A new broker often gets the same call at the worst possible time. A client who sounded confident at closing now sounds cornered. Revenue tightened, a payment was missed, and the borrower wants to know whether this is just a late month or the start of something much worse.

That moment decides what kind of broker the market sees. A transactional broker disappears once funding closes. A real advisor knows that a default loan SBA situation can affect the borrower's assets, future bankability, and the broker's own long-term pipeline. One mishandled file can turn a former client into a permanent dead end instead of a future referral source.

Table of Contents

- The Call Every Broker Dreads And Why It's Your Biggest Opportunity

- Understanding the Anatomy of an SBA Loan Default

- The Collection Cascade What Happens After Default

- Your Client Rescue Playbook Proactive Solutions for Brokers

- How Default Impacts Different SBA Loan Programs

- The Broker Blackout A Hidden Threat to Your Business

- Become the Go-To Advisor in Business Funding

The Call Every Broker Dreads And Why It's Your Biggest Opportunity

The phone rings on a Monday morning. Your client says they missed payments, the lender is sending letters, and they want to know if the business is about to lose everything. In that moment, the broker who guesses loses credibility fast. The broker who gets control of the facts can still protect the client, preserve options, and keep the relationship from turning into a future blacklist issue.

Your first job is to lower the temperature.

Do not start with reassurance. Start with a timeline, the loan documents, and the borrower's current cash position. A distressed SBA file can still be worked, but only if you know whether this is a short-term payment problem, a broken business model, or a case that is already sliding toward collections. If you want clients to understand trouble earlier, teach them how to read basic cash flow pressure using a plain-English guide to debt service coverage ratio calculation.

What a broker should say first

A good first conversation is disciplined. Ask for the facts you need before you offer strategy.

- Payment history: Confirm how far behind the borrower is and whether any partial payments were made.

- Lender correspondence: Review every late notice, default notice, and rights reservation letter.

- Current liquidity: Determine whether cash can cover payroll, taxes, rent, and debt service.

- Collateral and guarantees: Identify what business assets and personal assets may be exposed.

- Cause of distress: Separate a temporary revenue dip from margin erosion, tax problems, or owner withdrawals.

The rule is simple. Verify first. Advise second.

That approach protects the client, but it also protects you. New brokers often focus only on whether this loan can be saved. Experienced brokers know a default can also damage the client's future fundability for years. If the borrower becomes permanently hard to place, you do not just lose one transaction. You lose renewals, refinances, equipment requests, working capital opportunities, and referral flow from that account. That is the Broker Blackout, and it can turn one mishandled call into a long-term revenue loss.

Why this is an opportunity

Distress work separates order takers from real advisors. Any broker can submit an application when the file is clean. Far fewer can step into a problem loan, organize the facts, set expectations, and keep the borrower from making panicked mistakes.

Clients remember who was useful when the deal went bad.

Handled correctly, this call gives you a different position in the relationship. You are no longer the person who sold a loan. You are the person who can assess risk, explain consequences in plain language, and help the client choose the least damaging path. That is how brokers build trust that survives a bad quarter, and that is how they protect both reputation and future deal flow.

