Most states don't require a license for business loan brokering, while mortgage brokering usually requires 20 to 30 hours of pre-licensing education and a 75% passing score on the SAFE Mortgage Loan Originator exam. That difference makes business lending far more accessible for aspiring entrepreneurs who want to get into finance without the usual regulatory drag.

That's the part most advice gets wrong. It lumps every kind of broker into one bucket, then hands people a mortgage licensing checklist as if it applies to all finance brokering. It doesn't.

Those seeking finance broker qualifications are frequently guided toward the industry's most regulated sector initially. That's backward. The smarter path for many aspiring brokers, consultants, sales professionals, CPAs, bankers, and service providers is business lending. It can be home-based, remote, relationship-driven, and far easier to enter than residential mortgage brokering.

The crucial question isn't whether someone can survive a licensing maze. It's whether that person can learn how to help business owners secure funding, build lender relationships, and create a steady pipeline of deals. Those are the qualifications that matter.

Table of Contents

- What Are Finance Broker Qualifications Really

- Mortgage Broker vs Business Loan Broker Requirements

- The Skills You Need to Succeed in Business Lending

- Your Blueprint for Launching a Broker Business

- What to Expect Financially as a Finance Broker

- Traits of a Successful Independent Broker

- Take the Next Step with Business Lending Blueprint

What Are Finance Broker Qualifications Really

Many assume the wrong thing when they ask about finance broker qualifications. They assume qualifications are licenses, exams, and state paperwork. That's true for mortgages. It's often not true for business lending.

In many jurisdictions, commercial lending sits in a completely different category. Florida's Office of Financial Regulation states that most commercial lending is exempt. That single point changes the whole conversation.

The common assumption is wrong

The internet loves to recycle residential mortgage rules because they look official and complicated. But complexity doesn't equal relevance. For someone who wants to broker business loans, those mortgage requirements can be a distraction.

A better way to think about qualifications is this:

- Legal eligibility: Whether a state requires a license for the specific kind of brokering being done.

- Commercial competence: Whether the broker can understand deals, communicate clearly, and match business owners with the right funding path.

- Operational readiness: Whether the broker has a process for lead flow, lender access, file packaging, and follow-up.

That's the framework that matters in business lending.

Business lending rewards practical skill faster than paperwork.

The hidden opportunity in plain sight

A lot of talented people talk themselves out of this business because they think every path into finance starts with regulators, exams, and long wait times. That isn't the only path. For many people, the better route is to start where the barriers are lower and the service need is obvious.

Business owners need capital. They need help sorting through options. They need someone who can translate funding products into plain English and move deals forward. That role doesn't always require a government license. It does require judgment, responsiveness, and the right training.

For readers exploring a practical entry point, this guide on small business lending training and how to become a finance broker is a useful next read because it focuses on the business lending side instead of forcing mortgage rules onto the wrong model.

