A new loan broker sees this constantly. Two business owners submit applications. Both say the company does about the same annual revenue. Both sound confident on the phone. Both want fast funding.

Then the statements arrive.

One business collects what it sells, manages discounts tightly, and leaves room for payroll, marketing, and debt payments. The other gives away margin through refunds, credits, markdowns, and pricing concessions that looked harmless one invoice at a time. On paper, the top line looks similar. In lending, they are not the same borrower.

That gap is where many brokers lose deals they should have screened out earlier, or miss deals they could have structured better. Understanding net revenue vs gross revenue isn't accounting trivia. It's a practical underwriting skill. It helps brokers spot risk sooner, frame files more credibly, and guide business owners toward funding options that match the reality of the business rather than the optimism of a sales report.

Table of Contents

- The Hidden Story in a Company's Revenue

- Understanding Gross Revenue The Top Line Story

- Decoding Net Revenue The Money a Business Actually Keeps

- Gross Revenue vs Net Revenue A Side by Side Comparison

- How Lenders and Brokers Analyze Revenue for Risk

- Using Financial Insights to Grow Your Broker Business

- Become the Go-To Financial Expert for Business Owners

The Hidden Story in a Company's Revenue

A revenue figure without context can mislead a broker fast.

A business owner may proudly report annual sales, and that number can sound strong enough to support a working capital request. But lenders don't fund pride. They fund businesses that can convert sales activity into usable income and stable repayment capacity.

Same sales story different lending outcome

Consider two applicants with identical top-line billing. One runs a disciplined operation with few post-sale adjustments. The other relies on constant discounts to close deals and deals with frequent returns or credits after the sale. A broker who looks only at gross sales might treat both files the same, send both to the same lenders, and wonder why one gets traction while the other stalls.

The difference usually shows up in what the business retains from its sales.

Practical rule: Revenue tells a story, but retained revenue tells a lender whether that story can support debt.

That distinction changes the broker's role. Instead of acting like an order taker, the broker starts thinking like a credit advisor. Which number reflects operating reality? Which number belongs in the discussion with a lender? Which number should shape expectations before the application ever goes out?

Why this matters to a broker business

Brokers who catch this early save time on weak files and build credibility on strong ones. They ask better questions, request better documentation, and present cleaner narratives to funding partners.

That skill compounds in a referral-driven business. Accountants, consultants, and business owners remember the broker who explains why a deal is fundable, not just the broker who forwards an application. Over time, that creates stronger lender relationships and more repeatable deal flow.

Early in the conversation, the revenue label matters less than the quality of the revenue underneath it.

| Metric | What it shows first | What it can hide | Why a broker should care |

|---|---|---|---|

| Gross revenue | Sales activity and market demand | Returns, discounts, credits, and allowances | Useful for initial screening and market context |

| Net revenue | Revenue the business actually keeps after deductions | Whether the top line overstated capacity | More relevant for repayment analysis and deal positioning |

Understanding Gross Revenue The Top Line Story

A borrower sends over revenue numbers that look strong on first pass. The top line is big, the owner sounds confident, and the deal feels alive. Then the file gets tighter once you ask what portion of those sales held after credits, discounts, and returns. That is why gross revenue matters to a broker, but only if you treat it as an entry point rather than a conclusion.

Gross revenue is the total value of sales before any deductions. It shows what the business billed or rang up before post-sale reductions change the picture. For brokers, that makes gross revenue useful in the first screening conversation because it helps size the business, frame the opportunity, and test whether there is enough sales activity to justify a lending discussion at all.

It also tells you something practical about the sales engine.

A healthy gross figure can point to steady demand, repeat customer activity, or a business that has gained real traction in its market. That matters because lenders still want to see commercial momentum, even when they know the top line is not the same as repayment strength. If a client cannot produce meaningful sales volume, there may be no deal to structure in the first place.

Gross revenue is especially useful early when financials are incomplete. A new broker can use it to sort leads faster, ask better follow-up questions, and decide whether to spend time collecting a full package. Owners usually know this number off the top of their head, which makes it a practical starting point in discovery calls.

