A new broker usually meets MCA distress the same way. A business owner calls in a rush, says cash flow is collapsing, admits there are multiple daily withdrawals hitting the account, and asks for “one loan to clean this up.” The temptation is to chase the funding request fast. That's where weak brokers get trapped.

The stronger move is slower and more disciplined. MCA consolidation loans can be a real solution, but many offers marketed as consolidation are just another expensive advance with a cleaner pitch. A broker who understands that difference doesn't just close more deals. That broker earns trust, protects referral relationships, and builds the kind of remote, home-based lending business that survives market swings because clients keep coming back with harder files and better introductions.

Table of Contents

- The MCA Debt Spiral and Your Broker Opportunity

- Decoding MCA Consolidation Solutions for Your Clients

- The Broker's Playbook for Vetting Consolidation Deals

- Structuring the Deal and Securing Client Financing

- Sales Scripts and Critical Compliance Pitfalls

- Become the Go-To Expert in MCA Restructuring

The MCA Debt Spiral and Your Broker Opportunity

A stacked MCA file rarely arrives neatly organized. It shows up as panic. The owner is trying to make payroll, vendors are waiting, and the account is getting hit over and over by withdrawals that were manageable one at a time but destructive in combination.

That's where a broker's opportunity begins. Not because the client is desperate, but because the market is full of bad guidance. One of the clearest warnings in this space is that most content falsely frames MCA consolidation as a traditional loan with lower rates, while industry data confirms it's often a new, higher-cost MCA that replicates the same daily or weekly cash-flow drain without reducing total debt owed, as noted by National Credit Partners on merchant cash advance debt relief.

What the debt spiral looks like in practice

A broker should spot the pattern quickly:

- Multiple active withdrawals: The business has more than one funder pulling from the same operating account.

- Cash flow compression: Revenue may still be coming in, but timing has broken the business.

- Emergency borrowing behavior: The owner took the next advance to solve pressure created by the previous one.

- Loss of control: The client can't explain exact balances, payoff amounts, or maturity order.

Practical rule: If the client only wants “more money fast,” but can't clearly list existing obligations, the broker doesn't have a funding request yet. The broker has a diagnostic job.

This is also why a referral-based broker model works so well here. CPAs, consultants, insurance agents, and service professionals constantly meet business owners under this exact strain. The broker who knows how to assess MCA files becomes useful beyond one transaction.

Why this niche matters for a broker business

MCA files are messy, but they create durable referral relationships when handled correctly. Business owners remember the broker who explained the difference between real restructuring and another trap. Referral partners remember the broker who told the truth even when that meant slowing a file down.

Lead flow matters too. A broker who wants a steadier pipeline can automate lead generation with AI to surface conversations with owners already dealing with debt pressure, then qualify those opportunities before spending time on underwriting.

For a newer broker building a remote practice, this niche can become a specialty. Learning how to start a loan business is one thing. Learning how to manage complex MCA distress is what moves a broker from generalist to trusted advisor.

Decoding MCA Consolidation Solutions for Your Clients

Most clients use the word “consolidation” loosely. A broker can't. Different products solve different problems, and the wrong recommendation can make a strained account worse.

A true consolidation structure is meant to replace multiple high-cost positions with one structured obligation. In the clearest version of that model, repayment can stretch from 2 to 10 years with monthly payments instead of aggressive daily or weekly debits, as outlined by CNBC Select's explanation of merchant cash advances.

What true relief looks like

The first question isn't whether the client can get approved. It's whether the new structure changes behavior in the account.

A workable deal usually does three things:

| Deal characteristic | Why it matters to the client | Why it matters to the broker |

|---|---|---|

| One predictable payment | Reduces chaos in cash management | Makes the value proposition easy to explain |

| Monthly repayment cadence | Gives the owner breathing room between deposits and debt service | Separates real relief from disguised MCA stacking |

| Longer runway | Stabilizes operations and budgeting | Improves the chance of cleaner renewals and referrals |

That doesn't mean every longer-term offer is good. Extending a problem without fixing pricing or payment frequency isn't relief. It's delay.

A broker view of the main options

A strong broker usually sorts MCA relief options into three practical buckets.

True term-style refinancing: Best for businesses with cleaner statements, consistent deposits, and enough operational stability to support a structured monthly obligation. This is often the most credible path when the broker wants a lasting fix rather than a temporary patch.

Dedicated debt consolidation programs: These are built for borrowers already carrying expensive short-term debt. They can be useful when a bank-style file won't clear, but the broker still sees a realistic path to stabilized payments.

Portfolio buyout or mediation-style solutions: These fit cases where the capital stack is too messy for simple replacement financing. The broker's role here is less about “selling a loan” and more about managing expectations, sequencing payoffs, and preserving the client's ability to operate.

