A new broker usually gets this question earlier than expected.

A business owner gets on the phone, describes a funding need in two rushed sentences, then asks, “What's better for me, a term loan or a line of credit?” If the broker answers with a generic “it depends,” the call drifts. If the broker answers with clarity, the conversation changes. The client relaxes, the file gets cleaner, and the broker starts looking like a real advisor instead of someone shopping offers.

That moment matters because term loan vs line of credit isn't just product knowledge. It's positioning. Brokers who can diagnose the need behind the request tend to build trust faster, package stronger submissions, and get more repeat business from the same client base. A contractor, retailer, agency owner, or restaurant operator rarely wants a lecture on lending structures. They want someone who can translate the situation into the right funding path.

The strongest brokers also know that product fit starts before any application goes out. Good qualification discipline saves time, protects lender relationships, and prevents wasted submissions. For readers sharpening that front-end skill, Stamina's sales lead qualification guide is a useful companion because it reinforces the habit of asking better questions before offering solutions.

Table of Contents

- Your First Big Client Question

- Funding Foundations Term Loans vs Lines of Credit

- The Ultimate Comparison Chart for Brokers

- When to Recommend Each Funding Type

- The Broker Playbook Presenting Options and Packaging Deals

- From Broker Knowledge to a Thriving Business

- Start Your Loan Broker Blueprint Today

Your First Big Client Question

A new broker often assumes the hard part is finding leads. It usually isn't. The harder part is sounding credible once a qualified owner starts asking real financing questions.

One of the first big tests is simple on the surface. A client asks whether they should take a term loan or wait for a line of credit. The wrong answer is to treat both products like interchangeable pools of money. They aren't. Each one solves a different kind of business problem.

What the client is really asking

Most owners aren't asking for a textbook definition. They're asking four practical questions at once:

- What fits the need: Is this money for one purchase or for uneven cash flow?

- What can get approved: Does the business profile support the product they want?

- What will feel manageable: Will the payment structure create stress or stability?

- What should happen first: Is it smarter to pursue the ideal product, or the realistic one?

A broker's value shows up in how quickly those questions get sorted.

A broker doesn't earn trust by naming products. A broker earns trust by matching the product structure to the client's business reality.

Why this distinction builds a brokerage

This isn't minor product knowledge. It's a core advisory skill. A broker who can explain why a defined project usually points one way, while uneven working-capital pressure points another way, becomes easier to refer.

That reputation compounds in a practical way. Accountants, consultants, insurance professionals, and business service providers don't want to refer clients to someone who confuses speed with fit. They want a funding specialist who can listen, diagnose, and explain options in plain English.

For anyone building a remote, home-based brokerage, this is one of the earliest strategic areas. Product clarity leads to cleaner conversations. Cleaner conversations lead to stronger submissions. Stronger submissions tend to produce better long-term referral relationships.

