A new broker usually runs into the same moment early. A client finds a property with upside, needs money fast, and the bank stalls, asks for more paperwork, or refuses the deal outright because the asset needs work. The client is frustrated, the closing window is shrinking, and the broker either solves the problem or loses the relationship.

That's why hard money matters. It isn't a fringe product. It's a practical funding tool for borrowers who need speed, flexibility, and asset-based underwriting. It's a sharp niche for anyone building a brokerage from home because the need is constant, the use case is clear, and the value a broker provides is easy to prove.

For aspiring entrepreneurs, this is bigger than learning one loan type. It's learning how to step into deals banks can't handle and become the person who knows where the money is, how the terms work, and how to package a file so it closes.

Table of Contents

- Your Client Needs Fast Funding Banks Cannot Provide

- What Exactly Is a Hard Money Loan

- Hard Money Loans vs Traditional Bank Loans

- Understanding the Real Costs and Typical Terms

- Common Borrower Use Cases and Key Risks

- The 5-Step Funding Process From Application to Close

- The Broker Opportunity Turning Deals Into Income

Your Client Needs Fast Funding Banks Cannot Provide

A real estate investor gets a contract on a distressed property. The opportunity is real. The spread looks attractive. The seller wants certainty and speed. Then the investor walks into a bank and gets hit with the usual problem: the timeline doesn't work, the property condition doesn't fit the box, and the underwriting process drags.

That is where a broker earns the fee.

Hard money solves a very specific problem. It gives borrowers a path when time matters more than perfect documentation and when the property itself is the reason the deal works. A beginner broker who understands this product stops sounding like an order taker and starts sounding like an advisor.

Why this matters to a broker

Hard money is not just about rescuing one deal. It's about becoming useful to clients that traditional institutions ignore.

- Investors need options: A borrower who can't wait on a conventional process still needs capital.

- Speed creates trust: When a broker produces a real solution under pressure, that client remembers it.

- One deal can become many: Investors, flippers, landlords, and small developers often need repeat financing.

Practical rule: The broker who can solve urgent funding problems becomes the broker who gets the next call first.

This niche also fits a broader funding business. A client who uses hard money today may need another product tomorrow. Someone bridging a property purchase might later need working capital, equipment financing, or even a receivables solution such as accounts receivable lending for cash flow gaps.

The real opportunity

A lot of new brokers make the same mistake. They chase only the easiest bankable files. That limits the business fast.

The stronger move is learning products that solve actual urgency. Hard money does that. It gives brokers a clear role in transactions where timing, property condition, and execution matter more than a polished tax-return package. That makes it one of the most practical niches for a beginner building a recession-resistant brokerage.