The best recommendation is the one that changes the client's cash flow pattern for the better, not the one that sounds best on a call.

There's also a practical fit issue. Some businesses are too bruised for a clean refinance but still worth helping. Others look distressed on the surface and are strong candidates because revenue is healthy and the problem is structure, not demand.

For newer brokers serving challenged borrowers, product knowledge matters. That includes understanding the broader range of business loans for bad credit so the client isn't forced into an MCA-only conversation when better financing may exist.

The Broker's Playbook for Vetting Consolidation Deals

A broker earns the fee. Not at submission. Not at funding. At diagnosis.

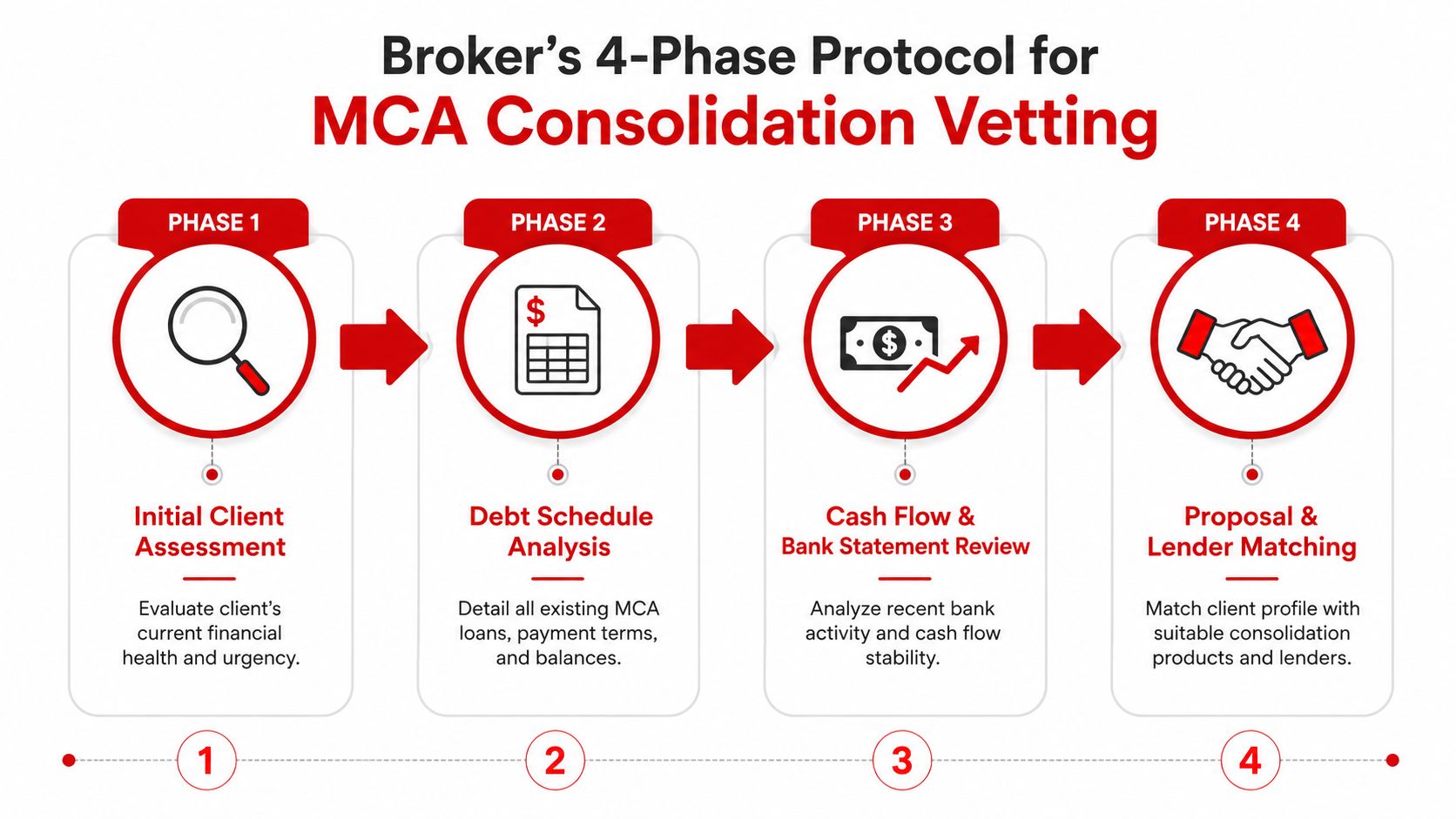

A reliable framework already exists. The process for MCA consolidation follows a four-phase protocol consisting of detailed financial assessment, strategic selection of a consolidation partner, term negotiation targeting lower rates, and direct settlement where the consolidation lender pays off existing advances, according to ROK's guide to stacked MCAs and consolidation.