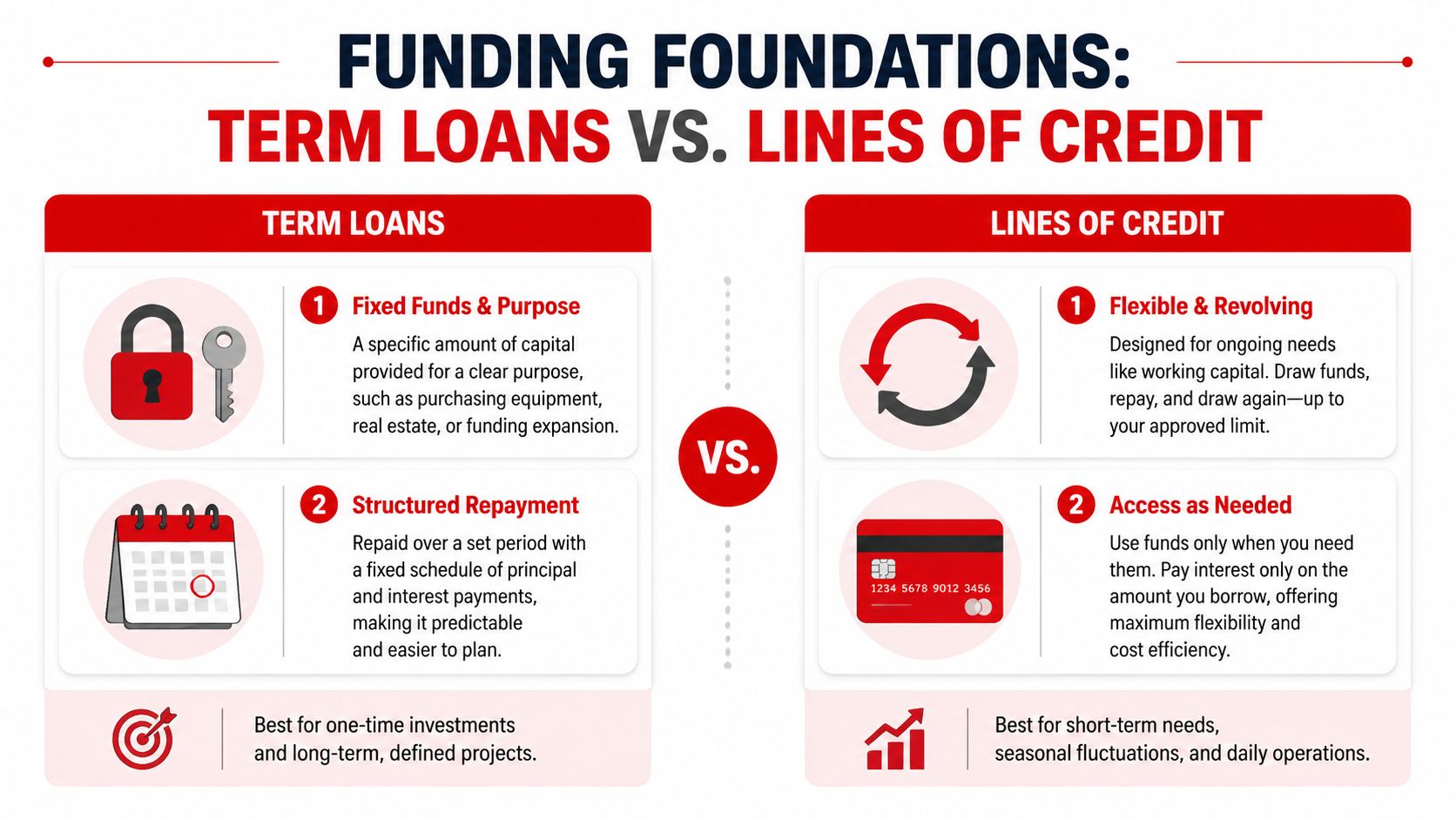

Funding Foundations Term Loans vs Lines of Credit

A new broker usually hears the same request on an early call. "My client wants a line of credit." The mistake is treating that as the diagnosis. It is only the opening statement.

The job here is to identify whether the client needs a fixed amount for a defined purpose or access to working capital that rises and falls with operations. Get that right, and the file gets cleaner, the lender match improves, and the client is easier to advise.

How to explain a term loan

A term loan gives the borrower a lump sum up front, then requires repayment on a set schedule over an agreed term. For broker conversations, that definition matters less than the use case.

Use this script with clients:

“A term loan fits a business that knows the amount it needs, what the funds will be used for, and how that payment will fit into the monthly budget.”

That framing keeps the conversation tied to structure instead of preference. It works well for equipment purchases, tenant improvements, expansion projects, partner buyouts, or any other use of proceeds with a clear price tag.

From a packaging standpoint, term loan files get stronger when the story is specific. The amount requested should match the project. The use of proceeds should be easy to document. The repayment case should show that the business can absorb the new obligation without strain. If you need to pressure-test that before submission, a debt service coverage ratio calculation guide helps you check whether the proposed payment fits the cash flow story you plan to present.

How to explain a line of credit

A line of credit gives the client access to a credit limit it can draw from, repay, and draw again. The value is not the one-time funding event. The value is access to liquidity when timing gets uneven.

A client-ready script sounds like this:

“A line of credit is usually the better fit when the business does not need all the money at once and wants flexibility for short-term gaps.”

That applies to inventory swings, delayed receivables, payroll timing issues, seasonal slow periods, or operating expenses that hit before cash collections catch up. Clients like the flexibility, but brokers need to be careful here. A line of credit can sound safer because the client only draws what it needs. Approval still depends on whether the business shows the operating history and cash movement that support revolving access.

