A lot of people looking at business loan brokering right now are in the same spot. They want a business they can run from home, they want something tied to a real market need, and they don't want to spend years trying to break into an industry guarded by banks, branches, and gatekeepers.

Bank statement business loans sit right in that gap.

They solve a common problem for business owners who are generating money every month but can't prove it in the format a traditional bank wants. For a new broker, that makes this product more than a financing option. It's an entry point into a large underserved market, a practical way to help business owners get funded, and a commission-based service that can be built remotely with low overhead.

Table of Contents

- Your First Step Into a $100 Billion Funding Gap

- What Are Bank Statement Business Loans

- Identifying Your Ideal Bank Statement Loan Client

- The Underwriting Secrets Lenders Wont Tell You

- Rates Terms and Your Commission Potential

- How to Package and Submit the Perfect Deal

- Pros Cons and Critical Red Flags to Avoid

- Start Your Journey as a Business Loan Broker Today

Your First Step Into a $100 Billion Funding Gap

A restaurant owner can have tables full every night and still get declined by a bank. The reason usually isn't that the business is dead. The reason is that the tax returns don't show enough profit after deductions.

That's the core problem bank statement business loans solve.

Traditional underwriting leans heavily on tax returns, formal financials, and clean documentation. Many small business owners don't fit that mold. They write off legitimate expenses, operate with uneven monthly income, or do not have the paperwork a bank prefers. A bank sees weak reported profit. A cash flow lender sees money moving through the account.

That distinction matters if someone wants to build a brokerage business around real demand instead of hype.

Practical rule: Follow the businesses that are earning but not presenting well on paper. That's where this product becomes useful, and where a broker becomes valuable.

Think of it this way. Profit on a tax return is an accounting result. Cash flow in a bank account is operating reality. A company can look thin on paper and still have enough steady deposits to support repayment. When a lender underwrites the movement of money instead of waiting for CPA-packaged statements, more businesses become financeable.

For a trainee broker, this creates a workable niche:

- Remote service model: Conversations, document collection, follow-up, and lender communication can all be handled from a home office.

- Referral potential: Accountants, consultants, real estate professionals, and service providers all know business owners who get turned down elsewhere.

- Repeat relevance: Clients who use one financing product often need another later, whether that's working capital, expansion funding, or a line of credit.

The opportunity isn't in selling a loan. It's in understanding why a borrower was declined, knowing which files can be repositioned, and matching that borrower to a lender that underwrites cash flow instead of paper profit.

