A new broker usually meets this deal in the first month.

A business owner has real sales, a clean product, and a clear use for capital. The company might sell online, bill on subscription, or collect repeat service revenue. The owner goes to a bank, gets asked for a longer operating history, stronger profitability, more collateral, or a tighter credit profile, then walks away frustrated. The revenue is there, but the file still dies.

That's where revenue based business loans start to matter.

For someone building a home-based brokerage, this product sits in a sweet spot. It solves a real funding problem for growing companies, it gives brokers a way to stand apart from basic rate shoppers, and it fits a referral-driven model that can be run remotely with low overhead. People exploring self-employment often start with broad advice on mindset and business formation, and Baslon Digital's entrepreneurship guide is a useful example of that bigger picture. The lending side gets more practical. A broker gets paid by matching a business owner with capital that fits how that company earns money.

That's the opportunity. Not hype. Not easy money. A real niche with real demand.

Table of Contents

- Your Next Big Opportunity in Business Lending

- What Exactly Are Revenue Based Business Loans

- The Anatomy of a Deal Terms and Pricing

- Identifying Ideal Clients for Revenue Based Loans

- RBF vs The Alternatives A Broker's Comparison

- Your Broker Playbook Sourcing and Placing RBF Deals

- Build Your Brokerage with Modern Funding Solutions

Your Next Big Opportunity in Business Lending

A founder gets turned down by the bank on Tuesday. By Friday, they still need capital to buy inventory, hire sales staff, or keep an ad campaign working. Revenue based business loans often fit that gap, and brokers who know how to place them stop losing good businesses just because the file does not fit a conventional credit box.

That is the opportunity.

A growing brokerage does not need more products on the shelf. It needs answers for the files that stall out in underwriting, frustrate the client, and die in follow-up. Revenue based business loans give you a strong position with companies that have real sales activity, uneven cash flow, or short operating history, but still have a clear use for growth capital.

Why this product gives brokers an advantage

New brokers usually chase the easiest approvals first. Clean financials, strong credit, and bank-ready borrowers attract every other shop too. Revenue based business loans put you in a different conversation. The client is not just comparing rate sheets. The client is trying to find someone who understands how revenue behaves, how repayment affects working capital, and whether the funding will help the business grow.

That changes how you win deals.

Practical rule: The best RBF prospects are often strong operators with imperfect paper, not weak businesses looking for a last-minute rescue.

That distinction matters. A seasonal ecommerce brand, a digital agency, or a subscription business can be a very workable file. A company with collapsing sales and no plan for the capital usually is not. Good brokers learn to sort those two groups fast.

This product also helps build referral channels that last. Accountants, consultants, and fractional finance professionals regularly see owners who need capital but are not ready for a bank term loan. If you can explain repayment clearly, set expectations early, and screen out bad fits, those partners remember it. Brokers serving founders who are still learning how to build and fund a company can also benefit from content such as Baslon Digital's entrepreneurship guide, because those clients often need both financing and a clearer operating plan.

Why the timing works

Business owners are more familiar with non-bank funding than they were a few years ago. That does not mean they understand the details. It means the conversation starts faster.

For a broker, that is useful. You do not have to spend the whole call defending the idea of alternative financing. You can spend it qualifying the file, testing whether revenue is stable enough, and making sure the owner understands the difference between top-line sales and actual cash available for repayment. If that distinction is fuzzy, send them to this guide on net revenue vs gross revenue before you try to structure terms.

A disciplined broker does not force every deal into RBF. That is how defaults rise and referral sources disappear. The upside comes from knowing when this structure is the right tool, presenting it with confidence, and protecting the client from a deal their revenue pattern cannot support.

