A new broker closes the first funded deal, sees the commission hit, and finally feels that the home-based model is real. The laptop on the kitchen table doesn't look temporary anymore. It looks like a business.

That's usually the moment when a smarter question shows up. Not “How fast can this grow?” but “Is this being built the right way?” A referral-driven brokerage can scale beautifully, especially when it serves business owners who need access to alternative lending options. It can also create exposure faster than most new brokers realize, because habits formed on early deals tend to become permanent operating practices.

Fair lending practices sit right in the middle of that decision. They aren't just a bank issue. They shape how a broker markets, screens inquiries, speaks with applicants, documents recommendations, and chooses lender partners. For anyone building a remote, flexible, recession-resistant business, this is one of the clearest lines between a durable brand and a risky side hustle.

Table of Contents

- Your First Funded Deal and Your First Big Risk

- What Fair Lending Really Means for Your Brokerage

- The Regulatory Minefield Key Laws You Must Know

- Common Violations and Everyday Red Flags

- Compliance Best Practices for a Modern Broker

- Your Fair Lending Policy and Documentation Toolkit

- Build Your Business the Right Way

Your First Funded Deal and Your First Big Risk

The first few deals often look clean on the surface. A restaurant owner needs working capital. A contractor needs equipment financing. A startup founder needs bridge funding after a bank says no. The broker collects documents, shops the file, gets an approval, and earns a commission. Business loan brokers typically earn commissions ranging from 1% to 5% of the total loan amount they facilitate, and “one point” means 1% of the funded amount for compensation calculations according to this business loan broker commission guide.

Then the hidden risk shows up in ordinary moments. A broker answers one prospect warmly and another prospect cautiously because the second applicant “doesn't sound fundable.” A referral partner sends leads from one neighborhood and none from another. A broker learns that certain lenders convert better and starts sending some business owners there first, even when the product fit is weaker.

None of that feels like a compliance problem when the goal is just to help people get funded. But those patterns create the record of how a brokerage treats applicants.

Practical rule: The first systems a broker installs should govern conduct, not just lead flow.

That matters for long-term stability. A brokerage that wants remote freedom and recurring referral relationships can't rely on improvisation. It needs operating discipline. That's just as important as understanding deal structure, default risk, or how products differ in the SBA and default loan landscape. The broker who builds correctly from day one has a stronger chance of keeping both reputation and revenue intact.