The broker view that separates amateurs from advisors

New brokers often explain these products as if the only difference is lump sum versus revolving access. That is not enough to win trust or get more deals approved.

The primary difference is how each product matches the client's cash pattern.

A term loan fits a defined investment with a repayment schedule the business can plan around. A line of credit fits uneven operating pressure where the client needs room to borrow, repay, and borrow again without refinancing every time cash flow tightens.

That distinction should show up in the file you submit. For a term loan, present the request around purpose, budget, expected benefit, and payment capacity. For a line of credit, present the request around receivables timing, inventory cycles, recurring gaps, and why revolving access makes more sense than overfunding the business with a lump sum.

That is how brokers stop sounding like order takers and start sounding like advisors worth referring.

The Ultimate Comparison Chart for Brokers

Keep this section close during sales calls. It helps a broker sort the client's request into the right structure before rate talk, before lender shopping, and before the client talks themselves into the wrong product.

Term Loan vs. Line of Credit at a Glance

| Feature | Term Loan | Line of Credit |

|---|---|---|

| Funding structure | One-time lump sum | Revolving access up to a limit |

| Best use case | Planned purchase, expansion cost, or fixed project | Recurring cash gaps, uneven receivables, or short-term working capital pressure |

| Repayment style | Set installments over a defined term | Payments tied to the amount currently drawn |

| Balance behavior | Declines through scheduled amortization | Moves up and down as the client draws and repays |

| Interest application | Charged under the loan structure on the funded amount | Charged only on funds actually in use |

| Rate behavior | Often paired with fixed payment expectations | More often variable or subject to periodic adjustment |

| Borrower appeal | Predictable payment planning | Flexible access to cash |

| Common broker angle | Clear purpose, clear amount, clear payoff path | Ongoing access without reapplying for every shortfall |

| Typical approval challenge | Showing the purchase makes sense and the payment fits cash flow | Showing enough operating history, account activity, and revenue consistency for revolving access |

A strong broker uses this chart to control the call. If the client starts with, "I want a line of credit," do not accept that at face value. Ask what they are trying to fix, how often the problem shows up, and whether the amount is known today.

Where brokers lose deals

The first mistake is letting the client choose the product before the file is diagnosed.

Owners usually describe a preference, not a financing strategy. A line of credit sounds safer because it feels less committal. A term loan can feel expensive because the full amount funds at closing. Neither reaction tells you which structure gives the lender the cleaner story or the client the better outcome.

The second mistake is selling price before payment fit.

A borrower who asks for the cheapest option is often asking for the option that creates the least pressure on weekly or monthly cash flow. Good brokers translate that early. "Cheap" in the client's mind may mean fixed payments, lower draw usage, or no need to refinance every time inventory turns slowly.

Practical rule: Match the use of funds, repayment pattern, and approval profile before you discuss speed or pricing.

Underwriting differences brokers should explain with care

Term loans and lines of credit do not get underwritten the same way, even when the client qualifies for both.

With a term loan, the underwriter usually wants a clean explanation for the amount requested, a sensible use of proceeds, and evidence that the business can carry the installment payment. With a line of credit, the lender often pays closer attention to bank activity, receivables rhythm, revenue consistency, and whether the business has a recurring need for revolving access.

That distinction matters when you package the file. If you submit a line-of-credit request for a one-time equipment purchase, you create friction for no reason. If you submit a term-loan request for a client who repeatedly runs short between vendor payments and collections, you may get an approval, but you still solve the wrong problem.

Tell the client that revolving products usually face tighter scrutiny around operating stability. That is specific enough to set expectations without boxing yourself into lender-specific rules that may not apply.

How to use the comparison in a live call

Keep the conversation tight. A good broker can sort this in a few questions.

- What is the money for right now? A defined purchase usually points toward term financing.

- Will this need come back in 30, 60, or 90 days? Repeating pressure usually points toward a line of credit.

- Is the client solving for payment certainty or access to cash? That answer changes how you present the options.

- Which structure is more realistic for approval today? The best theoretical product is useless if the file does not support it.

I coach new brokers to say it this way: "If this is a one-time spend, I want to show lenders a clean term request. If this is a recurring working-capital issue, I want to present it as a revolving need, because that matches how the business uses cash."

