A lot of people search for business loan broker salary when they're tired of a fixed paycheck and trying to figure out whether this path is a real business or just another commission-heavy sales role. That question makes sense. Most career moves start with income. But in this field, the better question isn't only “What does it pay?” It's “What kind of income model am I stepping into?”

A business loan broker doesn't usually operate like a salaried employee with predictable annual raises. The role works more like a real estate agent's model. Some positions offer a base plus incentive pay, but many brokers earn based on funded deals. That changes everything. Income is tied to pipeline, lender fit, follow-up, referral relationships, and the ability to move files from application to closing without wasting time.

That also means the ceiling and the learning curve both look different. Someone exploring building a six-figure business from home as a business loan broker isn't really evaluating a typical job slot. They're evaluating a business model with low overhead, flexible location, and direct upside tied to execution.

Many newcomers commonly get tripped up. They focus on the word “salary” and miss the structure behind the number. The people who do well in this space don't chase random leads and hope for approvals. They build systems, learn products, create referral channels, and become useful to business owners who need capital.

Table of Contents

- Introduction Decoding Your True Earning Potential

- The Two Core Business Loan Broker Compensation Models

- Typical Business Loan Broker Salary Ranges

- Sample Earning Scenarios How a Deal Turns into a Paycheck

- Key Factors That Directly Influence Your Income

- Proven Strategies to Boost Your Broker Earnings

- Conclusion Your Path to a Six-Figure Broker Business

Introduction Decoding Your True Earning Potential

Searching for business loan broker salary usually means a person wants clarity, not hype. They want to know whether this is a side income, a full-time replacement, or a serious long-term business. The honest answer is that it can be any of the three, depending on how the broker chooses to operate.

Salary mindset versus business mindset

There are two broad ways people think about compensation in this industry. The first is employee logic. That person wants a set income, predictable hours, and a narrow role. The second is owner logic. That person wants more control, accepts variable income early on, and builds a process that can grow.

Business loan brokering rewards the second approach more often.

A fixed salary limits upside but feels safe. A commission model can feel less certain at the beginning, but it creates a direct connection between effort, skill, and payout. That's why the word “salary” only tells part of the story here.

A better way to evaluate this field is to ask how quickly a broker can build repeatable deal flow, not just what a company might put on an offer letter.

Why the model matters more than the label

In a traditional finance role, income often climbs slowly. In a brokerage model, income can rise when the broker improves lead quality, lender matching, speed, and referral consistency. That makes this field attractive to people who want remote work, flexible hours, and an income path that isn't locked to a pay band.

That doesn't mean easy money. It means direct accountability. Brokers who treat it like a real business tend to create better outcomes than those who wait for a salary to carry them.

