A lot of readers are in the same spot right now. They want a business that can be run from home, they want something more durable than chasing one-off freelance projects, and they want a service that solves a real problem for small businesses instead of selling noise.

Working capital lines of credit sit right in that pocket. Small business owners hit cash flow gaps constantly. Payroll comes due before receivables clear. Inventory has to be ordered before the busy season. A large customer pays late and suddenly a healthy company looks stressed for thirty days. That gap creates a practical opening for a broker who knows how to place the right deal, with the right lender, and keep the client out of the wrong product.

For an aspiring broker, this is one of the most useful products to understand early because it teaches good habits. It forces proper deal diagnosis. It reveals how lenders think about risk. It also creates repeat business, because clients who use a line properly often come back for renewals, larger facilities, or other funding products later.

Table of Contents

- The Hidden Opportunity in Business Cash Flow Gaps

- What Is a Working Capital Line of Credit

- The Mechanics How These Credit Lines Really Work

- Choosing the Right Tool WCLOC vs Other Funding

- Unlocking Approvals The Truth About Underwriting

- Your Blueprint to Brokering These Deals

- Start Your Profitable Lending Business Today

The Hidden Opportunity in Business Cash Flow Gaps

A local contractor finishes a large job. The invoice goes out. Payment terms stretch. Meanwhile, payroll lands on Friday, materials need to be reordered, and two trucks need repairs. Revenue exists on paper, but cash isn't in the account yet. That owner isn't looking for theory. That owner needs liquidity.

That is where brokers earn trust. A working capital line of credit isn't just another product on a rate sheet. It's often the difference between a business owner staying calm and a business owner stacking expensive debt in a panic.

The demand is large enough to matter. The global working capital loan market was valued at USD 1.2 trillion in 2023 and is projected to reach USD 2.5 trillion by 2033, with lines of credit representing the dominant product category, according to working capital loan market analysis. For a broker building a home-based business, that matters because it points to a broad, recurring need rather than a niche trend.

Why this product creates repeat deal flow

Cash flow problems rarely show up once and disappear forever. They tend to follow operating cycles.

A seasonal retailer needs flexibility before inventory turns. A service company needs breathing room when large invoices age. A distributor may need short-term support between supplier payments and customer collections. The broker who solves one of those problems often becomes the first call when the next one appears.

Practical rule: Products tied to recurring business pain create better referral relationships than one-time transactions.

A broker who understands this product also starts seeing adjacent opportunities. A client who really needs receivables-based financing might be a stronger fit for invoice factoring for small business. A client struggling with operating discipline may also need basic help around managing cash flow for Florida SMEs, especially if collections, payables timing, and forecasting are part of the problem.

What new brokers usually miss

Many beginners chase only large term loan requests because those feel more substantial. That is backwards. Short-term liquidity products often move faster, solve a more immediate pain point, and open the door to long-term client relationships.

The broker's job isn't to sell debt. The job is to place the right kind of capital into the right kind of problem. Working capital lines of credit do that well when the need is operational and the timing gap is real.

