A likely reader is sitting in one of two places right now. Either a founder just got declined for equipment and asked for help, or a professional who already serves business owners is looking for a funding niche that can be built from home without chasing every trend that comes along.

Equipment financing for startups is that niche. It solves a real problem, it fits a referral-driven brokerage model, and it gives a new broker a practical way to create repeat business by helping companies acquire the machinery, vehicles, medical devices, kitchen systems, production tools, and technology they need to operate.

The mistake is treating startup equipment deals like ordinary bank loans. They aren't. Banks often say no because the company is new. A broker who understands alternative lenders, collateral-driven underwriting, and clean deal packaging can step into that gap and become valuable fast.

Table of Contents

- The Hidden Opportunity in Startup Equipment Financing

- Decoding Equipment Financing Products for Your Clients

- How Lenders Qualify a Startup and How You Can Prepare Them

- The Broker's Playbook for Application and Approval

- Structuring the Deal and Earning Your Commission

- Launch Your Lending Business with Business Lending Blueprint

The Hidden Opportunity in Startup Equipment Financing

A startup needs a key asset to move forward. A restaurant needs kitchen equipment. A contractor needs a machine. A clinic needs diagnostic equipment. The founder walks into a bank, gets declined because the business is too new, and assumes funding is dead.

That's where the broker business begins.

Those new to business lending often prioritize broad working capital deals first. That's a mistake. Equipment financing for startups is easier to explain, easier to position, and often easier to underwrite because the lender can evaluate a tangible asset instead of guessing whether a brand-new company deserves unsecured money.

The size of the market makes the opportunity hard to ignore. In 2025, the U.S. equipment finance market reached a total new business volume of $1.02 trillion, and the industry facilitates the acquisition of nearly two-thirds of all capital equipment purchased by American businesses, according to equipment finance market data from Crestmont Capital. That means this isn't a side category. It's one of the main ways American businesses acquire productive assets.

Why banks create the opening

Traditional banks want operating history, strong financials, and a file that looks safe on paper. Startups usually don't have that. They may have a strong owner, a real plan, and equipment that directly drives revenue, but the bank still says no.

Alternative lenders don't look at the file the same way. They care about the equipment, the guarantor, the cash flow story, and whether the deal makes sense. A broker who knows how to present those elements becomes useful immediately.

A new broker can also pair this niche with adjacent startup conversations. Founders exploring funding options often need more than one solution, which is why resources that help them explore startup credits and perks can support the broader funding discussion without distracting from the core equipment deal.

Practical rule: A bank decline is often the start of an equipment financing opportunity, not the end of it.

Why this works as a home-based brokerage model

This niche fits remote work well. The broker doesn't need inventory, a storefront, or a local branch. The work is advisory, document-driven, and referral-friendly. Accountants, consultants, insurance agents, equipment sellers, and startup advisors all know business owners who need funding but can't get it from a bank.

For readers already studying small business funding for startups, equipment deals are one of the cleanest entry points because the use of funds is specific and the value proposition is obvious. The business needs the asset to operate. The broker helps make that happen.

That's a real service. And it's the kind of service that creates repeat introductions.

Decoding Equipment Financing Products for Your Clients

A broker who can't explain product fit clearly won't last long. Startup founders don't need jargon. They need someone who can look at the asset, the cash flow, and the timeline, then point them toward the structure that fits.

