A new broker often gets the same email early in a client relationship. A business owner finds a building, gets excited, and forwards a short document with one question: can this be funded?

That document is usually the first real filter on the deal. Before tax returns, before bank statements, before a lender asks for a full package, the Letter of Intent tells a broker whether the transaction has structure or just enthusiasm. If the terms are clean, the broker can move quickly. If the terms are sloppy, missing, or risky, the funding path gets harder and the broker's commission gets less certain.

For anyone trying to build a flexible, remote business helping owners secure financing, understanding what a letter of intent in real estate is matters more than is often realized. It helps a broker protect the client, preserve momentum, and become the person who spots trouble before money and time get wasted.

Table of Contents

- The Broker's First Look at a Potential Deal

- Decoding the Letter of Intent What It Really Means

- Anatomy of a Real Estate LOI Key Clauses to Scrutinize

- LOI vs Purchase Agreement Know the Critical Differences

- The Broker's Playbook Negotiation Tips and Risk Avoidance

- From LOI to Funded Deal Your Next Steps to Success

The Broker's First Look at a Potential Deal

A buyer sends over a one-page LOI for a warehouse, office condo, or mixed-use building. The client usually focuses on the property and the price. The broker has to focus on something else first. Are the terms written in a way that gives the deal a realistic path to financing?

At this stage, the LOI isn't just paperwork. It's a screening tool. It tells a broker whether the buyer has enough time for underwriting, whether the seller is serious, whether due diligence is realistic, and whether the transaction looks organized enough to present to lenders without immediate friction.

What the LOI tells a broker right away

A broker reading an LOI for funding purposes should look for the practical issues first:

- Timeline pressure: If the closing target is aggressive and the document doesn't leave room for underwriting, appraisals, or property review, the deal may stall before it starts.

- Client readiness: A buyer who signs broad terms without understanding financing conditions may be setting up avoidable conflict later.

- Seller posture: Some sellers want speed. Others want control. The LOI often reveals which side is driving the paper.

Practical rule: The broker who reads the LOI early looks smarter than the broker who waits for the purchase contract and then starts raising problems.

A good broker also understands that the LOI is where reputation starts to form. Business owners remember who forwarded paperwork and who helped them interpret risk. That distinction matters in a referral-driven business.

Why this matters for a loan broker business

The funding side of commercial deals rewards people who can move from opportunity to structure fast. Brokers who build durable businesses often do it by working remotely, partnering with strong lenders, and creating referral relationships that produce repeat opportunities. That model is part of why many brokers aim for a home-based, scalable business with recurring introductions and steady deal flow, as discussed in this overview of high-value lender partnerships and referral-based broker growth.

A broker who can read an LOI and say, "this is workable," "this needs revision," or "this seller timeline will create financing pressure," becomes far more valuable than someone who only shops paper.

Clients dealing with lease-related property questions can also benefit from legal context outside the financing lane. For Texas transactions, this expert Houston commercial lease guide is useful background when occupancy terms and lease structure affect the deal.

A strong LOI review also ties directly into loan packaging. If the broker knows what lenders need before the file goes out, the borrower can prepare earlier. That shortens confusion and improves execution. This is the same discipline behind understanding requirements for a commercial loan, where complete files tend to move better than reactive ones.

