A new broker often sees the same pattern in a client file. Revenue looks respectable. Deposits are coming in. The owner insists the business is busy. Yet the profit and loss statement looks thin, and the lender hesitates. The gap usually sits in overhead.

That's why learning how to calculate overhead cost matters so much in business lending. It helps a broker explain weak margins, identify what can be tightened, and present a cleaner story to an underwriter. It also teaches a second lesson that matters just as much. A home-based brokerage can stay lean, flexible, and highly controllable when overhead is understood from day one.

Table of Contents

- Why Mastering Overhead Wins More Deals

- Fixed Variable and Semi-Variable Costs Explained

- A Broker's Method for Calculating Total Overhead

- Using Overhead to Analyze Deals and Advise Clients

- Keeping Your Own Brokerage Lean and Profitable

- Build Your Profitable Brokerage Today

Why Mastering Overhead Wins More Deals

A broker doesn't lose deals only because revenue is low. Deals also stall because the business can't show enough retained cash after operating expenses. Overhead is where that story becomes clear.

Lenders read overhead as a risk signal

Many owners focus on sales because sales feel like momentum. Lenders focus on what remains after the business pays to stay open. That includes rent, utilities, admin payroll, insurance, software, support staff, and the collection of small recurring costs that subtly erode margin.

In many small business settings, practitioners aim for an overhead rate of roughly 10 to 20% of total sales, and rates above 20 to 25% can signal higher operating costs, which lenders treat as a warning sign when judging repayment ability, as explained in Wall Street Prep's overhead rate guidance.

A broker who understands overhead can answer the questions underwriters care about:

- Is the business temporarily compressed or structurally inefficient?

- Are expenses stable, or are they creeping up faster than operations can support?

- Can new capital improve capacity, pricing, or execution enough to justify the request?

Practical rule: Strong revenue with weak profit usually means the broker should inspect overhead before blaming the business model.

That changes the broker's role. Instead of pushing paper, the broker becomes the person who can translate messy operating results into a clear lending case.

The same skill sharpens a broker's own model

This skill also matters on the brokerage side. A home-based loan brokerage can avoid many of the fixed burdens that hurt traditional businesses, but only if the operator stays disciplined. Remote work lowers overhead only when subscriptions, marketing spend, admin support, and workspace costs are tracked and kept rational.

A new broker who understands overhead sees two opportunities at once. First, client files become stronger because expenses are classified and explained better. Second, the brokerage itself becomes easier to scale because unnecessary overhead gets cut before it hardens into monthly drag.

That's one reason the business loan broker model appeals to entrepreneurs, consultants, bankers, CPAs, and sales professionals looking for a flexible and recession-resistant path. The work can be done remotely, commissions come from solving real funding problems, and referral relationships can create repeat business without the burden of a heavy office footprint.