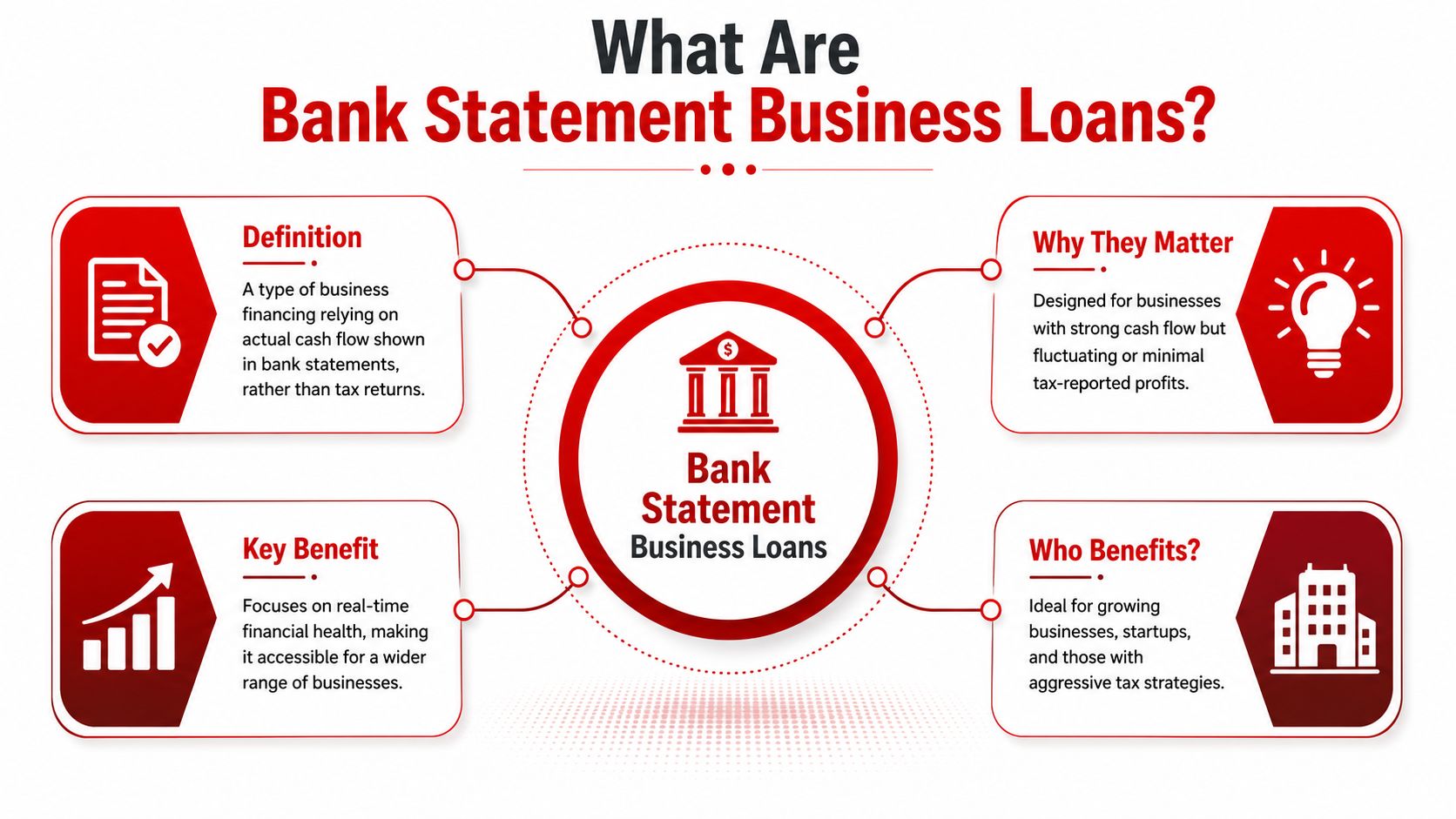

What Are Bank Statement Business Loans

Bank statement business loans are financing products built around actual deposits and account activity instead of traditional tax-return underwriting. Lenders review 3 to 6 months of transaction-level bank data, often require a minimum credit score of 600, and use consistent deposit patterns to estimate monthly revenue without formal profit-and-loss statements. That process can reduce processing time to 2 to 14 days because lenders pull income sources, expense categories, and balances directly from digital statements rather than relying on CPA-reviewed financials, according to Fora Financial's overview of business bank statement loans.

A simple way to explain it to a prospect is this. Tax returns are a snapshot. Bank statements are a video feed. One shows what was reported after deductions. The other shows how money moved through the business.

Cash flow beats paper profit

A consultant may have strong monthly deposits but a tax return that looks weak because of deductions. An e-commerce seller may be growing fast, yet the prior filing period doesn't reflect current momentum. A contractor may have uneven draws but steady inflows over recent months.

Those borrowers often fail in traditional channels because the documents don't tell the full story.

A bank statement lender starts from a different question. It isn't “What did last year's return show after write-offs?” It's “What do the recent statements show about stable deposits, operating rhythm, and repayment capacity?”

That's also why brokers need to understand the difference between gross revenue and usable cash flow. A borrower can confuse the two and overestimate what they'll qualify for. A clear explanation of net revenue vs gross revenue helps keep the conversation grounded before the file reaches underwriting.

The client profiles that show up most often

The best prospects usually aren't failing businesses. They're businesses that don't fit bank paperwork standards.

Consider these common profiles:

- The successful consultant with high write-offs: Revenue comes in regularly, but deductions reduce reported income.

- The seasonal operator: Deposits are strong during peak months, softer during off months, and the pattern needs interpretation.

- The fast-growing seller: Recent bank activity is stronger than historical tax documentation.

