A broker gets a client approved for a financing path that looks promising on Monday. By Thursday, the lender asks for updated bank statements, the client goes quiet, and by next week the borrower is angry because they thought funding was already on the way. Nothing “went wrong” in the technical sense. The actual problem started earlier, when the broker let hope replace process.

That's where many new brokers struggle. They think strong client relationships come from being available, positive, and persuasive. Those things help, but they don't control a deal. A clear system does. In business lending, clients are often stressed, time-sensitive, and financially exposed. If a broker doesn't define the path early, the client will fill in the blanks with assumptions.

Learning how to manage client expectations is one of the main skills that separates a calm, referral-driven brokerage from one that lives in constant cleanup mode.

Table of Contents

- Why Client Expectations Make or Break Your Broker Business

- The Foundation Your Onboarding and Discovery Process

- Setting Clear Expectations with a Funding Blueprint

- Mastering Proactive Communication and Updates

- Handling Delays Scope Creep and Difficult Conversations

- Turn Great Management into Your Referral Engine

Why Client Expectations Make or Break Your Broker Business

A frustrated borrower rarely says, “The process lacked expectation management.” They say, “You told me this would move faster,” or “Nobody explained that underwriting could change the terms,” or “Why am I finding this out now?”

That's the core job. A broker isn't only matching business owners with funding sources. A broker is also translating uncertainty into a process the client can understand and handle. The amateurs promise speed. The professionals explain sequence, conditions, and likely friction before it shows up.

A brokerage can survive a difficult file. It usually can't thrive on repeated disappointment. If clients keep feeling blindsided, they won't refer anyone, and they'll often leave with the impression that the broker lacked control. That's true even when the lender caused the delay.

Practical rule: Clients can tolerate uncertainty better than surprise.

This matters even more for brokers building a home-based, scalable business. A broker who wants flexible hours and repeat referrals can't spend every day reacting to angry texts and chasing avoidable misunderstandings. Strong expectation management lowers chaos. It also protects reputation, which has a direct effect on long-term earning potential in a referral business. For readers thinking about the broader upside of the profession, this breakdown of business loan broker salary paths shows why process matters as much as sales skill.

What poor expectation setting usually looks like

| Weak approach | Professional approach |

|---|---|

| “This should be quick.” | “This can move quickly if documents are complete and lender follow-up stays on pace.” |

| “You're approved.” | “You've cleared an early stage, but final terms still depend on review and conditions.” |

| “Send what you have.” | “Here's the exact document list, format needed, and the deadline to keep this moving.” |

Many new brokers think this level of detail will scare clients off. It usually does the opposite. It signals competence. Business owners don't expect perfection. They expect control.

The Foundation Your Onboarding and Discovery Process

A sloppy onboarding process creates almost every downstream problem a broker later blames on underwriting, lenders, or difficult clients.

The first real expectation-setting moment isn't the proposal or the approval call. It's the discovery conversation. That's where a broker learns what the client needs, how they make decisions, how urgently they need capital, and whether their version of “fast” or “affordable” is realistic.

Why onboarding is where trust is built

Clients don't only want funding. They want to feel understood. That's one reason expectation management has become more important. 73% of customers expect better personalization as technology advances, while 65% expect companies to adapt to their changing needs and preferences, according to Salesforce's overview of customer expectations. For a broker, that means the process must match the client's communication style, urgency, and level of financial sophistication.

A business owner who has never worked with a broker needs more explanation. A repeat borrower may want shorter updates and faster movement. One client wants text messages. Another wants email records they can forward to a partner or CFO. If a broker ignores those differences, even a technically solid process can feel impersonal and frustrating.

Some onboarding lessons transfer well from adjacent industries. A useful example is this Formbricks guide to user onboarding, which reinforces a practical point. People need clarity early, not after confusion starts.

The client judges the process long before the result arrives.

A discovery checklist for loan brokers

A strong discovery session should lock down goals, deliverables, timelines, budgets, and decision points, then turn that discussion into a written scope. Practitioners also recommend giving timelines as ranges because clients tend to anchor on the most optimistic date, which can create dissatisfaction later, as explained in ManyRequests' discussion of managing client expectations.