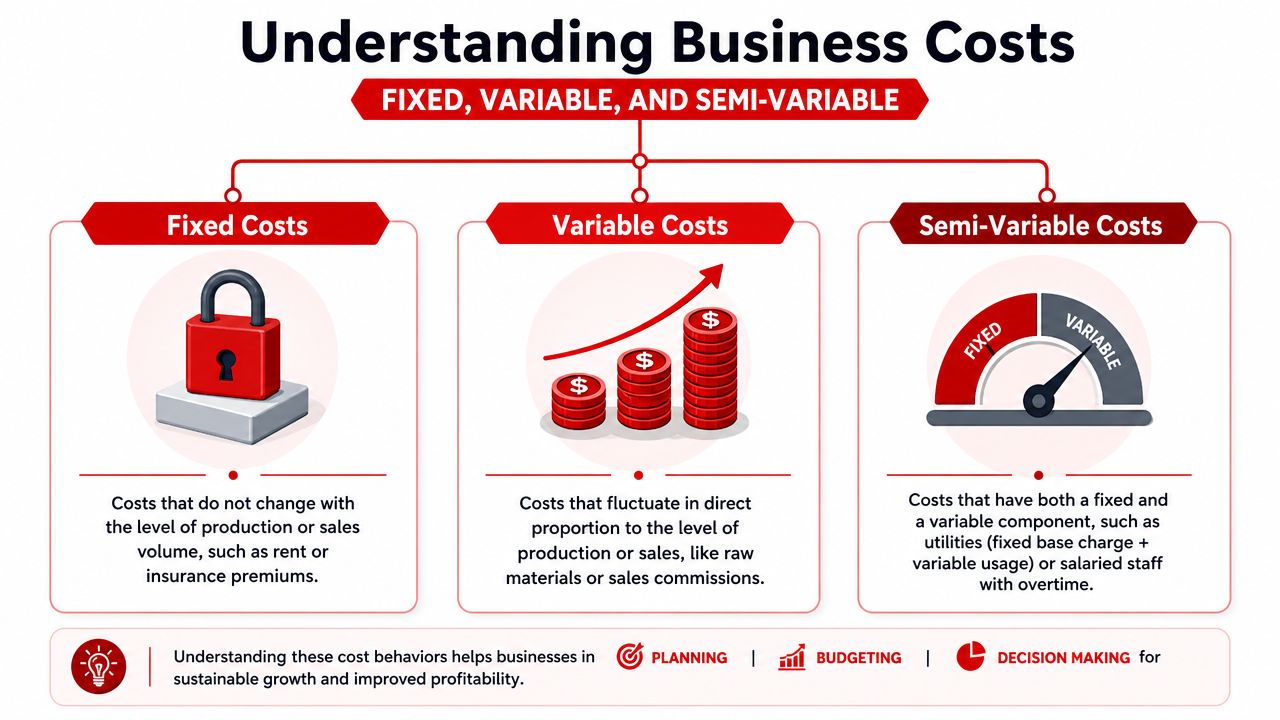

Fixed Variable and Semi-Variable Costs Explained

Most overhead mistakes begin before the math starts. They begin when expenses are labeled the wrong way.

Fixed costs stay put until the business structure changes

A fixed cost doesn't move much month to month just because sales changed. Office rent is the classic example. So is a standard insurance premium. In a home-based service business, a base software subscription or bookkeeping retainer may also behave like a fixed cost.

Fixed doesn't mean permanent. It means stable within a practical period. A business can still renegotiate a lease or cancel a subscription later. But for the current operating cycle, the cost stays mostly the same whether the business signs one client or several.

That distinction matters when reviewing a file. If a client claims margins will improve quickly, but most of the cost stack is fixed, the broker should ask what operational change will produce the improvement.

Variable and semi-variable costs need a closer look

A variable cost rises and falls with output or sales activity. In service businesses, sales commissions can behave this way. In product businesses, shipping or fulfillment support may move with transaction volume.

A semi-variable cost sits in the middle. It has a base level that must be paid, plus a usage-driven component. Utilities often fit this pattern. So can labor arrangements where staff receive a salary but also earn overtime during heavy periods.

Costs don't become easier to manage because a client calls them “general expenses.” They become manageable when each line item is tied to how the business actually operates.

A quick working test helps:

- Ask what happens if sales freeze for one month. If the cost stays, it's likely fixed.

- Ask what happens if workload doubles. If the cost rises almost in step, it's likely variable.

- Ask whether there's a base charge plus added usage. That usually points to semi-variable.

For brokers serving service firms, consultants, agencies, and independent operators, this skill matters because these businesses often blur expense lines. A communications plan may be fixed. Travel may be variable. A phone bill may be semi-variable. That's why a resource like Understanding business cost structure can help sharpen the distinction.

It also helps to understand how revenue is presented before expense analysis begins. Many owners confuse top-line numbers, which can distort every later ratio. A quick review of net revenue vs gross revenue helps frame the right base before overhead gets calculated.

A Broker's Method for Calculating Total Overhead

A client hands over a profit and loss statement that shows decent revenue and a thin margin. On paper, the deal looks close. Then you trace the underlying support costs behind delivery, admin payroll, software, insurance, occupancy, and mixed-use expenses, and the file changes. Sometimes it gets weaker. Sometimes it gets easier to defend because the numbers finally match how the business operates.

That is why overhead has to be calculated with a repeatable method. Brokers need one approach for underwriting a client's business and another for protecting margin inside a home-based brokerage, where low overhead is an advantage only if it is accurately measured.

Build the total from indirect costs only

Use a plain formula: Total Overhead = Indirect Labor + Indirect Materials + Indirect Expenses.

The formula is simple. The judgment sits in what belongs inside each bucket.

For a service firm, indirect labor usually includes admin staff, schedulers, bookkeepers, managers, and support roles that keep work moving but are not billed straight to a client job. Indirect materials cover low-cost supplies and operating items consumed in the background. Indirect expenses include occupancy, insurance, internet, software, licensing, professional fees, and other recurring costs of staying open.

For a home-based brokerage, the categories are smaller but they still count. CRM subscriptions, E&O insurance, licensing, phone service, internet, bookkeeping, continuing education, and a reasonable home office allocation are overhead. Commission splits tied directly to a closed deal usually are not.

