A new broker usually hits the same wall on an early call. The client asks whether the numbers work for buying a building, finishing a buildout, or refinancing a property tied to the business. The broker can talk confidently about funding options, but then the questions tighten. What would the payment look like, how much cash would be needed at closing, and will the lender even approve it?

That's the moment a Business Building Loan Calculator stops being a widget and starts becoming a sales tool. Used well, it helps a broker control the conversation, screen weak files before they waste time, and explain trade-offs in plain English. Used poorly, it turns the broker into a glorified payment reader.

For anyone building a remote, home-based brokerage, that difference matters. A calculator helps replace hesitation with structure. It gives the broker a repeatable way to qualify, advise, and move a prospect toward a real funding path instead of a vague “send over your docs and we'll see.”

Table of Contents

- From Uncertainty to Authority Your First Client Call

- Decoding the Calculator What Every Input Tells a Lender

- Beyond Monthly Payments The Metrics That Close Deals

- Running the Numbers Worked Examples for Brokers

- How to Interpret Results and Advise Your Clients

- From Calculation to Commission Your Blueprint for Success

From Uncertainty to Authority Your First Client Call

A prospect calls about buying a commercial building for the business. The conversation starts smoothly. Then the client asks whether the project is realistic with current rates, how much cash the lender will expect, and whether the business income supports the request. A new broker often freezes there, not because the deal is impossible, but because the broker is still thinking like a marketer instead of a credit advisor.

A seasoned broker handles that same call differently. The calculator comes up immediately. The broker starts testing scenarios, not guessing. Payment structure, cash injection, and qualification pressure points become visible within minutes. That gives the client something rare in lending. Clarity.

A practical habit helps here. New brokers should review calls the same way closers review game film. Resources on understanding sales call recording for founders can sharpen how objections, hesitation, and missing questions show up on real conversations. The calculator tells the broker what to ask. The recording shows whether those questions were asked well.

The shift from answering to diagnosing

Authority doesn't come from quoting a payment. It comes from diagnosing the file on the call.

A broker using a Business Building Loan Calculator correctly is listening for things like:

- Use of proceeds: Is this a straight purchase, a refinance, or a buildout with moving parts?

- Cash contribution: Does the client have the liquidity to close?

- Business strength: Is there enough reliable income to support debt?

- Deal friction: Are there existing obligations, weak reserves, or timeline issues?

Practical rule: The first call should reduce uncertainty. If the broker leaves the client with more confusion than they started with, the calculator wasn't used as a sales asset.

The recruit who learns this early gains an advantage fast. A calculator-led call feels more professional, creates trust sooner, and helps the broker decide whether to push forward, restructure, or redirect the client before time gets burned on a weak submission.