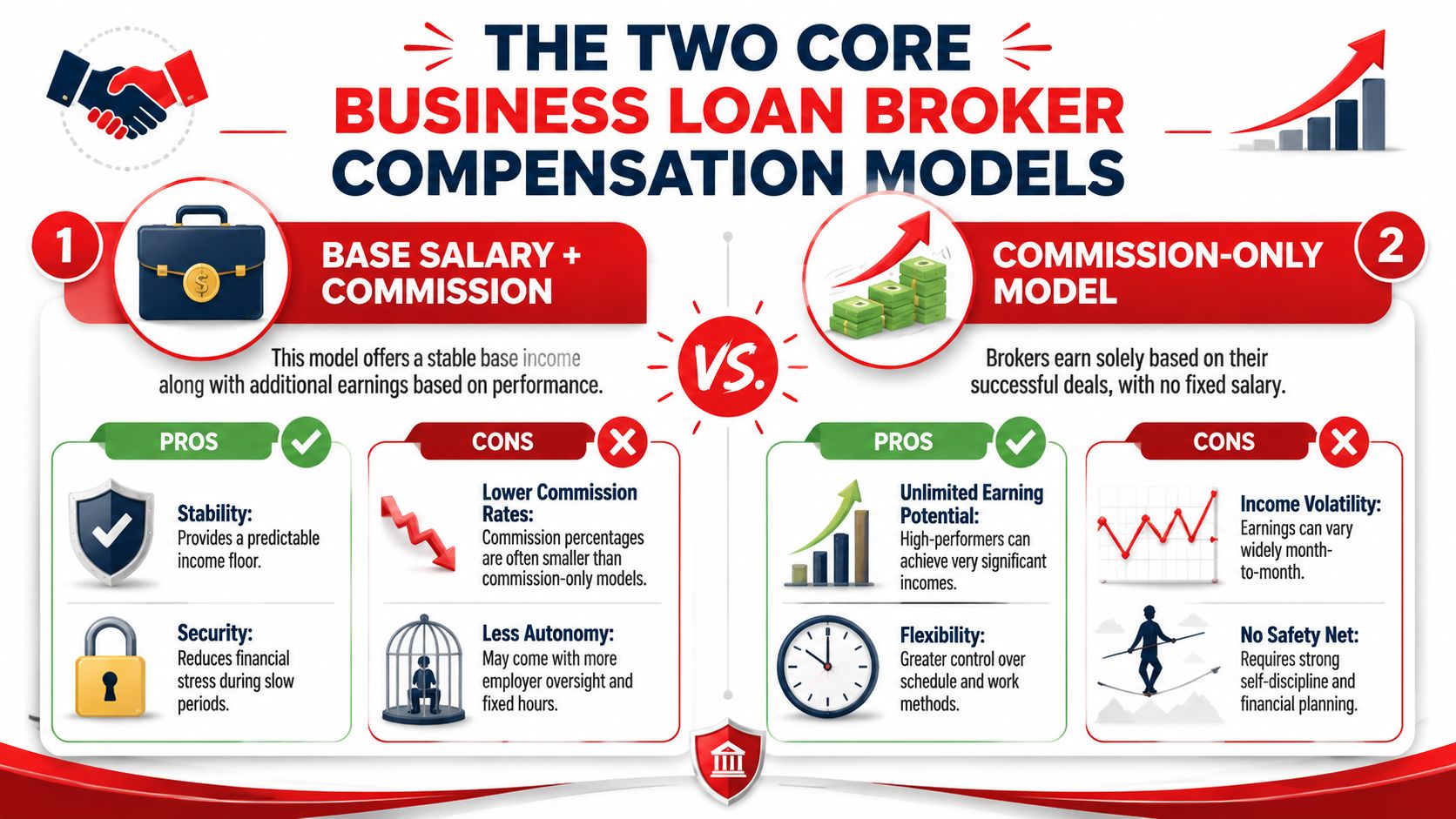

The Two Core Business Loan Broker Compensation Models

Business loan brokers generally get paid in one of two ways. Understanding the difference matters because each model creates a different lifestyle, risk level, and growth path.

Base salary plus commission

This model is more common inside established firms. The broker receives a fixed paycheck and may also earn bonuses or commissions on funded deals. It appeals to people who want structure and a financial floor while they learn.

The trade-off is straightforward. The employer often controls lead distribution, schedule, process, and payout structure. A broker may have less freedom to choose niche, messaging, and workflow. Commission percentages can also be less attractive because the company is absorbing overhead and paying a base.

For someone transitioning from banking, insurance, or another professional services role, this can be a gentler entry point. But it usually doesn't offer the same entrepreneurial upside as an independent model.

Commission only

This is the model many independent brokers prefer. The broker earns when a deal funds. No fixed paycheck. No automatic safety net. More responsibility, but more flexibility.

That structure creates income dispersion. ZipRecruiter salary data for business loan brokers reports an average of $25.97 per hour, with the middle range at $17.31 to $30.05 per hour and an observed span from $16.11 to $67.55 per hour. That spread shows why this isn't a normal wage story. Performance, deal flow, and efficiency matter far more than time on the clock.

Practical rule: If a broker depends on random inbound inquiries, commission-only pay feels unstable. If a broker builds repeatable lead sources and manages files well, the same model becomes far more attractive.

A commission-only broker also has more room to shape the business. They can work from home, build referral partnerships, specialize in products, and create a process that doesn't rely on a manager assigning leads.

For readers considering the independent path, a solid starting point is learning how to become a loan broker and start a lending business. The income model makes more sense once the business structure is clear.

Which model fits which person

The best model depends on temperament more than title.

- Base plus commission fits someone who values predictability, wants coaching inside a company, and prefers lower short-term volatility.

- Commission-only fits someone who wants control, can handle delayed gratification, and is willing to build systems instead of waiting for leads.

- Hybrid transitions fit professionals who start cautiously, then move toward independence once they understand products and closing mechanics.

Neither model is automatically better. But for people attracted to freedom, scalability, and home-based income, commission-only brokering is often the closer match.

Typical Business Loan Broker Salary Ranges

A realistic look at business loan broker salary has to separate broad labor data from broker-specific upside. The broad number gives a baseline. The broker-specific number shows what can happen when income is tied to funded volume.

The baseline and the upside

The U.S. Bureau of Labor Statistics reports that loan officers had a median annual wage of $74,180 in May 2024, with employment projected to grow 2% from 2024 to 2034 and about 20,300 openings per year on average, as shown in the BLS loan officer outlook. That's useful because it places lending work in a stable finance category, not a hype-driven occupation.

