A founder sits at a laptop with a solid idea, a rough budget, and a growing sense that the funding world was designed to confuse people. The business plan looks promising. The market makes sense. The numbers seem reasonable. Then the applications start, the questions get technical, and the rejections feel personal.

That founder usually asks the same things. Where should the money come from first? Which options are real for a startup with no track record? What gets approved before revenue exists? What should never be pursued because it wastes time?

Those are the right questions. Small business funding for startups isn't just about finding money. It's about matching the stage of the business to the right capital source, avoiding dead ends, and presenting the deal in a way lenders or investors can say yes to. Most founders don't fail because they lack effort. They fail because they chase the wrong funding too early, or they approach the right funding badly.

There's also a second reality hiding in plain sight. Because this process is messy, technical, and fragmented, a skilled intermediary can create serious value by guiding founders to the right funding path. That intermediary is often the person who gets paid to solve a problem business owners urgently need solved.

Table of Contents

- The Startup Dilemma Navigating the Funding Maze

- Why Traditional Banks Arent Built for Startups

- Your Complete Map of Startup Funding Options in 2026

- Securing Funds with No Revenue or Collateral

- How to Prepare Your Application for Success

- The Secret Weapon The Business Funding Broker

- Build Your Blueprint for a Profitable Broker Business

The Startup Dilemma Navigating the Funding Maze

A startup founder usually starts with confidence and ends up in confusion. The idea may be clear. The offer may be strong. But funding changes the tone fast because capital isn't one market. It's a maze of lenders, programs, investor types, eligibility rules, underwriting logic, and timing problems.

One founder might need a modest amount to buy equipment and launch. Another may need enough runway to build product, hire carefully, and survive the first year. A third may already have demand but still lack collateral, financial history, or the kind of projections a bank wants. All three need money. None should pursue the same solution.

The real problem isn't effort

Most startup advice is too generic to be useful. It tells founders to polish a business plan, improve credit, and keep applying. That sounds responsible. It's also incomplete.

A startup can do everything “right” and still hit a wall because early-stage businesses don't fit traditional funding boxes. The founder then mistakes a structural problem for a personal one. That's where frustration turns into bad decisions, including stacking the wrong debt, chasing unrealistic investors, or wasting months on applications that were never viable.

Most founders don't need more motivation. They need a funding map that matches how startup capital actually works.

Why this gets expensive fast

Bad funding decisions don't just delay growth. They distort the business. Founders under-raise, overpay, give up equity too early, or burn time on sources that were never meant for businesses at their stage.

That's why small business funding for startups has to be approached strategically. The right question isn't “Where can a startup get money?” The right question is “Which capital source fits this exact company, right now, with the least long-term damage?”

That shift matters. It turns funding from a desperate search into a sequence of decisions. And once that sequence becomes clear, startups stop guessing.