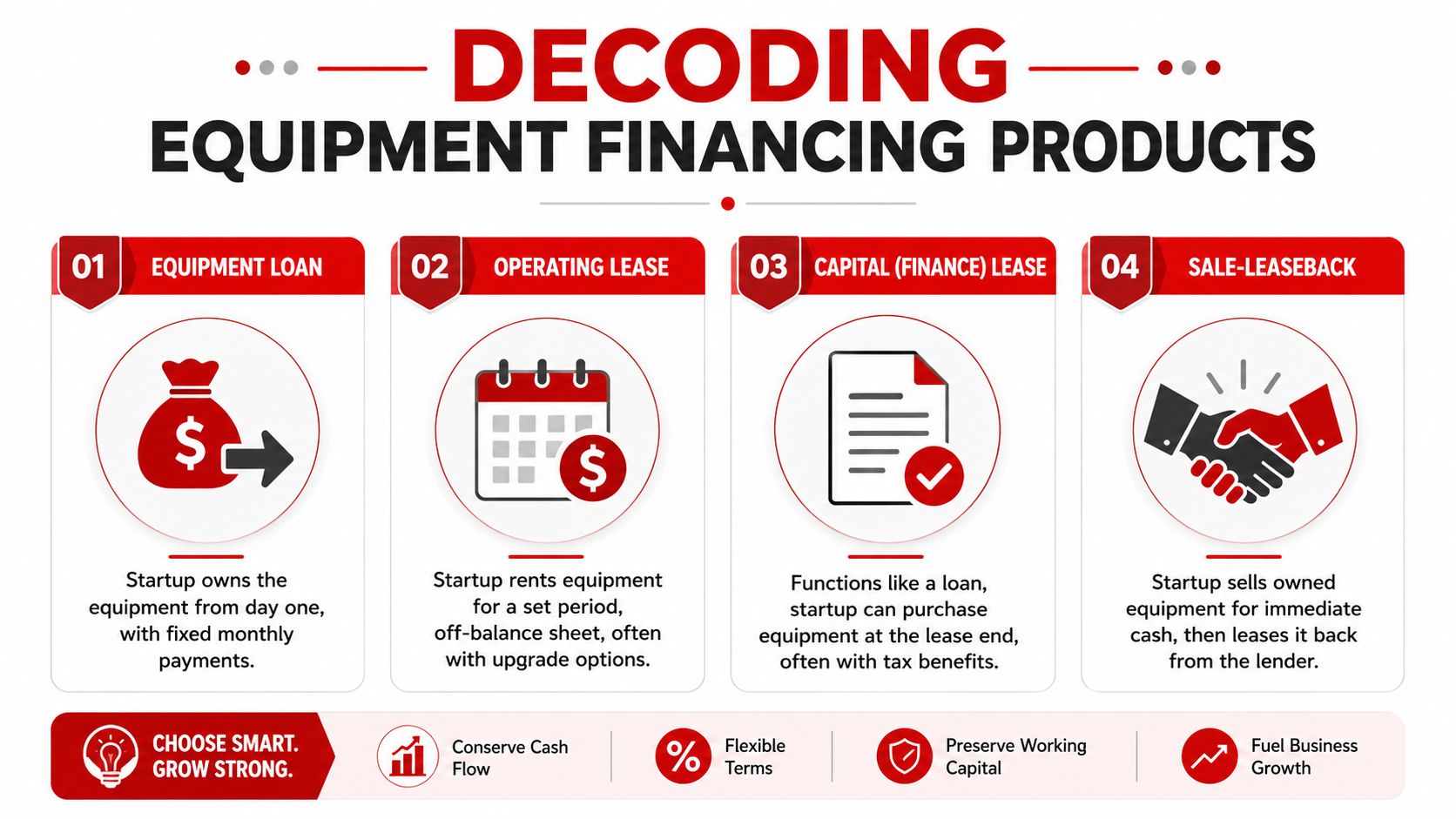

The four products that matter most

Equipment loan

This is the cleanest option when the client wants ownership from day one and the equipment has a long useful life. The startup makes fixed monthly payments and builds equity in the asset immediately. This works well when the founder is buying a durable asset they expect to use for years.

Operating lease

This is a better fit when the equipment may need to be upgraded, replaced, or returned. Startups in fast-changing industries often benefit from flexibility more than ownership. If the client is worried the equipment could become outdated before the financing ends, an operating lease deserves serious attention.

Capital lease

This structure functions much like financing, but it's packaged as a lease. It can make sense when the client wants a path to ownership at the end and likes lease-based structuring. In practice, a broker should treat this as a close cousin to a loan and focus on total cost, end-of-term obligations, and how the asset will be used.

Sale-leaseback

This is useful when a company already owns equipment and needs to free up cash. The lender buys the asset, then leases it back to the business. For an early-stage company with valuable equipment but tight liquidity, this can relieve pressure without shutting down operations.

How a broker chooses the right fit

The product should follow the business reality, not the broker's preference.

A broker should ask:

- How long will the client use the equipment: If the answer is “for a long time,” ownership structures usually deserve priority.

- Will the equipment become outdated quickly: If yes, leasing may protect the client from being stuck with obsolete gear.

- Does the client need lower friction or lower long-term cost: Those are different goals. The right product depends on which one matters more.

- Is the client preserving cash for payroll, inventory, or launch costs: That often pushes the file toward structures with less upfront strain.

A broker's job isn't to hand over a rate sheet. It's to match the financing structure to the way the business will actually operate.

