A lot of new brokers start the same way. Contact names sit in a spreadsheet, notes live in an inbox, follow-ups depend on memory, and referral partners get attention only when a deal is active. That setup can produce a few transactions, but it rarely produces a stable business.

A real brokerage runs differently. Leads, borrowers, documents, tasks, partner relationships, and post-close follow-up all live inside one system. That system doesn't just store names. It controls timing, visibility, accountability, and repeat business.

That's why the phrase CRM system for mortgage brokers matters well beyond mortgage. The same discipline applies to business lending, equipment finance, and other broker models. Any referral-driven brokerage needs a central operating system if the goal is to build something scalable, remote-friendly, and less dependent on constant prospecting.

Table of Contents

- From Chaos to Control Why Brokers Need More Than a Spreadsheet

- Your Digital Cockpit What a Broker CRM Actually Does

- The Anatomy of a High-Performance Broker CRM

- Building Your Referral Engine with a CRM

- Your Broker CRM Evaluation Checklist

- Implementation Roadmap and Measuring Your ROI

- Build Your System Build Your Freedom

From Chaos to Control Why Brokers Need More Than a Spreadsheet

A new broker often thinks the problem is lead flow. Usually, the first real problem is deal management.

One borrower sends tax returns by email. Another texts on a weekend. A referral partner wants an update. A lender asks for a missing document. The spreadsheet still says “working,” but nobody can tell what's waiting, who owns the next step, or which file is drifting toward silence. That's how businesses start feeling busy without becoming organized.

The firms that stay in control don't rely on memory. They build process into the business from the start. That's one reason CRM has moved from optional software to operating infrastructure. One industry projection puts the mortgage CRM market at about $240 million in 2025 and projects $569.3 million by 2035, implying roughly 9% annual growth, while also noting adoption of around 79% of federally regulated U.S. lenders and 71% of non-bank lenders in the same source, as outlined in these mortgage CRM market statistics.

That shift matters to anyone entering brokering. If established lenders already treat CRM as part of the baseline, an independent broker can't afford to run the business like a side project.

Practical rule: If a borrower, lender, or referral partner can fall through the cracks because one person forgot to follow up, the business doesn't have a system yet.

A spreadsheet still has a role. It can help with rough planning, list building, or quick analysis. It fails when it becomes the main place where pipeline, communication history, and relationship management live. Spreadsheets don't enforce next actions. They don't show bottlenecks clearly. They don't create a repeatable handoff if the business grows.

That's also why broader thinking around CRM strategies for B2B growth is useful here. The lending niche has its own compliance and workflow demands, but the core lesson is the same. Businesses grow when they systemize relationships, not when they collect contacts.

For readers thinking beyond a single loan file and toward an actual company, this matters even more when planning structure, positioning, and operations. A useful next step is understanding the broader business model behind starting a mortgage lending company. The technology only works when it sits inside a clear operating model.

Your Digital Cockpit What a Broker CRM Actually Does

A specialized broker CRM works best when it's treated like a digital cockpit. It gives one place to monitor movement, spot problems early, and trigger the next action before a file stalls.

That's very different from a contact database. A contact list stores names. A cockpit helps run the business.

One record instead of five versions of the truth

A true mortgage CRM should centralize borrower data from lead capture and pre-qualification through origination and post-close servicing, which reduces handoff friction and redundant re-entry across systems, as described in this overview of centralized borrower visibility in mortgage lending.

In practice, that means one borrower record should hold the essentials that matter to the brokerage:

- Contact history: calls, emails, messages, meeting notes, and pending follow-ups

- File status: where the deal sits, what's missing, who owns the next move

- Document trail: checklists, uploads, request history, and completion status

- Partner context: who referred the lead, who needs updates, and which relationship should be credited later

When this lives in one place, a broker stops reacting and starts managing.