What Exactly Is a Hard Money Loan

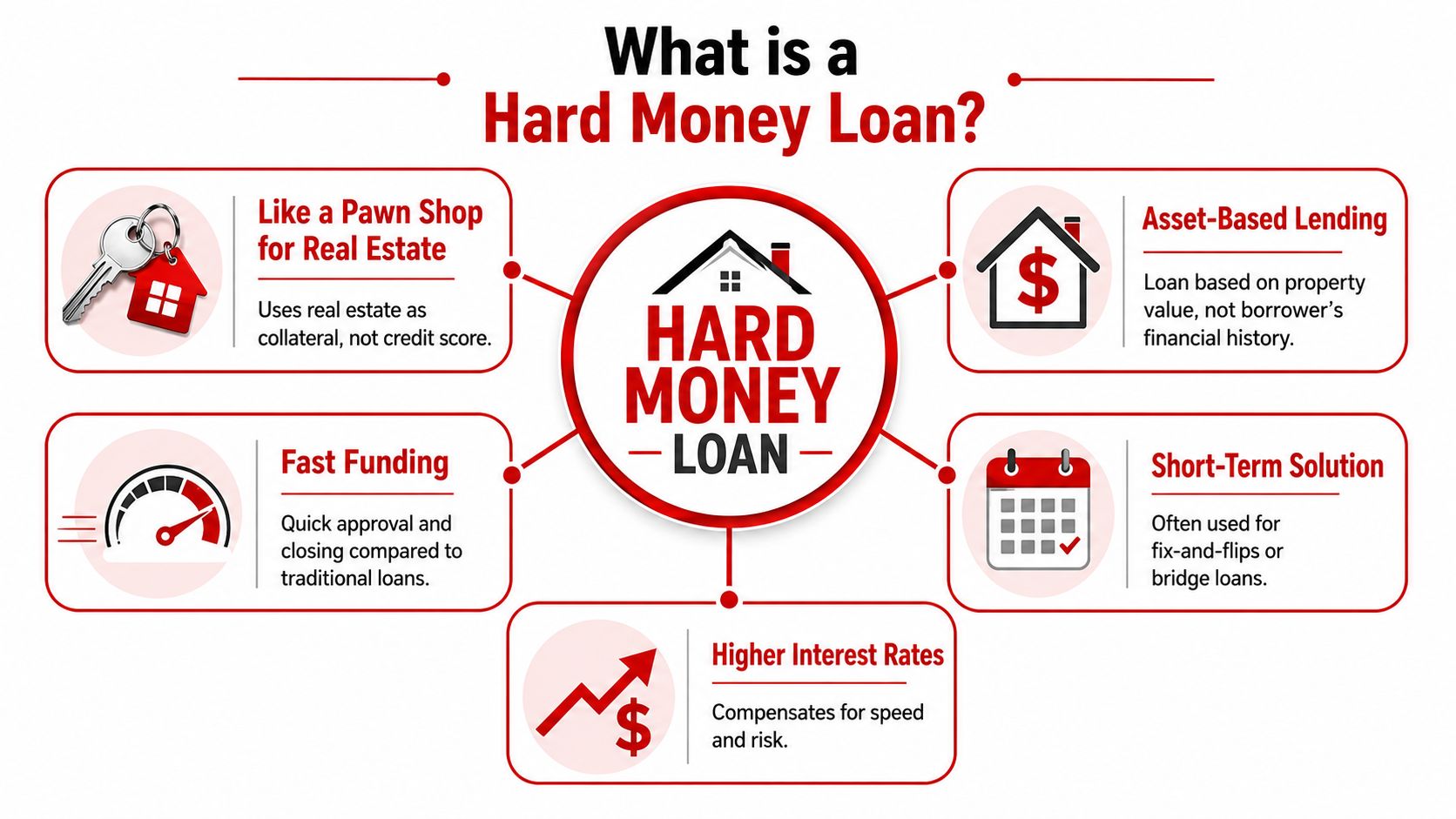

A hard money loan is best explained like this: it's a pawn shop model for real estate. The lender cares first about the asset. The property is the collateral, and the deal is underwritten around that collateral and the borrower's exit plan.

That simple framing helps beginners stop overcomplicating the product. Hard money isn't conventional mortgage lending with a different label. It's asset-based lending designed for short-term real estate transactions.

The simplest way to explain it

A bank usually asks, “Who is the borrower, what is their income, and how clean is the file?”

A hard money lender starts closer to, “What is the property worth, what could it be worth after repairs, and how does this loan get paid off?”

That distinction is the whole game. According to Herring Bank's hard money loan overview, hard money lenders commonly fund deals in 3 to 15 business days, while conventional financing often takes 30 to 60 days. The same source explains that approval is typically based on property value, with common loan-to-value ratios around 60% to 75% ARV/LTV, which means the borrower often needs roughly 25% to 40% equity or down payment.

For a broker, that means the conversation changes. The file is less about proving perfect borrower strength and more about proving the asset, the budget, and the payoff plan.

Why that structure creates speed

Hard money moves faster because the underwriting focus is narrower. The lender isn't trying to fit the deal into a broad consumer mortgage box. The lender is trying to answer a smaller set of practical questions:

- Is the collateral solid

- Does the rehab plan make sense

- Is there enough equity cushion

- Can the borrower exit through sale or refinance

That's why this product shows up often in fix-and-flip deals and bridge transactions. It also overlaps with creative capital stacking. Borrowers who want to understand how investors structure deals beyond bank financing can benefit from learning OPM strategies for real estate wholesalers.

Hard money is not “bad lending.” It's specialized lending for borrowers who need a fast, property-driven decision.

A broker who understands that distinction can explain the product cleanly, set expectations early, and avoid attracting the wrong borrowers. Anyone exploring adjacent real-estate funding models can also review how to start a mortgage lending company to see how different lending channels fit together.

Hard Money Loans vs Traditional Bank Loans

Borrowers don't choose hard money because it's cheaper. They choose it because the bank can't execute the deal that needs to happen now.