The four-phase review

The first phase is document gathering, but the point isn't paperwork. The point is visibility. The broker needs every active MCA, current payment cadence, estimated remaining balance, and recent account behavior.

The second phase is lender matching. Weak brokers blast a file. Strong brokers narrow the field based on the client's profile, urgency, and whether the lender is equipped for MCA-specific restructuring.

The third phase is negotiation. That doesn't mean squeezing for cosmetic talking points. It means pushing for terms that change the cash-flow reality, especially payment frequency, fees, and payoff mechanics.

The fourth phase is settlement execution. Existing positions should be addressed directly and cleanly. If payoff logistics are fuzzy, the broker should assume the deal can drift into a new stack instead of a reset.

Red flags that change the recommendation

Some files deserve a hard pause. Not because the client is unworthy, but because the wrong deal can do damage.

- Recent negative bank days: This suggests the account may not support even a restructured obligation.

- Unclear payoff information: If balances and creditor details are missing, settlement risk rises immediately.

- No operational profit outside the MCA burden: The business may have a core business model problem, not just a debt structure problem.

- A borrower focused only on speed: Urgency is normal. Refusal to review terms is dangerous.

A broker should never confuse urgency with suitability. The client's stress is real. That doesn't make every approval a good approval.

A practical way to improve underwriting quality is to use a checklist mindset borrowed from transaction work. A clean founder's due diligence checklist can help newer brokers think more rigorously about anomalies, trend breaks, and missing documentation before the file reaches a lender.