Decoding the Letter of Intent What It Really Means

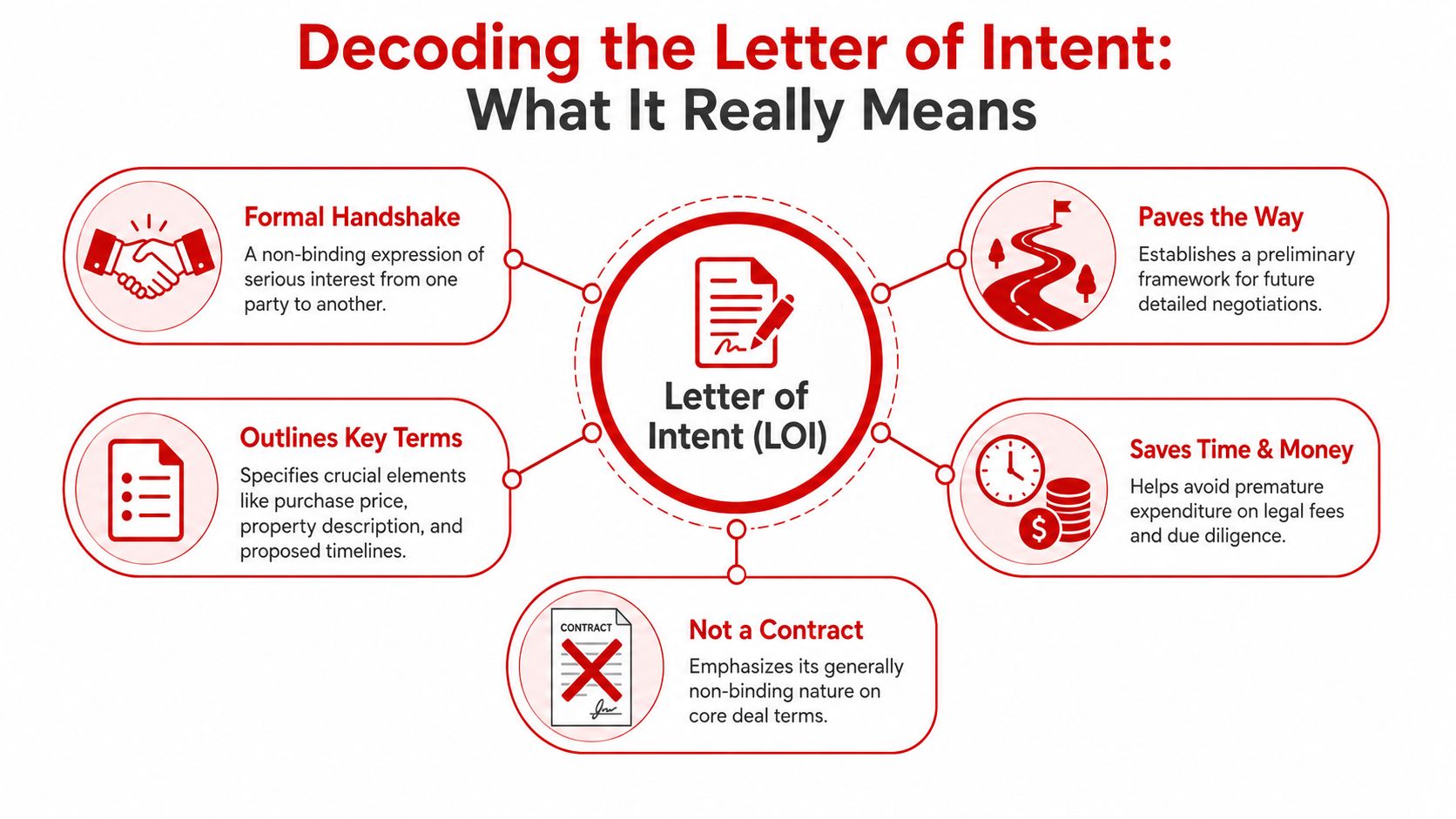

A Letter of Intent, or LOI, is a preliminary real estate document that sets out the main business terms before a formal contract gets drafted. In commercial transactions, it's usually short. According to Rochford Lawyers on commercial real estate letters of intent, an LOI is generally non-binding, is typically 1 to 3 pages, and often includes legally enforceable provisions on items like confidentiality and exclusivity even when the main deal terms aren't binding.

That single point trips up new brokers and buyers all the time. They hear "non-binding" and assume the whole document can be ignored. That's not how it works in practice.

The simplest way to think about an LOI

The LOI is the business framework for the deal. It answers the big questions first so the parties don't waste time paying lawyers and chasing documentation before they even agree on the basic economics.

A practical way to view it is as a test drive. The buyer and seller get to see whether they align on the core points before they commit to heavier costs, deeper diligence, and final legal drafting.

What the LOI is trying to accomplish

A solid LOI usually does three jobs at once:

- It confirms serious interest. The buyer isn't casually browsing anymore.

- It frames the negotiation. Price, timing, deposit, diligence, and financing get put on paper.

- It preserves optionality. The parties can explore the deal without treating it like a completed contract.

That last point matters a lot in funding. A buyer may need time to review financials, inspect the property, or test lender appetite. If the deal doesn't hold up under scrutiny, the LOI stage allows the parties to step back before the formal purchase agreement hardens everything.

A good LOI saves effort. A bad LOI just delays the argument until after everyone has spent more money.

What non-binding actually means

Non-binding doesn't mean meaningless. It means the LOI usually isn't the document that forces the purchase or sale itself.

That gives buyers room to investigate the asset and confirm that financing, legal, and operational realities support the transaction. Sellers benefit too. They get a structured expression of interest rather than vague verbal discussions.

Here are the trade-offs:

- What works: Clear core terms, realistic deadlines, and explicit language on what is and isn't binding.

- What doesn't: A vague LOI with missing business points and no clear treatment of confidentiality, exclusivity, or expiration.