What Is a Working Capital Line of Credit

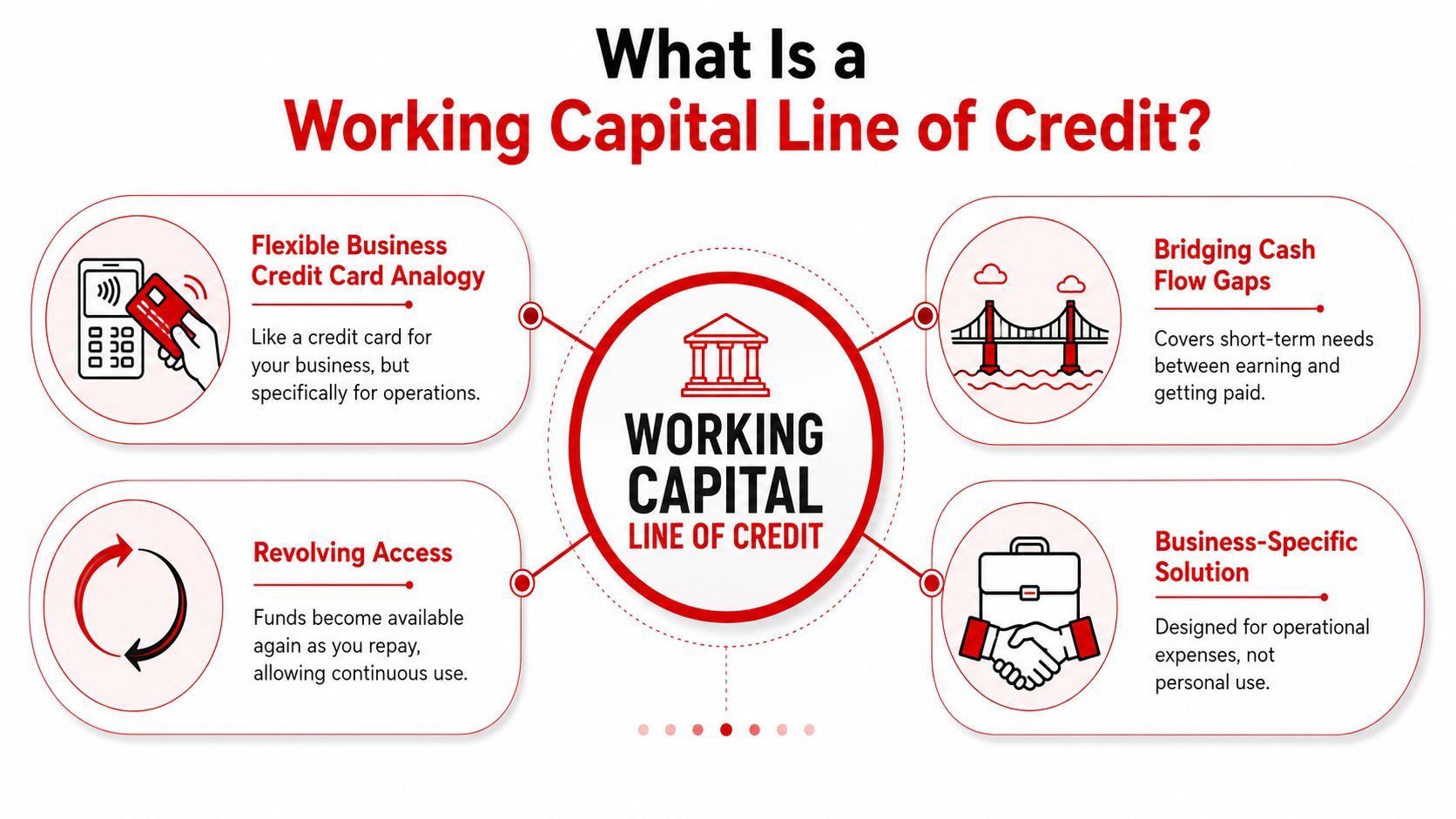

The simplest way to explain it to a client is this. A working capital line of credit is like a business credit card designed for operations, not personal spending and not long-range expansion.

A lender approves a maximum limit. The business draws only what it needs. As the balance gets repaid, that availability returns. The business doesn't have to reapply every time it needs to use the line within the approved structure.

The clean broker explanation

When training a new broker, the easiest client-facing script sounds like this:

- It covers short-term operating needs. Payroll, inventory, accounts payable, and unexpected gaps are the normal uses.

- It revolves. If the client draws, repays, and draws again, the line keeps functioning without a new full approval each time.

- It keeps borrowing tied to need. The client isn't forced to take a full lump sum on day one.

That last point matters. Borrowers often overfinance when they take a term product for a problem that only needs flexible access.

What it is not

This product gets abused when owners treat it like permanent growth capital.

An operating line is a liquidity tool. It is not the best answer for buying long-lived assets, funding an acquisition, or carrying an expansion project that will take a long time to pay back. That mismatch is where brokers either protect the client or fail the client.

A line of credit is a financial tap for liquidity. It isn't a fuel tank for long-term expansion.

That distinction becomes clearer when talking to owners in industries with uneven billing cycles. For example, owners focused on managing veterinary practice cash flow often need a product that smooths timing, not a product that forces them into a large fixed obligation for a short-term issue.

How to position it without sounding vague

New brokers often describe lines of credit in broad language that sounds harmless but doesn't help a borrower decide. Better language is specific.

Use phrases like these:

- For timing gaps: “This helps when cash comes in later than expenses go out.”

- For repeat use: “You can draw, repay, and draw again.”

- For operating needs: “This is meant for normal business activity, not big one-time expansion.”