For payment modeling, use a tool that shows the monthly impact in plain numbers. A business building loan calculator for broker payment scenarios helps turn product structure into a client conversation that feels concrete instead of theoretical.

When to Recommend Each Funding Type

Good brokers earn trust here. The client is not asking for a glossary. They are asking which structure gives them the best shot at approval, fits the cash need, and does not create a payment problem six months from now.

The recommendation should follow the business pattern. Use a term loan when the need is defined, the spend is easy to document, and the repayment can be tied to a purchase or project life. Use a line of credit when the need rises and falls, the exact draw timing is uncertain, and the business benefits from reusing the same facility instead of taking one lump sum.

That sounds simple. In practice, new brokers lose deals in situations like this. They listen to the product request instead of diagnosing the problem.

Scenario one with a contractor buying equipment

A contractor needs an excavator for jobs already under contract.

Recommend a term loan first. Lenders can see the use of funds, the asset supports the request, and the story is clean. Clean files get better traction.

Ask questions that help you package the deal fast:

- What is the exact equipment cost

- How soon does the machine need to be on-site

- How does this equipment produce revenue or reduce subcontractor expense

If the contractor says, "I want a line of credit so I have flexibility," do not accept that at face value. A practical broker response is: "For this purchase, I can usually present a stronger case with a term structure because the amount, purpose, and repayment path are all clear."

Scenario two with a retailer preparing for seasonal demand

A retailer needs to bring in inventory ahead of a busy season, but purchase timing will come in waves.

This usually fits a line of credit better. The client may draw for one order, pay it down as inventory sells, then draw again for the next cycle. That usage pattern matches revolving capital. A fixed lump sum can leave the owner paying on idle cash or force them to estimate the need too early.

My rule for recruits is simple. If the money will be used, repaid, and reused inside the same operating cycle, start the file as a revolving request unless the approval odds clearly point somewhere else.

Scenario three with an agency waiting on receivables

A marketing agency has good clients, but invoices clear after payroll and vendor bills come due.

Recommend a line of credit if the file can support it. The agency is not financing a big one-time purchase. It is smoothing timing gaps. That distinction matters because lenders want the structure to make sense for the use case.

On calls, I tell brokers to ask one direct question: "If receivables landed faster, would this cash need shrink on its own?" If the answer is yes, the case for revolving capital gets stronger.

Strong diagnosis starts before the application. Brokers who get better at qualifying leads effectively usually spot this pattern earlier and waste less time pushing the wrong product.

Scenario four with a restaurant facing a repair crisis

A restaurant needs an urgent HVAC repair before the weekend.

This takes judgment. If the repair is a single event and the business is otherwise stable, a term loan is often the cleaner recommendation because it funds the fix and puts repayment on a predictable track. If the repair is only the latest symptom of recurring short-term cash pressure, a line of credit may solve more than one problem, if the account performance supports that structure.

Do not ignore business stage here. A newer company, or one with limited operating history, may not fit neatly into either box through conventional channels. In those cases, review options such as unsecured business loans for startups instead of forcing a weak term-loan or line-of-credit narrative.

The inside track is this. Recommend the product that matches how cash moves through the business, then package the file so the lender sees the same logic in two minutes or less. That is how you get more approvals and protect your reputation with both clients and funding partners.