For a broker, the value is straightforward. The LOI shows whether the transaction has enough definition to start lining up financing conversations without pretending the deal is already done. That balance is exactly why seasoned brokers pay attention to the LOI before anyone celebrates a closing that hasn't happened.

Anatomy of a Real Estate LOI Key Clauses to Scrutinize

Commercial real estate LOIs are short, but they carry a lot of weight. According to CARR's CRE glossary entry on letters of intent, standard CRE LOIs are typically 1 to 3 pages and often include the property address, square footage, purchase price, earnest money deposit, due diligence period, financing structure, and an expiration window of 5 to 10 business days. The due diligence period is often 30 to 60 days.

Those aren't filler terms. They're the first indicators of whether a lender will see a coherent transaction or a moving target.

What belongs in the document

A broker should expect to see the core terms below, even if the wording differs from one LOI to the next.

| Clause | What it does | Why a broker cares |

|---|---|---|

| Purchase price | States the proposed economic basis of the deal | It anchors loan sizing and capital stack discussions |

| Earnest money deposit | Shows the buyer's commitment level | It affects risk perception and negotiating posture |

| Due diligence period | Gives the buyer time to inspect and verify | It creates room for underwriting and third-party review |

| Financing structure | Signals whether debt is part of the plan | It tells the broker how early to shape lender strategy |

| Closing date | Sets the target for execution | It determines whether the timing is realistic |

| LOI expiration | Forces a response window | It keeps negotiations from drifting |

A document can be short and still be complete. Concise is fine. Missing terms aren't.

What a broker should flag immediately

The broker's job isn't to rewrite legal language. It's to identify whether the business terms help or hurt fundability.

- Purchase price that doesn't match reality: If the price pushes the asset beyond what income, use, or condition can reasonably support, lenders may become conservative quickly.

- Deposit language with no clarity: If earnest money treatment is vague, disputes can start before the loan package is even assembled.

- Thin diligence window: A buyer who accepts too little diligence time may lose negotiating power before inspections, underwriting, and title work are complete.

- No financing clarity: If the LOI ignores financing altogether, the broker may have to untangle assumptions that should've been addressed earlier.

Deal note: A lender can work around a lot of issues. Confusion on timing and structure is harder to solve than a borrower usually expects.

Strong terms versus weak terms

A strong LOI doesn't need to be aggressive. It needs to be usable.

Stronger LOI language tends to have these characteristics:

- Specific business terms: The property, economics, and timeline are clearly identified.

- A workable diligence period: The buyer has enough room to investigate and line up debt.

- A visible financing path: The parties acknowledge how the acquisition is expected to be funded.

- A clean response deadline: The seller must engage or decline within the stated window.

Weaker LOI language usually creates these problems:

- Undefined deadlines: No one knows when decisions need to happen.

- Half-written economics: Price appears, but related terms are left open.

- Compressed timing: Underwriting gets squeezed, then blamed when the clock becomes unrealistic.

- Hidden friction points: Costs, conditions, or occupancy issues only emerge later.

For brokers underwriting the file mentally before it ever reaches a lender, the due diligence period often matters more than new trainees realize. If that period is too short, the client may not have enough time to gather documents, answer lender questions, review the property, and still negotiate from strength.

That concern ties directly into cash flow analysis as well. The better the broker understands how a lender will test repayment strength, the earlier weak spots can be addressed. A useful starting point is this guide to debt service coverage ratio calculation, because the LOI may look fine on paper while the income side still creates a financing problem.

