A new broker usually meets this client early. The company is busy, the owner sounds confident, sales are coming in, and invoices are stacked. On paper, it looks healthy. In the bank account, it looks tight.

That tension is where many strong funding relationships begin. A business can deliver work, wait on net terms of 30 to 90 days, and still struggle to cover payroll, inventory, or suppliers while customers take their time to pay, which is exactly why invoice factoring became such an important working-capital tool for small businesses according to Paychex's explanation of invoice factoring.

For a broker, that matters because invoice factoring for small business isn't just another product on a menu. It's a practical fix for a very specific pain point, and clients feel that difference fast when it's positioned correctly.

Table of Contents

- Your First High-Value Client Solution

- How Invoice Factoring Solves Your Client's Cash Flow Gap

- Identifying the Perfect Client for Invoice Factoring

- Mastering the Costs and Benefits to Close Deals

- Factoring vs Other Funding in Your Broker Toolkit

- From Application to Commission A Broker's Process

- Become the Go-To Funding Expert in Your Network

Your First High-Value Client Solution

A common scenario looks like this. A staffing firm lands new business, submits invoices on time, and keeps hearing the same thing from customers: payment is coming through normal terms. The owner isn't short on revenue. The owner is short on timing.

That distinction is where inexperienced brokers miss the deal. They hear “cash flow problem” and immediately think term loan, line of credit, or a product that forces the client into debt-service pressure. A stronger broker hears “slow-paying invoices” and starts asking who the customers are, how the invoices are structured, and whether receivables can be turned into immediate working capital.

Practical rule: When the business is performing but cash is trapped in receivables, the broker should think about the invoice first, not the owner's stress level.

This is why invoice factoring for small business can become one of the first valuable solutions in a broker's toolkit. It solves a problem owners understand instantly. They already did the work. They already earned the revenue. They just haven't collected it yet.

What makes this a broker opportunity

Factoring is easier to position when the broker talks in business terms instead of finance jargon. The business owner doesn't care about textbook definitions. The owner cares about making payroll on time, taking the next order, buying materials, and avoiding the embarrassment of saying yes to sales but no to growth.

A broker who can diagnose that gap becomes more than a rate shopper. That broker becomes the person who saw the bottleneck.

That creates two advantages:

- The client sees immediate relevance. This isn't abstract capital for some vague future use. It's cash tied directly to work already completed.

- The broker opens recurring conversations. Once a client understands one funding solution that fits operations, they're far more likely to come back for the next one.

What works and what doesn't

What works is leading with the business problem. What doesn't work is opening with product terminology and fee talk before the client sees the value.

A weak pitch sounds like financing. A strong pitch sounds like relief.

Good brokers don't sell factoring as a clever product. They present it as a way to stop profitable companies from getting squeezed by their own payment terms.

That mindset matters because the highest-value clients rarely need hype. They need clarity. When a broker gives them that, closing gets easier and referral relationships get stronger.