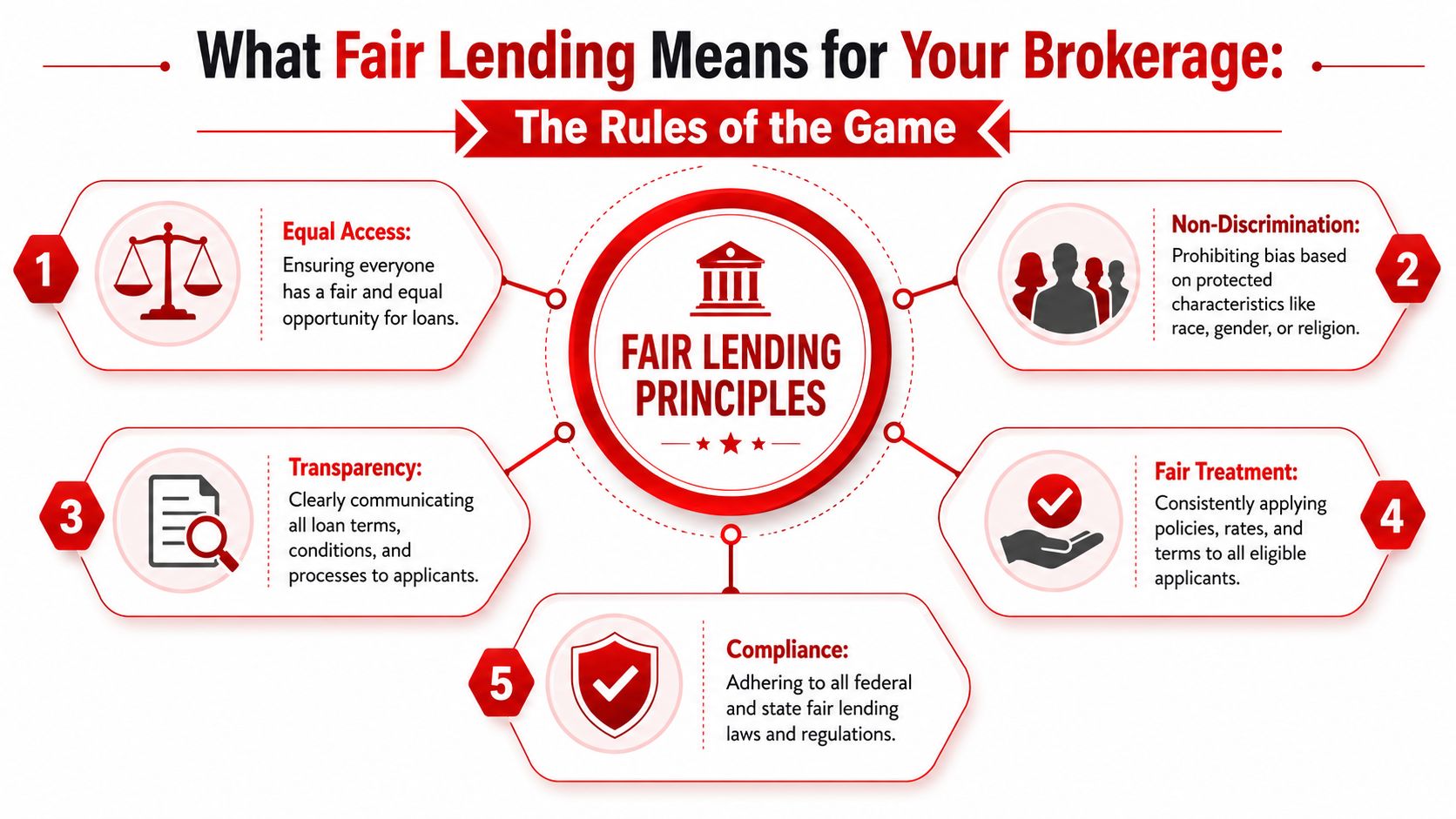

What Fair Lending Really Means for Your Brokerage

Fair lending practices are the rules of the road for access to financing. They exist so that a qualified applicant gets evaluated on legitimate credit factors, not on who that applicant is, what the applicant looks like, or which protected group the applicant belongs to.

For a broker, that principle applies earlier than many people think. It starts in ad copy, website language, intake questions, follow-up speed, document requests, lender matching, and the tone used when discussing options. A broker may not make the final underwriting decision, but the broker still influences who gets encouraged, who gets filtered out, and who gets shown which path.

The broker's role isn't passive

A common mistake is thinking fair lending is only the lender's problem because the lender issues the approval or decline. That view is too narrow. A referral-driven broker shapes the applicant's experience before the file ever reaches underwriting.

A broker creates risk when the process includes any of these habits:

- Selective encouragement: One applicant gets “let's find a way,” while another gets discouraged before a full review.

- Uneven product presentation: Better terms are discussed with some clients, while others are shown only expensive or restrictive options.

- Loose communication standards: Scripts change depending on assumptions about the applicant instead of documented criteria.

The practical test is simple. If two similarly situated applicants approached the brokerage, would they receive the same process, the same attention, and the same menu of possible solutions?

What this looks like in daily operations

Fair lending practices become real in the small details of a home-based brokerage:

- Marketing choice: Ads should invite broad categories of eligible business owners, not imply who is and isn't welcome.

- Intake discipline: Questions should gather business and credit facts relevant to funding, not drift into protected characteristics.

- Referral integrity: Lender placement should follow fit and program requirements, not assumption or convenience.

A broker doesn't need a giant compliance department to operate fairly. A broker needs repeatable standards.

That's where ethical business and scalable business start to overlap. The same consistency that protects against complaints also helps a brokerage train assistants, manage referrals, and create cleaner files for lender submission.

The Regulatory Minefield Key Laws You Must Know

A broker doesn't need to become a lawyer. A broker does need to know where the boundaries are. The most important laws aren't abstract. They affect what can be asked, how applicants are treated, and whether a pattern of conduct can be defended later.

ECOA is the foundation

The legal anchor for fair lending practices is the Equal Credit Opportunity Act, or ECOA. It was enacted in the 1970s under Regulation B and prohibits discrimination in all credit transactions based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance income, according to this overview of ECOA and fair lending enforcement. That same source notes that the CFPB has primary enforcement authority for ECOA regarding institutions with assets over $10 billion, and regulators can impose civil monetary penalties and restitution.