- The owner with non-standard records: The business may be healthy, but the owner doesn't maintain lender-friendly financial statements.

A new broker doesn't need to become an underwriter on day one. The first win is learning to spot when cash flow tells a better story than tax returns.

That's the heart of this product. It gives brokers a way to serve borrowers who are real, active, and fundable, even when their file doesn't look conventional.

Identifying Your Ideal Bank Statement Loan Client

New brokers often think the ideal client is “self-employed.” That label is too broad to be useful.

Some self-employed borrowers are excellent fits. Others look strong at first glance and collapse in underwriting because their statements don't support the story. The broker who learns that difference early wastes less time and submits stronger files.

The mistake new brokers make

The biggest mistake is chasing revenue instead of deposit quality.

A borrower may talk about top-line sales all day long. That doesn't mean the statements will qualify well. Lenders care about how deposits land, how consistent they are, and whether business cash flow remains stable after operating activity moves through the account.

That's where the deposit dilution issue catches inexperienced brokers. Some lenders reduce the strength of a file when heavy business expenses distort net deposits, even if the company is producing meaningful revenue. This is one reason generic prospecting language falls flat. A broker needs to ask better questions before promising anything.

Four borrower profiles worth targeting

The consultant or agency owner with legitimate deductions

This borrower often looks weaker on tax returns than in real life. Marketing spend, travel, software, contractors, and other write-offs shrink reported profit, but recent deposits may still support a deal.

The seasonal business with clear operating cycles

Landscaping, hospitality, specialty retail, and similar businesses can be good prospects when the broker frames the seasonality properly. The statements have to show a pattern, not chaos.

The e-commerce or service company growing faster than its paperwork

When current bank activity is stronger than older financial documents, bank statement underwriting can better reflect what the business is doing now.

The independent contractor with mixed account habits

This is a tricky one. Independent contractors often face more scrutiny than established small business owners because some lenders view deposits as personal rather than business-related if the account setup is sloppy. A broker needs to separate “self-employed” from “cleanly documented business operator” before choosing a lender.

A practical screening conversation should focus on three things:

- Account structure: Is revenue flowing through a business account, a personal account, or both?

- Deposit rhythm: Are deposits regular enough to tell a stable story?

- Expense behavior: Are large operational outflows going to weaken the file?

The broker who identifies account habits early will save hours of unnecessary submissions later.

At this point, a home-based brokerage becomes more than lead chasing. It becomes pattern recognition. Strong brokers don't just ask whether the client needs money. They ask whether the statements can carry the request.

The Underwriting Secrets Lenders Wont Tell You

Most denials don't happen because a borrower said the wrong thing. They happen because the bank statements reveal a repayment story the borrower didn't understand.

The biggest hidden issue is the deposit dilution trap. Lenders often penalize self-employed borrowers when high business expenses reduce net deposits, even when revenue looks strong. Farm Bureau notes that 60% of small business loan applications are rejected due to cash flow concerns, including situations where lenders subtract large one-time expenses from total inflows and weaken the file as a result, as explained in its discussion of bank statement loan cash flow issues.

What lenders really review

A new broker should stop thinking in terms of “sales” and start thinking in terms of statement behavior.

Lenders usually review items like these:

| Underwriting focus | What it tells the lender |

|---|---|

| Consistent deposits | Whether income arrives in a stable, repeatable pattern |

| Large one-off expenses | Whether outflows distort usable cash flow |

| Transfers between accounts | Whether deposits are true revenue or internal movement |

| Overdraft activity | Whether the business struggles to manage liquidity |

| Account balance trends | Whether the business maintains cushion or lives too tight |

That broader framework overlaps with what banks consider for business loans, especially around repayment ability, cash management, and documentation quality. The difference is that bank statement lenders lean harder on account activity than on formal financial statements.

Another concept brokers need to understand is debt service coverage. Even when tax returns aren't driving the decision, the lender still needs to judge whether cash flow can support repayment. A practical grounding in debt service coverage ratio calculation helps a broker see the file the way underwriting sees it.

Where deals break and where brokers save them

Some files fail for reasons the client could have explained if someone had asked.