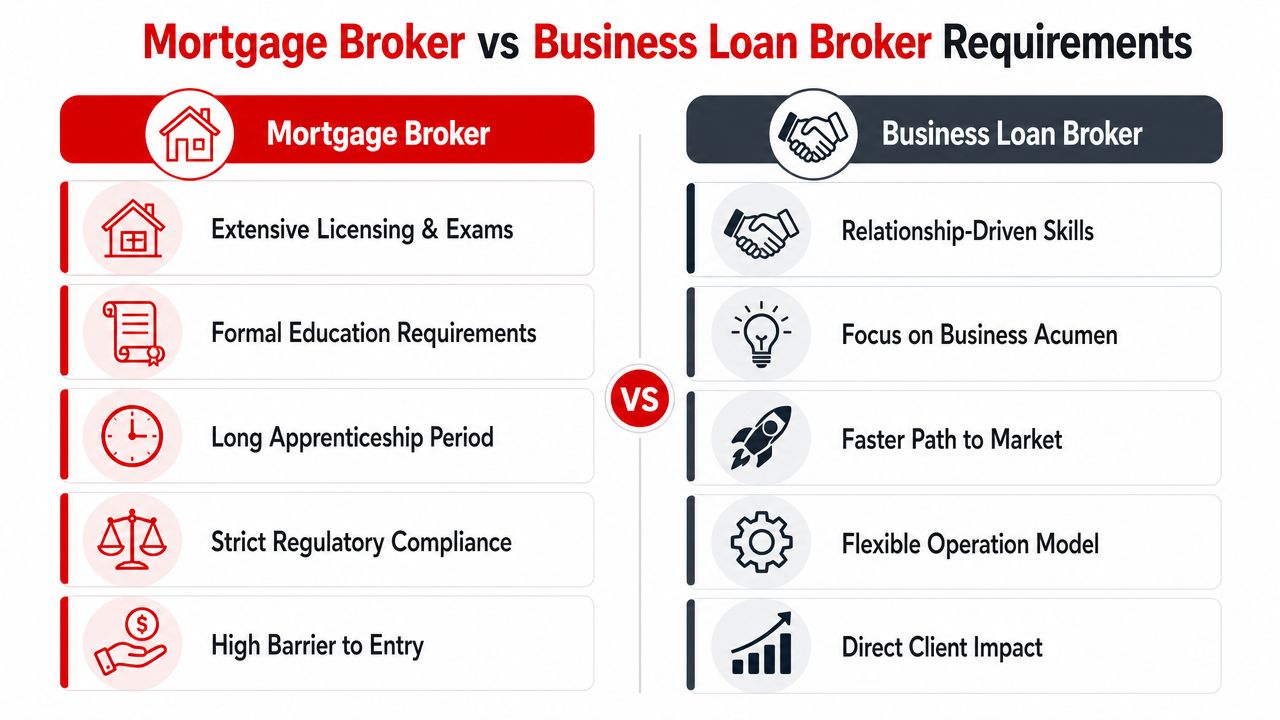

Mortgage Broker vs Business Loan Broker Requirements

If someone wants a clean answer, here it is: mortgage brokering is regulated like a gate-kept profession. Business loan brokering is often more like a consultative sales and advisory business.

That difference matters because it affects time to launch, cost, paperwork, and who can realistically enter the field.

What mortgage brokers usually face

To become a mortgage broker in the U.S., applicants generally must complete 20 to 30 hours of NMLS pre-licensing education, including three hours on federal law and regulations, three hours on ethics, two hours on nontraditional mortgage products, and twelve hours of electives, then pass the SAFE Mortgage Loan Originator exam with a minimum 75% on both the standard and Uniform State Test portions, according to Harbor Compliance's mortgage broker licensing overview.

That's only part of the picture. The same overview explains that training must be completed no more than three years before applying, exam results are typically available within 72 hours, and most states require one to three years of prior finance industry experience before someone qualifies for a broker license.

Then there's the bond requirement. Mortgage brokers may need to post a surety bond ranging from $50,000 to $150,000, with tiers tied to prior loan volume, as outlined in this Maryland mortgage broker bond explanation.

What business loan brokers usually face

For commercial lending, the path is lighter. Most states don't require commercial loan brokers to hold a license, though laws can vary and evolve. Anyone considering the mortgage side as a separate business model can review how to start a mortgage lending company and see how different the setup is.

The contrast is easiest to understand side by side:

| Category | Mortgage broker | Business loan broker |

|---|---|---|

| Entry path | Formal licensing process | Often license-exempt, depending on jurisdiction |

| Education | NMLS pre-licensing coursework | Practical training and deal knowledge |

| Testing | SAFE exam required | No equivalent exam in most states |

| Financial barriers | Bonding and other state-level requirements | Usually far leaner startup structure |

| Speed to market | Slower | Faster |

Which path makes more sense

For most aspiring entrepreneurs, business lending is the better first move. It lets a new broker focus on relationship-building, product knowledge, and client acquisition instead of spending months trying to qualify for a heavily regulated license.

Practical rule: If the goal is to build a remote, home-based brokerage quickly, business lending is usually the cleaner entry point.

That doesn't make mortgage brokering bad. It makes it specialized. Business lending is more accessible for people who want to start now, serve small businesses, and avoid burdens that don't apply to commercial deals.

The Skills You Need to Succeed in Business Lending

The absence of a license requirement doesn't mean the absence of standards. It means the standards shift from bureaucracy to performance.

A business loan broker's typical educational foundation is a high school diploma or GED, and focused training programs often last 1 to 2 weeks while covering skills like evaluating loan applications and marketing the business, according to Ameris Bank's overview of becoming a business loan broker.

Skill beats credentials in this niche

Business owners don't care whether a broker memorized a state test outline. They care whether that broker can help them secure funding and avoid wasting time.

The strongest brokers usually develop capability in a few core areas:

- Deal evaluation: They can review a file, spot obvious weaknesses, and decide whether the borrower fits the likely lender profile.

- Product fluency: They understand how common business funding options differ in structure, use case, and borrower fit.

- Client communication: They can explain terms in plain language without sounding vague or evasive.

- Referral development: They know how to build relationships with professionals who already serve business owners.

The practical qualifications that matter

A useful way to judge readiness is to ask whether someone can handle the work below consistently:

- Review a basic application package without getting lost in jargon.

- Ask follow-up questions that improve the file instead of slowing it down.

- Present realistic funding options rather than chasing impossible deals.

- Maintain communication with both borrower and lender until the deal closes.

Those are trainable skills. That's good news for career changers, consultants, and sales professionals who already know how to build trust.

Strong brokers don't win because they know more legal trivia. They win because they communicate clearly, package files well, and follow through.

A person with discipline, business sense, and coachability can become highly effective in this industry without the traditional barriers that dominate mortgage content.