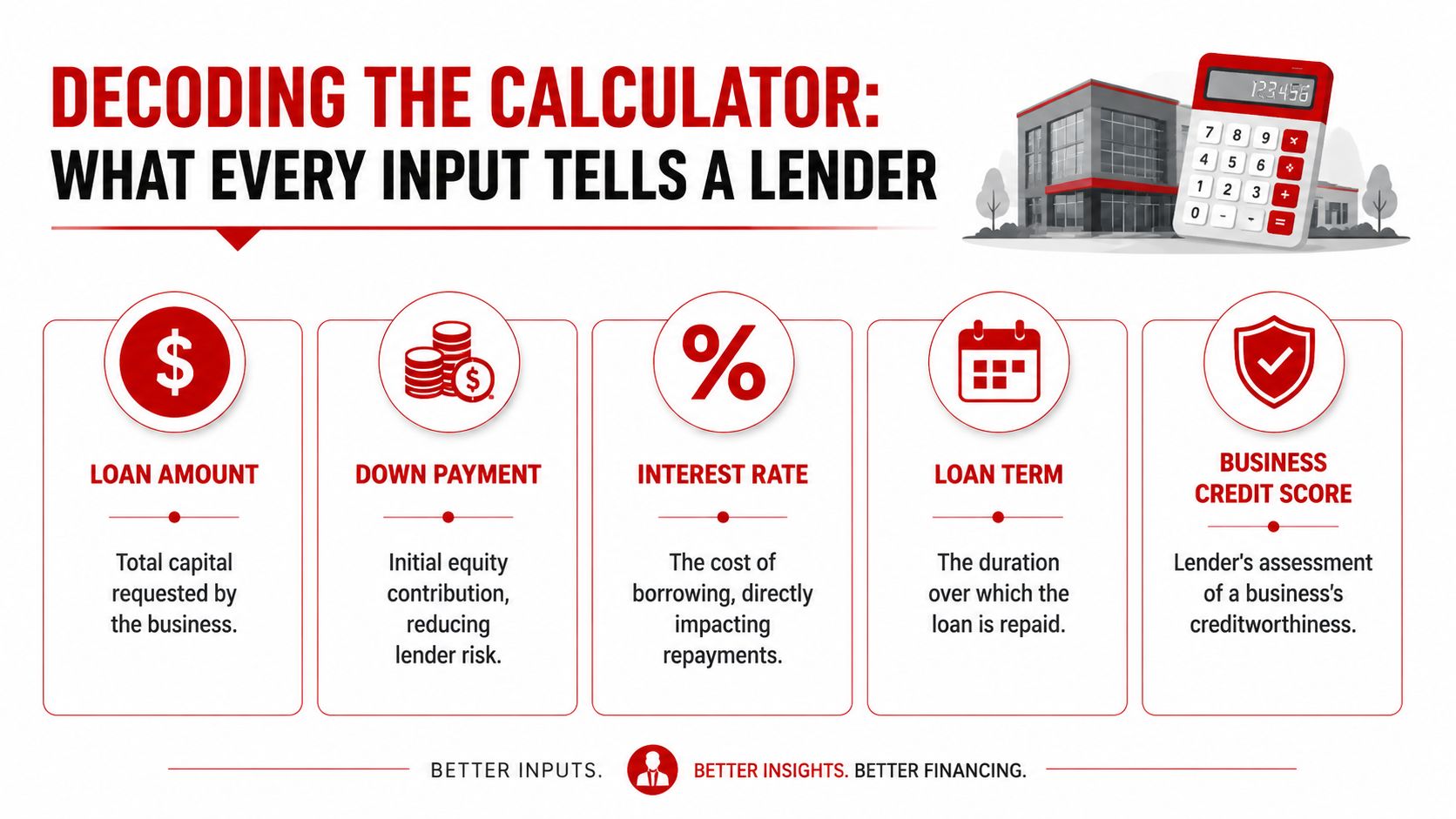

Decoding the Calculator What Every Input Tells a Lender

A broker earns credibility fast when the calculator becomes an intake tool instead of a guessing tool. A client may ask for a payment estimate. The lender is reading something else entirely. They are reading whether the request is coherent, whether the borrower can close, and whether the file deserves attention.

Start with the structure of the deal

New brokers often plug in a loan amount, rate, and term because that is what the client asks for first. That misses the point. The first job is to structure the request in a way a lender can assess.

For a building purchase, refinance, or buildout, the calculator should reflect the full capital stack. That means project cost or purchase price, borrower cash in, financed amount, expected fees, reserves if the lender wants them, and whether there is an interest-only period before full amortization. If those pieces are missing, the payment can look reasonable while the transaction is still dead on arrival because the borrower is short on cash to close.

That is the practical difference between quoting and qualifying.

Every input answers an underwriting question

Good brokers read calculator fields the way a credit officer reads an application. Each entry should trigger a follow-up.