Specialized broker compensation can look very different. In a business-loan-focused context, Capital Gurus' overview of broker pay cites commissions commonly ranging from 1% to 5% of the loan amount and includes a market estimate of $144,472 per year as an average U.S. business loan broker salary. That gap exists because funded volume changes the math fast.

What these ranges mean in practice

A person entering this field part-time shouldn't read the higher figure as an automatic expectation. Early income usually reflects three things:

- Whether leads are qualified.

- Whether the broker understands lender fit.

- Whether there is a repeatable referral engine behind the pipeline.

Someone with weak lead flow can stay stuck even with strong product knowledge. Someone with good referral partners and disciplined follow-up can gain traction much faster.

The phrase “business loan broker salary” can be misleading because many of the best earners aren't earning a salary at all. They're earning commissions through a structured brokerage process.

A simple way to think about income bands

Rather than focusing on titles, it helps to think in operating stages.

| Broker stage | What income usually depends on | Typical reality |

|---|---|---|

| Early-stage broker | Learning products, getting first submissions, handling objections | Income is uneven because the pipeline is still being built |

| Developing broker | Better lender matching, better scripts, referral momentum | Earnings become more predictable as funded files repeat |

| Established broker | Consistent referral sources, specialization, operational discipline | Income can outpace broader lending benchmarks because volume compounds |

This is why raw averages never tell the full story. Two brokers can work similar hours and produce very different income because one has a system and the other has activity without structure.

Why some brokers plateau

Plateaus usually don't happen because the opportunity disappears. They happen because the broker stays in reactive mode. They chase every borrower, submit weak files, rely on one marketing tactic, or fail to build partner relationships that send repeat business.

The opposite approach is much steadier. A broker picks a lane, builds trust with referral partners, understands a few products thoroughly, and turns each funded deal into future introductions.

Sample Earning Scenarios How a Deal Turns into a Paycheck

Commission becomes easier to understand when the math is visible. In this business, the payout is tied to funded volume, which is why deal selection matters as much as effort.

What a funded file can produce

Industry guidance commonly places broker commissions in the 1% to 5% range of the loan amount, and a single $100,000 deal could produce roughly $1,000 to $5,000 in broker compensation, as noted earlier in the linked salary range source. That doesn't mean every deal lands at the high end. It means the loan amount and fee structure directly affect payout.

Here is a straightforward way to visualize it.

| Deal Type | Loan Amount | Commission Rate | Broker Payout |

|---|---|---|---|

| Small working capital deal | $100,000 | 1% | $1,000 |

| Mid-sized business financing deal | $100,000 | 3% | $3,000 |

| Larger funded deal | $100,000 | 5% | $5,000 |

These examples use the same loan amount on purpose. They show that commission structure alone changes the outcome, even before loan size increases.

Why one broker closes more value from the same leads

The key lever isn't only the rate. It's how the broker handles the file.

A broker who pre-qualifies well tends to waste less time. A broker who knows how to position a borrower for the right product tends to move the deal faster. A broker who understands product categories, including options like revenue-based financing, can often match a business owner to a more suitable path instead of forcing one solution onto every file.

That matters because not all applications deserve the same time investment.

The payoff isn't random

Many beginners think commission income is unpredictable by nature. It isn't random. It's the result of a sequence.

- Lead quality comes first. Weak inquiries create false hope and long follow-up cycles.

- Pre-qualification protects time. A clean intake process filters out deals that shouldn't move forward.

- Product fit drives funding. Good brokers don't just “submit.” They place deals intelligently.

- Follow-up saves commissions. Many files don't die because of lender rejection. They die because the borrower goes silent and the broker doesn't manage momentum.

A funded deal is usually the outcome of a well-run process, not a lucky conversation.

That shift in thinking changes how a person sees business loan broker salary. The question stops being “What does the role pay?” and becomes “How many good files can the broker move through a reliable system?”

