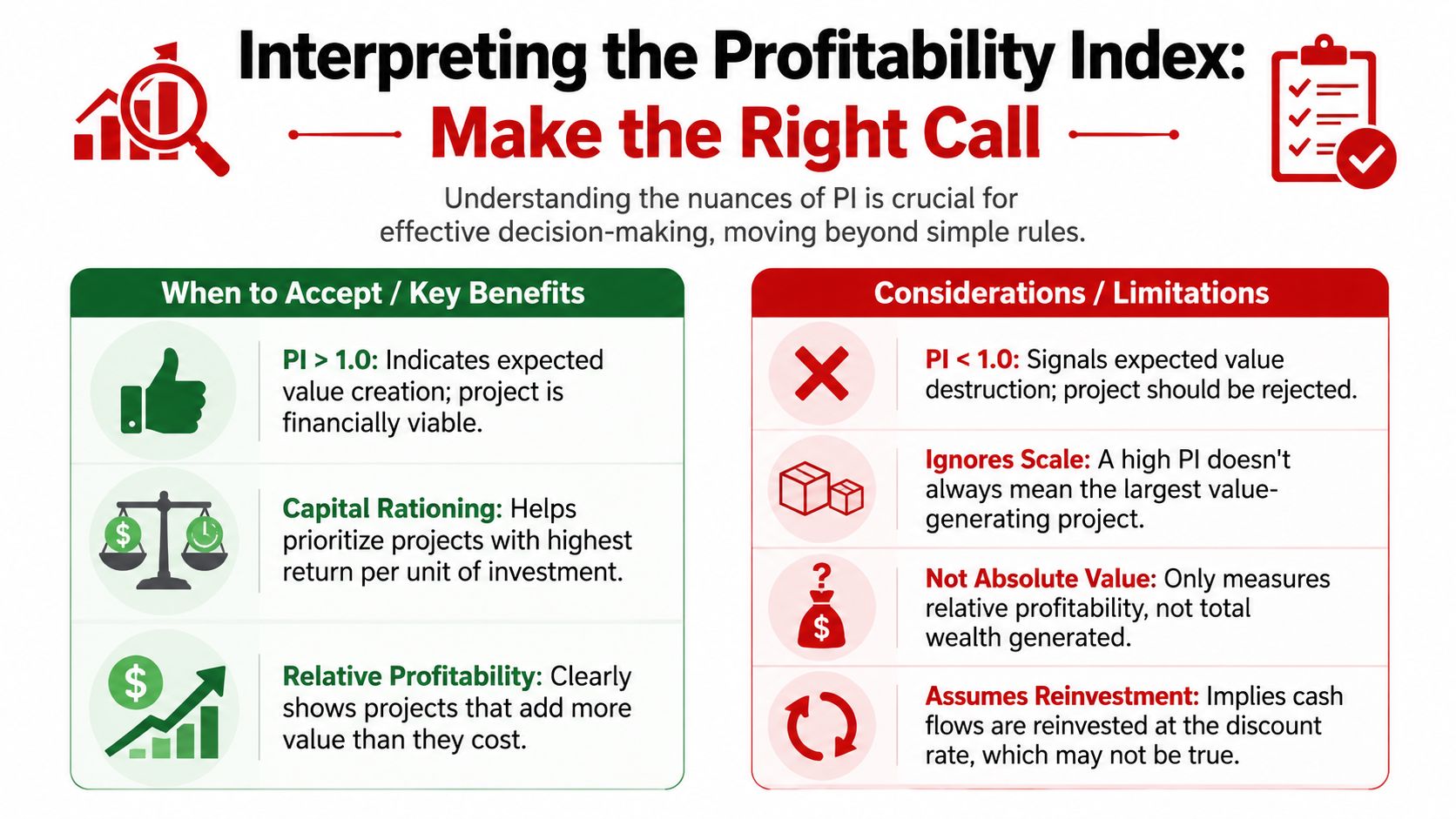

Calculating PI is useful. Interpreting it well is where judgment shows up.