That's the message a broker must deliver with confidence. If a borrower compares hard money to a long-term owner-occupied mortgage and stops at rate, the conversation is already off track. The right comparison is usefulness, not just cost.

What borrowers actually care about

A borrower making an offer on a distressed property usually cares about five things.

First, approval logic. Banks are borrower-heavy. Hard money lenders are asset-heavy.

Second, timing. A fast close can be the reason the seller accepts the offer.

Third, property condition. A rough property can kill a conventional loan even when the deal itself is strong.

Fourth, term structure. Hard money is short-term capital built for transition, not permanent financing.

Fifth, flexibility. Many hard money lenders can work with unusual files that would stall in a traditional channel.

The right loan is the loan that closes the deal and matches the exit. The wrong loan is the one that looks good on paper but misses the window.

Borrowers dealing with more complex real-estate scenarios, including international transactions, may also benefit from broader context on understanding cross-border property loans.

Hard Money vs. Bank Loan At a Glance

| Feature | Hard Money Loan | Traditional Bank Loan |

|---|---|---|

| Approval focus | Primarily the property, collateral position, and exit strategy | Primarily borrower income, credit profile, documentation, and standard guidelines |

| Speed | Built for fast execution | Usually slower and more process-heavy |

| Property condition | Often used when the property needs work or doesn't fit bank standards | Better suited for stabilized, financeable properties |

| Loan term | Short-term bridge capital | Long-term financing |

| Payments | Often structured around short-term project execution | Usually built around long amortization |

| Flexibility | More adaptable to unusual deal structures | Less flexible, more standardized |

A broker should also know when the borrower belongs in a different product category. If the client is buying for cash flow rather than a quick reposition, underwriting metrics matter in a different way. That's where debt service coverage ratio calculation for investment properties becomes important.

Understanding the Real Costs and Typical Terms

Weak brokers lose trust. They quote a rate and act like they've explained the loan. They haven't.

A hard money borrower needs the full cost picture. That includes rate, points, term length, payment structure, loan-to-value ratio, and the practical effect of carrying the loan until the exit happens.