When a broker can explain the product clearly, owners stop hearing “loan” and start hearing “control.” That shift is what gets conversations moving.

The Mechanics How These Credit Lines Really Work

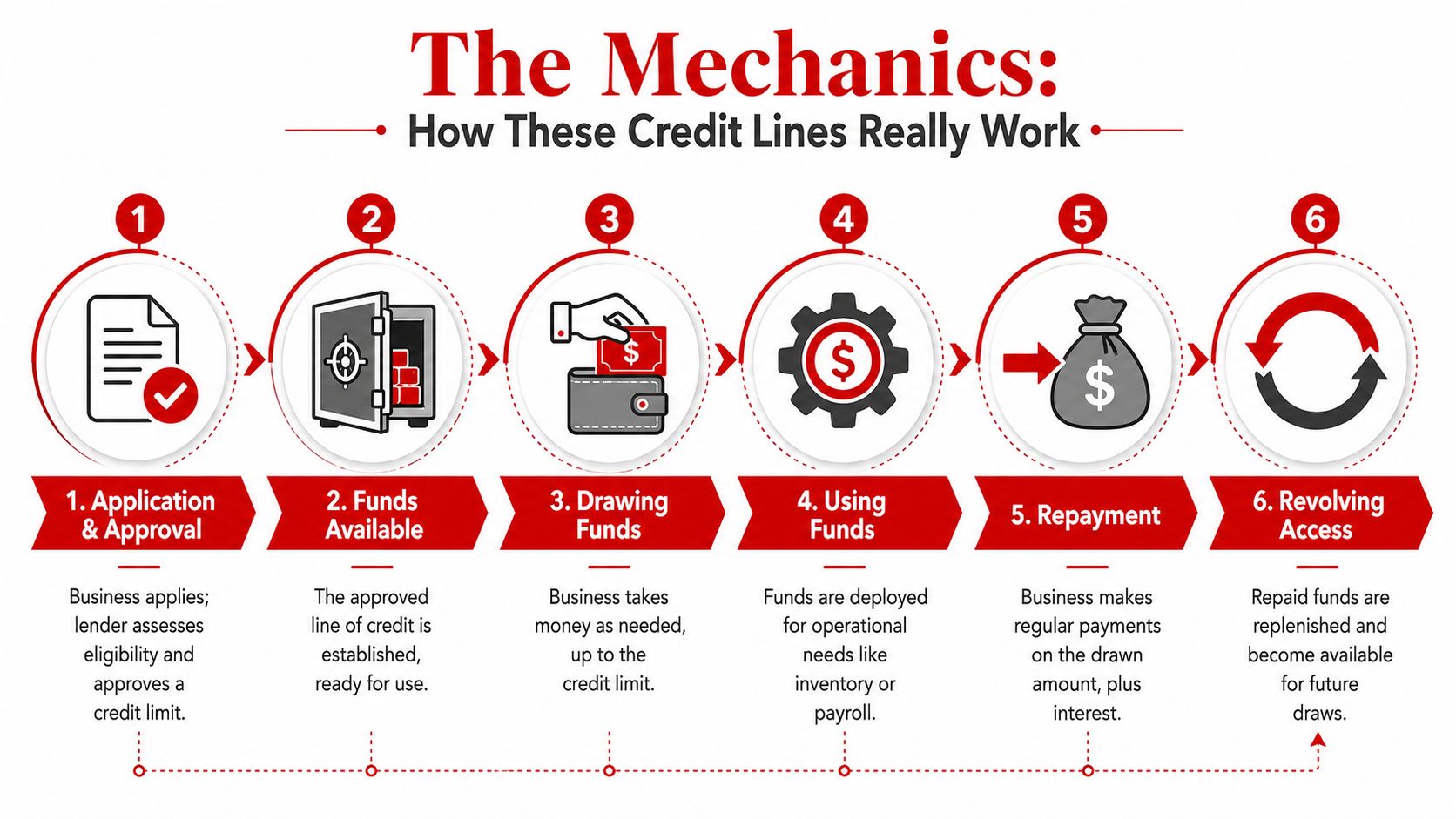

A new broker usually loses the client at the moment the owner asks a simple question: “If I pay this down, can I use it again next month?” If you cannot answer that clearly, you are not really brokering a revolving line. You are repeating lender marketing.