For a broker, ECOA matters because a referral model still sits inside the credit transaction. If a broker markets differently, screens differently, or routes applicants differently based on protected characteristics, the broker creates exposure even without signing the credit approval.

Many brokers who work with small business applicants also need to stay aware of reporting and process obligations tied to Dodd-Frank Section 1071 compliance, especially when lender partners collect and manage small business lending data. That doesn't replace legal advice, but it does help a broker understand the broader compliance environment affecting lender relationships.

A broker who wants to operate professionally should also understand the broader expectations around a finance broker qualification path, because compliance credibility starts with how the business is structured and trained.

Why FHA and UDAAP still matter to brokers

The Fair Housing Act, or FHA, becomes relevant when transactions touch real-estate-related credit. The key operational point isn't to memorize statutes. It's to recognize that housing-related lending creates another layer of anti-discrimination risk. If a broker touches commercial real estate, mixed-use property, or owner-occupied scenarios, that risk needs attention.

Then there's UDAAP or UDAP, the rules against unfair, deceptive, or abusive conduct. Even when a broker's conduct doesn't fit a classic discrimination claim, it can still create serious trouble if marketing overpromises, disclosures are muddy, or applicants are steered without a clear business reason.

A practical way to think about the legal environment is this:

- ECOA asks: Was the applicant treated differently in a credit transaction for an unlawful reason?

- FHA asks: Did housing-related credit conduct create discriminatory harm?

- UDAAP asks: Was the broker's conduct misleading, unfair, or abusive even if discrimination isn't the headline issue?

The safest broker isn't the one who talks about ethics the most. It's the one whose files show consistent treatment.

Common Violations and Everyday Red Flags

Most fair lending problems in brokerage don't start with obvious bias. They start with shortcuts. A broker gets busy, relies on instinct, and begins treating similar applicants differently without realizing a pattern is forming.

The law draws an important distinction here. Fair lending compliance separates disparate treatment, which is explicit discriminatory intent, from disparate impact, which is a facially neutral policy that disproportionately burdens protected classes. Evidence of intent isn't necessary to violate ECOA or the FHA if a policy lacks legal justification, and regulators use systematic risk assessments to identify discriminatory steering, redlining, and inconsistent discretionary pricing in underwriting, as described on the OCC fair lending page.

The two violation patterns that matter most

Disparate treatment is easier to spot. A broker gives one applicant more coaching because that applicant feels familiar, or avoids sending a file to a strong lender because the broker assumes the client won't qualify based on background rather than credit facts.

Disparate impact is more subtle. A brokerage adopts a policy that sounds neutral, such as focusing outreach only in certain zip codes or only partnering with referral sources that serve one narrow demographic. Nobody may intend discrimination. The effect can still exclude protected groups.

A few everyday examples make this concrete:

- A broker tells one business owner, “There's probably no point applying,” before collecting the same basic documents required from everyone else.

- A broker markets heavily in affluent areas and ignores majority-minority communities, even though the products offered could serve both.

- A broker routinely places some applicants into higher-cost options because “those deals close faster,” without a documented suitability process.

Fair Lending Red Flags for Loan Brokers

| Area of Operation | Red Flag Example | How to Correct It |

|---|---|---|

| Marketing | Ad copy uses coded language that suggests only certain types of applicants are welcome | Use broad, eligibility-based language focused on business profile and funding purpose |

| Lead intake | Staff ask different questions depending on who calls | Use one intake checklist for every inquiry |

| Pre-screening | Applicants are discouraged before a complete review | Require a documented minimum review before discussing likelihood |

| Product presentation | Some clients are shown only high-cost products | Present options based on objective fit and document why |

| Referral geography | The brokerage only markets or networks in limited areas without a business reason | Review outreach patterns and expand channels to avoid exclusionary habits |

| Record keeping | Notes are inconsistent, missing, or vague | Log conversations, recommendations, and reasons in a standard format |

The warning signs are often boring. That's why they're dangerous.

A broker should pay special attention to language that sounds harmless but pushes people away. “You probably won't qualify.” “This product is more realistic for someone like you.” “That lender is better for financially savvy borrowers.” Those aren't just sales phrases. They can become evidence of inconsistent treatment when repeated.

Compliance Best Practices for a Modern Broker

A modern broker doesn't win long term by being the fastest talker on the phone. The broker wins by being the most consistent operator. Strong fair lending practices protect the business, but they also improve execution. Referral partners trust a broker who runs a clean process. Applicants trust a broker who explains options clearly and treats every file with care.