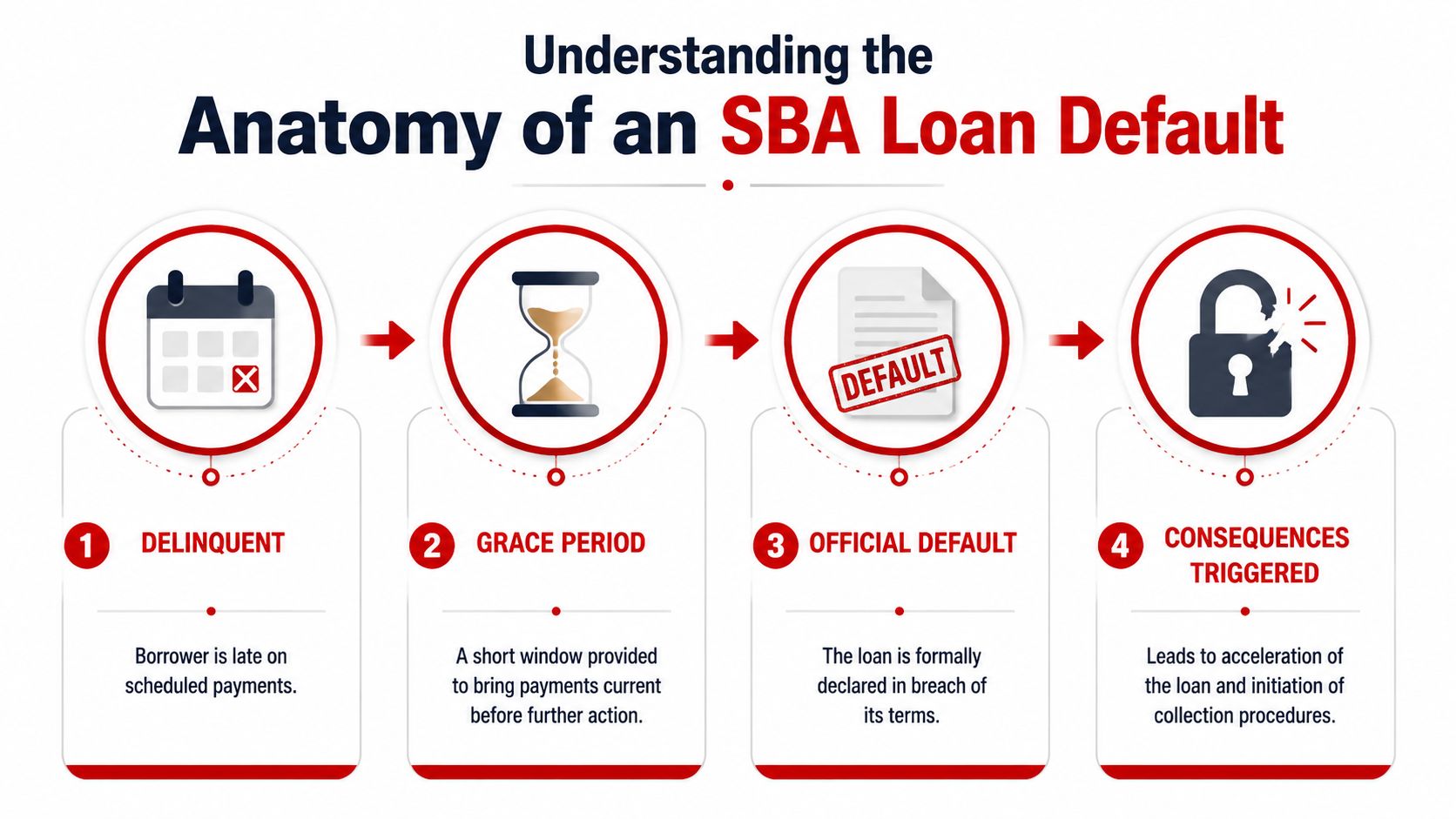

Understanding the Anatomy of an SBA Loan Default

A borrower can spend weeks telling themselves the loan is “just behind” while the file is already moving toward a much more serious stage. That gap between what the client thinks is happening and what the lender is documenting is where brokers lose control of the outcome.

Your job is to define the line clearly.

Delinquent is not the same as defaulted

Missed payments start the problem. Default changes the lender's legal posture.

A borrower is delinquent once scheduled payments are missed. Servicing notices follow. Calls start. Cure requests get more direct. If the borrower does not bring the account current over an extended period, the lender can move the loan into formal default and issue a demand letter for the full outstanding balance. At that point, the discussion is no longer about a late installment. It is about a breached note, possible acceleration, and recovery strategy.

That distinction matters because borrowers often act as if one partial payment fixes everything. In many cases, it does not. Once the file has advanced, the lender may still require a full workout package, updated financials, and a documented plan before considering any relief.

A broker should also explain that default is rarely caused by one missed payment alone. It usually starts earlier, when the business stops producing enough cash to service debt consistently. That is why I want brokers to be able to explain debt service coverage ratio calculation in plain English before a file gets distressed. If the owner cannot see the warning signs in the numbers, they usually wait until options have narrowed.