For a business loan broker, that discovery checklist should include:

- Funding purpose: What is the money for right now? Working capital, inventory, payroll support, expansion, equipment, tax pressure, or consolidation all change the urgency and lender fit.

- Timing reality: When does the client say they need funds, and what happens if that date slips?

- Amount versus affordability: What does the client want, and what monthly obligation can the business realistically support?

- Decision makers: Is the owner the only signer, or will a spouse, partner, bookkeeper, or manager slow approvals?

- Document readiness: Are bank statements, revenue reports, debt details, and entity documents ready now?

- Credit awareness: Does the client know their own weaknesses, or are they assuming a stronger file than they have?

- Communication preference: Does the client want one summary each week, or milestone updates only?

- Risk tolerance: Will the client consider a stepping-stone offer if the perfect structure isn't available today?

A broker also needs to understand the financial frame behind the request. If debt obligations are already tight, the conversation has to shift from “How much can be obtained?” to “What structure helps the business?” A practical way to sharpen that discussion is to understand the debt service coverage ratio calculation before presenting expectations around affordability.

The discovery call should end with a clear summary, not a vague promise to “see what can be done.” That one habit prevents a surprising number of future problems.

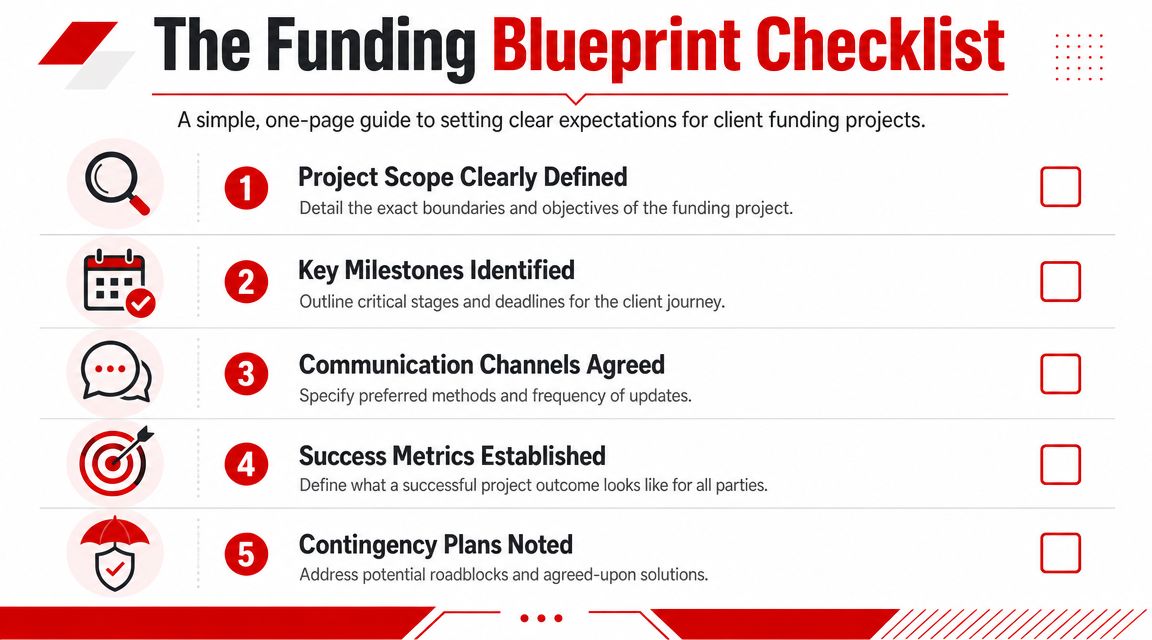

Setting Clear Expectations with a Funding Blueprint

Verbal alignment fades fast. Clients remember the shortest, happiest version of what they heard. That's why every broker should send a simple written Funding Blueprint after discovery.

This doesn't need to be long. One page is enough. The point isn't legal complexity. The point is to document the path in plain language so the client knows what happens next, what can change, and what the broker needs from them.