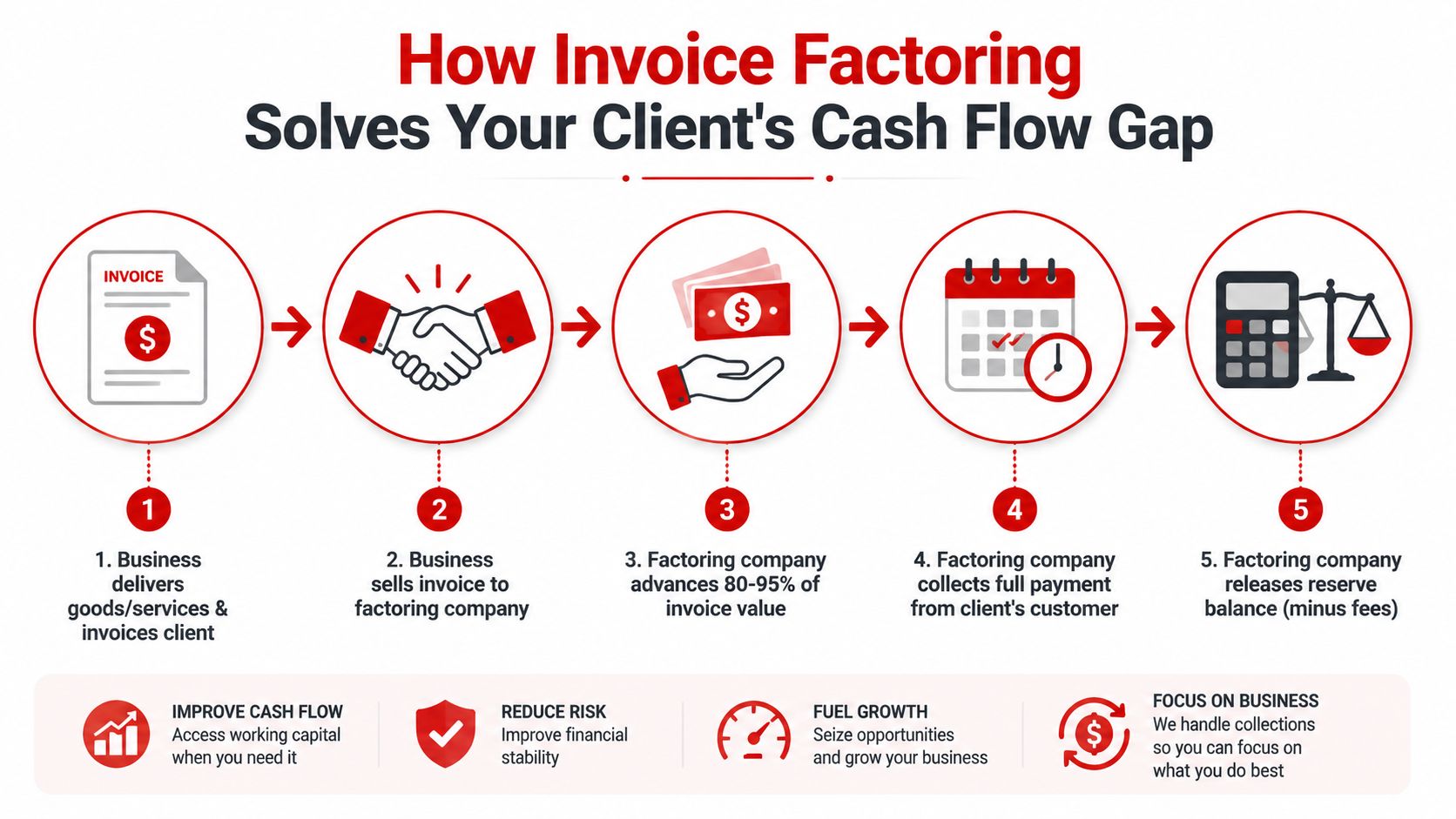

How Invoice Factoring Solves Your Client's Cash Flow Gap

A client finishes a job on Tuesday, sends the invoice on Wednesday, and still cannot cover payroll next week because the customer pays on net 45. That is the cash flow gap a broker is solving.

The clean explanation is simple. Factoring lets the business turn completed, billed work into usable cash before the customer's payment cycle ends. For a broker, that matters because the conversation becomes easier to close when the owner sees a direct line between one unpaid invoice and one immediate operating need.

For clients who want a broader plain-English breakdown of accounts receivable factoring, that resource can reinforce the concept without drowning them in lender language.

Clients usually grasp it fastest when they see the timing difference in plain terms:

| Business situation | Without factoring | With factoring |

|---|---|---|

| Work is complete | Revenue is earned but not yet available for spending | Part of that revenue is made available early |

| Bills are due now | Owner waits for customer payment | Owner uses the advance for operations |

| Growth opportunity appears | Business may delay the next step | Business has working capital to act |

The point is timing. Factoring does not create profit. It changes when the business can use cash tied up in receivables.

That distinction helps close deals.

Owners who misunderstand factoring often compare it to a term loan and get stuck on rate alone. A broker should bring them back to the operating question: what does waiting 30, 45, or 60 days cost this business right now? If the delay means missing payroll, slowing production, passing on a large order, or stretching vendors, the value becomes concrete.