What the borrower experiences next

From the client's side, the process feels abrupt. From the lender's side, it looks documented, sequential, and increasingly formal.

That difference matters.

The borrower sees pressure. The lender sees a file history that will justify the next action. Every missed promise, incomplete document set, and ignored notice makes the borrower look harder to work with. Brokers need to correct that fast, because lender confidence affects whether the client gets any room to negotiate.

A strong explanation to the client should cover three points:

- The lender is building a record. Notes from calls, payment failures, financial requests, and cure deadlines all become part of the file.

- Incomplete cooperation hurts credibility. Partial bank statements or outdated financials make the borrower appear evasive or disorganized.

- Delay reduces flexibility. The longer the borrower waits, the fewer practical solutions remain.

This is also the stage where hidden facts usually surface. Sales fell off. Tax balances stacked up. The owner drained cash to cover another business. Receivables slowed and never recovered. You need those facts early, because the right advice depends on the actual cause of failure, not the version the borrower first gives you on the phone.

There is another layer new brokers miss. Default does not only damage the borrower. It can damage the account itself as a future funding relationship. A client who mishandles an SBA default can become much harder to place with any lender later, which means the broker may lose years of future commissions tied to that borrower. That is the Broker Blackout. One bad outcome can shut down renewals, expansions, equipment requests, and referral business from that client base.

The discipline here is simple. Explain the timeline. Get full disclosure. Keep the borrower engaged with the lender. If the client also has exposure in other regulated collection matters, even outside SBA debt, the broker should understand adjacent risk areas like student loan collections compliance. Borrowers under collection pressure often make poor decisions across multiple obligations, and that pattern can make an already weak file worse.

A broker who can explain default in concrete terms does more than calm the client down. The broker protects the borrower from avoidable mistakes and protects their own book of business from turning one troubled loan into a permanent dead account.