What it does not tell you is just as important.

Gross revenue does not show how much of those sales stuck, how much was given back through concessions, or how much volatility sits behind the billing pattern. A business can post an impressive top line and still create problems for underwriting if too much revenue gets reversed after the sale. That is where newer brokers get into trouble. They present scale when the lender is really testing quality.

For readers working across markets, Turnover vs Revenue UK helps clarify a common terminology issue. Many owners use turnover and revenue as if they mean the same thing, and brokers need to pin down the exact definition before positioning a file.

If you want a sharper framework for reading the sales line the way credit teams do, review this guide to what top-line revenue means in lending analysis. It helps separate a headline sales figure from a number that can support a financing case.

The practical takeaway is simple. Gross revenue helps you identify opportunity, measure market activity, and open the conversation. It should never be the last number you rely on when you decide whether a client is financeable.

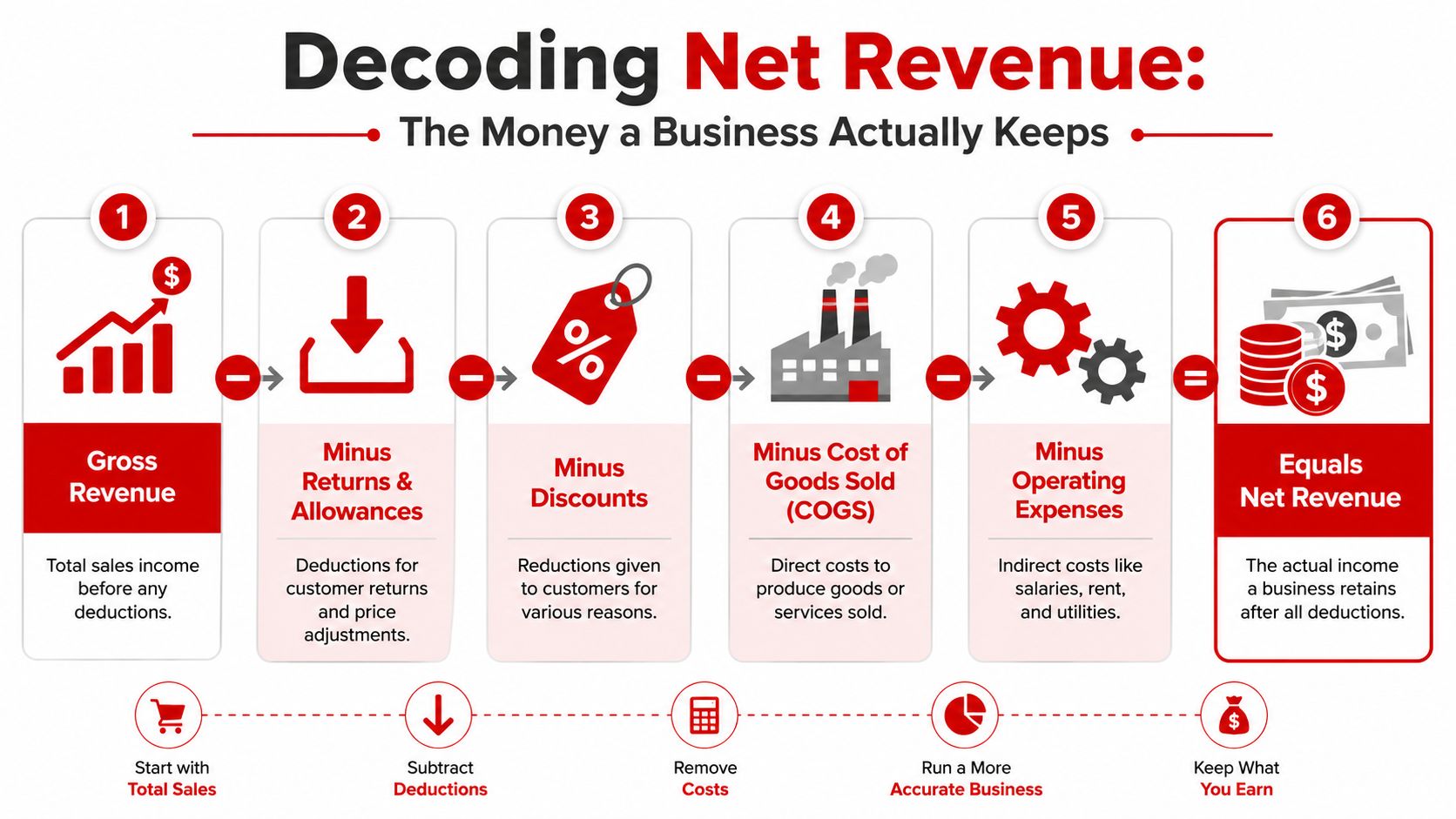

Decoding Net Revenue The Money a Business Actually Keeps

A borrower shows you strong sales, clean bank deposits, and real demand. Then underwriting finds a steady stream of returns, credits, and price concessions buried in the statements. The deal does not fall apart because the company lacks customers. It gets harder because too much of the original sale never sticks.

That is what net revenue exposes.

Net revenue is the sales income a business keeps after deductions tied directly to those sales, such as returns, discounts, allowances, refunds, and credits. For a broker, that number matters because it speaks to revenue quality, not just revenue volume. A company can sell aggressively and still leave very little usable income once post-sale reductions are accounted for.

How net revenue is calculated

The formula is simple. The interpretation is where brokers earn their keep.

- Gross revenue

- less returns

- less allowances

- less discounts

- less similar post-sale reductions