The draw repay replenish cycle

The core mechanic is simple. The lender approves a credit limit, the borrower draws only what the business needs, interest applies to the outstanding balance, and availability returns as the balance is repaid.

That sounds basic, but deals get messy when brokers skip the operating details. Some lenders allow immediate redraw after principal posts. Others use weekly or monthly borrowing base reviews, so the available amount can move up or down with receivables, inventory, or both.

A clean way to explain it to a borrower is this:

Approval creates a facility

The lender sets a maximum line amount, along with draw rules, reporting requirements, and any borrowing base limits.The borrower draws only what the operation needs

Payroll, supplier payments, and short inventory buys are common uses. If the client uses only part of the line, the unused portion stays available.Interest applies to what is outstanding

Cost is tied to funds in use, not the full credit limit. Some facilities also add maintenance fees, draw fees, or inactivity fees, so brokers need to review the full pricing page, not just the rate.Repayment restores capacity

As principal comes down, room opens back up, subject to the lender's current advance rules and collateral position.

That last part matters in real placements. Availability is not always the same as the headline limit on the approval letter.

What actually controls the line size

Many working capital lines are secured by short-term assets, especially receivables and inventory. The lender often lends against a percentage of eligible collateral, not against the owner's optimism about future growth.

That is why two companies with the same annual revenue can get very different outcomes. A borrower with clean aging reports, low customer concentration, and predictable inventory turnover usually gives a lender more comfort than a borrower with stale invoices and slow-moving stock. Brokers who place deals in this part of the market should understand how accounts receivable lenders review collateral and structure advances, because the credit logic overlaps.

Strong collateral gets more done than a strong pitch deck.

For sub-650 clients, this point gets even sharper. A weak personal score can be offset in part by better business bank activity, cleaner receivables, or a tighter explanation of where repayment comes from. It does not erase credit weakness, but it can keep a file alive with the right lender type.

Terms that matter in real deals

New brokers often focus on limit and rate. Underwriters care about the structure behind the line.

Watch these items before you submit:

- Borrowing base rules: The approved limit may be higher than the amount currently available to draw.

- Collateral eligibility: Old receivables, foreign invoices, concentrated customer exposure, or obsolete inventory may be excluded.

- Cleanup requirements: Some lenders want the line paid down for a period each year to prove it is being used for short-term operating needs.

- Demand features: Certain facilities let the lender call the line, especially after covenant issues, reporting failures, or material risk changes.

- Reporting cadence: Monthly aging reports, inventory reports, and bank statements are common, especially on asset-based structures.

One leading financial institution notes that working capital facilities are commonly tied to short-term operating assets and may include underwriting standards such as debt service coverage and revenue history requirements, depending on the structure and risk profile. That is the practical point brokers need to hear. Approval is not just about need. It is about proving the line will revolve in a controlled way.

Brokers who understand these mechanics package cleaner files, set better expectations, and keep clients out of the wrong product. That is how a line of credit becomes a repeatable brokerage opportunity instead of a one-off deal that blows up after closing.

Choosing the Right Tool WCLOC vs Other Funding

A broker loses trust fast by treating every cash need like a line of credit deal. Good placement starts with one question: is the client dealing with a timing problem, or a capital need?

A working capital line of credit fits timing problems. Payroll hits before receivables clear. Inventory has to be bought before the next sales cycle pays out. The amount needed changes month to month, and the balance should come down as cash comes in. That is the kind of pattern a revolving facility is built for.

A fixed loan fits a different job. If the borrower is opening a second location, buying equipment, refinancing expensive debt, or funding a project with a clear total cost, a lump-sum product usually makes more sense. The repayment term should match the useful life of what is being financed. If the asset or project will still be producing value years from now, short-cycle revolving debt is often the wrong match.

Funding Options at a Glance

| Funding Type | Best For | Repayment Structure | Typical Cost |

|---|---|---|---|

| Working capital line of credit | Repeating operational gaps, short inventory cycles, uneven receivables timing | Revolving. Borrow, repay, reuse | Varies by collateral, borrower profile, and lender type |

| Term loan | Defined project cost, equipment, expansion with a longer payoff timeline | Fixed repayment over a set term | Often more suitable than a line when the asset or project is long term |

| Merchant cash advance | Urgent situations when other options don't fit | Frequent remittance tied to sales or a fixed structure depending on provider | Often expensive and easy to misuse |

| Invoice factoring | B2B companies with collectible invoices and slow-paying customers | Advance against invoices, then settle when invoices pay | Depends on invoice quality and structure |

The easiest way to train a new broker on product fit is to listen for how the owner describes the problem.