A good CRM also improves the client experience. Borrowers don't want to repeat the same story to three different people. Referral partners don't want to chase updates. Teams don't want to guess whether a condition was already requested. A centralized system cuts that friction.

Visibility changes behavior

A strong CRM doesn't just store information. It makes work visible.

That means the broker can open the dashboard and immediately see which deals are fresh, which have gone quiet, which partners are sending business, and which files have been waiting too long in one stage. That visibility changes daily decisions. Follow-up becomes scheduled instead of emotional. Prioritization becomes clearer. Capacity becomes easier to manage.

A broker with clear pipeline visibility usually looks more responsive to the market because the next action is already defined before the borrower asks for an update.

Automation sits on top of that visibility. Tasks can be assigned when a file reaches a stage. Borrowers can receive the next instruction without manual chasing. Partners can get status updates at moments that matter. For teams trying to sharpen this side of operations, practical guidance on mastering CRM workflows helps translate the concept into daily execution.

Client communication also gets stronger when expectations are structured instead of improvised. That's why many brokers pair CRM discipline with a clear process for managing client expectations. The system holds the truth. The communication reinforces it.

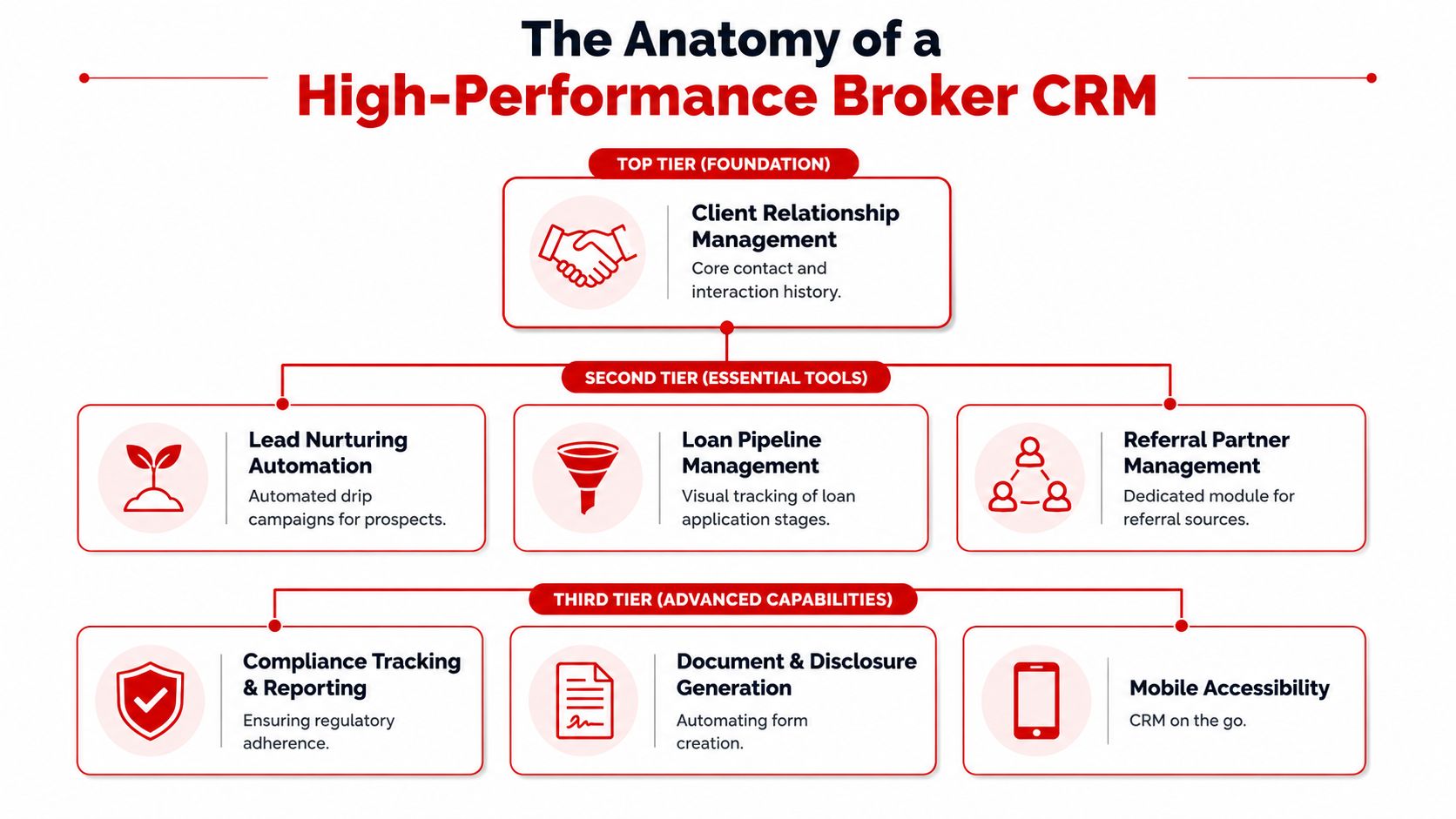

The Anatomy of a High-Performance Broker CRM

Not every CRM built for sales is built for lending. A broker can force a generic system to work, but that usually creates extra admin, broken workflows, and weak visibility where it matters most.

A high-performance CRM system for mortgage brokers has layers. The first layer keeps the business organized. The second helps it scale. The third reduces avoidable risk.

Foundation first

The foundation is simple. The system needs to fit the brokerage's actual deal cycle.

That starts with custom pipeline stages. A broker shouldn't be stuck with vague stages like lead, qualified, proposal, and won. Lending files move through more specific milestones. Inquiry, intake, application received, docs pending, submitted, conditionally approved, funded, and post-close are the kinds of stages that create real operational clarity.