For example, a company may invoice $1,000,000 in gross revenue and give back $60,000 through returns and discounts. Net revenue is $940,000. That missing $60,000 affects more than presentation on a P&L. It changes how much income is available to cover payroll, marketing, inventory, and debt service.

This is also where newer brokers confuse net revenue with net income. They are not the same. Net revenue is still a sales measure. It does not subtract operating expenses, interest, taxes, or owner distributions. If you want to understand how existing obligations fit into the picture, review how a debt schedule helps lenders map current liabilities.

Why lenders care about net revenue

Credit teams use net revenue to test whether reported sales hold up under normal business friction. That matters in files where returns are common, pricing is flexible, or contracts include frequent credits. A wide gap between gross and net can signal weak controls, customer churn, fulfillment issues, or an operator who buys volume by cutting price too often.

Good brokers do not treat that gap as an automatic decline.

They treat it as a diagnostic tool. If the deductions are normal for the model and management can document them clearly, the file may still fit the right lender. If the owner cannot explain the pattern, you have found a risk issue early, before you burn credibility with underwriting.

What the spread between gross and net revenue can reveal

A larger spread usually points to one of a few business realities:

- High return volume: Often tied to product quality, fulfillment mistakes, or weak customer fit.

- Heavy discounting: Can keep sales moving while compressing retained revenue and future margins.

- Frequent credits or allowances: Often linked to service disputes, billing errors, or contract slippage.

Those details help with placement strategy. A lender focused on stable recurring collections may view these patterns differently than a lender comfortable with seasonal or transaction-heavy businesses. That is one reason brokers who understand business loan requirements in Australia and similar market-specific standards can frame revenue quality more effectively.

The practical lesson is straightforward. Gross revenue helps you spot activity. Net revenue helps you judge whether the business keeps enough of that activity to support a loan, protect lender confidence, and give you a stronger case to take to market.