Classification is where files get distorted. Owners often push too much into direct cost because they want margins to look stronger, or they dump everything into one general expense line that tells a lender nothing. A broker should reclassify the ledger so the expense structure can be defended in a credit memo.

Pull a full-year view before you total anything

One month is noisy. Use 12 months of actual expenses when possible.

That gives you a cleaner average for recurring costs, catches seasonal spikes, and exposes expenses that the owner forgot to mention in conversation. Annual insurance, license renewals, tax prep, software upgrades, and occasional contract admin help can disappear in a single-month review and then show up later as a surprise.

A simple worksheet is enough:

| Expense Item | Monthly Cost | Cost Type (Fixed, Variable, Semi-Variable) | Overhead Category (Indirect Labor, Indirect Materials, Indirect Expense) |

|---|---|---|---|

| Administrative assistant pay | |||

| Office supplies | |||

| Internet service | |||

| Insurance premium | |||

| Software subscriptions | |||

| Fuel for mixed-use vehicle | |||

| Home office allocation |

Once the ledger is sorted, total the monthly average for each category and combine them into total overhead. Then compare that number against monthly revenue. A high overhead load does not kill a deal by itself, but it tells you where repayment pressure will show up first if sales soften.

Handle mixed-use expenses with discipline

Hybrid expenses are where credibility is won or lost.

Home office, vehicle, phone, internet, and shared equipment often support both personal and business use. If the owner assigns too much to the business, the file looks aggressive. If too little gets assigned, the business appears cheaper to run than it really is, which creates problems when new debt is added.

Use a basis you can explain in one sentence:

- Home office by dedicated business square footage as a share of total home space

- Vehicle by business miles as a share of total miles

- Phone and internet by business usage pattern

- Equipment by actual business use over total use

Lenders do not require perfect precision. They do require a method that is consistent and believable.

Labor-heavy files need extra care here because payroll burden often gets buried inside broad wage lines. The insights on PEO labor burden for CFOs are useful when you need to separate direct service labor from the support costs wrapped around that labor.

Convert overhead into a number you can use in the deal

After you have monthly total overhead, test it against three questions.

First, does the business still show enough gross profit to cover this overhead comfortably? Second, what happens if revenue drops for a quarter? Third, will the new loan payment fit after overhead is paid, not before?

That last question matters for both sides of the broker's desk. When you are structuring financing for a client, overhead tells you whether repayment capacity is real or just optimistic. When you are running your own brokerage, overhead tells you how many funded deals you need each month to stay profitable without bloating the business. A quick check with a business loan payment and project cost calculator helps pressure-test the post-funding cash flow before you pitch terms.

Good brokers do not stop at revenue. They calculate what it costs to keep the machine running, because that number decides whether a deal closes cleanly, gets restructured, or should never be submitted at all.

Using Overhead to Analyze Deals and Advise Clients

Total overhead by itself is only a lump sum. It becomes useful when the broker converts it into a decision tool.

Allocation turns one big number into decision-making data

The standard allocation formula is straightforward: Overhead Allocation Rate = Total Indirect Costs ÷ Allocation Base. The harder part is choosing the right base.

For service businesses, direct labor hours often make sense because client work consumes staff time. For production-heavy firms, machine hours or direct costs may track better. What matters is fit. Best-practice guidance says the allocation base should strongly correlate with overhead consumption, and businesses using arbitrary allocations are 25 to 30% more likely to underprice or overprice certain service lines, according to Xero's guide to overheads.

A broker should be skeptical when a client spreads overhead evenly across every job just because it feels simple. Equal spread almost never reflects real operating behavior. Some services require more admin touch, more revisions, more billing effort, or more support time than others.

What overhead reveals in a lending conversation

Once a rate is assigned, the broker can ask better questions.

- Which services carry too much hidden support cost? A client may think a low-ticket offer is profitable because it sells often, but the service may consume heavy admin time.

- Where can pricing be justified? If billable work carries more overhead per labor hour than the owner realized, a price increase becomes easier to defend.

- What financing request improves efficiency? Equipment, staffing support, or process upgrades make more sense when the broker can show what overhead pressure they relieve.

That's where the broker stops being a form filler and starts acting like an advisor. A useful lens for that broader review is this guide to financial analysis strategy, especially for understanding how overhead fits inside wider credit presentation.

Underwriting insight: A lender is more comfortable when the broker can explain not just what the business spends, but why those costs behave the way they do.