The second foundation is the borrower profile. It should include more than name and phone number. It needs custom fields for referral source, funding purpose, business or property profile, key dates, loan amount, assigned owner, and document status. If a broker can't open one record and understand the file in under a minute, the profile isn't built properly.

A practical setup often includes:

- Stage-specific checklists: each deal stage carries its own required items

- Task ownership: every open item has a person attached to it

- Communication logging: notes don't live in scattered inboxes

- Referral attribution: every funded file traces back to a source

A calculator can support analysis, but the CRM should remain the command center. Financial planning tools such as a business-building loan calculator help with scenario work, while the CRM keeps the workflow moving.

The scale layer

Once the foundation is stable, the next question is whether the system removes manual work or just documents it.

For brokers, the strongest pattern is event-driven integration between the point-of-sale system, loan origination system, and CRM. When an application is completed or a loan status changes, the CRM should automatically create or update the contact and deal record, shift the pipeline stage, and trigger the next communication or task. That implementation pattern is described in this discussion of event-driven mortgage CRM integration.

That matters because manual re-entry creates hidden damage. People mistype phone formats. Dates land in the wrong field. Loan amounts don't match. Follow-ups wait because nobody noticed the change.

A scalable CRM should also support:

| Layer | What it should handle | What happens if it doesn't |

|---|---|---|

| Pipeline automation | Move files when milestone events occur | Staff updates stages late or not at all |

| Task triggering | Create reminders based on status or aging | Follow-up depends on memory |

| Data mapping | Normalize phone, date, and amount fields | Reporting becomes unreliable |

| Communication workflows | Send the right update at the right moment | Borrowers and partners feel ignored |

The risk-control layer

Advanced capability isn't only about speed. It's about control.

A lending CRM should support audit-friendly communication logs, clear permissioning, and document handling that fits a regulated workflow. AI-assisted follow-up can be useful, but only when the brokerage can review what's sent, when it's sent, and what data triggered it.

Good automation feels quiet. It removes repetitive effort without making the brokerage lose track of what was said, promised, or stored.