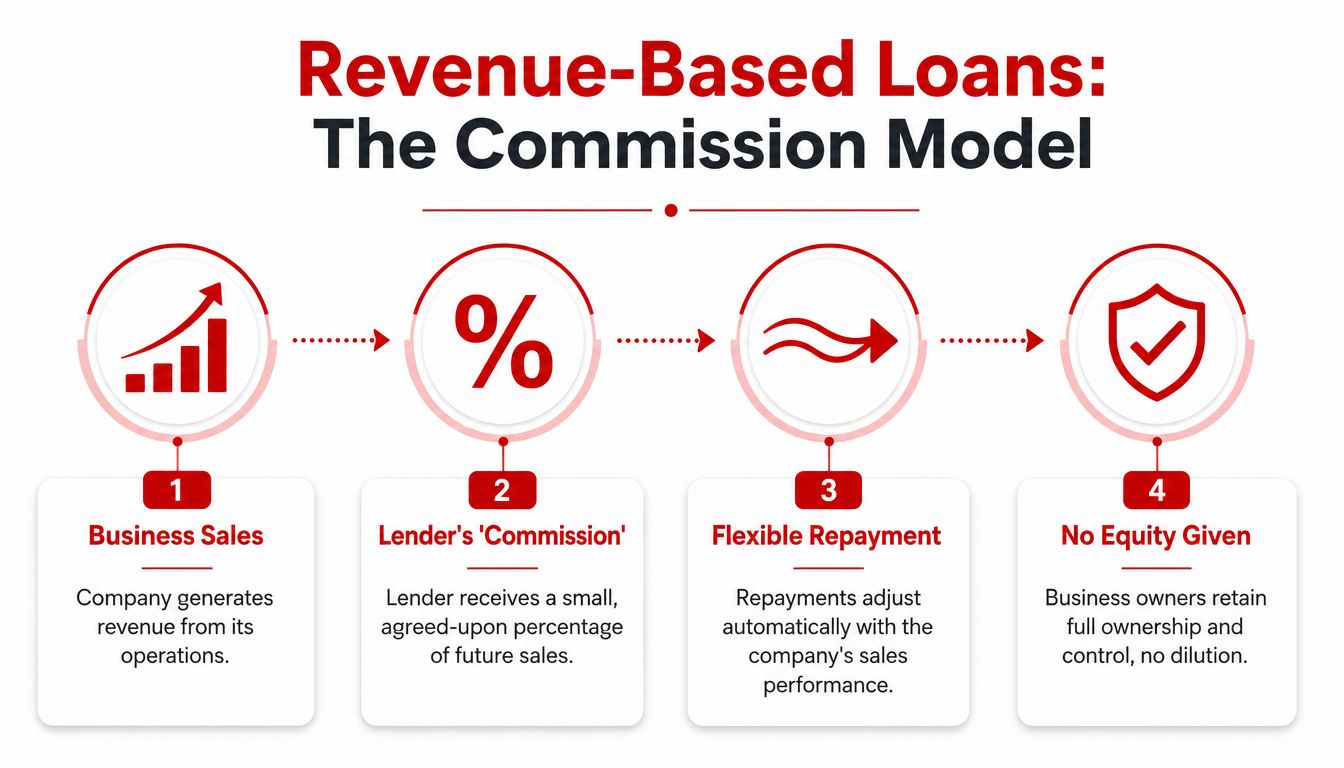

What Exactly Are Revenue Based Business Loans

The cleanest way to explain revenue based business loans is this: the lender gets a temporary share of future sales until a fixed total has been collected.

That explanation lands because it sounds like the underlying economics of the deal. It's not equity. The lender doesn't own part of the company. It's not a traditional installment loan either, because the payment amount moves with revenue rather than staying fixed every month.

The simple way to explain it

A good broker can explain this in one minute without sounding technical.

A business receives capital upfront. In return, the funder collects an agreed percentage of future revenue. When sales are stronger, the collected amount rises. When sales slow down, the collected amount falls. The agreement ends once the business reaches the contracted repayment cap.

That's why many founders respond well to the “temporary sales commission” analogy. The company keeps ownership. The lender gets paid from revenue performance for a defined period.