Loan amount

This shows the lender's exposure and whether the request lines up with collateral value and business capacity. Round-number requests often signal that the borrower has not worked through the actual use of proceeds.Equity injection or down payment

This reveals both liquidity and commitment. More cash in can widen lender options. Thin equity usually means tougher pricing, tighter structure, or a lower probability of approval.Interest rate assumption

This is a stress test, not just a quote input. If the deal only works at an optimistic rate, the broker should rework the structure before sending it out.Term and amortization

These shape affordability, but they also expose weakness. A stretched amortization can improve the payment while masking weak cash flow or poor debt service coverage.Credit profile and business financials

These tell the lender whether the borrower has enough stability and documentation to move from conversation to credit review.

The calculator becomes more useful when the broker stops asking, "What payment does this produce?" and starts asking, "What concern will this number raise with the lender?"

Use the calculator to spot missing documents early

Strong files usually have clean inputs because the intake was handled properly. Weak files often show up as contradictions inside the calculator. The borrower says revenue is strong, but existing debt is vague. They claim ample liquidity, but cannot document the source of funds. They want maximum proceeds, but the equity line is still uncertain.

That is why supporting documents matter at this stage, not later. A debt schedule is one of the fastest ways to see what fixed obligations are already competing with the new payment. Brokers who need a refresher should review what a debt schedule is before they start sizing deals from borrower memory alone.

Bank statements create the same issue. Manual entry slows down intake and creates avoidable mistakes. If your process still depends on keying in deposits and withdrawals by hand, it helps to automate bank statement data entry so you can verify cash flow faster and spend more time on structure.

Sloppy calculator output usually starts with sloppy intake.

Some commercial mortgage training materials also show how lenders size requests with inputs beyond payment math, including property income, debt service assumptions, and collateral-based constraints, as explained by the CCIM commercial real estate glossary. That matters for brokers because it reframes the calculator. It is not a widget for answering basic questions. It is an early-stage screen for lender fit, file quality, and deal strategy.

Used well, the calculator helps a broker do three things before an application is submitted. Confirm whether the borrower is financeable, identify the pressure points in the file, and decide whether to proceed, restructure, or walk away.