A broker-friendly way to explain the process

Keep the walkthrough practical and tied to the invoice.

- The client completes the work and issues the invoice. The receivable needs to reflect delivered goods or finished services, with clean backup documents.

- The broker places the deal with the right factor. Strong customer credit, clear terms, and organized paperwork usually improve approval odds.

- The factor advances funds against the invoice. The client gets access to part of the invoice value before the customer pays.

- The customer pays the factor under the invoice terms. Payment goes through the assigned collection process.

- The remaining balance is sent to the client, minus fees. That final settlement closes the transaction.

Brokers who want a clearer sense of which funding sources focus on receivables can review these accounts receivable lenders and funding programs.

A good explanation also includes the friction points. Deals slow down when invoices are disputed, proof of delivery is missing, purchase orders do not match, or the customer has a weak payment record. Those are not minor details. They are often the difference between a file that funds quickly and one that dies in underwriting.

This is why factoring can be a strong commission product for a broker who knows how to package the deal. You are not selling abstract capital. You are presenting a finance company with a receivable, a payer, and a business reason the advance makes sense now. That clarity helps the client get funded and helps the broker build repeatable revenue.

Identifying the Perfect Client for Invoice Factoring

The fastest way to waste time in this category is to treat every cash-strapped business as a factoring prospect. Not every business has the right receivables profile, and not every owner should be steered into this option.

The key structural point is that invoice factoring is a sale of accounts receivable, not a loan, and underwriting often centers on the credit quality and payment behavior of the invoice debtor rather than the business itself, as explained by OnDeck. That single idea changes how a broker qualifies the deal.

Green flags that usually lead to real opportunity

The strongest candidates tend to share a few traits. They bill other businesses, they issue clear invoices, and their customers pay, even if they pay slowly.

A broker should look for these signs early:

- B2B receivables: Factoring fits best when the client invoices businesses, not scattered consumer accounts.

- Completed work: The invoice should represent delivered goods or finished services, not projected work.

- Recognizable payment process: The client knows how customers approve invoices, who pays them, and what documentation buyers require.

- Stable customer base: A handful of repeat commercial buyers is easier to underwrite than random one-off customers.

- Operational need, not chaos: The business needs timing help, not rescue from constant disputes, chargebacks, or bad bookkeeping.

This is also why basic financial literacy matters in client conversations. Some owners still blur the line between what the business owns and what it owes. A simple guide to what are assets and liabilities can help newer clients understand why receivables are valuable and how that value can support funding.

For brokers building a broader receivables strategy, this overview of accounts receivable lenders helps frame where factoring fits among adjacent products.

Red flags that waste time

Some files look promising until the details come out. Then the deal falls apart for reasons that were visible from the first call.

Watch for these issues:

- Disputed invoices: If the customer may challenge the bill, the receivable isn't clean.

- Poor documentation: Missing purchase orders, weak backup, or sloppy invoicing creates avoidable friction.

- Highly concentrated customer risk: If one buyer drives almost everything and pays unpredictably, the deal may become fragile.

- Consumer-heavy billing: Small retail invoices usually don't fit the typical factoring profile.

- Owner confusion about collections: If the owner can't explain who pays, when they pay, or why they delay, the broker doesn't have enough to work with.

A broker should qualify the customer as carefully as the client. In factoring, the end payer often tells the real story.

The best prospects aren't always the businesses with the loudest urgency. They're the ones with receivables that can stand up to scrutiny. That difference protects time, improves close rates, and keeps brokers focused on fundable deals.