Where the cost really comes from

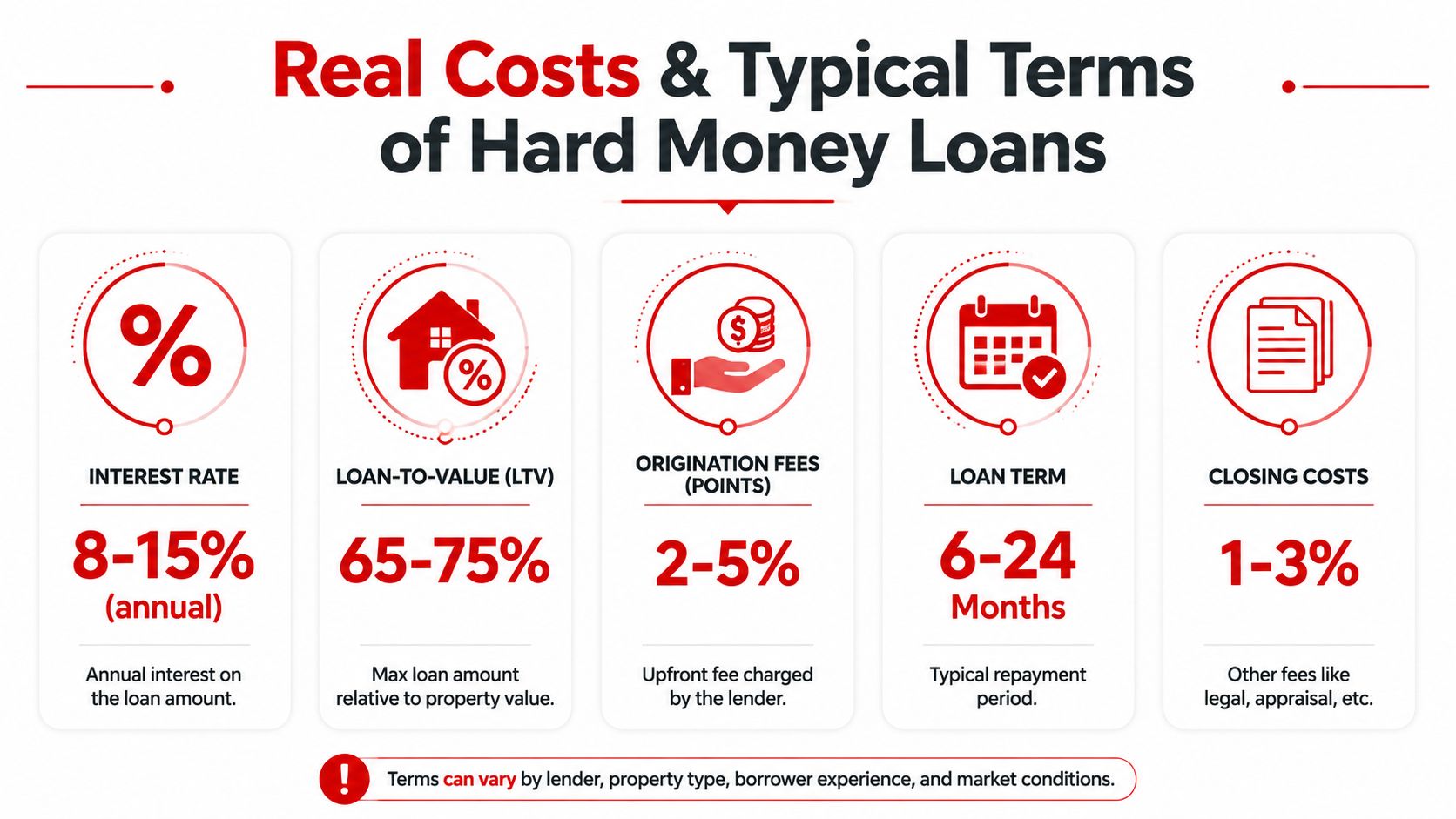

According to MortgageCalculator.org's hard money loan guide, current market guidance places hard money rates broadly around 8% to 18%, with fees commonly adding 1 to 5 points at origination. The same source notes that these loans are typically short-term, often 6 to 12 months, sometimes up to 36 months, and commonly use interest-only payments with a balloon payoff at maturity.

That structure changes how a broker should discuss affordability.

The borrower isn't buying a long runway. The borrower is renting speed. The lender gives quick access to capital, but the borrower must get in, execute, and get out. If the project drags, cost piles up fast.

Cost components a broker should discuss

- Interest rate: The annual borrowing cost is higher than conventional financing because the loan is short-term and risk-adjusted.

- Origination points: These are upfront fees charged at closing. They matter because they hit the project before any renovation progress is made.

- Balloon payoff: The principal usually isn't slowly amortized away. It comes due when the term ends.

- Loan-to-value: A smaller loan proportion means the borrower needs to commit more of their own funds to the transaction.

What a broker should model before submitting a deal

A clean hard money quote starts with the borrower's full capital stack, not just the note terms.

A broker should walk through:

- Cash needed at closing

- Planned rehab spend

- Monthly carry

- Expected sale or refinance path

- Time cushion if the project slips

Broker advice: If the borrower only asks about the rate, the borrower doesn't yet understand the loan.

Many new brokers quickly prove their worth. They don't need to be contractors or appraisers. They need to be disciplined enough to force a realistic conversation about cash in, cash out, and time. That's what protects the client and protects the file.

Common Borrower Use Cases and Key Risks

Hard money works best when the transaction has a short, clear purpose. It works poorly when the borrower is vague, undercapitalized, or hoping the market will rescue a weak plan.

That's why beginners need to know both sides of the product. The use cases are attractive. The risks are unforgiving.

Where hard money fits best

The most common fit is a property that needs to be bought and improved quickly. A borrower buys below market, renovates, then exits through sale or refinance.

Another fit is a bridge situation. A borrower needs short-term capital to move from one event to the next, such as acquiring a property before longer-term financing is in place.

Commercial situations can fit too, especially when the borrower needs speed and the property or timing doesn't line up with traditional underwriting.

These deals can work well because the loan is built around a transition. The property is changing condition, ownership, or financing status.

Where beginners get hurt

The biggest mistake is obsessing over the headline rate and ignoring total carry cost. According to Ridge Street Capital's discussion of hard money lenders for beginners, beginners should focus on total carry cost, with market examples showing 8% to 15% annual interest plus 1 to 5 points upfront, typical terms of 6 to 24 months, and a need for a strong exit plan through resale or refinancing.

The danger is simple. If the rehab runs long, the listing sits, or the refinance falls apart, the maturity date doesn't care.