That's the difference between a CRM that looks modern in a demo and one that can support a serious brokerage.

Building Your Referral Engine with a CRM

Most brokers use their CRM like a transaction tracker. That leaves money on the table.

The better use is building a repeatable referral engine. In a relationship-driven business, the database isn't just a list of past activity. It's the business's future pipeline if it's segmented, maintained, and worked with discipline.

One major blind spot in mortgage CRM usage is post-close and referral-partner operations. A widely discussed industry view is that brokers need to manage borrower retention and partner nurturing, not just the initial lead pipeline, because relationship-based revenue depends on those repeat loops. That gap is highlighted in this discussion of post-close and referral-focused mortgage CRM strategy.

Past clients are not closed files

A funded deal should trigger a new workflow, not the end of one.

Many brokers stop communicating once the file closes unless the borrower reaches back out. That's a mistake. The CRM should immediately place that client into a post-close sequence built around value, timing, and memory.

A practical post-close structure often includes:

- Immediate follow-up: confirm funding completion, next steps, and key contacts

- Check-in cadence: periodic outreach tied to likely future needs or milestones

- Referral prompts: ask for introductions only after trust has been reinforced

- Reactivation flags: surface prior clients whose profile suggests a new financing conversation may be timely

This matters in both mortgage and business lending. A borrower who had a smooth, organized experience is far more likely to return and refer than one who felt chased, confused, or forgotten.

A closed file should become a managed relationship category inside the CRM, not a dead archive.

For people building a flexible, home-based brokerage, this is one of the cleanest paths toward steadier revenue. It aligns closely with broader thinking around passive income business ideas, because the actual asset isn't passive software. It's an active relationship database that keeps producing introductions over time.

Partners need their own workflow

Referral partners shouldn't sit in the same bucket as borrowers.

A broker should create separate records, fields, and activity plans for accountants, agents, consultants, attorneys, and other relationship sources. Their workflow is different. They need touchpoints, status updates, appreciation, co-marketing opportunities, and attribution tracking.

A useful referral-partner CRM structure includes:

| Partner element | What to track |

|---|---|

| Source profile | niche, geography, client type, preferred deal size |

| Activity history | meetings, calls, introductions, shared content |

| Open opportunities | deals sent, status, pending updates |

| Relationship plan | next touch date, value-add idea, review cadence |

When this is done well, the broker stops guessing where business came from and starts seeing which relationships deserve more attention.

Your Broker CRM Evaluation Checklist

A CRM demo can be misleading. Almost every system looks clean for twenty minutes. The crucial question is whether it can support the way a lending brokerage operates.

The easiest way to avoid buying the wrong system is to evaluate it as an operator, not as a shopper. The broker shouldn't ask whether the dashboard looks polished. The broker should ask whether the system can handle handoffs, exceptions, partner relationships, and follow-up discipline.

Questions for pipeline and workflow control

Start with workflow reality.

- Can stages be customized to match the brokerage's actual lending process? Generic sales stages create confusion fast.

- Can tasks trigger automatically when a file changes status or sits too long in one stage? If not, the team will chase manually.

- Can the system show aging by stage? A pipeline without aging visibility hides bottlenecks.

- Can one record hold notes, tasks, documents, and communication history together? If data is split, staff will work from partial information.

A practical demo should include one messy file, not one perfect file. The broker should ask the provider to show how the system handles missing documents, stalled communication, reassignment, and repeated follow-up.

Questions for integrations and partner management

A CRM becomes more valuable when it talks cleanly to the systems around it.

- Does it support stable integration with the brokerage's intake, origination, and communication stack?

- Can fields be mapped cleanly for phone, date, amount, and source data?

- Can separate record types be created for borrowers and referral partners?

- Can referral source, referral date, and relationship owner be tracked without workarounds?

If the answer to those questions is weak, the broker may end up paying for software that creates admin instead of removing it.