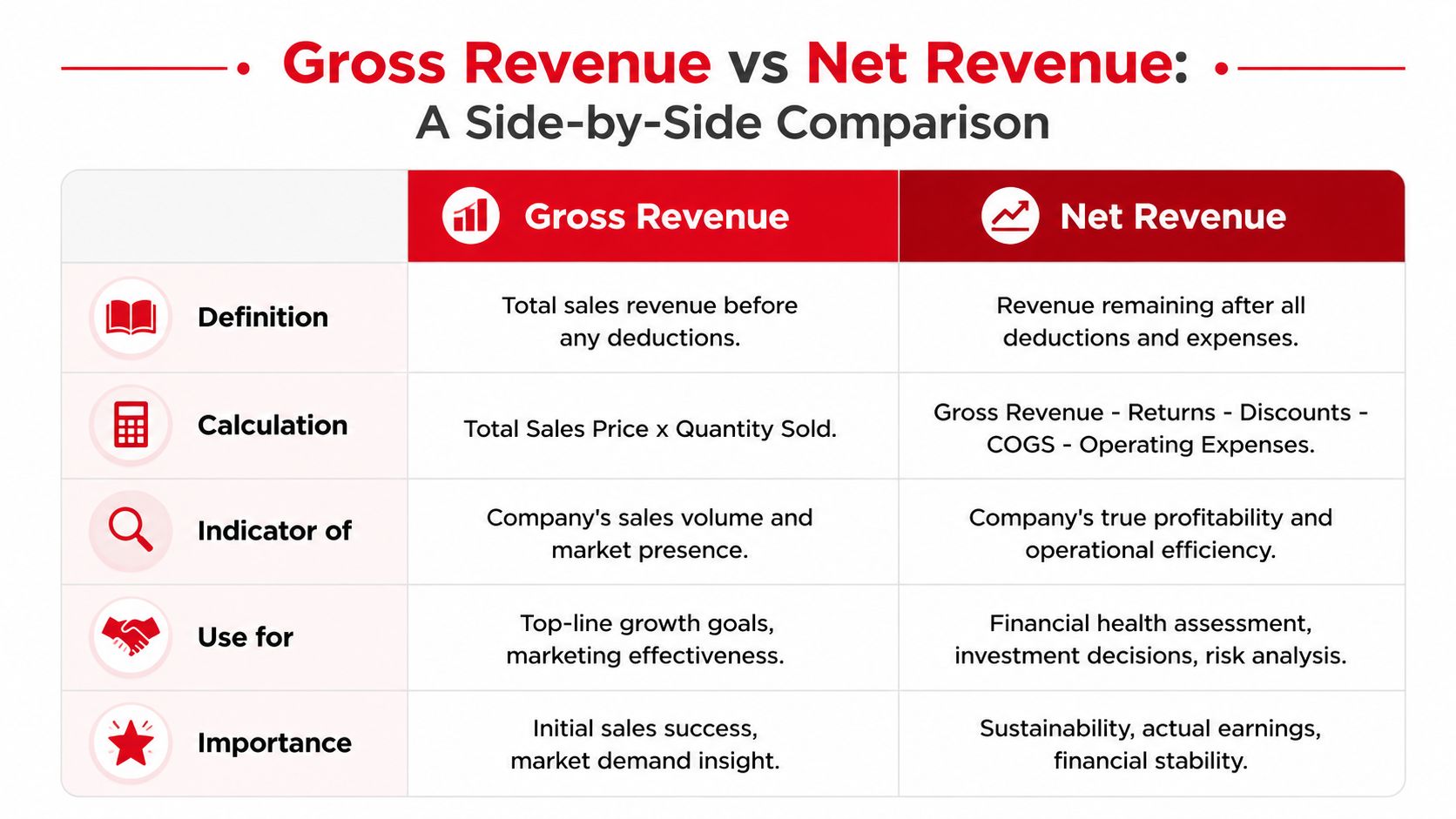

Gross Revenue vs Net Revenue A Side by Side Comparison

Many owners talk about revenue as if it were one clean number. In practice, net revenue vs gross revenue is a distinction between activity and retained value. Brokers who keep that difference clear ask better questions and package deals with fewer surprises.