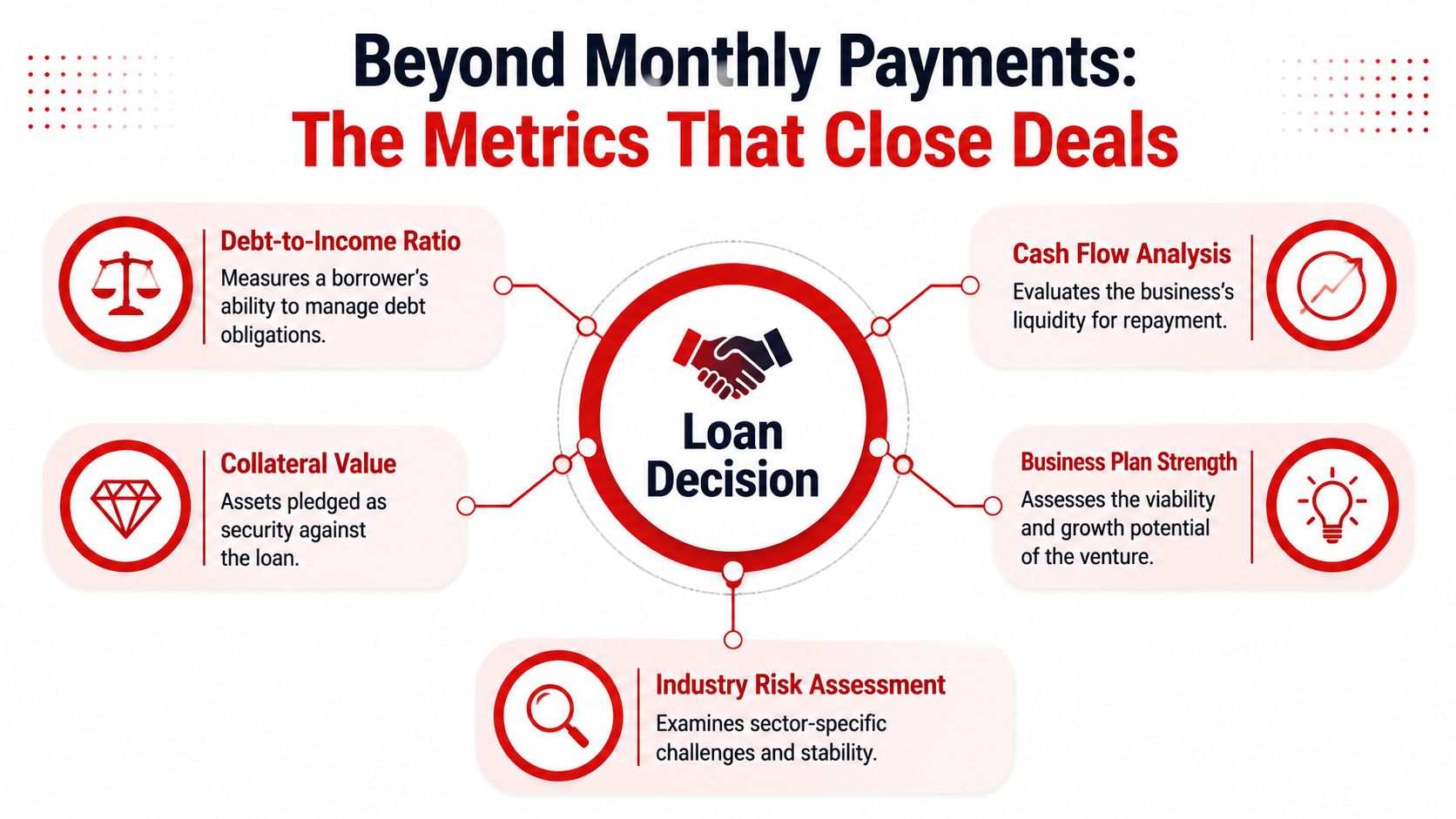

Beyond Monthly Payments The Metrics That Close Deals

A borrower says, “The payment works.” A lender still declines the file.

That gap is where brokers earn their fee.

Why underwriting metrics matter more than a pretty payment

A payment estimate only answers whether the note looks affordable on the surface. Approval usually turns on whether the income, collateral, and structure fit a lender's credit box. If a broker does not test those points early, the calculator becomes a false comfort tool instead of a qualification tool.

Three metrics do most of the screening work:

| Metric | What it tells the lender | Why the broker should care |

|---|---|---|

| DSCR | Whether business or property cash flow covers debt service | It shows whether the file has a realistic path to approval |

| LTV | How much debt sits against the collateral | It helps sort lender fit and likely equity requirements |

| Debt yield | Property income relative to loan amount | It matters more on income-producing real estate where collateral strength drives the credit decision |

Many lenders want to see a DSCR that clears their minimum threshold, and 1.25 is a common benchmark in commercial lending guidance from banking regulators and lender training materials. The practical point for a broker is simple. The calculator is not there to produce a payment the client likes. It is there to test whether the request survives real underwriting standards.

Brokers who want a tighter grasp of this ratio should review this walkthrough of debt service coverage ratio calculation. It helps connect a calculator output to the credit conversation you will have with lenders.

How a broker uses the metrics to place the deal

Payment is the visible result. DSCR is the credit test.

When DSCR comes in light, the broker needs to diagnose the cause before sending the file out. Sometimes the deal carries too much debt. Sometimes the term is too short, which pushes the payment higher than the cash flow can support. Sometimes the building request is fine, but existing obligations are already eating up too much monthly room.

That leads to a short list of real options:

- Change the structure. A longer amortization or different term can improve coverage, though it may increase total interest and affect lender appetite.

- Trim the loan amount. Less borrowing lowers debt service, but it also means a larger equity contribution from the client.

- Bring in more cash. More equity can improve both coverage and collateral position, though not every borrower has the liquidity.