Questions for compliance and reporting

At this stage, many buyers get too casual.

Ask the vendor to show the audit trail, not just talk about compliance.

A serious evaluation should include:

- Message logging: can the brokerage review what was sent and when?

- Permission controls: can access be restricted by role?

- Consent handling: can the business manage communication preferences clearly?

- Reporting: can the system produce useful views on lead sources, stage movement, and funded outcomes?

The right CRM should make the brokerage easier to manage. If basic reporting still requires exporting everything into spreadsheets, the system probably isn't ready for growth.

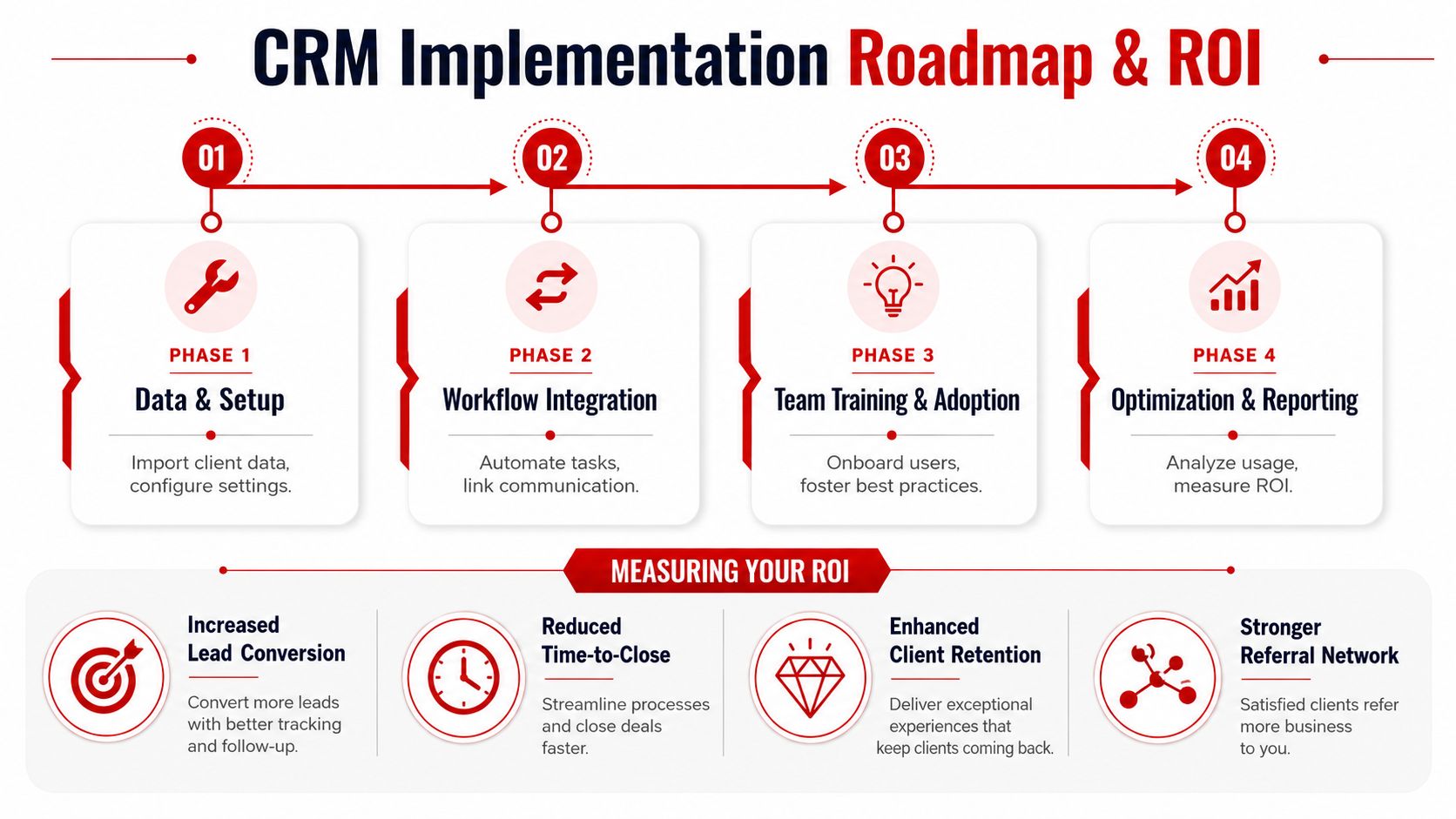

Implementation Roadmap and Measuring Your ROI

A lot of CRM projects fail for a simple reason. The business tries to build the perfect system before building a working one.

The better approach is phased implementation. Clean data first. Then workflow. Then adoption and reporting. That sequence keeps the project manageable and makes it easier to spot what's working.

Phase one through phase three

Phase one is data and setup. Import contacts, clean duplicates, define borrower and partner record types, build pipeline stages, and set required fields. If the data goes in sloppy, the reporting comes out sloppy.

Phase two is workflow automation. Add stage-based tasks, reminders, templates, and core follow-up sequences. Keep it simple at first. A few high-value automations usually outperform a complicated setup nobody trusts.

Phase three is integration and adoption. Connect intake sources, origination events, and communication channels where appropriate. Then train everyone on one standard way to use the system. Good CRM discipline depends less on software brilliance and more on consistent usage.

For teams that want a broader operational view of CRM adoption and integration, implementation guidance is useful. The key is still execution. A brokerage needs documented rules for what gets entered, when stages change, and who owns exceptions.

What ROI looks like in practice

ROI from a broker CRM usually shows up first in control, then in conversion.

The most useful measurements are practical business metrics such as:

- Time-to-close: are files moving with fewer delays?

- Lead-to-funded ratio: are more qualified opportunities reaching the finish line?

- Referral partner conversion rate: which relationships produce actual funded volume?