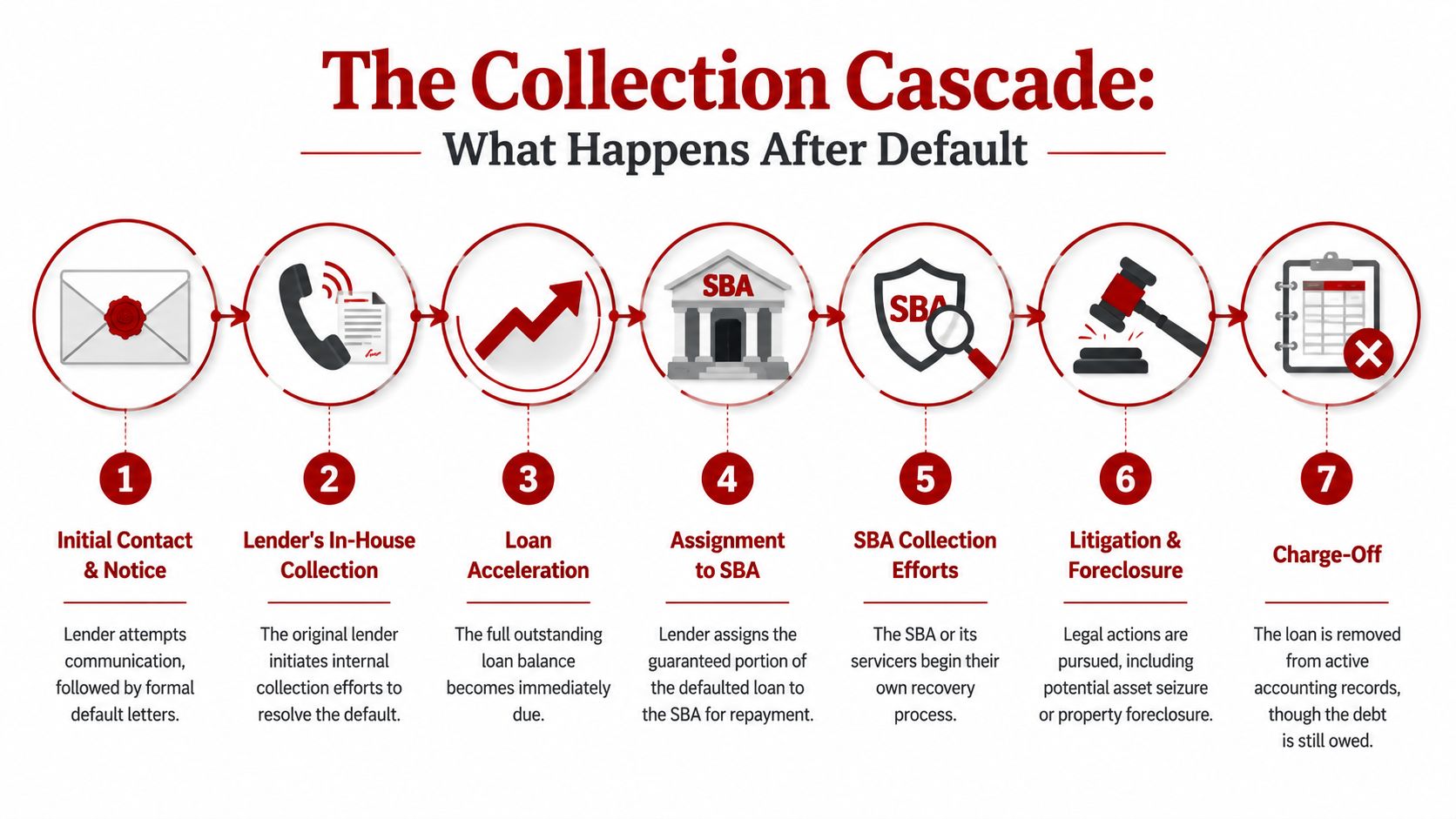

The Collection Cascade What Happens After Default

Once the file enters formal default, the borrower is no longer dealing with a simple servicing issue. The file moves into a collection path with its own rules, deadlines, and pressure points. A broker needs to know that path well enough to explain it in one conversation.

The sequence a broker needs to explain clearly

The lender's first obligation is to pursue recovery. That usually means demanding liquidation of available collateral and applying proceeds against the debt. If there's still a deficiency, the SBA can take over collection responsibility, and the borrower may try an Offer in Compromise if the file qualifies.

If the compromise route fails, the consequences get much harder. As explained in Nav's discussion of SBA default and forgiveness mechanics, the SBA can escalate to the Treasury Offset Program (TOP) or Administrative Wage Garnishment (AWG), and those tools have no statute of limitations and remain active until the debt, interest, and fees are fully paid.

That's the part many borrowers underestimate. They think the file “charges off” and disappears. It doesn't. Accounting treatment and collection reality are not the same thing.

Where brokers still have leverage

The broker can't erase the default, but the broker can still improve the borrower's odds by forcing order into a chaotic situation.

Use this playbook:

- Get the full debt stack on paper: A broker should map every obligation, not just the SBA note. That's easier when the borrower has a real debt schedule framework instead of scattered statements and memory.

- Separate secured from unsecured pressure: The borrower needs to know what collateral may be liquidated first and what remains as a personal exposure issue.

- Push complete disclosure early: Lenders and agencies respond better to organized borrowers than to borrowers who drip out information.

- Stop side promises: A borrower should never casually promise cure dates or settlement amounts without a realistic basis.

Field insight: Distressed files rarely collapse because one payment was missed. They collapse because communication breaks down, documents arrive late, and nobody owns the process.

Brokers who work around collections also benefit from understanding broader contact and documentation discipline. A practical resource on student loan collections compliance is useful here, not because the debt type is identical, but because it sharpens how regulated collection workflows, communication records, and escalation controls should be handled.

The practical urgency

There is a narrow window where the borrower still looks cooperative and salvageable. Once the file is deep into liquidation and federal collection channels, bargaining power diminishes sharply. The broker's role is to keep the borrower engaged, realistic, and documented.

That alone can protect relationships that would otherwise implode under stress.