What goes into the Funding Blueprint

A useful Funding Blueprint has four core parts.

| Component | What to include |

|---|---|

| Timeline range | A realistic range for review, submission, lender response, and closing steps |

| Fee clarity | How compensation works, when it applies, and what the client should expect in writing |

| Communication plan | Update cadence, primary contact method, and who needs to respond on the client side |

| Approval scenarios | Best-case, likely-case, and difficult-case outcomes |

For brokers, this document becomes the anchor. If emotion rises later, the conversation can return to what was documented and agreed.

A short debt summary can also improve clarity here, especially if multiple obligations affect the deal structure. When a broker understands what a debt schedule is, it becomes easier to explain why the requested amount, term, or payment target may need adjustment.

Simple language that keeps clients grounded

The wording matters. Overly polished language creates false certainty. Plain language creates trust.

Use language like this:

“Based on the information available today, the expected funding path is a range, not a guaranteed date. Timing depends on complete documents, lender review speed, and any follow-up conditions.”

For fees:

- State the trigger clearly: “Compensation is tied to a completed funding transaction, not to initial review or prequalification.”

- Explain where confusion happens: “Early interest from a lender isn't the same as final approval.”

- Put disclosures in writing: “Any fee structure should be confirmed before the client proceeds.”

For outcome scenarios, brokers should avoid broad reassurance and use a more disciplined frame:

- Best-case: The file is clean, documents are complete, and the lender returns terms quickly.

- Base-case: The lender requests additional items, clarifications, or revised statements before issuing final terms.

- Worst-case: The client receives a lower amount, a different structure, delayed movement, or no workable approval.

That last point matters. Clients in financial stress often hear only the optimistic path. A broker's job is to keep them informed without crushing momentum. The Funding Blueprint does that. It gives hope a boundary.

Mastering Proactive Communication and Updates

Most client frustration grows in silence.

A borrower submits documents, hears nothing for a few days, and starts guessing. They assume the file stalled, the broker disappeared, or the lender found a problem. Even if none of that is true, the broker is now behind because the client's confidence has already started to drop.

Set a cadence before the client asks for one

Clients increasingly expect the process to feel personal and responsive. 71% of consumers expect companies to provide personalized interactions, and 76% feel frustrated when this doesn't happen, according to Wavetec's customer experience statistics summary. In brokerage terms, that doesn't mean constant access. It means the client should know when they'll hear from the broker and what kind of update to expect.

A simple communication rhythm works well:

- Welcome update: Sent right after onboarding. Confirms receipt, next steps, and document needs.

- Submission update: Sent when the file goes out for review.

- Standing weekly update: Sent on the same day each week, even if the update is brief.

- Milestone update: Sent when terms arrive, conditions change, or a decision is needed.

- Closeout update: Sent when the file funds, pauses, or ends.

This kind of cadence can be handled manually or with light automation. Brokers who want help organizing follow-ups can review GPT for Work's comprehensive AI tool guide for workflow ideas. The useful principle isn't the software. It's consistency.

Templates that reduce anxiety and save time

A broker shouldn't rewrite every message from scratch. The best communication feels personal, but it follows a standard.

Submission confirmed

Your file has been submitted for review. At this stage, the main variable is whether the lender asks for follow-up items. If that happens, a fast response keeps momentum.

Lender follow-up needed

The lender has requested additional documents before moving forward. This is part of normal review. Once the items below are received, the file can continue through evaluation.

No update update

There isn't a material change to report today, but the file is still active. No action is needed from your side right now. The next scheduled update will be sent on Friday unless a lender response comes sooner.

Keep this standard: no news still gets an update.

A broker serving clients remotely also benefits from setting one preferred update lane. Email for summary and documentation. Phone for decisions. Text for reminders only. That prevents scattered conversations and missing details.

When clients need short-term capital solutions and expect speed, clarity matters even more. A broker discussing fast-moving products like accounts receivable lenders should be especially careful not to let “faster than traditional lending” turn into “funding is imminent.” Those are not the same thing.