Common risk points include:

- Weak renovation planning: Borrowers underestimate scope, time, or contractor issues.

- Thin reserves: The project looks fundable until unexpected costs hit.

- Bad exit assumptions: The borrower assumes a quick sale or easy refinance without enough margin.

- Overpaying on the purchase: A bad buy cannot be fixed by fast money.

A hard money loan can forgive an imperfect borrower. It does not forgive an imperfect exit.

A responsible broker should reject weak deals, not force them through. That protects reputation, lender relationships, and future referrals.

The 5-Step Funding Process From Application to Close

A smooth hard money transaction is rarely accidental. Someone has to control the flow of information, set expectations, and keep the lender focused on the strengths of the file. That someone is usually the broker.

The process is fast, but only if the file is clean and the lender fit is right.

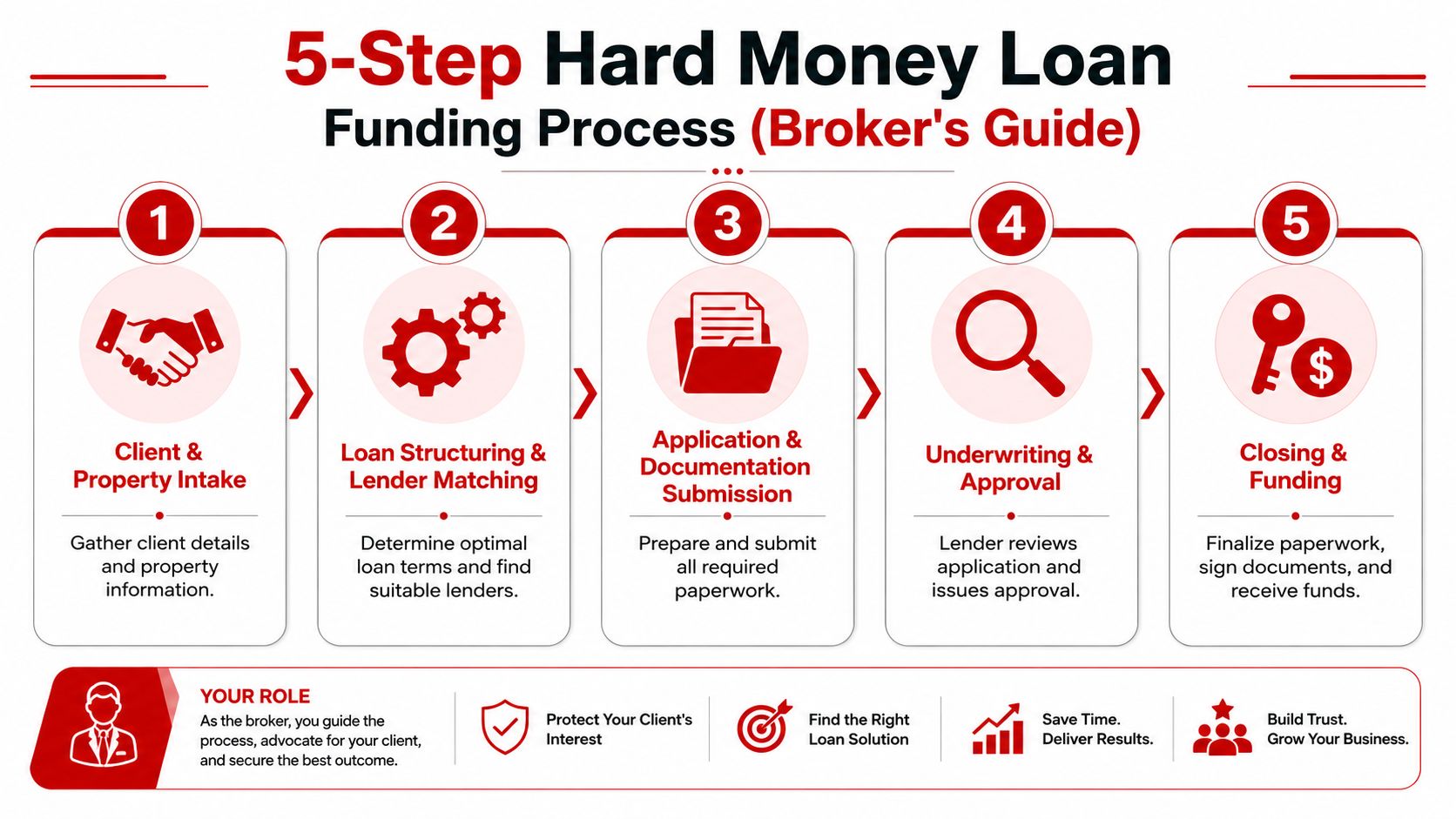

Step 1 through Step 3

Step 1 is intake.