The basic decision rules are straightforward. A PI above 1.0 means the project creates more present-value benefit than it costs. PI = 1.0 is breakeven. PI below 1.0 suggests the project destroys value. Those principles come directly from the same Wall Street Prep framework discussed earlier.

The decision rules that matter

A broker can use PI as a quick screen, but the interpretation should stay grounded.

| PI result | Practical meaning |

|---|---|

| Above 1.0 | The project appears to create value |

| Equal to 1.0 | The project appears to break even |

| Below 1.0 | The project appears to destroy value |

That sounds simple because, at one level, it is.

But the better brokers don't stop there. They also ask whether the borrower's assumptions are stable enough to trust the output and whether another project might create more total value even if its ratio is lower.

Where PI helps most

PI is especially useful when a client has more than one possible use of capital and can't pursue all of them at once. In that setting, PI helps rank opportunities by return efficiency.

That's valuable in practical scenarios. Borrowers often face capital rationing even when they qualify for financing. They may need to choose between equipment, expansion, inventory, or process upgrades. PI helps compare those opportunities on a value-per-dollar basis.

A broker who also understands repayment capacity can pair this insight with operating credit analysis, including the mechanics behind debt service coverage ratio calculation. PI asks whether the project appears worth funding. Debt service coverage asks whether the business can carry the payment burden. Good advisory work uses both lenses.

A project can look efficient on paper and still create strain if the repayment structure doesn't fit the business.

Where brokers get into trouble

The most common interpretation mistake is treating PI as the only answer. It isn't.

Wall Street Prep specifically notes that PI can favor smaller projects with higher ratios over larger projects with greater absolute value. That's why final selection should still be checked against NPV, especially when multiple projects compete for capital. PI measures value per dollar invested. It doesn't measure total wealth creation by itself.

Another problem is false precision. A broker can build a neat ratio on top of weak assumptions and end up sounding more certain than the facts justify.

A disciplined broker avoids that by stress-testing the logic:

- Challenge the forecast: Are the cash flows tied to real operating changes?

- Challenge the timing: Are inflows arriving soon enough to justify the model?

- Challenge the scale issue: Is a higher-ratio project the best use of capital overall?

Used this way, PI becomes a decision aid. Used carelessly, it becomes a misleading badge of sophistication.

Turn Financial Insights into a Thriving Broker Business

A broker who knows how to find profitability index brings a different kind of value to the table. The conversation stops being only about rates, terms, and lender appetite. It starts including capital efficiency, project quality, and whether the proposed use of funds makes financial sense.

That matters for business building. Clients remember the broker who helped them think clearly, not just the broker who forwarded an application. Referral partners remember the broker who screens deals intelligently and protects relationships by sending better opportunities forward.

What this skill does for a broker's business

Used consistently, PI helps a broker:

- Filter deals earlier: Time goes toward opportunities with a stronger economic case.

- Strengthen lender narratives: The use of proceeds is tied to a reasoned investment argument.

- Deepen client trust: The broker becomes more than a funding intermediary.

- Build repeatable advisory habits: Strong analysis leads to stronger referrals over time.

A broker doesn't need a traditional finance background to work this way. What's needed is a repeatable framework, disciplined questioning, and a willingness to go beyond surface-level deal packaging.

Better analysis creates better positioning

This is also where simple support tools can help. A borrower who struggles to organize financial statements may benefit from a lightweight tool for financial insights before the broker starts mapping project cash flows. Clean inputs don't guarantee a good deal, but messy inputs almost always slow one down.

The larger point is straightforward. Financial insight compounds inside a brokerage business. Every time a broker explains a deal more clearly, qualifies an opportunity more intelligently, or helps a client avoid a poor capital decision, that broker becomes easier to refer and harder to replace.

The brokers who last in this business don't build on hype. They build on judgment.

If building that kind of brokerage business sounds appealing, the next move is simple. Watch the free training from Business Lending Blueprint or schedule a strategy session to see how to launch and grow a home-based business loan brokerage with the right systems, lender access, and mentoring.