Your Client Rescue Playbook Proactive Solutions for Brokers

A good broker doesn't wait for the official default stamp before taking action. The rescue playbook starts earlier, when there's still room to influence lender behavior and borrower choices. It also has to fit the SBA program involved, because not every file carries the same structure, collateral path, or intermediary relationship.

What works before the file hardens

Some interventions help. Some waste time.

What usually works:

- Early lender contact: Borrowers who acknowledge trouble and provide current financials are easier to work with than borrowers who go silent.

- Short-term workout requests: If the business has a temporary disruption rather than permanent collapse, the broker can help the borrower package a credible request for modified payments or a temporary deferment.

- Refinancing analysis: Sometimes another financing product can solve a cash timing issue. Sometimes it only adds more debt to a bad structure. The broker has to tell the truth.

What usually doesn't work:

- Using expensive short-term money to cover a structurally unpayable SBA note

- Sending partial documents and vague explanations

- Treating every distress case as a sales opportunity instead of a triage case

A broker who wants to preserve trust should also set expectations carefully from the start. Distressed borrowers often hear what they want to hear, which is why disciplined communication matters. This is the same mindset behind managing client expectations in funding relationships.

How to evaluate options across SBA programs

Different SBA products create different rescue dynamics. Newer brokers often get sloppy in these situations.

| Program | What tends to matter most in distress | Broker focus |

|---|---|---|

| 7(a) | Broad use of proceeds, common personal guarantee exposure, mixed collateral | Cash flow reality, guarantor capacity, workout viability |

| 504 | Asset-backed structure with fixed asset exposure | Collateral value, business continuity, liquidation implications |

| Microloan | Intermediary lender relationship can shape the tone and pace | Communication quality, local process, realistic hardship package |

The broker doesn't need to act like an attorney. The broker does need to know where the pressure will likely land first.

Offer in Compromise preparation checklist

For borrowers already in liquidation status, an Offer in Compromise may become the main path worth exploring. Based on the verified mechanics, it's only viable when the loan is in liquidation, the borrower isn't in active bankruptcy, and the full amount can't be recovered through legal collection. If the compromise fails, collection can continue through federal tools already covered above.

A broker adds value by helping the borrower gather a coherent package, such as:

- Personal financial statement: Current income, expenses, assets, liabilities.

- Business financials: Recent statements showing the company's inability to cure.

- Narrative of hardship: A fact-based explanation of what changed and why recovery is limited.

- Collateral summary: What exists, what's already been liquidated, and what value remains.

- Guarantor information: Any other liable parties and their current financial condition.

- Settlement source explanation: Where the proposed compromise funds would come from.

A borrower facing broader pressure beyond the SBA note may also need legal guidance on solutions for small business debt. That kind of resource can help the broker understand when the issue has moved past workout strategy and into broader financial distress planning.

The broker's job in a rescue isn't to promise a win. It's to organize facts fast enough that the borrower still has choices.

That's what separates a broker who closes deals from a broker who builds a stable, referral-driven business over time.

How Default Impacts Different SBA Loan Programs

Not all SBA defaults behave the same way in practice. A broker who treats every file like a standard 7(a) problem will miss important structural differences, especially around collateral, lender relationships, and how pressure reaches the guarantor.

Why program structure changes the broker's advice

With 7(a), the broker often deals with the broadest range of use cases. That means the collateral mix can be uneven, the business may have borrowed for working capital rather than a hard asset, and the personal guarantee can become the central issue once the business can't carry the note.

With 504, the default discussion often centers more tightly on the financed asset and the two-part structure involving the bank and the development component. The broker needs to think like a liquidation strategist, not just a cash-flow coach.

With Microloans, the intermediary lender relationship matters more. The borrower may be dealing with a smaller institution that has its own process and communication style. That can help or hurt depending on how organized the borrower is.

Risk also varies by industry. According to Monitor Daily's analysis of industry default variance, restaurants and food service show the highest default rates, ranging from 14.7% to 17.8%, while accounting firms sit at 2.3%. For a broker, that should shape origination discipline long before distress shows up.