A sound fair lending Compliance Management System, or CMS, is more than a policy binder. It's a governance framework that requires ongoing mystery shopping and self-testing so customer treatment stays consistent across marketing channels. It should include clear policies and procedures, regular training, dynamic risk assessments, and rigorous data analysis, as outlined in these best practices for strengthening a fair lending program.

Consistency beats charisma

The strongest brokerages standardize the moments where risk usually enters:

- First contact: Every prospect gets the same basic explanation of process, documentation, and next steps.

- File review: Every recommendation ties back to objective factors such as business history, cash flow profile, use of funds, and lender criteria.

- Lender matching: The broker documents why a lender or product was selected and why alternatives were not.

That structure matters more in a home-based business because there usually isn't a compliance officer looking over anyone's shoulder. The workflow itself has to enforce discipline. A broker who wants a cleaner operation can borrow practical ideas from broader guidance on good business compliance practices and adapt them into simple internal rules.

Mystery shopping is especially useful. Have someone review the website, fill out a lead form, or call the brokerage posing as a prospect. Then compare whether the experience stays consistent. If the message changes depending on tone, accent, location, or assumptions about sophistication, the process needs work.

Compliance becomes a brand asset

There's a business upside to this. Referral partners don't want to send clients into a sloppy process. Accountants, consultants, agents, and service professionals tend to keep referring when a broker is predictable, respectful, and well documented.

A broker can turn compliance into a competitive advantage by doing a few things well:

- Use scripts without sounding scripted. The goal is consistency, not stiffness.

- Review marketing quarterly. Old ad copy often contains the most overlooked risk.

- Audit exceptions. If the broker makes judgment calls, those calls need written reasons.

- Improve process continuously. Even simple workflow reviews can tighten quality, especially when borrowing ideas from a broader process improvement example for small businesses.

Clean documentation tells referral partners that the broker is serious. It also tells regulators that decisions weren't random.