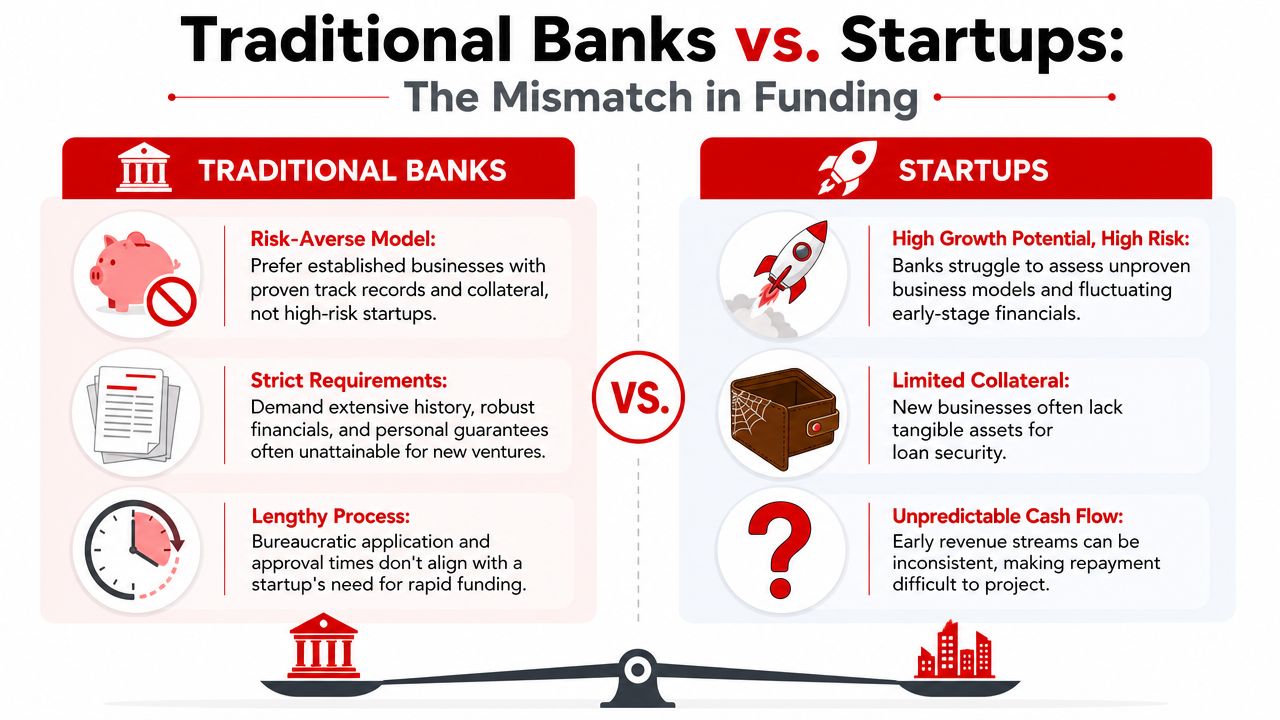

Why Traditional Banks Arent Built for Startups

Banks still carry the aura of legitimacy. Many founders assume a business loan should start there. That assumption costs time.

Traditional banks aren't built to fund uncertainty. Startups are uncertainty. That mismatch is the whole story.

The bank model conflicts with the startup profile

A new business usually has limited operating history, little or no collateral, uneven early cash flow, and financial projections that depend on execution rather than proven results. A bank underwriter sees that and reads risk, not potential.

For startup small businesses, the main barrier is the lack of historical credit performance and tangible asset collateral, which drives a denial rate exceeding 75% for businesses under two years old. Banks also often require a minimum credit score of 680 and three years of positive cash flow before they're comfortable moving forward. Those facts alone explain why so many founders get rejected before the conversation really starts.

A founder may hear “not enough history,” “insufficient collateral,” or “cash flow doesn't support repayment.” The wording changes. The logic doesn't.

Banks want proof that startups don't yet have

Banks prefer businesses that can document stable operations. They want records, not promises. That's rational for them. It's terrible for early-stage founders.

A startup often needs capital before the track record exists. That creates the classic funding trap. The business needs money to build history, but the lender wants history before offering money.

Here's what banks usually want to see:

- Operating consistency: Several years of business performance, not a promising launch plan.

- Cash flow visibility: Predictable revenue that supports debt repayment.

- Asset support: Equipment, property, or other collateral they can underwrite against.

- Clean borrower profile: Strong personal credit and fewer open questions.

Practical rule: A bank rejection usually means the deal is outside that institution's model. It doesn't mean the business is unfundable.

The smarter move is to pivot early

Founders waste months trying to force a bank fit that isn't there. Smart founders pivot early to funding channels designed for newer businesses, thinner files, or founder-led underwriting.

That's where alternative lending, microloans, targeted startup programs, and structured broker support become valuable. The founder stops asking a bank to behave like an investor or a startup lender. Instead, the founder starts matching the business to the capital source that funds this stage of risk.