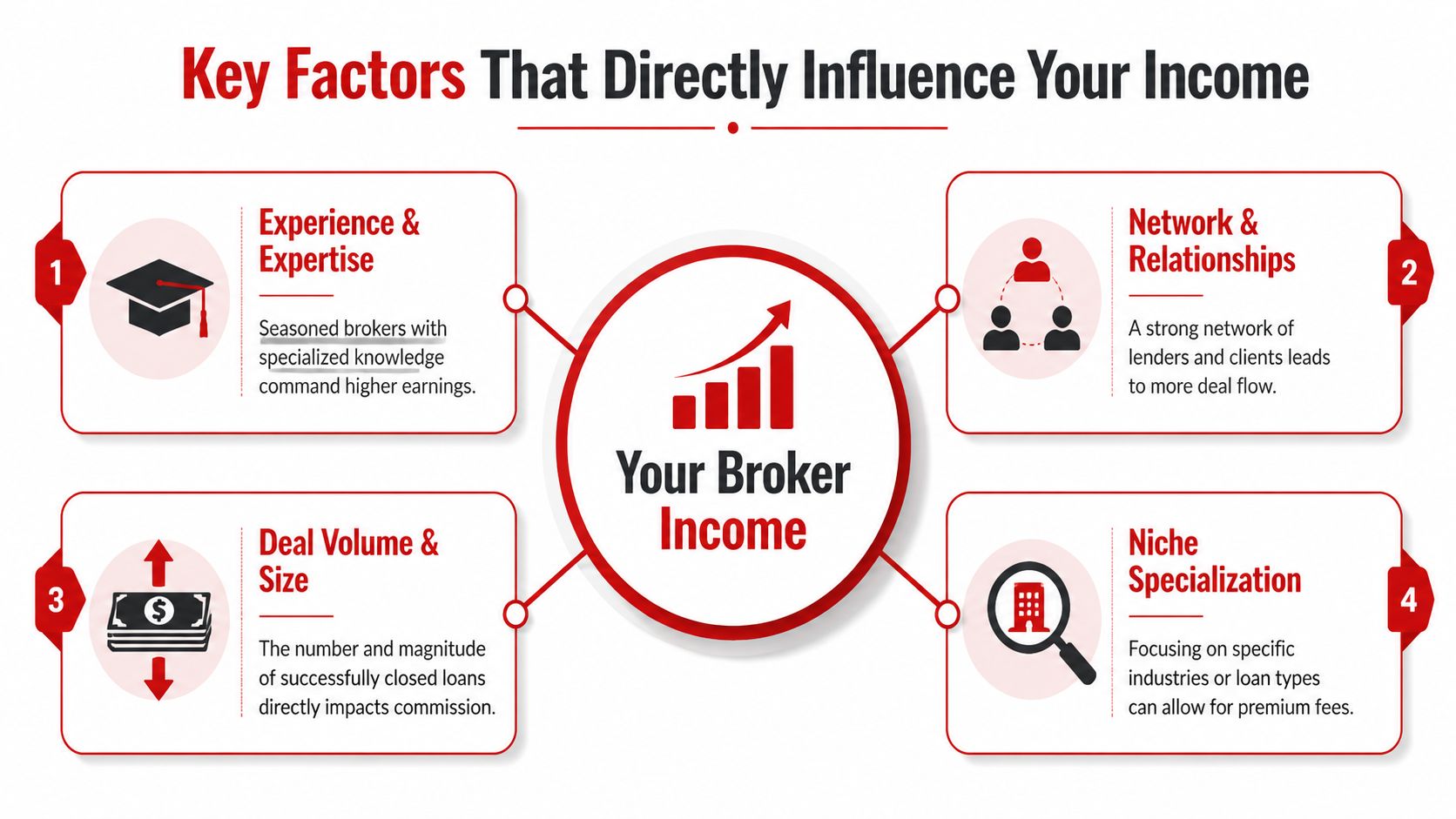

Key Factors That Directly Influence Your Income

Two brokers can have access to similar products and produce completely different results. The difference usually comes down to controllable factors, not talent alone.

Lead flow quality

Volume without quality burns time. A broker can spend all day talking to business owners and still have very little to show for it if the leads aren't fundable. That's why qualification standards matter so much. For anyone refining that skill, this guide on how to get qualified leads is useful because it sharpens the difference between interest and actual opportunity.

Referral-based lead flow tends to be stronger than random outreach because trust is built in earlier. CPAs, consultants, real estate professionals, and business service providers often know which owners are actively looking for capital and which ones are only browsing.

Specialization and positioning

Generalists often stay busy but inconsistent. Specialists are easier to refer because people know what to send them. A broker who becomes known for helping a certain borrower type or funding situation usually has an easier time attracting cleaner deals.

That specialization also improves communication. The broker knows the language of the borrower, the common objections, and the lender expectations tied to that niche. This reduces wasted motion.

Lender relationships and underwriting judgment

Income rises when placement improves. A broker who sends weak files to the wrong lenders creates delays, declines, and borrower frustration. A broker who understands what a lender wants can package the deal properly and preserve credibility.

Knowledge of underwriting alternatives also helps. In many cases, the broker who understands alternative data for credit scoring can think more creatively about viable paths for borrowers who don't fit conventional boxes.