- Clean up other obligations. Refinancing or paying down outside debt can make a marginal request financeable.

LTV answers a different question. It tells the lender how exposed they are if the deal goes wrong and they have to rely on the property. A borrower can show solid operating income and still miss the mark because the requested amount is too high for the asset type, location, or lender policy. In broker terms, that is not always a dead deal. It may be a different lender lane, a lower advance, or a conversation about adding cash.

Debt yield gives another layer on investment and owner-occupied real estate where collateral quality matters. If DSCR looks acceptable because the amortization is stretched, debt yield can still expose a weak loan request. That matters when you are deciding whether to spend time packaging the file or resetting expectations before you have lender fatigue.

This is also where brokers separate themselves from rate shoppers. Clients usually ask about rate first because it is easy to compare. A broker who can explain why the file is tight on coverage or too aggressive on collateral position sounds like an advisor, not a quote machine.

Some borrowers also need operational cleanup before a larger real estate request makes sense. Content that helps them stop small business cash flow failures can support that discussion. Better cash management will not fix every weak deal, but it can improve the next set of statements you submit.

A calculator earns its place when it helps you identify the actual obstacle early, then choose whether to proceed, restructure, or decline the opportunity. That is how brokers protect time, place cleaner files, and close more of the deals worth chasing.

Running the Numbers Worked Examples for Brokers

The fastest way to learn a Business Building Loan Calculator is to watch how the same tool changes role from one deal type to another. A broker handling a purchase, an investment property, and a construction request is not doing the same analysis three times. The math may sit in one calculator, but the questions change.

Buyer of an existing business property

Start with a client buying a building tied to an operating business. On the surface, this looks simple. Price, estimated down payment, likely rate, and desired term go into the calculator. The monthly payment appears, and the client feels relieved.

That's where weak brokers stop.

The stronger broker immediately asks whether the business income supports that payment alongside current obligations. If the client's existing debt load is already heavy, the payment result isn't the answer. It's just the start of the review. This is also where supporting financials and existing obligations become more important than a polished verbal pitch.

A useful companion in this review is a profitability screen. This guide on how to find profitability index helps a broker think beyond surface affordability and toward whether the project creates enough economic value to justify the financing path.

Investor on a small office acquisition

A commercial mortgage file requires a different discipline. Here, scenario analysis matters because rate sensitivity can reshape the deal quickly.

After the Federal Reserve's rate-hiking cycle began in 2022, commercial mortgage pricing moved sharply higher. One rate table showed regional banks and credit unions moving from a 2020 midpoint of 4.18% to 6.13% in 2022, a 46.53% increase, while debt funds rose from 7.25% to 9.25% and life insurers from 4.00% to 4.77%, as shown by commercial mortgage rate tables and calculator examples. For a broker, that matters because a calculator turns market movement into payment stress, interest burden, and deal viability.

At this point, the conversation gets practical. The broker doesn't need to dramatize rates. The broker needs to model them.

A strong workflow for this type of file looks like this:

- Run a base case using the client's expected terms.

- Run a stressed case using a less favorable pricing assumption.

- Compare affordability and coverage under both outcomes.

- Decide whether the client should proceed, renegotiate, or increase equity.

If the deal only works in the best possible scenario, the broker doesn't have a financeable file yet.

That kind of analysis makes a recruit sound experienced fast because it reframes the broker from order taker to advisor.

Developer on a buildout or construction file

Construction and buildout requests require the most caution. A generic calculator can create false confidence because the project may have no stabilized income during part of the loan period. The broker has to look at interest-only periods, draws, balloon exposure, cash needed before the space produces revenue, and whether the client can cover gaps.

Here the recruit must slow down and ask sharper questions:

- What stage is the project in? Land, permits, shell, tenant improvement, or near completion all create different risk.

- When does income begin? That timing changes how debt burden should be modeled.

- What cash must the borrower bring? The down payment isn't the whole story if fees and project gaps exist.