For brokers, this works best when the client already understands top-line performance. If a prospect confuses cash in the bank with revenue, the conversation gets muddy fast. A quick primer on sales income for service businesses helps frame how top-line revenue differs from other financial measures. For a more lending-specific distinction, this breakdown of net revenue vs gross revenue also helps brokers explain what lenders usually care about in these files.

The mechanics a broker must know

The core terms matter because they determine whether deals are won or lost.

Revenue based business loans are non-dilutive, with lenders purchasing 2% to 8% of future recurring revenues for upfront capital. Repayment ends at a fixed cap, typically 1.5x to 2.5x the principal. Underwriting commonly requires 3 to 6 months in business, $5,000 to $15,000 in monthly revenue, and a FICO score over 500, with funding often available in 1 to 7 days, according to this overview of revenue-based business loans.

A broker should also remember what this product is not. It's not a magic answer for businesses with no revenue. It's not ideal for erratic one-off project income. It's not cheap because the paperwork says “no interest.”

The repayment amount flexes. The cost still has to make sense.

That's the distinction that earns trust. Founders appreciate flexibility, but they appreciate honesty more. If a broker explains the structure clearly, the client can compare certainty, speed, and ownership retention against total repayment cost.

The Anatomy of a Deal Terms and Pricing

Most new brokers lose credibility when the conversation turns from concept to terms. They can describe the product, but they can't model the deal in plain English.

That's fixable. Revenue based business loans are easier to explain once three parts are separated: how much the client receives, how much the client must repay in total, and how quickly the lender takes its share from revenue.

The three terms that control the deal

Here are the terms that matter most on a live call:

- Advance amount: This is the upfront capital the client receives. In many structures, the amount can be tied to recurring revenue strength.

- Repayment cap: This is the total payback, expressed as a multiple of the funded amount.

- Capture rate or holdback: This is the percentage of revenue collected during the repayment period.

According to Swoop's explanation of revenue-based financing, repayments generally range from 5% to 25% of monthly gross revenue until a cap of 1.2x to 1.6x the loan is met. The same source states that loan amounts can be 4 to 7 times monthly recurring revenue, with typical repayment timelines of 6 to 18 months that flex with performance and carry no penalties for slow months.

That one sentence gives a broker plenty to work with.

A sample structure a broker can explain clearly

Use a simple example. Keep it clean.

If a client takes $100,000 and the repayment cap is 1.4x, the total owed is $140,000. If the capture rate is 10%, the monthly collected amount depends on revenue.

| Revenue month | Capture rate | Payment that month |

|---|---|---|

| $50,000 | 10% | $5,000 |

| $20,000 | 10% | $2,000 |

That table shows the product's biggest operational advantage. The payment burden adjusts with sales instead of ignoring them.

A broker should still walk the client through the trade-off. Flexibility protects cash flow in soft months, but it doesn't erase cost. The repayment cap remains the cap. Faster or slower revenue changes timing, not the contracted total.

For brokers who want to pre-screen economics before sending a file out, a business building loan calculator can help organize repayment discussions and set expectations before underwriting reviews the file.

Clients don't need a lecture on factor structures. They need to see what happens in a strong month, an average month, and a weak month.

When a broker can model those three scenarios clearly, objections drop. The product stops sounding exotic and starts sounding usable.

Identifying Ideal Clients for Revenue Based Loans

A new broker's biggest mistake is treating every fast-moving file like an RBF deal.

The better approach is to screen for revenue quality before you ever discuss terms. Good placements usually come from businesses with recent, trackable sales, clear deposit activity, and a use of funds that can produce more revenue fast enough to support the repayment structure. That is how you protect lender relationships and spend your time on files that can close.

Who usually fits best

The best RBF clients tend to have a business model you can explain in two minutes to an underwriter and defend in ten minutes to the owner.

Look for patterns like these:

- Recurring or repeat customer revenue: Membership businesses, subscription models, ecommerce sellers with steady reorder behavior, and service companies with ongoing billing usually present better than one-off project businesses.