LOI vs Purchase Agreement Know the Critical Differences

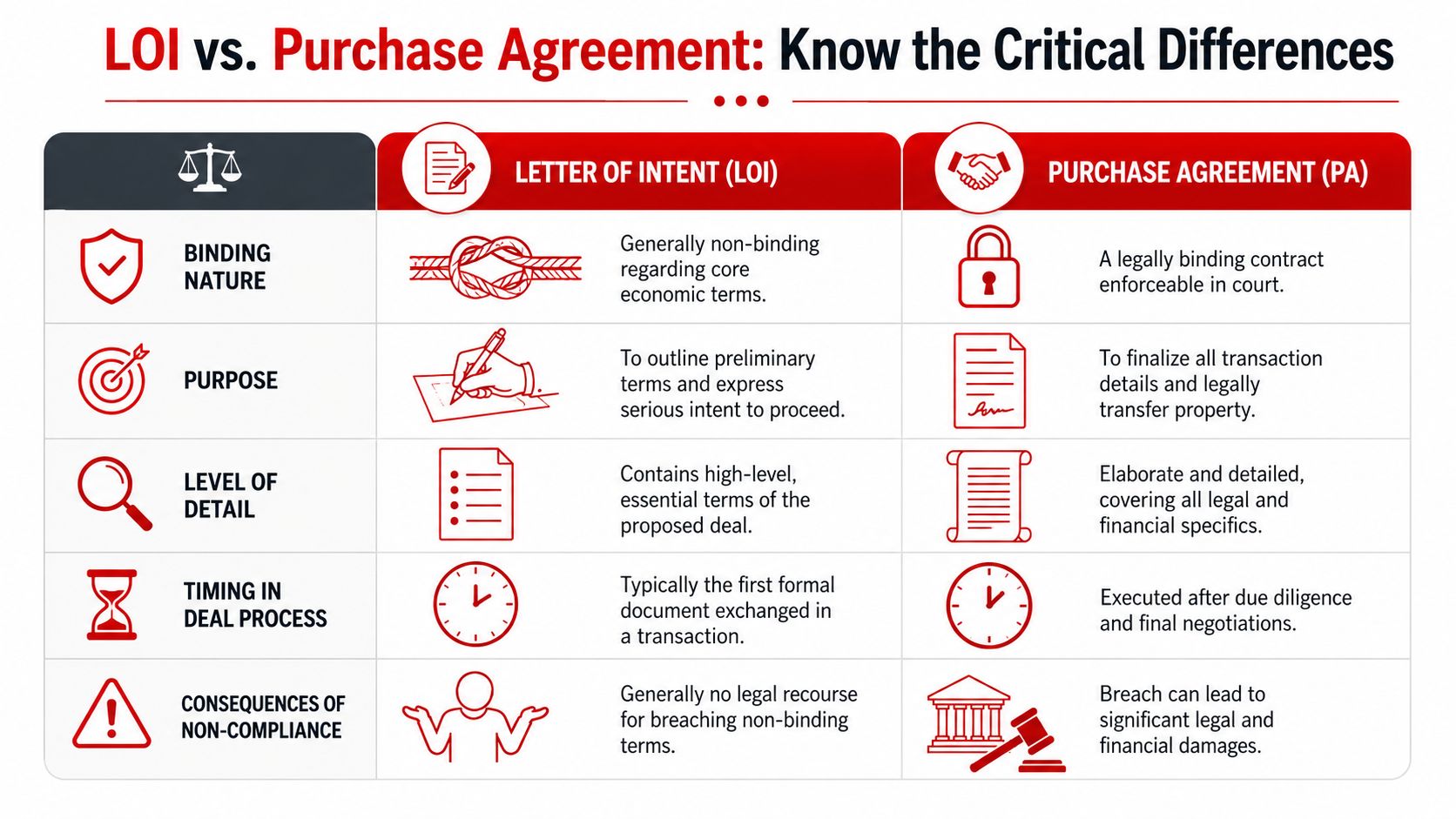

Clients confuse these two documents because both describe the same transaction. The difference is legal weight and operational consequence.

An LOI is the opening business outline. A purchase agreement is the detailed contract that governs the sale. As explained in Bean Kinney's overview of letters of intent, the LOI is an agreement to agree. It exists so the parties can align on main points before committing to a full contract and the costs that come with it.

Side by side differences

| Issue | LOI | Purchase agreement |

|---|---|---|

| Purpose | Frames the proposed deal | Finalizes the legal transaction |

| Binding effect | Usually limited on core terms | Intended to be enforceable |

| Detail level | High-level business points | Extensive legal and financial detail |

| Timing | Early in the process | Later, after negotiations deepen |

| Funding use | Helps a broker assess viability | Supports formal lender review and closing process |

The LOI asks, "Do the parties broadly agree?" The purchase agreement asks, "What exactly happens, when, under what conditions, and what if something goes wrong?"

Why clients confuse them

From a buyer's perspective, signing either document can feel like a commitment. Emotionally, that's true. Legally, they aren't the same.

The confusion usually shows up in three ways:

- The buyer assumes the LOI guarantees the property. It usually doesn't, unless binding rights were drafted into parts of it.

- The buyer thinks the purchase agreement is just a longer version of the LOI. It isn't. It adds legal precision, remedies, representations, conditions, and closing mechanics.

- The buyer expects financing to fit automatically once the LOI is signed. That expectation creates pressure if the purchase agreement is negotiated on timelines that don't match lender reality.

A broker who explains this distinction clearly reduces panic later. That matters because funding delays often aren't caused by the loan itself. They're caused by a borrower treating an early-stage document like a final commitment and then building unrealistic expectations around it.