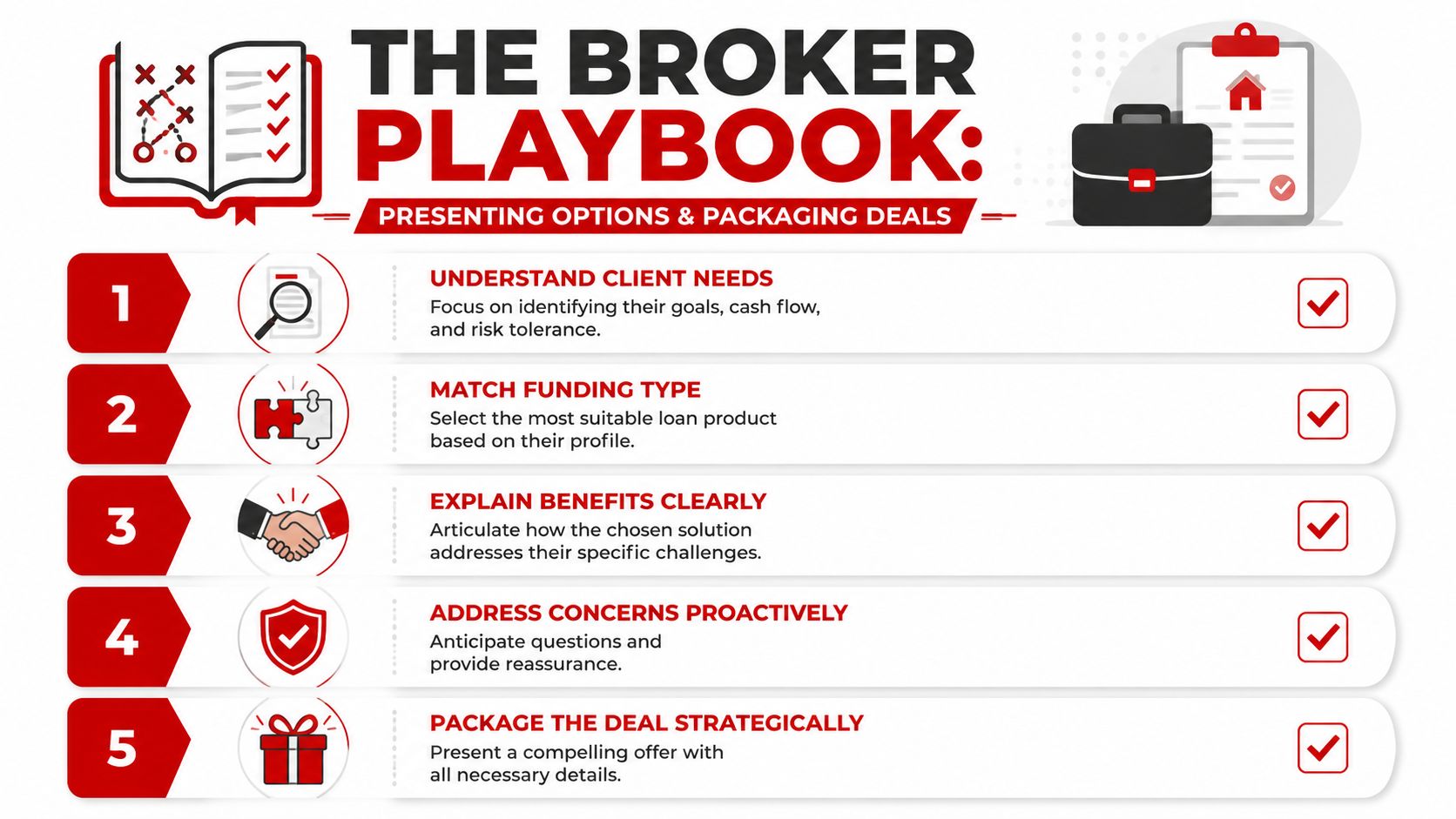

The Broker Playbook Presenting Options and Packaging Deals

A client says, “Just get me a line of credit.” A weak broker takes the order. A strong broker slows the conversation down, tests the use of funds, and presents the structure that closes.

That distinction is where reputations are built. Owners remember who gave them a real recommendation, not who echoed back the product name they asked for.

How to present options without sounding uncertain

Present one lead option and one fallback. More than that usually sounds like guesswork.

Use language that ties the product to the business pattern you uncovered in discovery. For example:

“Based on how this expense shows up in the business, the term loan is the better fit. It covers the full project, gives you a fixed repayment path, and avoids paying for access you may not need right now.”

For a revolving-capital case, keep it just as direct:

“Your issue is timing, not total capital. A line of credit fits better because the business needs reusable access for short gaps, not one lump sum sitting on the balance sheet.”

That phrasing does two jobs. It shows judgment, and it gives the client a reason to trust the recommendation.

What to say when the client is fixated on a line of credit

This comes up all the time. Owners hear “flexibility” and assume it is the stronger product in every case.

It is not.

Revolving products often face tighter credit standards than installment products. If the file is thin, the cleaner strategy is usually to explain the mismatch early and redirect the client before you burn lender capital or your own credibility.