Quick comparison for brokers

| Criteria | Gross revenue | Net revenue |

|---|---|---|

| Basic meaning | Total sales before deductions | Revenue remaining after sales-related reductions |

| Primary signal | Demand and sales volume | Retained income from sales |

| Best use | Early screening and market context | Underwriting context and repayment discussion |

| Who leans on it most | Sales-focused operators | Finance-focused decision makers |

| Main broker question | How much did the company sell? | How much of that revenue actually stayed? |

That table is simple by design. In lending, simple frameworks are useful because brokers often review files quickly and need a fast way to separate presentation from substance.

The practical decision rule

Gross revenue helps answer whether a company can generate business. Net revenue helps answer whether the company can keep enough of that business to support financing.

Those are different questions. A broker who blends them together may overestimate borrower strength. A broker who separates them can explain a file in terms a lender respects.

Underwriting lens: Gross revenue opens the file. Net revenue shapes the conversation.

This distinction also helps when a client uses terms loosely. Some owners mix revenue, turnover, sales, and receipts in the same conversation. Others confuse net revenue with profit. A broker doesn't need to correct them harshly, but the broker does need to translate their language into the right financial category before presenting the file.

For readers who deal with tax-inclusive and tax-exclusive language, this explainer on net of VAT for UK freelancers can help clarify why “net” means different things in different contexts and why precision matters when discussing business financials.

Why this comparison affects product fit

Some funding products are more forgiving of uneven top-line performance than others. Some lenders care more about consistency in collected revenue than headline sales. That is why a broker shouldn't choose a funding path based only on what sounds impressive in the intake call.

This is especially relevant when evaluating revenue-based financing, where the shape and quality of revenue often matter as much as the size of the sales number itself.

How Lenders and Brokers Analyze Revenue for Risk

A borrower says the company does $300,000 a month in sales. The statement looks impressive at first glance. Then the processing reports show refunds, chargebacks, and pricing concessions that cut significantly into what the business ultimately collects. That is the point where a file shifts from attractive to questionable, and a good broker catches it before the lender has to.

Lenders review revenue with caution because top-line sales do not make loan payments. Retained revenue does. The gap between the two helps underwriters judge whether the business has enough real earning power to support new debt without creating stress a few months after funding.

Why a large gap gets attention

A wide spread between gross revenue and net revenue usually points to something operational, not just something accounting-related. Returns may be high. Discounts may be carrying too much of the sales load. Collections may be weaker than the owner realizes. Each of those affects risk differently, and each one changes how a broker should position the file.

For lenders, the concern is straightforward. If a business regularly gives back a meaningful share of its sales, then gross revenue overstates repayment capacity. A borrower can look large on paper and still have thin room for debt service once the normal revenue leakage shows up.

For brokers, this determines whether money is made or lost. A weak file sent out with no explanation damages credibility. The same file, framed with the right context, can still get traction with the right lender.

Questions a strong broker asks before submission

Strong brokers pressure-test revenue before the package goes out. They do not wait for underwriting to expose the problem.

Ask questions that get to the cause of the gap:

- What is creating the reductions? Returns from damaged goods tell a different story than subscription churn or frequent refund requests.

- Are discounts strategic or permanent? A short promotional period is less concerning than a business that depends on constant price cuts to close sales.

- Do bank statements and processor reports support the owner's story? If adjustments are common, the documentation should show that pattern clearly.

- Has the issue been fixed, or is it still active? Lenders treat a resolved fulfillment problem differently from a habit that shows up every month.

- What happens after debt service is added? Revenue quality matters more when the business already carries stacked obligations or uneven payment cycles.

These questions help a broker sort files faster. They also help match the borrower to a lender that prices the risk correctly instead of wasting time on avoidable declines.

What lenders are really trying to determine

Underwriters usually test three things at the same time. Is the revenue durable? Does management understand the drivers behind the numbers? Will future cash flow hold up well enough to repay the new facility?

That last point matters more than many new brokers realize. A company may have decent sales volume and still struggle if revenue swings after refunds, seasonal discounting, or customer concentration are taken into account. Once existing obligations are layered in, the margin for error gets small. That is why a clear debt schedule showing current obligations and repayment pressure adds real value to the package.