The LOI opens the door. The purchase agreement decides what happens after everyone walks through it.

The Broker's Playbook Negotiation Tips and Risk Avoidance

A passive broker waits for the signed contract and then tries to solve problems. A better broker gets involved at the LOI stage, because that's where preventable mistakes are still cheap to fix.

One of the most overlooked risks is enforceability. The "non-binding" label doesn't always protect the parties. According to the North Carolina Realtors discussion of LOI enforceability, courts can enforce LOIs as binding contracts when they contain definite terms and mutual assent, and LOI-related litigation has increased where non-binding language failed because other provisions created enforceable obligations. That nuance matters for every broker advising a client who thinks an LOI is harmless.

Terms that help a deal get funded

The broker should push for business terms that preserve flexibility without making the client look unserious.

Consider these priorities:

- Room for diligence: A buyer needs enough time to investigate the asset and complete financing work without negotiating under panic.

- Clarity on financing: If debt will be used, the LOI shouldn't pretend otherwise.

- Defined exclusivity if needed: If the seller is expected to stop shopping the deal, that needs to be explicit and understood.

- Clear expiration mechanics: A floating offer creates confusion and wasted motion.

In these circumstances, brokers protect both the borrower and their own commission. If the terms leave no room for lender review, the borrower may blame the financing side for a problem created on page one of the deal.

Risk that can trap a buyer early

The biggest practical danger is sloppy drafting around binding versus non-binding sections. A client may think, "It's just an LOI," while signing enforceable duties on confidentiality, exclusivity, or negotiation conduct.

That risk gets worse when the buyer hasn't thought through what happens if inspections reveal issues or financing terms change. Negotiation discipline matters here. Buyers trying to rework economics later often do better when they understand how property findings affect their negotiating advantage. For residential-style negotiation logic that illustrates this principle well, this homebuyer's guide to price reduction offers a useful example of how new information changes bargaining position.

A broker should also watch for these red flags:

- Exclusivity with no financing path: The buyer gets locked into the process while still uncertain about debt options.

- No practical diligence cushion: The client may lose the chance to exit cleanly if material issues appear.

- Overconfidence from the seller side: Fast timelines can sound efficient but may narrow the buyer's ability to close.

- Loose client communication: When expectations aren't managed early, every later delay feels like failure.

Good brokerage is often expectation management disguised as deal management. Clients need straight answers on timing, conditions, and risk from the start. This guide on how to manage client expectations fits that reality well, especially when a borrower starts assuming that a signed LOI means guaranteed funding.

Brokers add value when they prevent bad commitments, not just when they submit applications.

From LOI to Funded Deal Your Next Steps to Success

Once the LOI is signed, the transaction moves from interest to execution. At this point, many deals either become organized or start drifting.

The broker's role is straightforward. Turn the LOI into a funding roadmap, identify missing items early, and keep the client moving in an order that lenders can work with.

A clean post-LOI checklist

After a signed LOI is in hand, the next moves should be disciplined:

Confirm the business terms

Make sure the buyer understands the economics, timing, and any binding provisions that survived the signing.Get legal review moving

Counsel should review the LOI and begin shaping the purchase agreement so the borrower doesn't discover major conflicts later.Start due diligence immediately

Property review, financial review, title questions, occupancy issues, and condition concerns shouldn't wait.Prepare the financing file

Gather borrower and property documents in the format lenders will expect.Match the deal to the right financing lane

Some deals fit conventional underwriting. Others need a more flexible structure. In tighter or time-sensitive situations, borrowers often explore options like hard money commercial loan.Coordinate toward closing

Keep legal, borrower, seller, and lender timelines aligned so the purchase agreement and loan process don't move in conflict.

A borrower who wants a plain-English overview of what happens after the financing process starts can also benefit from this mortgage application process explained, especially when trying to understand how paperwork, underwriting, and closing stages connect.

The larger lesson is simple. Knowing what a letter of intent in real estate is isn't enough. A broker needs to know how to read it, pressure-test it, and use it to determine whether the deal deserves lender attention. That's how brokers become trusted funding partners instead of paper pushers. It's also how a remote, referral-based business becomes more stable, more scalable, and more valuable over time.

Business Lending Blueprint shows aspiring brokers, consultants, bankers, CPAs, sales professionals, and career changers how to build a profitable home-based business helping owners secure funding through alternative lenders. The model is built around practical deal flow, flexible remote work, scalable systems, commissions that are typically earned when loans close, and referral relationships that can produce repeat business over time. To learn how to turn opportunities like real estate and business funding requests into a recession-resistant brokerage, watch the free training at Business Lending Blueprint or schedule a strategy session.