- A clear growth plan for the capital: Inventory, paid acquisition, equipment tied to production capacity, and hiring tied to booked demand are easier to place than vague working capital requests.

- Owners who want to keep equity: Founders who care about control often respond well once they see that repayment tracks revenue instead of forcing a fixed amortization schedule.

- Businesses that miss bank credit for structure reasons: Asset-light companies, newer firms, and borrowers with uneven net income can still be solid candidates if top-line performance is strong.

As noted earlier, the revenue-based financing market is projected to grow quickly over the next several years. That matters to brokers because it signals something practical. More lenders are entering the category, more borrowers are hearing about the product, and more deals can be won by brokers who know how to pre-qualify fit instead of pitching it blindly.

I also pay attention to how the client reports their numbers. If they can show monthly revenue trends, explain customer retention, and connect the funding request to a realistic sales plan, the file usually has a path.

Who usually causes trouble

Bad-fit files usually show their problems early, and a disciplined broker does not force them through.

Pre-revenue companies belong in a different capital conversation. So do businesses with erratic margins, heavy customer concentration, or no reliable way to verify current sales. If the owner is shopping only for the lowest advertised cost, RBF is often the wrong product unless flexibility matters more than price.

Another common problem is weak financial fluency. An owner does not need a finance degree, but they do need command of the basics. They should know monthly revenue ranges, average ticket size, gross margin direction, and what the capital is supposed to change over the next quarter.

Good RBF clients do not just need capital. They can explain how the capital should produce future revenue.

That point helps a broker build a lane. Instead of chasing every business owner with deposits, focus on companies where sales are visible, the funding use is tied to growth, and the repayment method matches how the business earns. If the client has slow-paying invoices rather than daily or weekly card-driven revenue, accounts receivable lenders for invoice-heavy businesses may be the better fit.

That is how you close more of the right deals. You stop selling a product and start matching structures to revenue behavior.