A large equipment purchase can crush one month's deposit profile. A transfer from another owned account can look like unverifiable revenue. Multiple small returns or reversals can make the account look unstable even if the business itself is fine.

Brokers earn trust not by arguing with underwriting, but by preparing the explanation before submission.

Use a short deal summary when the statements need context:

- Flag the anomaly: Identify the unusual transaction rather than hoping nobody notices it.

- Tie it to business purpose: Explain whether it was inventory, equipment, payroll catch-up, or another operational reason.

- Clarify recurring vs nonrecurring: Underwriters need to know whether the issue is a pattern or a one-time event.

- Show what's stable: Bring attention back to repeating deposits and normal operating behavior.

An underwriter doesn't need a novel. A few clean lines that explain the statement often matter more than a long sales pitch.

What doesn't work is submitting messy files, hiding weak months, or overstating revenue. That damages lender confidence quickly. A broker's reputation grows when submissions are honest, organized, and pre-screened before they ever reach a funding desk.

Rates Terms and Your Commission Potential

Clients will ask two questions quickly. What will this cost, and why wouldn't they just go to a bank?

The answer needs to be direct. Bank statement loans are usually more expensive than traditional bank financing because the lender is taking more risk with less formal documentation. But cost alone isn't the right comparison. Ultimately, the comparison is available funding versus no funding.

According to Biz2Credit, bank statement loans often carry interest rates 3% to 8% higher than traditional SBA or bank term loans, with origination fees typically ranging from 1.5% to 5%. The same source states that these loans can deliver approval rates up to 40% higher for small businesses that were declined by traditional lenders, and that traditional banks reject 80%+ of applications in this segment. It also notes a broker niche with $1K to $15K per-funded-deal margins in this market, as described in its analysis of no-doc versus bank statement loan options.

How to set expectations before submission

A broker should never wait until the offer arrives to explain the trade-off.

Use a simple client conversation:

- Start with fit: “This is a cash-flow-based product for businesses that don't qualify cleanly through traditional paperwork.”

- Frame the trade-off: “The pricing is usually higher, but access is easier when recent deposits are strong.”

- Anchor to purpose: “If the capital solves a real business problem, the cost may be justified. If the use of funds is weak, it probably isn't.”

- Set packaging expectations: “Clean statements and clear explanations improve the odds of a useful approval.”

That kind of conversation builds credibility. It also reduces fallout later.

For brokers who want a more realistic view of long-term earning mechanics, this breakdown of business loan broker salary helps connect deal flow, funded volume, and commissions without hype.

How the economics work for a broker

The opportunity here comes from market mismatch. Many borrowers can't get through a bank's filter, but they still need capital for inventory, working capital, equipment, or growth. A broker who can source those borrowers consistently has a repeatable business model.

A few operating truths matter:

- Volume beats perfection: Not every file will fund. The business grows through qualified opportunities, not emotional attachment to one deal.

- Packaging affects payouts: Better-prepared files move faster and protect lender relationships.

- Repeat clients matter: A funded borrower often returns when another financing need appears.

The best broker conversations aren't about rates alone. They're about whether the funding creates more value than it costs.

This is one reason bank statement business loans are a strong product for a home-based brokerage. The market is active, the need is ongoing, and the service can be delivered remotely with systems, referral channels, and disciplined follow-up.

How to Package and Submit the Perfect Deal

A weak deal can sometimes fund if the business is strong enough. A strong deal can still die if the package is sloppy.

Packaging is where a broker stops being a lead generator and starts acting like a professional. The lender should be able to open the file and understand the borrower quickly, without digging through random attachments and trying to reconstruct the story.

A clean file funds faster

Business loan brokers typically earn 1% to 3% of the total loan amount, paid by the lender upon closing, with the exact compensation set between broker and lender and varying by deal type and complexity, according to Bluestone Loans' guide to broker commissions. That means packaging isn't an admin task. It directly affects whether the broker gets paid.

A practical submission checklist usually includes:

- Recent bank statements: Gather the full statement set requested by the lender, not screenshots or partial exports.