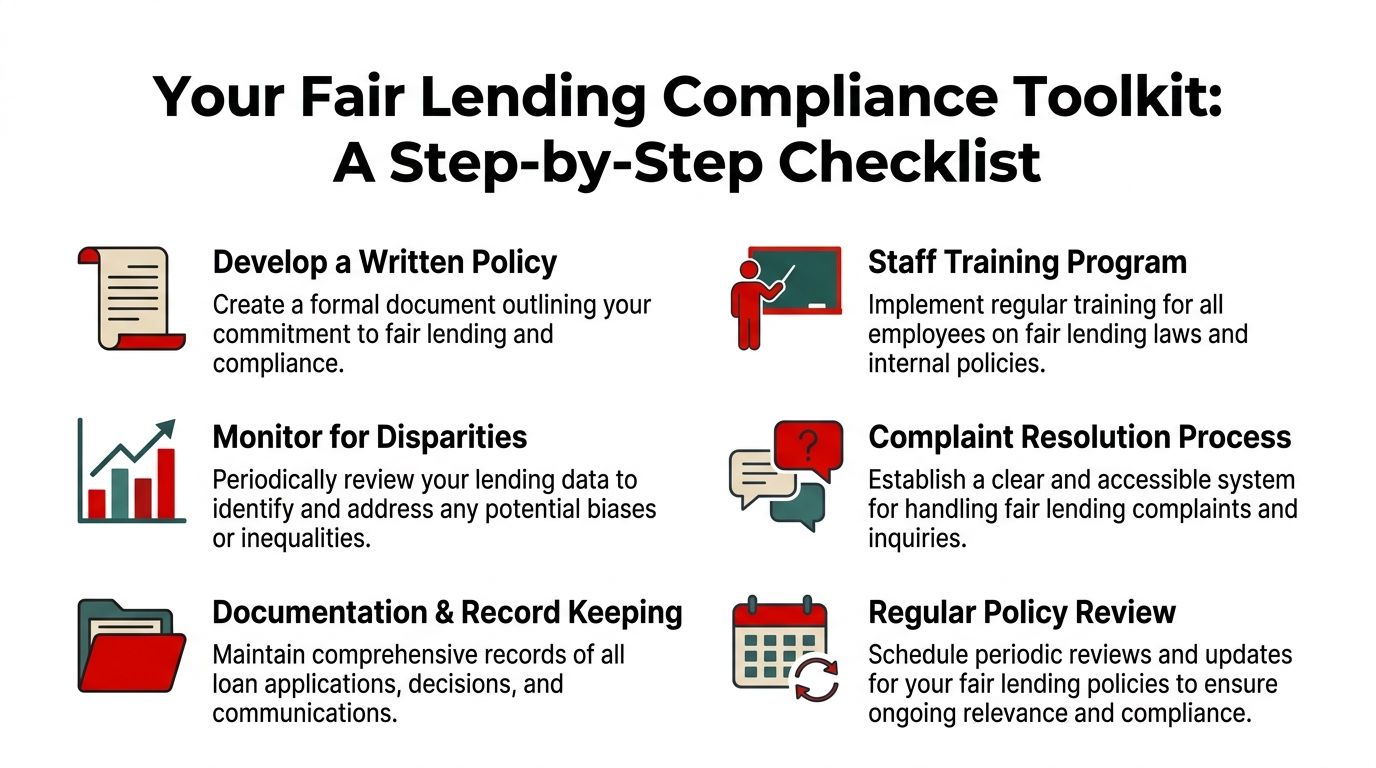

Your Fair Lending Policy and Documentation Toolkit

A one-person brokerage can build a practical compliance toolkit without making the business heavy or bureaucratic. The goal isn't complexity. The goal is proof. If someone asks how the brokerage promotes fair lending practices, the answer should live in written policy, documented workflows, and complete records.

Institutions with heightened fair lending risk are expected to conduct annual fair lending risk assessments that examine inherent risk, controls that mitigate risk, and residual risk. Sound practices also include written policies, oversight over discretion, and second reviews for denials to prevent disparities, according to this summary of statistical fair lending analyses and risk assessment expectations.

Build a simple policy that actually gets used

A strong policy for a small brokerage should fit on a few pages and cover the basics clearly.

Include these elements:

- Statement of commitment: The brokerage provides equal and fair access to financing opportunities and doesn't discriminate in inquiries, intake, referrals, or communications.

- Scope of coverage: The policy applies to marketing, lead handling, intake, lender submissions, follow-up, and record retention.

- Decision standards: Recommendations must rely on objective business and credit factors, not assumptions or stereotypes.

- Escalation rule: Any unusual case, complaint, or uncertainty gets reviewed before the broker declines to proceed.

This doesn't need legal jargon. It needs operational language that the brokerage will actually follow.

A useful companion to the policy is a documented business loan application process that shows exactly how applicants move from inquiry to submission. If the process is consistent, the compliance posture is usually stronger.

Create records that explain decisions

Documentation should answer three questions. What happened? Why did it happen? Was the same approach used consistently?

A practical toolkit includes:

- Intake script: Standard opening questions focused on business need, time in business, revenue pattern, credit profile, requested amount, and use of proceeds.

- Communication log: Date, contact method, summary of discussion, documents requested, options discussed, and next action.

- Referral rationale note: Why the broker chose a lender or product, and what factors supported that choice.

- Complaint tracker: Even a small spreadsheet works if it captures issue, date, response, and corrective action.

A second review process also helps. If the broker plans to stop working a file, decline to submit, or present only limited options, the file should be rechecked against policy. In a solo operation, that may mean waiting, reviewing notes, and confirming that the decision is based on documented criteria rather than instinct.

The file should tell the story even if the broker isn't there to explain it.

Build Your Business the Right Way

A brokerage built on fair lending practices is easier to scale, easier to defend, and easier to trust. That matters for anyone building from home, relying on referrals, and trying to create a business that lasts through changing markets.

The practical path is straightforward. Learn the rules. Remove discouraging language. Standardize intake. Match applicants based on fit. Document exceptions. Review complaints and weak spots before they become patterns. None of that slows growth. It supports growth by making the business more stable.

The best part is that ethical discipline and commercial success aren't competing goals. In this business, they support each other. A broker who treats applicants consistently creates better lender relationships, stronger referral confidence, and a reputation that compounds over time.

For aspiring brokers, that's a significant opportunity. Not just earning commissions on funded deals, but building a respected lending business that works remotely, serves business owners well, and stands up to scrutiny when the stakes get higher.

Business Lending Blueprint shows aspiring brokers how to start and grow a profitable lending business the right way, with practical systems for referrals, lender relationships, deal flow, and compliance-minded operations. It doesn't provide loans. It provides training for people who want to build a real brokerage business from home with flexibility, scalability, and long-term credibility. To take the next step, watch the free training from Business Lending Blueprint or schedule a strategy session to see how the model works.