Government-backed options also belong in the conversation when the startup has the patience and profile for them. According to startup equipment financing terms and SBA options summarized by Nomad Excel, SBA 504 loans can finance up to 90% of fixed asset costs, and SBA 7(a) loans can provide up to $5 million with down payment requirements between 10% and 20%. Those options aren't always the fastest path, but they can be strong fits when the asset is central to the business and the founder wants longer-term structure.

Industry-specific context also matters. Restaurant founders, for example, often need a mix of hard equipment and cash preservation. A broker serving that niche should understand common funding paths and review practical examples such as this guide to Silverchef equipment funding to see how operators think about flexibility versus ownership.

For readers who want a deeper niche angle, restaurant equipment financing strategies show exactly why product selection matters. A freezer, oven line, or point-of-sale bundle doesn't always deserve the same financing structure.

How Lenders Qualify a Startup and How You Can Prepare Them

A founder walks in excited about a new piece of equipment and assumes the quote is the hard part. It isn't. The hard part is proving to a lender that the borrower can carry the payment, the equipment holds value, and the deal makes sense on paper. Your job as a broker is to spot the weak points before underwriting does.

What Underwriters Care About

Startup equipment lenders underwrite the owner as much as the business. They start with personal credit, cash flow visibility, time in business, and whether the equipment is easy to value and resell. They also want to know one simple thing. Does this asset help the company make money or keep operating?

That last point matters more than many new brokers realize. A revenue-producing machine, vehicle, or production unit is easier to place than a loosely defined package of miscellaneous equipment. Underwriters like clean stories. If the founder cannot explain why the equipment is necessary, the file gets weaker fast.

Use a practical screen before you ever submit the deal:

- Founder strength: Review personal credit, liquidity, relevant industry experience, and any recent payment issues.

- Business logic: Tie the equipment directly to revenue, delivery capacity, production output, or required operations.

- Collateral quality: Confirm the asset has a clear invoice, identifiable resale value, and a category lenders already understand.

- Cash position: Check whether the client has enough cash to cover a down payment, soft costs, delivery, installation, and early operating pressure.

Brokers' earnings stem from their role in identifying viable financing opportunities. You are not paid to push paperwork. You are paid to filter out weak submissions and present financeable ones.

How to prepare the client before the file goes out

A startup file gets stronger when the borrower looks organized, realistic, and ready to close. That means tightening the request and cleaning up the package before it ever reaches a lender.

Start with the equipment list. Cut anything speculative, inflated, or unrelated to immediate operations. A focused request is easier to approve and easier to place with the right funding source.

Then clean up the documentation. Bank statements should make sense. Entity names should match across invoices, applications, and formation documents. The founder should be ready to explain deposits, recent overdrafts, large transfers, and any mismatch between personal and business activity.

If you want a good model for assembling documents and managing submissions, study this business loan application process for brokers. It helps you standardize intake, reduce avoidable errors, and move faster on approvals.

How to handle weaker startup files

Weak files can still close. Badly packaged files usually do not.

If the founder has limited history, your structure and presentation matter more. Push for a stronger invoice, a clearer business plan, and a tighter explanation of repayment. If the owner has relevant industry experience, bring it forward. If the startup already has signed contracts, pre-orders, or recurring customer demand, make sure the lender sees that early.

Use this mindset with every startup submission:

Underwriting lens: New businesses are judged on the owner, the asset, and the repayment story.

That framework helps you manage client expectations without killing the deal. Strong owners with clean bank activity and sensible equipment requests get more options. Marginal borrowers need more cash in, better documentation, or a smaller ask. Say that early and directly.

Some founders also need to tighten broader cash controls before they apply. If a client holds digital assets or has exposure there, reviewing effective crypto treasury strategies can help them present a cleaner financial profile.

The broker who wins these deals does the prep work first. Screen hard, package tightly, and send lenders a file that already answers the obvious objections.