Strong brokers don't just collect applications. They screen, shape, and place deals with intention.

Systems and operating discipline

Many aspiring brokers underestimate the business: good income doesn't only come from selling. It comes from process.

- Response speed matters. Business owners move on when communication stalls.

- Document collection has to be simple. Friction kills deals.

- Follow-up needs a cadence. Too loose and the borrower disappears. Too aggressive and trust erodes.

- File tracking protects momentum. A broker can't scale if every deal lives in memory.

How this compares with salaried finance roles

Traditional finance jobs can offer stability, but they also cap upside and often tie advancement to tenure, internal politics, or job openings. Brokerage income is less linear. It can be volatile at first, but it gives the broker much more influence over outcomes.

That trade-off appeals to professionals who want more control over schedule, location, and income drivers. It doesn't fit everyone. But for the right person, the ability to build referral relationships and compound deal flow is more valuable than waiting for an annual raise.

Proven Strategies to Boost Your Broker Earnings

The brokers who earn more usually aren't working wildly longer hours. They're doing fewer low-value activities and more repeatable ones.

Build referral channels instead of chasing strangers

Cold prospecting can produce deals, but it often creates a feast-or-famine business. Referral partners are different. When a CPA, consultant, or service provider trusts a broker, the broker doesn't have to restart credibility from zero every time.

That kind of pipeline is especially important in a market that has shifted toward performance-based compensation. Janover's discussion of commercial mortgage broker pay notes that experienced brokers often move from a $40,000 to $60,000 base into commission-heavy or commission-only structures. That shift makes pipeline ownership far more important than job title.

Master one product category first

New brokers often slow themselves down by trying to learn every funding option at once. A better approach is to become highly competent in one area, close deals there, and then expand.

That focus improves confidence and speed. It also makes referral conversations easier because the broker can explain exactly who they help and how the process works. Once that lane is producing, adjacent products become easier to add.

Tighten the handoff from lead to funded deal

Many commissions are lost between the first conversation and document collection. Borrowers get busy. Files stall. Emails pile up. A broker who simplifies the next step will usually outperform a broker with better talk tracks but poor follow-through.

Useful habits include:

- Clear intake expectations. Borrowers should know what documents are needed and why.

- Fast recap messages. Summaries after calls reduce confusion.

- Consistent status updates. Silence makes borrowers nervous.

- Referral partner communication. Keeping partners informed strengthens repeat business.

Use a proven operating framework

Trial and error is expensive when every mistake delays revenue. Some brokers piece together their own process over time. Others prefer training and mentorship that provide scripts, lender access, workflow guidance, and a clearer path to first funded deals. Business Lending Blueprint is one example of a program built around that type of structured brokerage setup.

Brokers usually increase earnings faster when they stop improvising every part of the process and start repeating what already works.

The key is not motivation. It's execution. A simple, disciplined process beats scattered effort almost every time.

Conclusion Your Path to a Six-Figure Broker Business

A search for business loan broker salary starts with income, but it should end with business model clarity. This field isn't best understood as a static paycheck. It's better understood as an entrepreneurial income path built on commissions, referral relationships, lender fit, and consistent execution.

That distinction matters because it filters the opportunity correctly. Someone looking for guaranteed pay and very little variance may prefer a more traditional finance role. Someone who wants flexibility, home-based work, scalable income, and direct control over results may find brokering far more attractive.

What most people need to know before starting

A finance degree isn't the gatekeeper. Product knowledge, process discipline, and communication matter more. The strongest beginners usually focus on a few practical questions:

- How will leads come in? Referral strategy matters more than random activity.

- How will files be screened? Pre-qualification protects time and reputation.

- How will deals be placed? Matching borrowers to realistic options is where trust is built.

- How will skills improve? Sales, lender communication, and follow-up all get sharper with repetition.

For readers who want to strengthen the communication side of the business, this resource on mastering sales techniques to close a sale can help sharpen the conversations that move borrowers from interest to action.

The real opportunity

There is a practical reason this path appeals to entrepreneurs, consultants, former bankers, sales professionals, and people building a second income from home. Business owners constantly need capital, and many need help finding the right funding path. A broker who becomes good at solving that problem can build something much more flexible than a conventional job.

The six-figure outcome that many people want doesn't come from chasing a title. It comes from building a pipeline, learning how to qualify and place deals, and repeating a process that serves business owners well.

If becoming a business loan broker sounds like the right fit, the next step is simple. Watch the free training from Business Lending Blueprint or schedule a strategy session to see how the brokerage model works, what the day-to-day looks like, and how to build a real funding business from home with a clear plan.