The broker gathers the basics: purchase contract, property details, renovation scope, borrower liquidity, entity information, and exit strategy. If any of those pieces are fuzzy, the file is not ready.

Step 2 is lender matching.

This matters more than beginners think. According to FCTD's overview of different hard money lender types, the market includes local private lenders, mortgage funds, and nationwide lenders, with terms varying widely. Some require 20% to 30% down, while others may offer up to 75% to 90% LTV/ARV. The best lender is the one whose niche fits the deal.

Step 3 is submission.

The broker packages the file clearly. The lender should be able to understand the property, requested terms, borrower contribution, and exit path without chasing scattered documents.

Step 4 and Step 5

Step 4 is underwriting and term sheet review.

The lender reviews the collateral and structure, then issues terms if the deal fits. A broker's real value is earned by spotting issues before the borrower signs something poorly understood.

Step 5 is closing and funding.

Title, insurance, closing documents, and final conditions all have to move fast. A broker who stays organized can help prevent a last-minute collapse.

A practical workflow looks like this:

- Get the story straight early: If the borrower changes the plan every two days, the lender loses confidence.

- Submit complete documents: Missing items create unnecessary delay.

- Match before shopping: Sending a rehab-heavy file to a lender that prefers light cosmetic deals wastes everyone's time.

- Review the exit realistically: If the payoff plan is weak, the term sheet won't save the deal.

This is why hard money brokering can become a real business. The broker isn't just forwarding an application. The broker is structuring, filtering, and guiding the transaction from first call to funded loan.

The Broker Opportunity Turning Deals Into Income

A new investor calls on Tuesday. The property is good, the seller wants a fast close, and the bank timeline kills the deal. If you can step in, explain the loan in plain English, and get the file to the right lender, you are no longer just "helpful." You are the person who kept the transaction alive and got paid for doing it.

Hard money is not only a financing product. It is a brokerage business model with clear demand, fast feedback, and strong referral potential. New brokers should pay attention to that. You do not need a large office, a giant team, or years in banking to start. You need judgment, process, lender relationships, and the discipline to qualify deals before they waste your time.

Why this niche works for a home-based broker

Hard money brokering fits a remote model because the job is built on conversations, deal screening, file packaging, lender matching, and follow-up. That work rewards organization more than overhead.

The opportunity is attractive for several reasons:

- Repeat business: Real estate investors rarely stop after one successful project.

- Natural referral partners: Realtors, contractors, attorneys, and accountants regularly meet clients who need speed and flexible underwriting.

- Low fixed overhead: A disciplined broker can build a serious operation from a home office with systems and lender contacts.

- Expansion potential: A borrower who starts with hard money often needs other funding later, which creates more income per relationship.

Anyone building pipeline in this niche should study both referral strategy and lead flow. A useful outside reference is this broker's 2026 guide to loan leads, which outlines how brokers attract deal opportunities through relationships and targeted outreach.

How to build around referral relationships

Many new brokers stall because they keep studying and never start. That is a mistake. Start by becoming known for one thing: getting investor deals placed with speed and clarity.

Build the business in a simple sequence:

- Master the pitch: Explain hard money terms, pricing, risks, and exit plans without jargon.

- Build a lender bench: Keep options for different property types, borrower profiles, and deal structures.

- Own the intake process: Ask better questions early so weak files do not clog your pipeline.

- Win referral trust: Stay in front of investor-friendly professionals and update them consistently.

- Work the relationship after closing: One funded deal should lead to the next deal, plus introductions.

Income follows competence. Brokers who screen well, communicate clearly, and protect borrowers from bad lender fits get repeat clients faster than brokers who chase every inquiry. If you want a clearer picture of earnings across this business model, review business loan broker salary and revenue mechanics.

Hard money is one of the best entry points for an aspiring broker because the client problem is urgent and easy to understand. The borrower needs speed. The bank cannot deliver it. You bring a workable path, manage the process, and turn that skill into a referral-driven business with low overhead and room to grow.