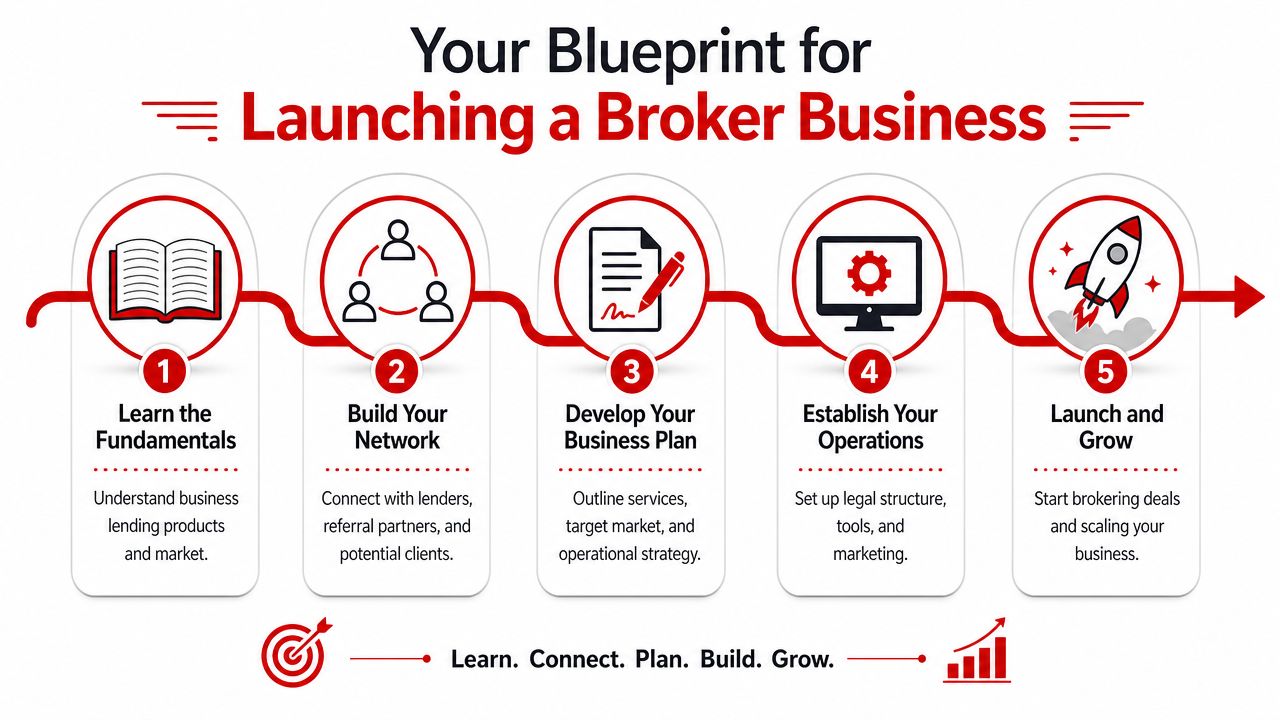

Your Blueprint for Launching a Broker Business

A business loan brokerage doesn't need to start big. It needs to start clean. The best launches are simple, lean, and focused on getting competent fast.

Most states exempt commercial loan brokers from licensing, but laws can change. California is considering Senate Bill 869, which would require licensing for brokers handling commercial loans of $5,000 or more, according to Mayer Brown's analysis of California Senate Bill 869. That's why smart operators verify the rules in the jurisdictions where they plan to work.

A lean launch model works best

Most new brokers make one of two mistakes. They either overbuild and waste time on branding details, or they underprepare and start pitching deals they can't package properly.

A better launch sequence looks like this:

- Learn the lending fundamentals: Understand borrower profiles, common funding scenarios, and how lenders evaluate opportunities.

- Choose a simple business structure: Keep operations clean, documented, and easy to manage from a home office.

- Build lender access early: A broker without lender relationships is just a marketer with nowhere to send files.

- Create a referral plan: Relationships with professionals who already serve business owners produce better leads than random outreach.

- Install a repeatable process: Intake, document collection, lender matching, and follow-up should work the same way every time.

Compliance first, speed second

Launching quickly matters, but clean setup matters more. If the business will operate in California, formation details deserve special attention because state rules and compliance steps can affect how the brokerage is structured. This ultimate California business formation guide is a useful resource for understanding those setup considerations.

A practical roadmap for getting the brokerage off the ground is outlined in this guide on how to start a loan business. The key is keeping the operation lean enough to launch and structured enough to grow.