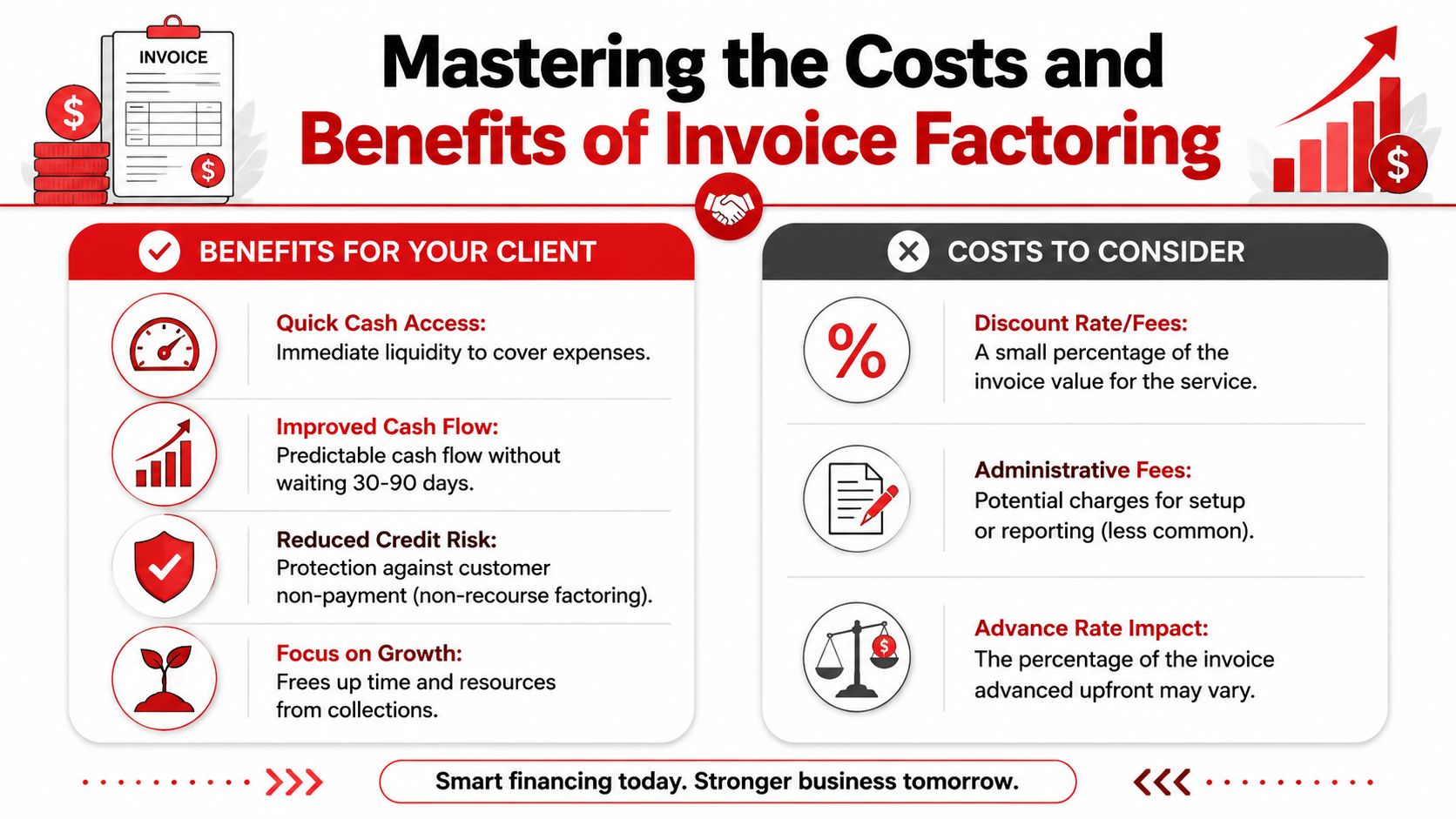

Mastering the Costs and Benefits to Close Deals

A deal often turns on one hard question.

The owner looks at the fee sheet and says, “Why should I pay to get my own money early?” If a broker answers that poorly, the file stalls. If the broker answers it with context, numbers, and business consequences, the client usually sees the product differently.

The right frame is speed and opportunity, not ownership. The client is not paying because the invoice lacks value. The client is paying to turn a slow-paying receivable into working capital now, while payroll, materials, freight, and growth decisions still matter.

How to frame the cost without sounding defensive

Keep the explanation simple. Factoring cost usually depends on the advance rate, the fee structure, how strong the end customer is, and how long the invoice stays unpaid. The longer the customer takes to pay, the more the capital costs.