Handling Delays Scope Creep and Difficult Conversations

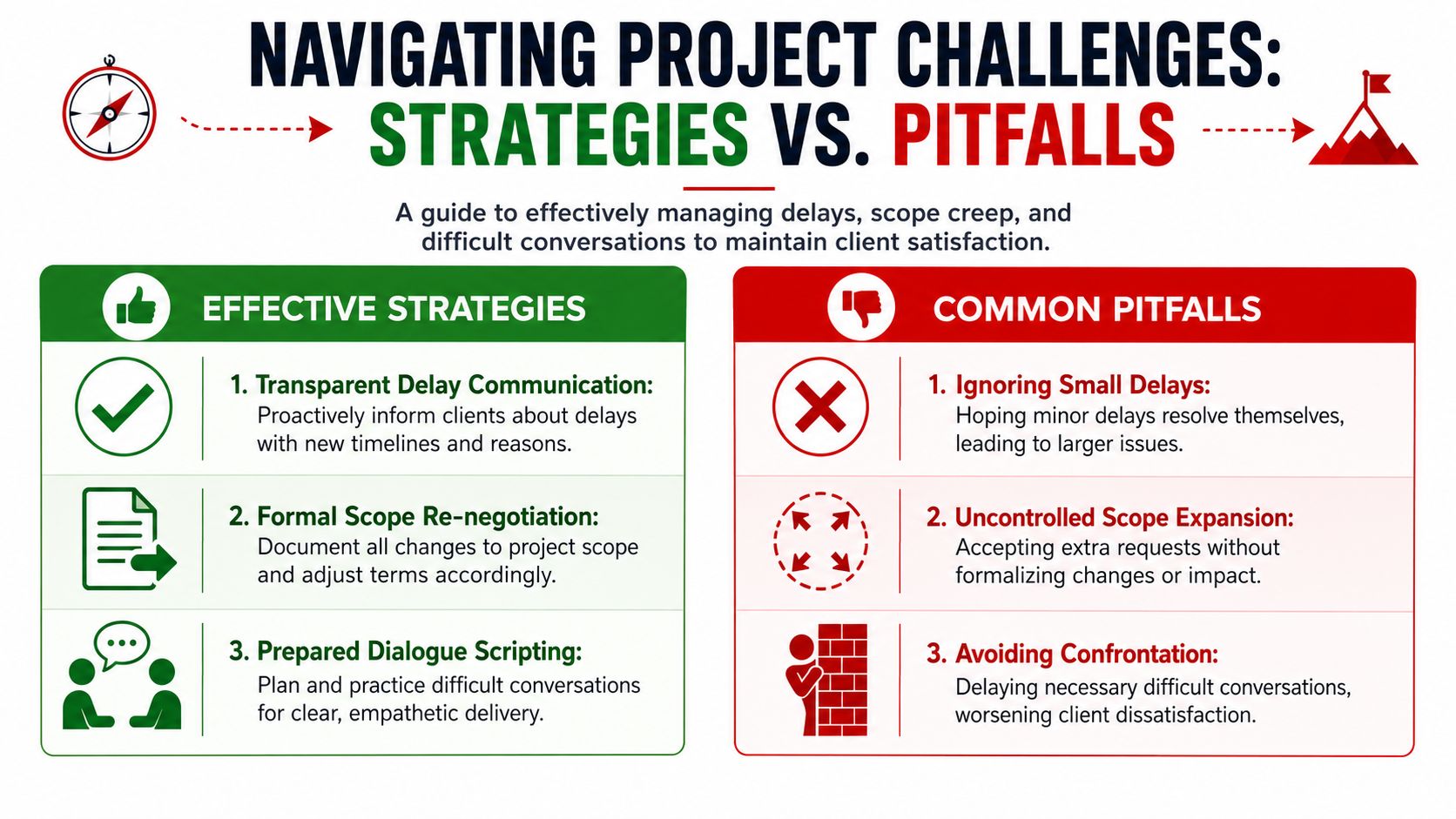

Every broker eventually faces a file that drifts off the original path. The problem isn't that this happens. The problem is that many brokers respond too late, too softly, or too vaguely.