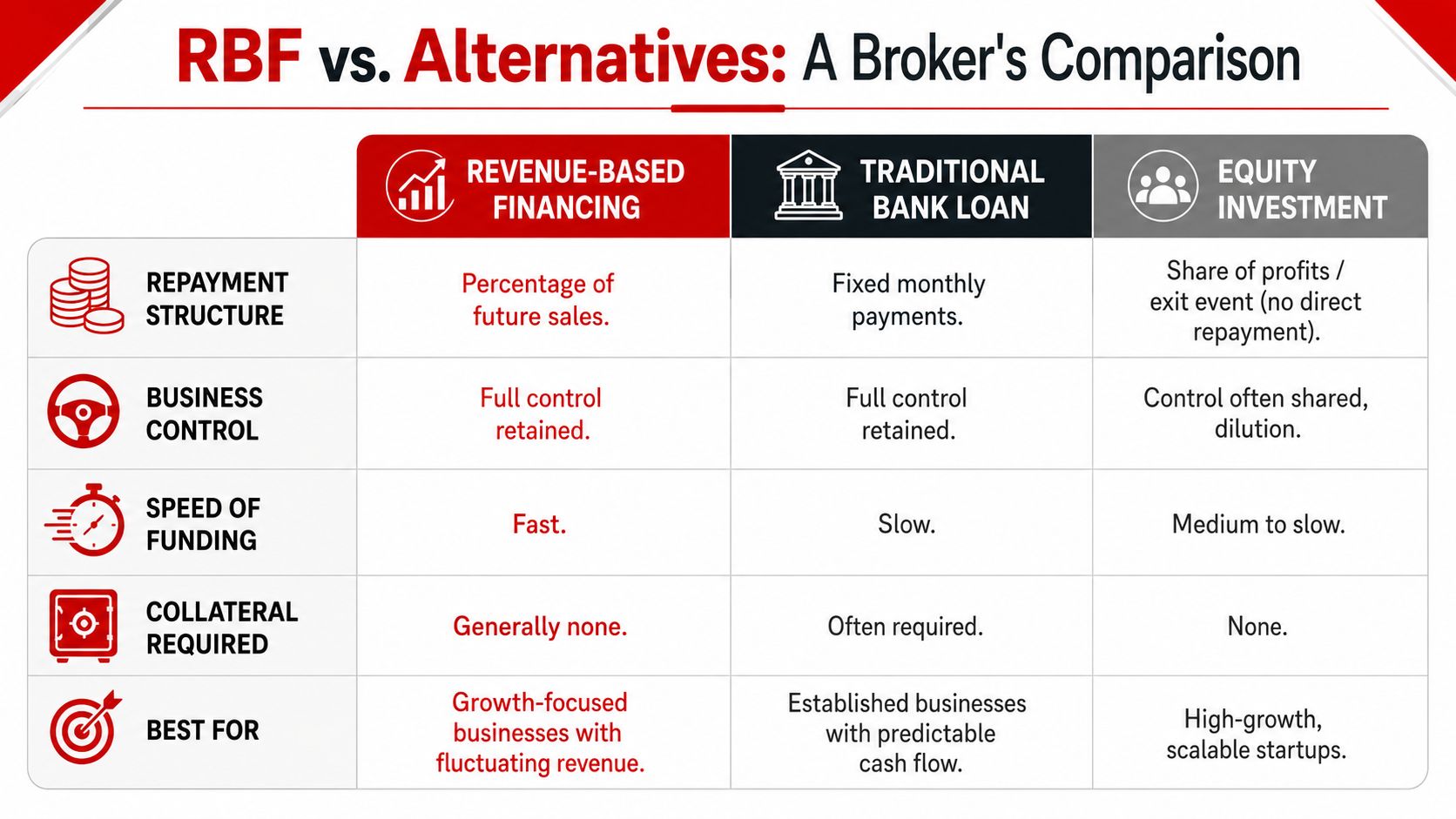

RBF vs The Alternatives A Broker's Comparison

Clients rarely ask for a funding product by its exact structure. They ask for money, speed, flexibility, and control. A broker's job is to translate those needs into the right fit.

Revenue based business loans sit in a middle ground. They're not traditional installment debt. They're not equity. They also aren't always the answer. The smart broker knows how to compare them without forcing the product.

When RBF beats a term loan

A term loan usually works better when the client has stable cash flow, strong documents, and enough predictability to handle fixed payments comfortably.

RBF usually wins when that same client has solid revenue but needs payments to breathe with the business. That matters for companies with seasonality, recent growth swings, or aggressive reinvestment plans. Fixed debt doesn't care whether the month was strong or soft. Revenue-based repayment does.

A term loan can look cheaper on paper. Sometimes it is. But many businesses can't qualify, can't wait, or can't absorb a fixed schedule without strain.

When it beats an MCA and when it does not

A lot of inexperienced brokers blur the line between revenue-based structures and other high-cost receivables products. That creates confusion.

RBF is usually easier to position when the business has broader revenue quality and wants a structure tied to ongoing performance rather than a blunt daily drain. If a client is also reviewing receivables-based options, this look at accounts receivable lenders can help frame how collateral style and repayment logic differ across products.

Here's a practical comparison:

| Option | Best fit | Main tension |

|---|---|---|

| Revenue based financing | Growth-focused company with trackable revenue | Flexible repayment can still be expensive |

| Traditional term loan | Established company with predictable cash flow | Fixed payments can pressure slower months |

| Equity capital | High-growth founder willing to trade ownership | Dilution and shared control |

Why founders compare it with equity

For some founders, the key comparison isn't debt versus debt. It's debt versus dilution.

RBF keeps ownership intact. That's a serious advantage when the owner believes the company's future value will be much higher than it is today. But ownership retention doesn't mean the capital is cheap. A broker has to say both parts.

According to SoFi's overview of revenue-based business loans, the repayment cap is often 1.5x to 2.5x principal and the capture rate often falls between 2% and 8% of revenue. That same source notes that a $100,000 loan could cost $250,000 if revenue stagnates, which shows how flexibility can come with a very high effective cost.