A line is usually the right answer when the owner says:

- “This keeps happening.” Recurring gaps usually call for a reusable facility.

- “The amount is never exactly the same.” Variable need favors a revolving structure.

- “We just need to bridge until invoices pay or inventory sells.” That lines up with short-term operating use.

A line is usually the wrong answer when the owner is trying to force short-term debt into a long-term role. That is how clients get trapped. They draw the line for expansion, carry the balance too long, pay repeated fees or high interest, and never create the cash cycle needed to pay it down cleanly.

That mistake creates a brokerage problem too. The deal may fund, but the client comes back stressed, overextended, and harder to place next time. Brokers who build durable books avoid that by matching structure to use, even when a faster approval is sitting on the table.

For invoice-heavy companies, it helps to understand our factoring solution so you can explain how receivables funding differs from a revolving operating line. And if a borrower is weighing reusable access against a one-time disbursement, this guide on term loan vs line of credit gives a cleaner framework for the conversation.

One practical rule: if the balance will still be sitting there long after the receivables should have collected or the inventory should have turned, the product is probably wrong. That is the point new brokers need to learn early. Product fit protects the client, improves renewal potential, and keeps your reputation intact.

Unlocking Approvals The Truth About Underwriting

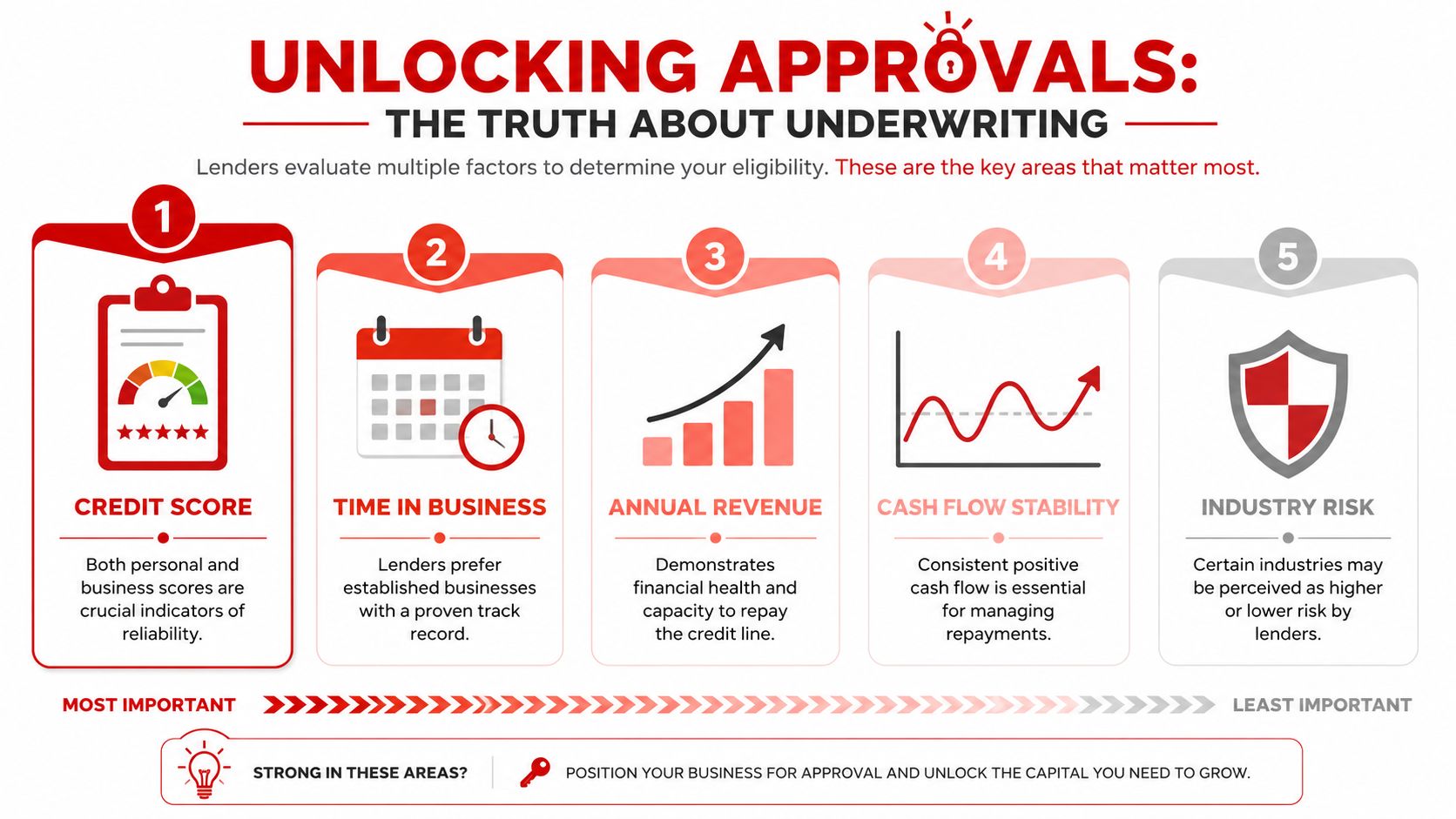

A new broker gets a file that looks dead on arrival. The owner has a 612 score, thin financials, and a prior decline from a bank. An inexperienced broker stops there. A productive broker asks a different question. What, specifically, made this borrower fail one lender's box, and which lender will view the same cash flow differently?

The approval picture is more nuanced than many assume

Working capital line underwriting is rarely a single yes-or-no test. Lenders weigh several variables together. Credit score matters, but so do deposit consistency, average daily balance, overdraft history, industry risk, time in business, and whether the requested line makes sense relative to revenue.

That matters for brokers because approvals often depend on fit, not just borrower quality in the abstract. A company that misses a bank's standards may still qualify with a non-bank lender that puts more weight on recent bank activity and less weight on tax-return strength. The broker's job is to know which weaknesses are fatal, which are explainable, and which can be offset by stronger cash flow.

Underwriters also look for proportionality. If a borrower with modest annual revenue asks for a line that is too large for the business, the file gets harder to defend. If the request tracks a believable operating need, such as covering payroll between receivable collections or buying inventory for a repeat sales cycle, the story holds together better.