Clients can handle bad news better than mixed messages. What damages trust is hesitation. If the lender slows down, say so. If the client caused the delay, document it clearly. If the approval won't match the original hope, reset the frame before the client invents a better outcome in their head.

When the delay is outside the broker's control

A broker loses credibility when acting as if lender delays don't exist. They do. Files get additional review. Conditions change. Underwriters request fresh statements. The right move is immediate transparency.

Use language like this:

- Acknowledge the shift: “The lender's review is taking longer than originally expected.”

- Name the cause if known: “They requested another round of verification before issuing terms.”

- Reset the next checkpoint: “The next update will be sent by Wednesday, even if the lender hasn't finalized a response.”

That keeps the broker in control of communication, even when not in control of the timeline.

When the client is the bottleneck

Many brokers become too polite and hurt their own deals. A common blind spot in expectation management is that delays often come from the client's speed, not the broker's delivery. Slow feedback, approvals, and missing inputs can stall a file, and a stronger approach is to set decision deadlines and default approvals in writing, as noted in Moxo's article on managing client expectations.

A broker can say:

We can keep this file active, but the requested items need to be in by tomorrow at noon. If they arrive later, the review timeline may shift and some terms may need to be refreshed.

That isn't harsh. It's operationally honest.

A useful policy set looks like this:

- Document deadlines: Every request should include a due date and the consequence of delay.

- Use one request list: Don't scatter needed items across email threads and text messages.

- Define inactivity: If the client goes silent, note when the file will be paused.

- Set decision windows: If an offer is time-sensitive, say when the client must accept, decline, or ask questions.

When optimism hits financial reality

Some of the hardest conversations happen when the client wants a strong approval, but the file only supports a weaker option or no workable offer at all.

Don't soften the truth so much that the client misunderstands it. A better script is simple: “Based on the current file, the likely outcomes are narrower than originally hoped. There may still be a path forward, but it may involve a lower amount, a different structure, or more time before the business is ready.”

That preserves honesty and leaves room for guidance. It also prevents one of the worst broker mistakes, which is keeping a client emotionally attached to an outcome that the numbers don't support.

Turn Great Management into Your Referral Engine

A client gets approved for less than expected, two days later than hoped, and still thanks you for the work. Then they send their CPA your name.

That happens more often than new brokers expect. Referrals usually come from a process that felt clear and steady during a stressful file, not from a perfect outcome. In business lending, your client is often carrying payroll pressure, vendor pressure, or cash flow pressure at the same time you are trying to place the deal. They remember how you handled that pressure.

What sticks with clients is simple. Did you explain what was likely to happen. Did you tell them the truth early. Did you keep them from sitting in silence while they worried about approval, timing, and terms.

Hard conversations matter here. Borrowers do not expect every file to go exactly their way. They do expect you to be straight with them about uncertainty. That point is echoed in Advocate Magazine's article on managing client expectations. For a business loan broker, that means setting the expectation that funding can shift if documents arrive late, underwriters ask new questions, or the numbers support a smaller approval than the client wants.

Clients refer the broker who made the process feel controlled.

I tell new brokers to judge their client management by four standards:

- Qualify the file accurately. A client who should wait 90 days is not a good same-week submission.

- Put the process in writing. Memory changes. Written expectations hold.

- Update before the client asks. Silence creates fear, and fear creates distrust.

- Reset the file fast when conditions change. Bad news delivered early is easier to respect than bad news delivered late.

These habits do more than protect one deal. They make your brokerage easier to run, easier to delegate, and easier to grow through referral partners like CPAs, consultants, and commercial real estate professionals. Those partners care about the borrower experience because your process reflects on them too. If their client says, "My broker kept me informed, explained every turn, and never disappeared," you stay on the short list for the next introduction.

Business Lending Blueprint teaches brokers how to qualify borrowers, structure deal flow, and manage communication through the funding process. That operating discipline is what turns client management into repeat business and referrals.

A broker who wants more funded deals and more referrals does not need better hype. You need a better operating standard. To see how a structured loan brokerage model works, watch the free training from Business Lending Blueprint or schedule a strategy session to see how this business can be built from home with a process-driven, referral-first approach.