That's the honest broker script. RBF can be the right answer when speed, non-dilution, and payment flexibility matter more than headline cost. It's the wrong answer when the client can access cheaper capital and comfortably live inside fixed payments.

Your Broker Playbook Sourcing and Placing RBF Deals

Most brokers don't struggle because the product is hard. They struggle because their deal flow is random.

Revenue based business loans reward focus. A broker who knows where to source them, how to package them, and how to explain them will close more often than a broker who waits for generic inbound leads.

Where good deals actually come from

The best RBF referrals usually come from professionals who already see the pain before a broker does.

- CPAs: They know when a client has revenue but doesn't fit bank underwriting.

- Bookkeepers and fractional finance professionals: They can spot recurring deposits, margin pressure, and immediate capital needs.

- Startup and small business attorneys: They often hear founders say they need capital but don't want dilution.

- Marketing consultants and agencies: They work with companies that need ad spend or growth capital to scale revenue.

The key is specificity. Don't ask referral partners to “send anyone who needs money.” Ask for companies with proven sales, a near-term growth plan, and reluctance to give up ownership.

How to package the file for underwriting

A sloppy submission creates delays. A clean file gets attention.

According to Cirrus Capital's explanation of revenue-based financing, these structures often provide $50,000 to $3 million in capital, repaid with 3% to 8% of monthly revenue until a 1.3x to 2.5x cap is reached. Collections are automatic, and many agreements include a maximum term of 3 to 5 years.

That gives a broker a solid framework for positioning the product. To package the deal well, gather:

- Recent business bank statements. Lenders want to see revenue flow, consistency, and deposit behavior.

- A simple revenue narrative. Why did revenue rise, dip, or flatten? Underwriters want context, not mystery.

- Use of funds tied to growth. Inventory, marketing, hiring, or expansion usually reads better than vague working capital.

- Basic customer concentration notes. Heavy dependence on one customer can create concern.

- Ownership and business background. Clear explanations reduce avoidable follow-up.

A lender can work with imperfect credit faster than it can work with unclear revenue.

Language that moves deals forward

Brokers don't need clever scripts. They need clean language.

For a business owner:

“This isn't about replacing a bank loan if a bank loan is the best fit. This is for companies with real revenue that need flexible repayment and want to keep ownership.”

For a referral partner:

“A strong fit is a business with sales momentum, a clear use for capital, and a file that may not land with a conventional lender.”

For an uncertain prospect:

“The main question isn't whether the payment is fixed. The main question is whether a percentage-of-revenue structure helps the business grow without choking cash flow.”

That kind of clarity helps a broker build a business from home without turning into a hard closer. The model scales because the conversations are consultative, the referrals compound, and funded clients often come back when new capital needs show up.

Build Your Brokerage with Modern Funding Solutions

Revenue based business loans do more than fund companies. They teach a broker how to think like an advisor.

A broker who can identify revenue quality, explain flexible repayment clearly, and place modern funding solutions with the right clients has a business that can grow through referrals instead of constant chasing. That's attractive to entrepreneurs, consultants, sales professionals, bankers, CPAs, and career changers who want a flexible, home-based business with room to scale.

Brokers who want to build visibility around that expertise can also benefit from consistent professional content, and SleekPost for LinkedIn growth offers useful ideas for showing up credibly online. For a step-by-step look at the business model itself, this guide on how to start a loan business is a practical next read.

The opportunity isn't in memorizing one product. It's in building the judgment to match the right product to the right borrower, then turning that skill into a remote, recession-resistant brokerage with recurring referral relationships.

If building a business loan brokerage sounds like the right next move, Business Lending Blueprint is the place to start. The training shows everyday people how to work from home, help business owners access funding solutions, and build a scalable commission-based business through practical systems, vetted lender relationships, and step-by-step support. Watch the free training or schedule a strategy session to see how this model works in practice.