Why sub-650 files still fund

Sub-650 does not mean automatic decline. It means the rest of the file has to work harder.

For these borrowers, lenders usually focus on behavior. They want to see deposits coming in regularly, not random spikes followed by droughts. They want to see that the account is being managed, even if margins are tight. They want a use of funds that matches a short operating cycle. A weak score tied to old personal credit events is easier to work around than active business stress showing up every week in the statements.

New brokers either earn their commission or waste everyone's time depending on their diligence. Sending the same sub-650 file to every lender on a spreadsheet is sloppy. Read the statements first. Count negative days. Look for NSFs. Check whether revenue is stable or sliding. If the business has enough gross inflow but poor account management, package the explanation carefully. If deposits are shrinking and the owner needs money to cover an ongoing loss, calling it working capital will not save the deal.

Some programs will consider younger businesses and bruised credit profiles, but the trade-off is tighter limits, more monitoring, and higher pricing. That can still be a good outcome if the line solves a short-term cash cycle problem and creates a path to refinance later.

Pricing follows file quality and lender risk

Rates and fees vary because the risk varies. A lender secured by receivables or inventory can usually price more aggressively than a lender advancing against projected cash flow alone. A borrower with clean statements and steady revenue gets treated differently from one with frequent overdrafts, volatile deposits, or thin history.

New brokers need to say that plainly. Approval is not the win by itself. The win is placing the borrower into a structure they can carry.

- Secured lines usually come with lower pricing because the lender has collateral support.

- Unsecured lines often cost more because repayment depends more heavily on cash flow stability.

- Short operating history or lower credit can still get approved, but pricing and limit size usually reflect that added risk.

- Messy bank activity often hurts more than owners expect, even when monthly revenue looks acceptable on the surface.

Good brokers do not sell hope. They qualify, package, and set expectations. If the offer is expensive, explain why. If the borrower should wait, clean up statements, or choose another product, say that early. That is how you build a book that renews instead of a pile of one-time commissions and frustrated clients.

Your Blueprint to Brokering These Deals

Product knowledge turns into a brokerage business. A new broker doesn't need a giant office or a bank background. What matters is a repeatable process for finding the right borrower, qualifying fast, and packaging the file correctly.