A broker earns trust by identifying weakness early, explaining it clearly, and showing why the deal still makes sense or why it should be restructured.

This is also where brokers can spot opportunities others miss. If the revenue gap is tied to a temporary issue with a clean explanation, the file may still be financeable. If the gap reflects a structural weakness in the model, the better move may be a smaller request, a shorter term, or a different product entirely.

For brokers working with international applicants, document standards can vary by market. This overview of business loan requirements in Australia shows how requirements differ across jurisdictions, even though the core credit question stays the same. Does reported revenue convert into dependable repayment capacity?

Using Financial Insights to Grow Your Broker Business

Knowing the difference between gross and net revenue only matters if it improves execution. In a broker business, this knowledge creates an edge because it sharpens qualification, improves communication with lenders, and builds trust with clients who often don't understand why one revenue number sounds strong but still doesn't produce easy approvals.

Shift from application taker to advisor

Clients notice when a broker asks more thoughtful questions than “What are your monthly sales?”

A broker who explains the revenue gap in plain language becomes more than a form processor. The conversation changes from “How much can this owner get?” to “What will a lender believe, and how should this file be positioned?” That is the kind of guidance business owners remember and refer.

Three habits help:

- Translate the numbers: Show the owner why billed sales and retained revenue lead to different funding conversations.

- Reset expectations early: If deductions are hurting the file, say it before the owner assumes every lender will ignore it.

- Document the reason: If returns or discounts are normal for the industry or tied to a temporary issue, put that explanation into the package.

Use revenue quality to match the right deal

Not every borrower needs the same structure, term, or lender audience. Brokers who understand revenue quality can sort files with more precision.

A business with stable retained revenue may fit one path. A business with noisy collections, heavy adjustments, or inconsistent post-sale reductions may need a different approach, more documentation, or a delayed submission until financial cleanup is done.

That same thinking should carry into broader cash flow analysis. A revenue number, even a good one, doesn't answer whether the company can handle another payment. Brokers who also understand debt service coverage ratio calculation are in a stronger position to test whether the deal makes sense before sending it out.

Build a brokerage that scales on credibility

The easiest way to waste time in this business is to chase every file equally. The best brokers don't do that. They identify red flags quickly, invest energy where the narrative is supportable, and protect their lender relationships by sending better-prepared opportunities.

That discipline creates practical business benefits:

- Cleaner submissions: Lenders get fewer surprises and more context.

- Higher-quality conversations: Referral partners learn that the broker can interpret financials, not just collect documents.

- More repeat business: Owners return when they feel the broker helped them understand the problem, even if the first deal wasn't ready.

A remote, home-based brokerage grows faster when the operator has a repeatable decision process. Revenue quality is one of the strongest filters in that process because it separates headline sales from financeable reality.

Become the Go-To Financial Expert for Business Owners

The value in understanding net revenue vs gross revenue isn't the definition. It is the judgment that comes from knowing which number belongs in which conversation.

Gross revenue helps identify demand. Net revenue helps reveal operating reality. Lenders care about that reality because repayment depends on what the business retains, not what it hoped to keep. Brokers who understand the difference can qualify deals faster, package them more intelligently, and explain outcomes in a way that business owners respect.

That is how a broker becomes useful in a crowded market. Not by reciting terminology, but by spotting the revenue story hidden inside the statements. A broker with that skill can identify risk earlier, uncover opportunities others miss, and build stronger long-term relationships with both borrowers and funding sources.

For aspiring brokers, this is exactly the kind of financial literacy that turns a flexible, home-based business into a credible professional practice. It supports better referrals, stronger lender confidence, and a more scalable operation because the broker isn't relying on guesswork.

Business owners need brokers who understand more than intake forms. If you're ready to learn how to evaluate deals, work with lenders, and build a real business around funding solutions, watch the free training from Business Lending Blueprint or schedule a strategy session to see how the model works.