Good brokers do not stop at “here is the fee.” They translate that fee into a business decision the owner already understands.

Use questions like these:

- What does a delayed payroll week cost in morale and distraction?

- What margin is lost when the client cannot buy inventory or materials on time?

- How much revenue slips when the business has to pass on new work because cash is trapped in receivables?

- What happens if the owner keeps spending hours managing collection timing instead of selling and operating?

That is the sales conversation. A factoring fee should be weighed against the cost of waiting, not against the fiction that delayed cash is free.

I tell newer brokers to make one point very clear. Factoring is expensive capital if the client uses it to cover a broken business model. It can be very reasonable capital if it helps a healthy business bridge a timing gap created by slow-paying commercial customers.

That distinction helps close deals and protects your reputation.

For clients comparing factoring with term debt or a line, this guide to debt service coverage ratio calculation for business financing helps explain why a company can have real revenue and still struggle to qualify for scheduled-debt products.

Objections that need a real answer

Customer contact is usually the first objection. Owners worry that a factor will collect too aggressively, confuse the account debtor, or make the business look stressed.

That concern should be addressed directly. The process does affect how payments are handled, so the broker needs to explain who contacts the customer, what notices are sent, and how disputes or short pays are managed. A practical explanation matters more than reassurance.

A useful response sounds like this:

“Your customer will notice the payment instructions. What matters is whether that interaction is handled professionally, with clear documentation and no surprises.”

The second objection is dependency. Some clients want factoring to solve every cash problem. That is where broker judgment shows up.

If the company has weak margins, chronic billing errors, loose collections, or pricing that never leaves enough room for cash buildup, factoring may buy time but it will not cure the problem. Say that plainly. Clients trust brokers who can separate a timing issue from a structural issue.

There is also a closing angle many brokers miss. Cost objections often soften once the owner sees the revenue side. If access to cash helps the client fulfill larger orders, start jobs faster, or stop turning away work, the fee becomes easier to defend because the capital produced a result.

That is how experienced brokers present factoring. They do not apologize for the cost. They show the client what the cost buys, where the product fits, and where it does not. That approach improves close rates and leads to better repeat referral relationships.

Factoring vs Other Funding in Your Broker Toolkit

The broker who understands only one product becomes a salesperson. The broker who knows when not to use that product becomes an advisor.

Invoice factoring for small business is powerful when the issue is trapped receivables. It becomes a poor recommendation when the problem is broader, longer-term, or unrelated to invoicing.

When factoring is the better fit

Factoring usually wins when the client has commercial invoices, cash pressure today, and limited appetite or ability for another scheduled debt obligation.

A few examples make that clearer:

| Scenario | Better fit | Why |

|---|---|---|

| The client has slow-paying business customers and completed invoices | Factoring | It monetizes receivables already earned |

| The client needs capital that can scale with sales volume | Factoring | More invoices can support more availability |

| The client is weak on traditional bank-style underwriting but serves solid commercial buyers | Factoring | The payer profile matters heavily |

The strategic comparison should stay grounded in opportunity cost. The broker's job is to help the owner decide whether the fee is cheaper than delayed hiring, missed jobs, stalled payroll, or the inability to accept new work, which is the framing emphasized by Paro.

When another product should win

Some clients need flexibility that isn't tied to invoices. Others need capital for a purpose that doesn't line up with completed receivables.

That usually points elsewhere:

- Line of credit situation: The client wants ongoing access to working capital for mixed business needs and has the profile to support a revolving facility.

- Purchase order situation: The client needs funds to fulfill new orders before invoicing can happen.

- Revenue-based financing situation: The business has strong incoming revenue patterns but not the receivables structure that factoring requires. For that use case, this explanation of what is revenue-based financing helps clarify the distinction.

The best recommendation isn't the one that closes fastest. It's the one the client can still defend six months later.

Trust compounds in such scenarios. If the broker says, “Factoring isn't your best move,” the client starts listening more closely when the broker later says, “This one is.”