For more advanced files, activity-based costing can sharpen the analysis further by grouping overhead into activities such as support, billing, and facilities, then assigning those pools using operational drivers. Even without building a full activity-based model, the broker who thinks this way will usually spot margin leaks faster than a broker who relies only on top-line revenue.

Profitability analysis also becomes stronger when overhead is tied back to service economics. A client deciding which projects to pursue, which channels to cut, or which service line deserves expansion benefits from a simple decision framework like the one behind this profitability index guide.

Keeping Your Own Brokerage Lean and Profitable

A brokerage doesn't need heavy infrastructure to operate professionally. That's one of the model's biggest advantages. But low overhead doesn't happen automatically. It comes from refusing to stack fixed costs before revenue patterns justify them.

Low overhead creates room to grow

A home-based broker can structure the business around essentials. That usually means a reliable workspace, communication systems, file organization, compliance habits, and relationship management. It doesn't require a storefront, a full in-house support team, or broad marketing overhead from the start.

That structure creates practical benefits:

- More flexibility: the operator can work remotely and serve clients without geographic limits.

- More resilience: fewer fixed obligations make uneven deal cycles easier to absorb.

- More scalability: support can be added in layers as deal flow becomes consistent.

For professionals coming from banking, consulting, insurance, tax, or sales, this can be a refreshing shift. The business can be built around referrals, repeat relationships, and funded transactions rather than around maintaining a large expense base.

Practical controls that protect margin

The fastest way to lose the advantage of a lean brokerage is to let small recurring expenses multiply. That happens when every new need turns into another subscription, another paid service, or another loosely defined contractor relationship.

A disciplined broker should keep a short control list:

- Choose systems by necessity first. If a process can be handled cleanly without adding another monthly bill, keep it simple.

- Build around referral channels. Referral relationships often outperform scattered paid outreach because they bring warmer borrowers and lower acquisition waste.

- Use support labor selectively. Admin help can be valuable, but it should be tied to consistent workload, not optimism.

- Review recurring charges monthly. Small software and service fees become permanent overhead if nobody challenges them.

- Track client acquisition cost qualitatively. Even without formal dashboards, every broker should know which activities produce funded opportunities.

A relationship-driven business also needs organized follow-up. A broker evaluating process discipline can look at what matters in a CRM system for mortgage brokers and apply the same logic to lending operations. The goal isn't complexity. The goal is visibility, consistency, and low-friction follow-through.

A lean brokerage has a hidden advantage in tough markets. It doesn't need a huge monthly nut just to stay alive.

That matters for long-term profitability. When overhead stays controlled, commissions stretch further, reinvestment decisions improve, and the business can grow without losing the freedom that made the model attractive in the first place.

Build Your Profitable Brokerage Today

A borrower walks in convinced revenue is the problem. Ten minutes into the file, the underlying issue shows up. Overhead is eating the business alive, and nobody has sorted the numbers cleanly enough to explain it to a lender.

The skill behind better files and better businesses

That is why overhead matters so much in brokerage work. It is not just an accounting label. It affects whether a deal looks stable, whether margins hold up under underwriting, and whether your borrower sounds like an owner who understands their business.

The formula itself is straightforward: Overhead Cost = Indirect Materials + Indirect Labor + Indirect Expenses. The problem is classification. If a client lumps direct costs into overhead, the business can look less efficient than it really is. If they push indirect costs into direct production numbers, margins look stronger than they are, and the lender eventually sees the inconsistency.

Both mistakes hurt deals.

From the broker side, clean overhead analysis helps you build a tighter loan package. You can explain pressure on cash flow, show where margins can improve, and present the borrower as someone who has a handle on operations. From the business-owner side, the same skill protects your own brokerage. A home-based model can produce strong income because the overhead base stays low, but only if you keep recurring costs under control and avoid adding fixed expenses before volume supports them.

A practical next step

This is a strong business for people who want flexibility without carrying the weight of a traditional office setup. Referral-driven origination, remote operations, and disciplined expense control give a broker room to stay profitable through uneven months and still scale when deal flow improves.

I have seen this lesson pay twice. First, it helps brokers spot what is really happening inside a client's numbers and package the file accordingly. Second, it keeps their own operation from drifting into the same overhead problems they warn borrowers about.

Business Lending Blueprint shows everyday people how to launch and scale a business loan brokerage from home, serve business owners who need funding, and build a flexible, referral-driven income stream without unnecessary overhead. To see the full model, watch the free training from Business Lending Blueprint or schedule a strategy session to explore the next step.