A practical script:

- Acknowledge the request: “I understand why you want the line. It is useful when the need repeats.”

- Set expectations: “Approval for revolving credit can be stricter, especially if the revenue story or credit profile is uneven.”

- Reframe the recommendation: “For a one-time project, the term loan gives us a more financeable story and a better chance of getting this done now.”

That last line matters. Brokers do not get paid for winning product debates. They get paid for getting the file approved.

Packaging the file so the underwriter gets the story fast

Underwriters should understand the logic of the deal in under two minutes. If they have to guess why the client needs the money or how repayment works, the file is not ready.

A term loan package should stress the fixed purpose of the request:

- Use of funds: a clear purchase, project, refinance, or expansion need

- Amount logic: why the requested number matches quotes, invoices, or the actual project cost

- Repayment case: how the capital improves revenue, margin, efficiency, or stability

A line of credit file needs a different story:

- Cash-flow rhythm: recurring receivable gaps, inventory buys, seasonal swings, or payroll timing

- Draw-and-repay logic: evidence the business will use and cycle the line, not sit on it like a term loan

- Operating consistency: deposits, invoicing patterns, and account activity that support revolving access

This is also the point where good discovery work pays off. Brokers who are better at qualifying leads effectively usually collect the right details before they ever ask for documents, which makes packaging cleaner and submissions faster.

A simple broker checklist before submission

Run this check before you send the deal anywhere:

- Can I explain the need in one sentence?

- Does the product match the cash-flow pattern, not just the client's preference?

- Is the amount supported by a clear business reason?

- Will the repayment structure feel manageable based on actual account performance?

- Would an underwriter understand the full story without calling me for basics?

One more point new brokers miss. Existing debt can kill an otherwise workable file if you do not organize it properly. A clean debt schedule for lender review helps you show what is already on the books, what is being paid as agreed, and where the new facility fits.

The brokers who last in this business do not just know product definitions. They know how to frame the recommendation, handle pushback, and submit a file that makes sense on first read.

From Broker Knowledge to a Thriving Business

This skill has a bigger payoff than one funded file.

When a broker can answer the term loan vs line of credit question with authority, the broker becomes useful in a way that clients remember. The business owner may come in asking for one product, but what they really remember is that someone took the time to diagnose the situation correctly. That's what drives repeat conversations.

Why this creates referral momentum

Referral partners care about reliability. They want to know that when they send over a client, the broker won't force every situation into the same offer.

That's why product-fit knowledge turns into business growth. A CPA, consultant, real estate professional, or agency owner is more likely to refer when the broker consistently gives grounded recommendations. Over time, those relationships create a steadier flow of conversations than random outreach ever will.

A broker's reputation is built one well-matched funding recommendation at a time.

Why the model works from home

This business can be run remotely because the core asset isn't an office. It's judgment. The broker who can qualify, position, and package files well can work from a home office, build flexible hours, and grow through referrals and strategic partnerships.

For brokers using professional networking as part of that process, a proven LinkedIn lead generation framework can help sharpen outreach and relationship-building without relying on cold, generic messages.

Start Your Loan Broker Blueprint Today

A lot of people interested in business lending stay stuck in research mode. They read about products, watch industry content, and collect terminology, but they never build the practical skill of guiding a client to the right structure.

That skill is what separates casual interest from a real brokerage. A broker doesn't need to know everything on day one. But a broker does need a repeatable way to evaluate need, explain options, package submissions, and communicate with confidence. Term loan vs line of credit is one of the first places that discipline shows up.

What the next step should look like

The practical next move isn't to memorize more definitions. It's to learn a working process:

- How to qualify the opportunity

- How to identify the right product fit

- How to present a primary recommendation

- How to package the deal for approval

- How to build referral relationships around that expertise

That's how a remote, flexible, recession-conscious brokerage starts to become real. One conversation. One file. One funded client at a time.

If the goal is to build a business around helping owners access funding instead of guessing through product choices, the next step should be structured training and a clear roadmap.

Business owners need brokers who can do more than forward applications. They need someone who can think through the deal, explain the options, and guide the file toward the strongest funding path. If that sounds like the kind of business worth building, watch the free training from Business Lending Blueprint or schedule a strategy session to see how to launch a home-based loan broker business with a clear process and real support.