Your Complete Map of Startup Funding Options in 2026

A founder sits down to raise $75,000 and starts with the wrong question. They ask which funding source sounds best. The right question is which funding source fits the stage, the risk, and the use of funds.

That distinction saves time, protects equity, and keeps a young company from taking expensive money for the wrong reason. It also points to a clear business opportunity for anyone who wants to broker funding deals. Founders are overwhelmed by choice. A broker who can match startup profile to capital source solves a real problem and gets paid for judgment, packaging, and access.

Analysts at this startup funding data summary found that founders still rely heavily on personal funds early, while loans, credit cards, and credit lines make up a large share of financing for new firms. The takeaway is simple. Startup funding is usually layered, and debt enters the picture much earlier than founders expect.

The funding options founders actually use

| Funding Type | Typical Amount | Best For | Key Pro | Key Con |

|---|---|---|---|---|

| Bootstrapping | Varies | Proof of concept and early control | No outside approval required | Limited runway |

| Friends and family | Varies | Very early launch capital | Flexible terms if structured well | Personal relationship risk |

| Angel investment | £25,000 to £500,000 | Startups with strong upside and story | Can bring capital and guidance | Equity dilution |

| Venture capital | Often at least £250,000 focus | High-growth companies needing scale capital | Large checks possible | Hard to access and highly selective |

| SBA microloan | Up to $50,000 | Early-stage businesses with modest capital needs | Designed for startups and expansion | Smaller funding ceiling |

| SBA 7(a) or similar loan | Varies | Businesses with stronger projections and repayment path | More established lending channel | Underwriting is stricter |

| Alternative term loan or line of credit | Varies | Startups shut out by banks but needing working capital | Faster and more flexible than bank paths | Pricing can be higher |

| Revenue-based financing | Varies | Businesses with revenue that want non-bank capital | Repayment tied to revenue flow | Not ideal for pre-revenue companies |

| Grants | Varies by program and industry | Specific use cases, often targeted | Non-dilutive funding | Highly restrictive and competitive |

| Crowdfunding | Varies | Consumer-facing brands and audience-driven launches | Validates demand while raising capital | Requires marketing execution |

Which option fits which startup

Bootstrapping and personal cash

This is the first money in for a lot of startups because it buys speed. It also keeps control in the founder's hands. Use it to hit a milestone that makes the next round easier, not to carry payroll forever.

Friends and family

This can be excellent seed capital if the paperwork is clean. If it is informal, it creates confusion, resentment, and future cap table problems. Smart founders document terms from day one. Smart brokers insist on it.

Angel investors

Angel money fits startups with a believable growth story and a founder who can explain exactly what the capital will do. The check can be large enough to change the company's trajectory, but angels still expect discipline. Story matters. So does use of proceeds.

Venture capital

Too many founders chase VC because it sounds ambitious. It is a narrow path built for a small slice of startups, usually the ones with outsized growth potential and a credible case for scale. Founders working on attracting venture capital should treat it as a specialized strategy, not the default answer to every funding need.

SBA loans and startup debt

These programs work best when the founder has decent credit, a specific need for funds, and a repayment plan that holds up under scrutiny. They are often more practical than equity for founders who want to keep ownership. For startups exploring debt options without pledging hard assets, this guide to unsecured business loans for startups gives a useful starting point.

Alternative term loans and lines of credit

These products matter because they fund deals banks pass on. They can cover inventory, working capital gaps, equipment, or launch expenses when timing matters. They can also hurt a startup fast if the structure is wrong. That is exactly why a good broker has value. Matching purpose, term, and cost is where money is made and bad deals are avoided.

Revenue-based financing

This fits companies that already have sales coming in and want payments that rise and fall with revenue. It is not a pre-revenue solution. It is a cash flow tool for startups with traction and healthy margins.