Start with the borrower, not the lender

The first conversation should answer four practical questions:

- What is the money for? If the answer sounds long term, the broker should slow down before pushing a line.

- How does cash move through the business? The broker wants to understand invoicing, collections, seasonality, and recurring expense pressure.

- What does the recent bank activity look like? Lenders care about the facts in the statements, not just the owner's optimism.

- What will repayment come from? The answer should tie to the operating cycle.

This step is where many new brokers improve fast. They stop “taking applications” and start diagnosing financing fit.

Build a clean submission package

A messy file gets priced worse, delayed, or ignored. A clean one gets attention.

A basic packaging workflow usually includes:

Recent business bank statements

These show deposits, volatility, negative days, and overall account conduct.A current profit and loss statement

Even when a lender leans heavily on statements, a P&L helps tell the story.Basic business details

Time in business, industry, ownership, and use of funds need to be clear and consistent.A short credit narrative

If the owner has bruised credit, the broker should explain the cause and the current stability, not pretend the issue doesn't exist.

For brokers still learning the structure of a solid file, the best habit is to follow a documented workflow like this guide to the business loan application process.

The lender should never have to guess what the borrower needs, why the line makes sense, or how the line gets repaid.

Match the deal to the lender box

This part separates professionals from amateurs.

Some lenders are better suited to secured operating lines tied to receivables and inventory. Others are built for thinner files, shorter operating histories, or lower scores. Non-bank working capital lines may accept businesses with 6+ months in operation, $50K+ annual revenue, and a 550+ FICO score, while conventional revolving lines typically require 3+ years in business and documented revenue history, according to this summary of non-bank versus conventional working capital line requirements.

That means the broker's value isn't merely “access.” It is placement logic.

Build referral channels that keep feeding the pipeline

The strongest brokerages don't rely on random outreach forever. They build referral relationships with professionals who already hear cash flow pain first.

Useful referral partners often include:

- CPAs who see tax pressure, declining liquidity, and seasonal strain

- Bookkeepers who notice late receivables and recurring working capital gaps

- Consultants helping owners expand operations faster than cash allows

- Insurance, real estate, and business service professionals whose clients regularly ask where to find funding

A broker working remotely can build those relationships without a storefront. That is one reason this business model appeals to professionals, career changers, and side-hustlers looking for a flexible, scalable service business.

Start Your Profitable Lending Business Today

A lot of new brokers start by chasing every product on the menu and end up mediocre at all of them. Working capital lines are a better starting point because they force good habits early. You learn how to read cash flow pressure, match the line to the use of funds, spot repayment risk, and keep a client out of debt that solves one problem while creating a bigger one next month.

That matters if the goal is to build a brokerage that lasts.

A working capital line gives you repeat business, not just one transaction. Clients draw, repay, and come back when the next inventory cycle, payroll squeeze, or receivables delay shows up. For a broker, that means more renewal chances, more referrals, and more visibility into which lenders perform well after funding, not just at approval.

It is also one of the cleaner ways to learn placement strategy for harder files. A bankable borrower may qualify for a lower-cost revolving line. A thin-file client or a borrower below 650 may need a non-bank option with tighter limits and higher pricing. The broker's job is to explain that trade-off clearly, set expectations before submission, and package the file so the lender sees stability instead of distress.

That is where many beginners either build a real business or burn through their reputation. If you send poorly structured files, oversell approvals, or place clients into expensive debt they cannot manage, referral partners stop sending opportunities. If you stay disciplined, document the story well, and match the product to the operating cycle, the pipeline gets stronger over time.

This business also fits the way many brokers want to work. It can be run from home. It can start part time. It can grow into a referral-based operation without a large staff, as long as the broker gets good at lender selection, file prep, and follow-up.

For sales professionals, consultants, former bankers, CPAs, and first-time entrepreneurs, this is a practical entry point into commercial finance. The product is useful. The learning curve teaches skills that transfer to other deal types. And each well-placed line can lead to renewals, cross-sell opportunities, and long-term client relationships.

Business Lending Blueprint teaches people how to launch and grow a profitable, home-based business loan brokerage by helping business owners secure funding through alternative lenders. It doesn't provide loans. It provides the training, mentorship, systems, and lender network to help people build a real lending business with flexibility, remote work potential, scalable operations, and recurring referral relationships. To see how the model works, watch the free training at Business Lending Blueprint or schedule a strategy session.