- Completed application: Make sure names, business entity details, and funding purpose match the supporting docs.

- Government-issued ID: Confirm the ID is current and legible.

- Voided check or bank verification item: Use whatever the lender requests to confirm the operating account.

- Short deal summary: Explain business model, use of funds, and any statement anomalies in plain language.

A broker who wants a stronger operational framework should study a clear business loan application process and turn it into a repeatable intake system.

A simple intake script that works

A strong first call doesn't need to be flashy. It needs to surface the facts that matter.

This kind of script works well:

“How long has the business been operating? What do the monthly deposits usually look like? Are all deposits going through one main account? What is the funding for? Were there any unusual large purchases or transfers in the recent statements?”

That script does two things. It qualifies the deal, and it tells the borrower that this process is based on actual cash flow, not guesswork.

A clean comparison helps trainees understand what good packaging looks like:

| Poor submission | Strong submission |

|---|---|

| Partial statements | Full statement set in order |

| No context for odd transactions | Short written explanation included |

| Inconsistent business details | Matching details across all docs |

| Random file names | Cleanly labeled documents |

| Oversold story | Clear, supportable summary |

What doesn't work is sending files that require the lender to ask the same questions three times. That slows approvals, frustrates account reps, and weakens trust in the broker.

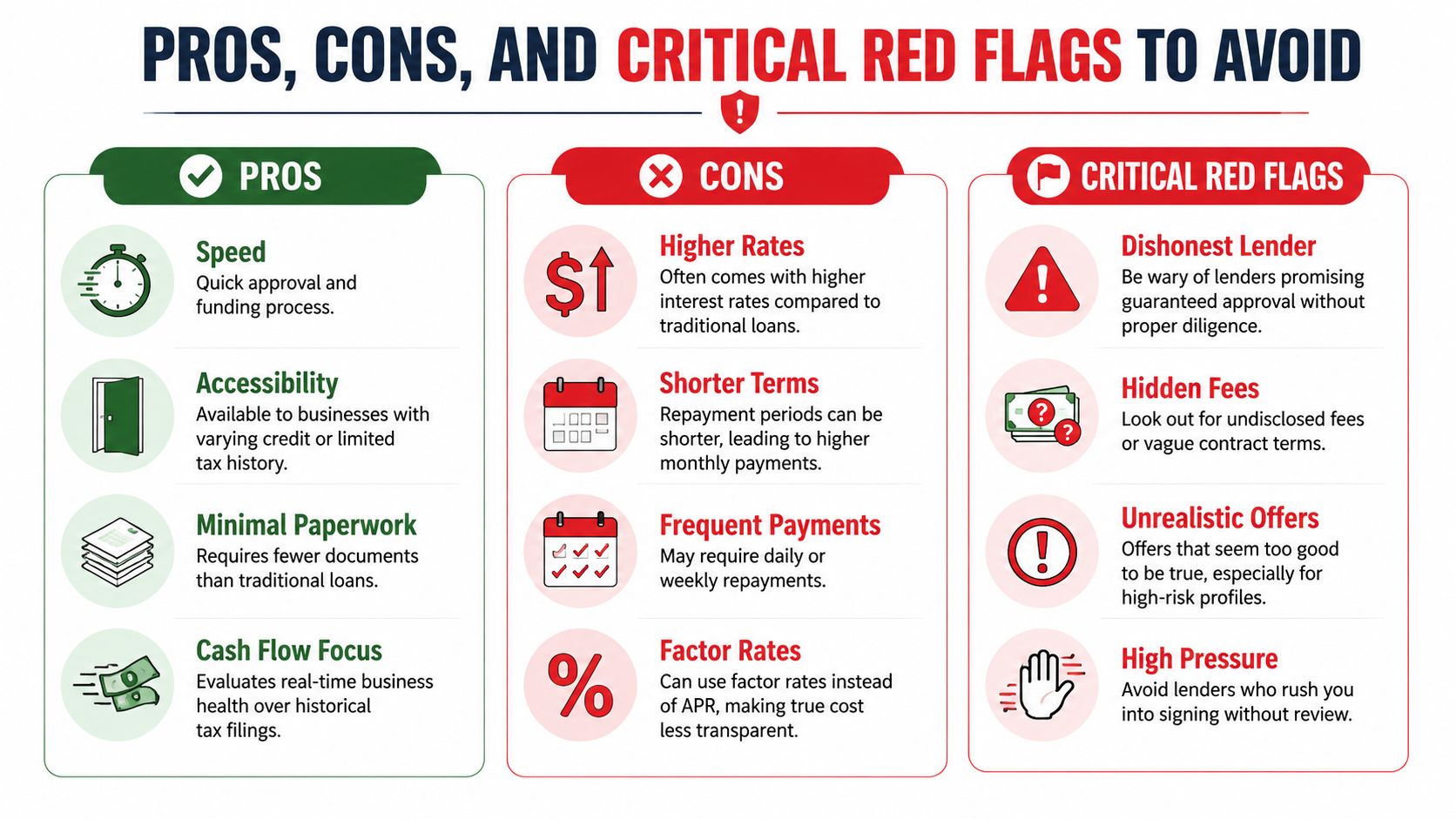

Pros Cons and Critical Red Flags to Avoid

A broker builds a lasting business by telling the truth about the product.

Bank statement business loans can be excellent solutions. They can also be the wrong solution when the borrower only focuses on speed and ignores cost, payment frequency, or cash flow strain. A balanced explanation protects the client and protects the broker's reputation.

A balanced way to position the product

The advantages are straightforward. These loans are often faster, require less traditional paperwork, and can open access for borrowers who don't fit bank underwriting. The focus on current account activity can help businesses that are healthy now but poorly represented by old financials.

The drawbacks are just as real. Pricing is typically higher than conventional options. Repayment structures may feel tighter. Some offers can be less intuitive for borrowers who are used to standard bank loans.

A useful way to frame it is simple:

- Best use case: A business with real cash flow, a clear reason for funding, and limited access to traditional channels.