That credibility creates longer referral chains than aggressive selling ever will.

From Application to Commission A Broker's Process

A broker usually earns this commission before the file funds. It happens in the client call where the owner says, "I sent the invoices, so why is this taking so long?" The answer is almost never the product itself. It is usually the paperwork, the customer profile, or a missed expectation that should have been handled on day one.

That is why strong brokers treat factoring submissions like deal management, not document forwarding.

What to collect before submission

A fundable file tells a clear story. The business delivered real work, billed a creditworthy customer, and can prove both without a scavenger hunt through email threads and spreadsheets.

Start with the documents that let the factor underwrite fast:

- Accounts receivable aging: This shows what is open, how long it has been outstanding, and whether the client has a concentration issue with one customer.

- Sample invoices: The factor needs to see whether the invoices are clear, consistent, and tied to completed work.

- Customer list: The end customers matter as much as the client in many factoring approvals.

- Bank statements: These help confirm operating activity and show whether cash pressure is temporary or chronic.

- Delivery confirmations, signed tickets, or service proof: Funding gets easier when completion is documented cleanly.

Messy support slows everything down. It can also expose a deeper problem. If the client cannot produce clean invoice records, collection records, or backup for fulfilled work, the broker should address that before promising a quick close. Better systems for efficient invoice data extraction can reduce repeat friction and make future submissions much easier to package.

I also want a basic picture of existing obligations before I pitch terms too hard. A broker who understands the client's current payments, liens, and debt stack can avoid ugly surprises in underwriting. This quick guide on how to read a debt schedule before packaging a file is useful for newer brokers who need a cleaner pre-submission process.

How the broker keeps the deal moving

The broker sets the tempo.

A practical process usually looks like this:

- Confirm the actual funding trigger. Late-paying receivables should be the bottleneck. If the business has margin problems, disputes, or unstable operations, factoring may not fix the issue.

- Clean the package before submission. Missing invoice support, unclear aging, and inconsistent customer names create avoidable underwriter questions.

- Explain pricing in plain language. The client should know there is an advance rate, a fee structure, and a final cost that changes with debtor quality, invoice size, and how long the customer takes to pay.

- Prepare the owner for customer verification and notice steps. Resistance often shows up here, especially if the client never expected their customers to hear from a funding company.

- Stay involved through approval and activation. Brokers who answer questions quickly, chase missing items, and keep the owner engaged fund more deals.

Clean submissions close faster than excited submissions.

That line matters because many new brokers try to sell energy when the file needs discipline. The owner does not care how enthusiastic the broker sounds if underwriting is stalled for three days over unsigned invoices or unverified delivery.

The commission opportunity is in repeatable execution. A broker who qualifies fit, collects the right support, sets expectations early, and manages communication well will usually get funded more often and get referred more often. One successful factoring file can open the door to the owner's next need, and to other businesses in the same network that are dealing with the same cash gap.

Become the Go-To Funding Expert in Your Network

Invoice factoring for small business gives brokers something valuable very early in their career. It gives them a way to solve a painful, urgent problem for companies that are doing real business but waiting too long to get paid.

That matters because many owners don't need a lecture on capital structure. They need a broker who can recognize when receivables are the bottleneck, explain the trade-offs transparently, and guide the file from confusion to funding. When that happens, the broker stops sounding like a marketer and starts sounding like a trusted resource.

This product also fits the kind of business many aspiring brokers want to build. It can be run remotely, referred through professional relationships, and repeated across industries where B2B invoicing creates constant working-capital pressure. The commission opportunity comes from being useful, not flashy.

The strongest brokers build their reputation one solved problem at a time. Factoring won't fit every deal, and that's exactly why learning to position it correctly matters. It sharpens judgment. It improves client conversations. It creates referral trust that supports a broader funding practice over time.

Business Lending Blueprint shows aspiring brokers how to build that kind of funding business with practical training, lender access, and a model built for remote, flexible work. To learn how to package deals, understand products like invoice factoring, and build a referral-driven brokerage, watch the free training at Business Lending Blueprint or schedule a strategy session.