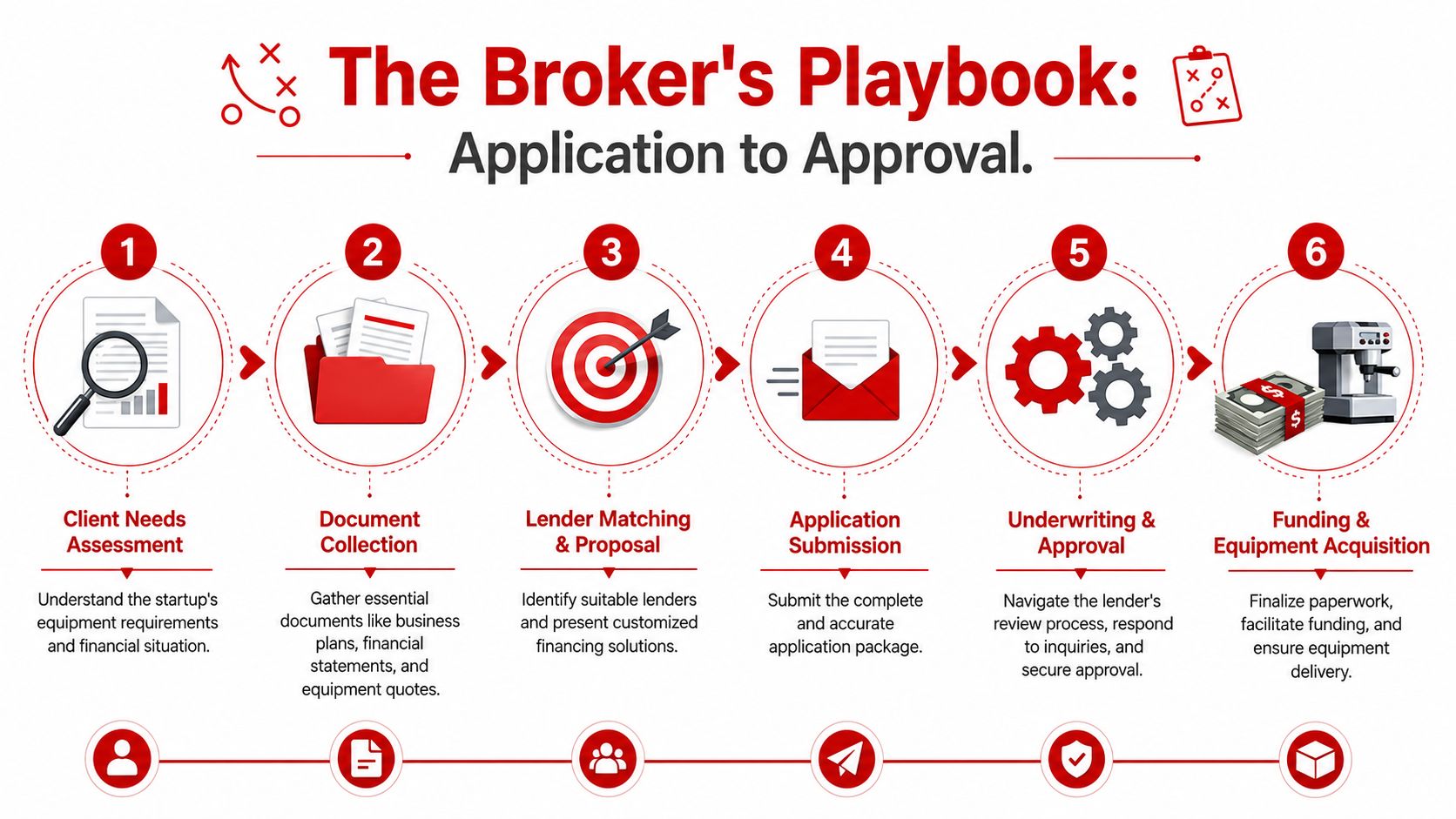

The Broker's Playbook for Application and Approval

Good startup equipment deals don't close because the client is enthusiastic. They close because the broker runs a disciplined process.

The submission process that gets taken seriously

For startups lacking two or more years of history, approval is driven by a math-based screen. According to startup equipment underwriting guidance from The Credit People, equipment costs must remain under 30% of monthly revenue, combined with the founder's personal credit. The same guidance recommends mapping the equipment to asset-class-specialized lenders and submitting a soft-pull application with 3 to 6 months of bank statements and a detailed equipment quote.

That means the broker should stop treating all lenders as interchangeable. They aren't. Startup equipment financing gets stronger when the deal goes to a lender that understands the asset category and knows how to value it.

A simple workflow works best:

- Qualify the founder first. Personal credit, business purpose, and expected use of equipment need to be clear.

- Confirm the asset. The quote must be detailed, current, and tied to a real vendor.

- Check revenue logic. If the company has revenue, the request has to fit the lender's math.

- Choose the lender type carefully. Asset fit matters as much as borrower fit.

- Submit a complete file. Incomplete submissions get ignored, delayed, or declined.

What goes into a lender-ready package

A broker should gather the file like an underwriter, not like an assistant. The point isn't to collect paper. The point is to remove uncertainty.

A strong package usually includes:

- A clean application: Names, entity details, ownership, and contact information must match across every document.

- Bank statements: The right statements, in full, with no missing pages.