- Client lifetime value: do past clients come back or refer others?

These don't need invented benchmarks to be useful. A broker only needs a before-and-after view inside the same business. If follow-up is tighter, if fewer deals go cold, and if partner attribution becomes clearer, the CRM is producing real return.

One caution matters here. AI and automation can create compliance risk if they aren't managed carefully. Mortgage CRM guidance increasingly emphasizes that workflows should be auditable and respect communication and data privacy requirements, as discussed in this review of AI and compliance considerations in mortgage CRM.

Common implementation mistakes usually look like this:

- Overbuilding too early: too many fields, too many stages, too many automations

- Weak training: each person uses the CRM differently

- Poor data hygiene: duplicates, missing fields, inconsistent naming

- Unreviewed automation: messages go out without enough oversight

The best CRM rollout is boring in the beginning. Clean records, clear rules, and a handful of reliable automations beat a flashy system nobody follows.

Build Your System Build Your Freedom

A CRM is often treated like software overhead. For a broker, it's closer to operational strength.

It replaces scattered notes with visibility. It replaces reactive follow-up with structured workflow. Most important, it turns past clients and referral partners into a managed business asset instead of a forgotten contact list.

That's the larger point behind choosing the right CRM system for mortgage brokers. The software itself isn't the win. The win is what the system allows a broker to build: a company that can operate from home, run with less chaos, scale through relationships, and produce repeat business without depending on constant cold outreach.

The brokers who last don't just close files. They build systems that make future files easier to win.

That same thinking applies to anyone entering business lending. The opportunity isn't just in one transaction. It's in building a referral-driven brokerage with process, follow-up discipline, and a database that grows more valuable over time.

Business Lending Blueprint shows aspiring brokers how to build that kind of business from the ground up. If the goal is to create a flexible, home-based brokerage built on referral relationships instead of random hustle, watch the free training at Business Lending Blueprint or schedule a strategy session to see how the model works in practice.