- Bad use case: A business already strained on cash that wants money without understanding repayment pressure.

- Broker role: Match the product to the need, not the need to the product.

Good brokers don't force-fit a borrower into an approval path. They filter out bad-fit deals before the client signs anything.

Red flags that should stop a deal

Upfront fees are one of the clearest warnings. SoFi notes that upfront fees charged by small business loan brokers are considered a red flag, while legitimate brokers are normally paid by the lender only after the loan closes. It also states that in commercial lending a success fee is typically around 1% of the loan amount and paid by the borrower or lender with proper disclosure at closing, as described in its guide to how business loan brokers get paid.

A broker should also watch for operational red flags on both sides.

For the client:

- Vague use of funds: If the borrower can't explain why they need capital, the deal may not be healthy.

- Hidden account activity: Unexplained transfers, missing statements, or evasive answers usually get worse under review.

- Pressure to rush: Borrowers who demand instant submission often haven't prepared the file.

For the broker:

- Altered documents: Even small inconsistencies can damage lender relationships.

- Guaranteed approval language: Serious professionals don't promise outcomes before review.

- Undisclosed compensation: Fee conversations should be clean and transparent.

Ethical discipline matters in this business. A broker can work remotely and build recurring referrals, but only if lenders trust the files being submitted and clients trust the guidance being given.

Start Your Journey as a Business Loan Broker Today

Bank statement business loans give new brokers a practical place to start. The product is straightforward to understand, the demand is real, and the broker's value is easy to see when a business owner has strong deposits but weak tax-return presentation.

That combination matters for anyone looking to build a home-based, flexible business around a real service. The work can be done remotely. The model can scale through referrals. The commissions are tied to funded deals, which keeps the focus where it belongs, on helping business owners secure financing that fits.

The bigger opportunity isn't just learning one product. It's learning how to source, qualify, package, and close financing opportunities across the alternative lending space with a system that can grow over time.

If building a remote, recession-resistant brokerage business sounds like the right next move, watch the free training from Business Lending Blueprint or schedule a strategy session to learn how to start a profitable lending business the right way. Business Lending Blueprint doesn't provide loans. It teaches people how to build and scale a business loan brokerage.