SBA Loan Default Comparison 7(a) vs 504 vs Microloan

| Feature | SBA 7(a) Loan | SBA 504 Loan | SBA Microloan |

|---|---|---|---|

| Typical default concern | Cash flow failure and personal guarantee exposure | Fixed asset liquidation and repayment shortfall | Borrower communication and intermediary collection process |

| Collateral emphasis | Can vary widely by deal | Usually tied closely to financed assets | Often smaller-scale collateral or limited recoveries |

| Guarantor pressure | Often significant | Can still be serious, especially after collateral liquidation | Depends on structure, but personal liability can still matter |

| Broker's best role | Triage cash flow, gather full file, prevent silence | Clarify asset position and realistic outcomes | Keep borrower responsive and documentation clean |

| Best time to intervene | Before formal default if possible | As soon as payment stress threatens asset position | Immediately at signs of hardship |

Brokers who understand program differences protect more than one client. They protect their own future income by avoiding preventable blowups.

That's the business case. A broker building a remote, flexible brokerage can't rely only on origination skill. Long-term growth comes from protecting relationships, preserving referral trust, and steering high-risk files before they become reputation damage.

The Broker Blackout A Hidden Threat to Your Business

Most default discussions stop at borrower pain. They focus on collection letters, seized assets, and settlement attempts. The bigger brokerage issue is what happens after that borrower becomes toxic to future underwriting.

Why one default can erase years of future deal flow

The hidden cost is the Broker Blackout. Once a client falls deep into federal collection channels, the borrower may no longer be a realistic candidate for future financing for a very long time. That means the broker loses more than one commission. The broker loses renewals, future placements, and the referrals that often come from helping a business grow after the first deal.

The urgency is growing. The Tax Guard analysis of early SBA default changes notes that the SBA 7(a) default rate reached 3.7% in 2024, the highest since 2012, with $1.6 billion in defaulted loans repurchased by the SBA, and that once a borrower hits TOP, they're effectively locked out of the lending market for 6+ years.

A broker who ignores that reality is thinking too short-term.

What disciplined brokers do differently

Strong brokers treat distress management as pipeline protection.

They screen for risk factors earlier. They educate borrowers better at closing. They also understand the compliance side of the profession, including practical issues around working without a license as a business loan broker, so they can build a legitimate business that survives hard markets and difficult files.

The Broker Blackout idea changes how a broker should view every SBA file:

- One defaulted client may become permanently unfundable

- One mishandled workout can damage referral trust

- One well-managed rescue can create loyalty that lasts for years

The broker who stays present when deals go bad usually becomes the first call when better deals appear.

That's why this topic matters so much to anyone building a recession-resistant brokerage from home. The market doesn't just reward the broker who can place paper. It remembers the broker who can guide a client through pressure without disappearing.

Become the Go-To Advisor in Business Funding

A broker's reputation is built in hard conversations. Anybody can celebrate an approval. Fewer people can explain default timing, collection mechanics, compromise strategy, and future bankability without creating false hope.

That expertise compounds. It helps a broker serve business owners better, earn trust across referral partners, and build a remote business with real staying power. People who come from sales, banking, consulting, tax, insurance, or advisory work often do especially well here because they already understand that long-term income comes from relationships, not one-off transactions.

The same principle shows up in adjacent industries. A useful example is this look at how mortgage loan officers find clients, where trust, consistency, and referral habits matter more than flashy outreach. Business lending works the same way. The broker who solves real problems earns repeat attention.

A serious broker doesn't need hype. The opportunity is already strong. Small business owners need funding guidance, banks still decline many applicants, and skilled brokers can build scalable referral-based businesses from home with low overhead and flexible schedules. The edge comes from knowing what to do when the file stops being easy.

Business Lending Blueprint shows aspiring brokers how to build a practical, home-based business loan brokerage with real training, lender access, and systems for creating referral-driven deal flow. To learn how to help business owners secure funding, grow a flexible remote business, and become the advisor clients trust in good markets and bad, watch the free training or schedule a strategy session with Business Lending Blueprint.