- Is the exit clear? Some files only work if the borrower can refinance or stabilize on schedule.

These examples show why one calculator output is never enough. A broker's job is to run the file from more than one angle and explain what changes if assumptions move. That's not overcomplication. That's what protects pipeline time and improves funding odds.

How to Interpret Results and Advise Your Clients

The client doesn't pay attention to calculator outputs because the math is exciting. The client pays attention because the numbers answer a business decision. A broker creates value by translating the result into next steps.

Translate outputs into decisions

Many calculators focus on monthly payment but miss the borrower's real question, which is “Can I qualify?” Lenders use underwriting inputs like DSCR to make decisions, and broker conversations should shift from simple affordability to actual eligibility, as reflected in this lender calculator approach.

That means the broker should avoid delivering raw outputs without context. Instead of saying, “Here's your payment,” the broker should say what the result implies:

- Comfortable payment, weak qualification: The monthly number may be manageable, but the file may still need stronger cash flow support.

- Tight payment, possible structure fix: The request may work with more equity, a different term, or a reduced loan amount.

- Solid qualification, weak liquidity: The business may qualify operationally but still struggle with closing cash.

Turn a weak result into an action plan

The best brokers don't present a weak result as a dead end. They present it as a roadmap.

A practical client-facing framework sounds like this:

| Output | What the broker says | What happens next |

|---|---|---|

| Coverage is thin | The business may need stronger support for this debt level | Review existing obligations, adjust structure, or lower request |

| Cash to close is too high | The transaction may require more liquidity than expected | Rework equity plan or phase the project |

| Payment is workable but risk is high | Another lender type or revised loan format may fit better | Repackage before submission |

“The numbers aren't a rejection. They're instructions.”

That approach protects the relationship. It also improves close rates because the client sees guidance instead of confusion. The calculator gives the broker evidence. The broker's interpretation turns that evidence into a plan the client can act on.

From Calculation to Commission Your Blueprint for Success

A calculator only earns money for a broker when it leads to cleaner submissions and funded files. Once the preliminary numbers make sense, the process shifts from analysis to packaging.

What happens after the pre-qualification

The broker should move quickly while the client's urgency is still high. That means collecting the documents that support the assumptions used in the calculator. If income, debt, liquidity, and project scope were central to the pre-qual, those are the first items that need verification.

A clean handoff usually includes:

- Business financials: To support the cash flow story used during screening.

- Debt schedule: To confirm fixed obligations and avoid surprises.

- Project or property details: To validate collateral and use of proceeds.

- Liquidity evidence: To confirm down payment and closing capacity.

The broker who packages a file this way makes lender review easier. Easier review usually means faster clarity, fewer avoidable conditions, and less fallout.

How brokers build a repeatable pipeline

A new broker shouldn't think of the Business Building Loan Calculator as a one-off prospecting aid. It belongs in a repeatable workflow.

That workflow looks like this in practice:

- Use the calculator on the first serious call to establish whether the deal deserves full intake.

- Identify the obstacle early so the file gets structured before submission.

- Collect only the documents needed to validate the scenario instead of overwhelming the client.

- Submit a tighter package because the deal has already been pressure-tested.

- Turn funded clients into referral relationships because advisory value was demonstrated upfront.

The long-term benefit is greater efficiency. A broker working from home can handle more opportunities when weak files are screened earlier and better files are packaged faster. That's one reason many people explore this business model as a flexible income path. Anyone evaluating the opportunity can review this overview of business loan broker salary to understand the role more broadly.

The recruit who masters this process doesn't just become better at quoting loans. That person becomes easier to trust, easier to refer, and easier for lenders to work with.

Business Lending Blueprint shows aspiring brokers how to turn skills like these into a real, home-based lending business. If the goal is to help business owners secure funding, build referral relationships, and create a flexible income stream without relying on hype, the next step is simple. Watch the free training at Business Lending Blueprint or schedule a strategy session to see how the model works.