- Equipment quote: Detailed enough to show exactly what's being financed.

- Cash flow explanation: Brief and specific. It should explain how the equipment supports operations and repayment.

- Any relevant business support documents: Formation records, licenses, or other basics that confirm the company is real and active.

Send a file that answers the lender's next five questions before they ask them.

Brokers who want a broader framework for document flow, submission order, and expectation-setting can review the business loan application process and apply the same discipline here.

A short executive summary can also help. It doesn't need to be long. It needs to be persuasive. It should identify the business, describe the asset, explain the owner's background, and state why the transaction makes sense. When a startup deal is marginal, clarity often determines whether the lender leans in or walks away.

Structuring the Deal and Earning Your Commission

A funded approval is not the finish line. Bad structure creates unhappy clients, early stress, and damaged referral relationships. Good structure protects the borrower and protects the broker's reputation.

Good structure protects the client and the broker

The biggest mistake is stretching the term beyond the asset's useful life. According to equipment financing risk benchmarks from Delta Capital Group, the most common pitfall in startup equipment financing is failing to align the financing term with the equipment's useful life, which leads to a detrimental financial outcome. The same source says a critical benchmark is maintaining a Cash Flow Safety Margin where monthly equipment payments never exceed 70% of the additional monthly revenue generated by that equipment.

That rule is practical. If the payment consumes too much of the value the equipment creates, the client is boxed in the moment sales dip, repairs show up, or the ramp takes longer than expected.

A broker should structure with four priorities in mind:

- Asset life first: A short-lived asset shouldn't carry long debt just because the payment looks smaller.

- Payment realism: The founder must be able to absorb normal business volatility.

- Total cost clarity: End-of-term obligations, fees, and buyout terms need to be understood before closing.

- Lender fit: The cheapest-looking approval isn't always the best approval.

Sample deal commission breakdown

The exact commission depends on the lender agreement, and no ethical broker should promise a fixed outcome before a lender issues terms. Still, every aspiring broker needs a simple worksheet for analyzing a file and understanding where revenue may come from.

| Metric | Example Value |

|---|---|

| Equipment cost | Quoted purchase price from vendor |

| Down payment | Based on credit profile and lender terms |

| Financed amount | Equipment cost minus any required down payment |

| Financing structure | Loan, operating lease, capital lease, or sale-leaseback |

| Rate or factor | Provided by lender after review |

| Monthly payment | Based on final approved terms |

| Broker compensation | Lender-paid commission per agreement |

| Net benefit to client | Cash preserved, equipment acquired, and repayment fit |

That table matters because it forces discipline. The broker should be able to explain every line in plain English.

A founder doesn't just need approval. The founder needs to understand what they're signing, what happens at the end of the term, and whether the asset will still be productive when the obligation is over. That level of clarity creates trust, and trust is what turns one funded deal into referrals from vendors, accountants, consultants, and clients.

Launch Your Lending Business with Business Lending Blueprint

Equipment financing for startups is one of the best entry points for an aspiring broker because it solves a concrete problem. Business owners need equipment. Banks often decline new entities. Alternative lenders fill the gap. A broker who can qualify, package, and place those files can build a serious business around that need.

The market behind that work is not small, and it isn't going away. The global alternative lending market is projected to reach US$607 billion by 2026, growing at an annual rate of 13.4%, according to alternative lending market projections from Research and Markets. That matters because brokers operate inside that broader non-bank funding ecosystem. When traditional institutions stay rigid, alternative capital keeps moving.

Why this model attracts smart operators

This business appeals to people who want flexibility without building something flimsy. It can be run remotely. It can be built through referrals. It can complement an existing professional practice or become a standalone brokerage over time.

It also rewards competence. The broker who knows how to screen founders, match deals to lender appetite, and prevent bad structures becomes valuable quickly. That's far more durable than chasing random side hustles or depending on one lead source.

For readers serious about building this into a real business, how to start a loan business is the right next step. The opportunity isn't in reading one more generic article. It's in learning a repeatable process, using vetted lender relationships, and building a system that produces funded deals consistently.

A lending business doesn't need to begin with a huge team, an office, or years of prior finance experience. It needs a clear process, the right training, and a commitment to helping business owners access capital when banks won't.

Business Lending Blueprint teaches people how to build a profitable, home-based business by becoming a business loan broker. It doesn't provide loans. It provides the training, systems, mentorship, and lender-network guidance to help people launch and grow a lending business that serves real business owners. To see the model in action, watch the free training or schedule a strategy session with Business Lending Blueprint.