What the first operating phase should look like

The early phase should be boring in the best way. It should focus on consistency, not theatrics.

| Priority | What it should look like |

|---|---|

| Lead intake | Clear process for collecting borrower details and documents |

| Lender relationships | Organized communication and fit-based submissions |

| Referral development | Ongoing contact with professionals serving small businesses |

| Workflow | Standard checklist from inquiry to funded deal |

Operator's view: A new brokerage doesn't need a fancy setup. It needs a reliable process that clients and referral partners can trust.

That's how a home-based brokerage becomes scalable. Not by trying to look huge, but by handling deals with discipline.

What to Expect Financially as a Finance Broker

The business lending model gets attractive because the cost structure is lighter than the mortgage route, the timeline is shorter, and the revenue model is straightforward.

Commercial loan brokers typically negotiate commissions between 1% and 2.5% of the total loan amount, and that often translates into $1,000 to $15,000 per funded deal, according to this commercial loan broker commission overview.

The financial model is simple

A broker earns by bringing together the right borrower and the right capital source. That means income depends on funded deals, not on punching a clock.

The advantage of this model is flexibility. A broker can start part-time, build referral relationships, and grow into a full-time operation without carrying the fixed overhead of a traditional office.

The real cost question

The wrong comparison is business lending versus a salaried finance job. The right comparison is business lending versus a highly regulated brokerage path with licensing fees, bonds, and qualification hurdles.

Mortgage licensing can involve meaningful upfront costs and ongoing state-level obligations, as covered earlier. Business lending usually avoids much of that burden, which improves the risk-reward profile for a new entrant.

For brokers who want to grow through education and referral-based visibility instead of random promotion, this resource from Gilkes Media on financial marketing offers useful perspective on how financial service businesses can approach marketing more strategically.

What realistic growth looks like

A serious broker should think in stages:

- First stage: Learn the products, understand deal fit, and close initial files cleanly.

- Second stage: Build referral relationships that create recurring opportunities.

- Third stage: Systematize follow-up, lender communication, and lead handling so volume doesn't create chaos.

Readers who want a deeper breakdown can review this article on business loan broker salary, which explains how commission-based earnings scale in practice.

A funded-deal model won't suit people who want guaranteed paychecks with zero variability. It does suit people who want a business with low overhead, remote flexibility, and direct upside tied to performance.

Traits of a Successful Independent Broker

Some people are a natural fit for this business long before they know the funding products. Others hate it even if they understand the mechanics.

The strongest independent brokers usually share a few traits. None of them require a license. All of them affect whether the business lasts.

They like solving messy problems

Business owners rarely show up with perfect files, tidy explanations, and ideal timing. A successful broker doesn't get frustrated by that. That broker asks better questions, organizes the facts, and keeps the deal moving.

People from consulting, sales, tax, banking, insurance, and client service roles often adapt well because they already know how to bring order to imperfect situations.

They're relationship-builders, not script-readers

This business rewards trust. Referral partners send deals to people who communicate well, protect relationships, and don't overpromise.

A strong broker usually does the following:

- Listens closely: Borrowers often reveal the underlying issue after the first answer, not during it.

- Sets expectations well: Clear communication prevents confusion and protects credibility.

- Stays organized: Deals stall when documents, deadlines, and conversations get scattered.

- Follows up without being pushy: Persistence matters, but professionalism matters more.

The best independent brokers act like advisors, not order-takers.

They want autonomy more than titles

A lot of people chase finance careers for prestige. Independent brokers usually want something different. They want control over schedule, income potential, client mix, and where they work.

That's why this path appeals to career changers, side-hustlers, veterans leaving structured employment, and professionals who want to add funding solutions to an existing client base. The work is practical, remote-friendly, and tied to real business needs. That combination gives it staying power.

Take the Next Step with Business Lending Blueprint

The best answer to the finance broker qualifications question is also the simplest one. For mortgage brokering, the qualifications are formal and regulated. For business lending, the qualifications are mostly practical. Learn the business, understand how deals work, build lender relationships, and operate with discipline.

That distinction creates a major opportunity. It opens the door to entrepreneurs who want a home-based, flexible, recession-resistant business without getting buried in the licensing framework that applies to residential mortgages.

People who do well in this field don't wait for permission to start building useful skills. They focus on becoming valuable to business owners. They learn how to evaluate opportunities, structure conversations, and create reliable referral channels.

That's why the fastest route usually isn't chasing the most complicated credential. It's choosing the part of the finance industry that offers a cleaner entry point and then getting trained properly.

For aspiring entrepreneurs, consultants, sales professionals, CPAs, bankers, and anyone who wants to build a scalable remote brokerage, business lending is the clearer path. It offers flexibility, recurring referral relationships, and a service that business owners need in every economy.

Business Lending Blueprint shows everyday people how to build a profitable, home-based business as a business loan broker. The program focuses on practical training, vetted lender access, and a referral-driven model that helps brokers work remotely while serving business owners with real funding solutions. To see how the model works, watch the free training at Business Lending Blueprint or schedule a strategy session to map out the right path forward.