Grants

Founders waste too much time here. Grants exist, but usually for specific industries, demographics, research activity, or local development goals. If the business clearly fits the program, apply. If not, move on.

Crowdfunding

Crowdfunding works best when the product is easy to understand and the founder can market aggressively. It raises money, but it also tests demand in public. A weak campaign often exposes a weak offer.

The right funding choice is the one that matches the company's stage, use of funds, and tolerance for repayment or dilution. A founder who understands that gets funded faster. A broker who can explain it clearly builds a profitable business around that skill.

Securing Funds with No Revenue or Collateral

This is the question most founders care about. Can a startup get funded before revenue exists and without assets to pledge? Yes, but not by pretending to be a mature company.

The earliest-stage funding market rewards founders who choose the right channel. It punishes founders who apply blindly.

What works before traction exists

One of the clearest paths is the SBA Microloan Program. It exists specifically to help small businesses start up and expand, with loans of up to $50,000, as noted in Third Way's analysis of underserved business capital. That matters because many founders don't need a huge round. They need enough to launch, test, and survive long enough to generate proof.

Nonprofit and community-based lenders also matter more than many founders realize. They often look beyond the standard bank checklist and focus more on the founder, the plan, and the local impact. That makes them far more relevant for very young firms than traditional banks.

A founder trying to improve approval odds should also understand how lenders increasingly think about nontraditional borrower signals. This article on alternative data for credit scoring gives useful context for how underwriting can stretch beyond a simple old-school credit file.

What lenders evaluate instead

If there's no revenue and no collateral, the file has to become stronger somewhere else. That usually means four things.

- Clear use of funds: Lenders want to know exactly what the capital will do. “Working capital” alone is weak. Inventory, equipment, launch costs, or a defined operating buffer is stronger.

- Founder credibility: Industry experience, execution ability, and a coherent plan matter more when the business itself has limited history.

- Reasonable projections: Forecasts don't need to look glamorous. They need to look believable.

- Personal financial strength: When the company is new, the founder's personal profile carries more weight.

Early-stage lenders often fund the founder's preparedness as much as the business itself.

The biggest mistake at this stage is chasing capital that requires traction the startup doesn't yet have. The better move is to seek smaller, more realistic funding first, hit a milestone, then use that milestone to qualify for better capital later. That sequence is how unfundable-looking startups become financeable.

How to Prepare Your Application for Success

A weak application doesn't always mean the business is weak. It often means the file is sloppy, incomplete, or financially unconvincing. Founders lose approvals because they submit hope instead of a lending case.

Preparation fixes that.

Build a lender ready file

Start with the basics. Every founder seeking small business funding for startups should prepare a compact, organized funding package.

That package should include:

- A lean business plan: Not a bloated document. Just a clear description of the business, target market, offer, leadership, and use of funds.

- Financial projections: Monthly assumptions that show how revenue is expected to develop and where cash goes.

- Personal financial information: Many startup applications lean heavily on the owner's personal profile.

- Business formation documents: If the entity exists, the paperwork should be clean and current.

- A debt snapshot: If the founder carries obligations personally or through the business, they should be documented clearly.

For founders building organized reporting, simple operational tools like bank reconciliation templates for Excel can help keep financial records consistent before those records go into a lender file. Clean books don't guarantee approval. Messy books absolutely hurt it.

Model repayment before asking for money

One of the most overlooked technical issues is debt service coverage. Startups seeking SBA 7(a) funding often need to demonstrate a Debt Service Coverage Ratio of at least 1.25x, meaning operating cash flow should exceed debt obligations by 25%. If projections don't show that, denial becomes much more likely.

That's why a founder shouldn't just ask, “How much can be borrowed?” The better question is, “What payment can the business reasonably support?” When the repayment logic is sound, the request becomes credible.

A good supporting exercise is to build a proper debt schedule before applying. It forces the founder to list every obligation, understand payment stacking, and see how new financing affects overall cash flow.

Underwriting insight: Projections should be conservative enough that a lender believes them, but detailed enough that repayment looks planned, not guessed.

Strong applications also tell a simple story. Who is the founder? What problem does the business solve? Why does this amount of capital make sense now? Why will repayment or growth be feasible? If that story can't be explained clearly, the application isn't ready.

The Secret Weapon The Business Funding Broker

Founders usually discover the need for a broker after wasting time. They apply in the wrong places, misunderstand lender requirements, and get inconsistent answers from people who don't understand startup funding.

That's where a business funding broker becomes useful. Not as a magician. As a translator and strategist.

Why founders need a guide

The funding market is fragmented. One lender likes stronger credit. Another likes specific industries. Another may tolerate limited time in business if the rest of the file is compelling. A founder rarely knows these distinctions in advance.

A broker shortens that learning curve. The broker helps package the deal, match it to the right capital source, and filter out options that were never likely to work. That saves time, reduces unnecessary credit hits in some scenarios, and gives the founder a more rational path through the market.

That role matters because 38% of startup failures are tied to running out of cash or failing to raise new capital, according to small business startup data compiled here. When capital access determines survival, guidance has real economic value.

Why this is also a business opportunity

This same complexity creates a legitimate home-based business for the person who learns the funding environment well. Startups need help. Established small businesses need help. Banks say no all the time. Alternative lenders and specialized programs still need qualified deals. Someone has to sit in the middle and make the match.

That someone can build a brokerage around:

- Referral relationships: Accountants, consultants, real estate professionals, and service providers all know business owners who need capital.

- Application support: Many owners need help assembling a fundable file.

- Capital matching: The broker becomes the person who knows which deals fit which products.

- Repeat business: One funding need often turns into future lines, expansion capital, equipment financing, or referral opportunities.

A person exploring this path should study the business model carefully, including how brokers structure offers, relationships, and positioning. This overview of business loan broker salary helps frame the economics without pretending the work is passive or automatic.

Business Lending Blueprint is one training option in this space. It teaches people how to launch a business loan brokerage, work with a lender network, and build a referral-driven model around helping businesses secure funding. That's relevant here because startup funding is hard enough that real guidance creates genuine demand.

The broker doesn't create money. The broker creates clarity, access, and fit. That's why the role gets paid.

Build Your Blueprint for a Profitable Broker Business

A founder gets turned down by a bank on Monday, finds an online lender on Tuesday, and still has no idea which offer will help the business instead of trapping it in expensive debt. The person who can sort that out has a real business.

That is the broker opportunity.

A profitable brokerage exists because startup funding is confusing, fragmented, and full of bad fits. Founders need someone who can size up the deal, clean up the file, choose the right capital source, and present the application properly. For an aspiring intermediary, that creates a service business with clear demand and repeat revenue.

A practical path into the industry

Treat this like an advisory business from day one. Serious brokers learn products, underwriting logic, documentation standards, lender preferences, and referral development. That knowledge is what turns a random lead into a funded client and a one-time client into a long-term account.

The fastest path is to build around relationships and process. Accountants, tax preparers, consultants, insurance agents, and other business service providers already know owners who need capital. Your job is to become the funding specialist they trust to assess deals, package them correctly, and place them with the right funding source.

Lead flow matters too. A broker who wants steady deal volume needs outreach that starts conversations with founders and referral partners. For ideas on building that pipeline, review this guide for B2B lead generation for startups.

The business model is attractive for a reason. You are not inventing demand. You are stepping into a market where startups need guidance, lenders want cleaner submissions, and both sides benefit when someone experienced handles the process well.

Business Lending Blueprint teaches people how to start and grow a business loan brokerage from home, build referral relationships, and help startups and small businesses access funding across multiple products. If that model fits your goals, review the training and decide whether you want to build a brokerage that gets founders funded and gets paid for creating that result.