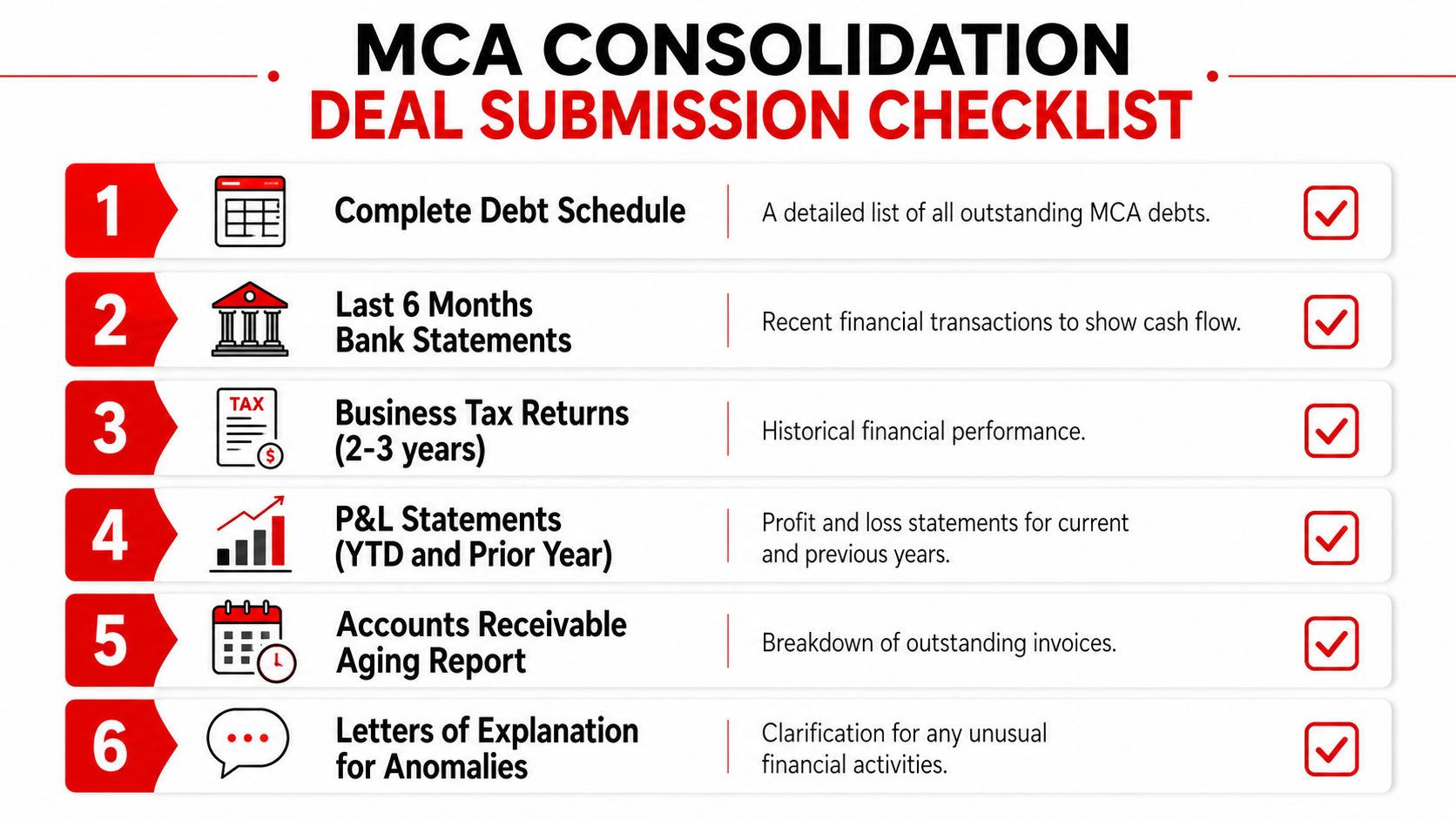

What a clean file should include

The debt schedule is the backbone of the package. Without it, a broker is guessing. This is one reason it helps to understand what a debt schedule is and how to build one that a lender can use.

A strong submission package usually includes:

- A complete debt schedule. Every MCA, payment frequency, estimated remaining balance, and contact point should appear in one place.

- Recent business bank statements. These show whether the account can carry a reset.

- Tax returns and current financials. These help separate temporary debt stress from chronic weakness.

- Explanations for anomalies. Large deposits, overdrafts, unusual transfers, or temporary disruptions should be addressed before underwriting asks.

The newer broker's edge isn't charm. It's preparation. MCA consolidation deals close faster when the file already answers the lender's obvious questions.

Structuring the Deal and Securing Client Financing

Once the file is viable, the broker's job changes. Diagnosis matters less now than presentation. A good structure still dies if the client doesn't understand it, doesn't trust it, or thinks “single payment” automatically means “better deal.”

How to present the deal clearly

The broker should explain the new offer in plain business terms, not lender jargon. Clients under MCA pressure are usually listening for one thing first. “Will this stop the bleeding?” The answer should be grounded in payment structure, not promises.

A practical presentation usually covers these points:

- What gets paid off: Identify which obligations will be settled at closing.

- What the new payment rhythm looks like: Monthly matters because it changes how cash sits in the account.

- What doesn't change: If total debt isn't shrinking, say that plainly.

- What operational habits must improve: The owner needs to avoid taking new short-term debt on top of the reset.

A simple before-and-after explanation can help. The exact numbers will vary by file, so the broker should stay qualitative unless the live deal documents support the calculation. The point is to show how replacing multiple withdrawals with one predictable structure can stabilize payroll timing, inventory buying, and vendor planning.

Field note: Clients rarely buy consolidation because they love debt strategy. They buy because they want control of the account back.

The collateral conversation brokers must handle correctly

Misleading terminology can lead to future complications. Clients often ask whether MCA consolidation can be done without collateral. That question needs a precise answer.

A key distinction is that brokers must separate true unsecured loans from MCA consolidation offers that still rely on a purchase of future receivables, effectively tying the business's daily income to the new funder, as explained by Biz2Credit's discussion of unsecured debt consolidation and the MCA cycle.

That means “unsecured” can be misleading if the economic reality still captures receivables.

A broker should walk through it like this:

| Client question | Straight answer a broker can give |

|---|---|

| Is this unsecured? | “It may not require hard collateral, but the agreement may still be tied to future receivables.” |

| Will daily cash still be affected? | “That depends on how repayment is structured. The documents matter more than the label.” |

| Is this true refinancing? | “Only if the new structure meaningfully improves payment terms and doesn't recreate the same drain.” |

This is also where expectations must be tightened around documentation. Payoff letters, authorizations, entity records, and financial statements all support a clean close. They also help the broker explain exactly what the lender is buying, paying off, and expecting in return.

Sales Scripts and Critical Compliance Pitfalls

A broker can be skilled, helpful, and still create compliance problems with careless language. MCA distress makes owners vulnerable to overpromises, so the broker's script has to stay accurate.

There's a reason caution matters here. Industry data indicates MCA debt consolidation rarely works as a standalone solution, and many firms resolve only 70% to 95% of enrolled debt through alternative strategies rather than pure consolidation. The same source notes that if a business has already defaulted on existing funders, the chance of securing an offer drops to close to zero, according to Second Wind Consultants on why businesses shouldn't just consolidate MCA debt.

Scripts that keep the conversation honest

A broker doesn't need a flashy pitch. A broker needs language that is truthful and calming.

Good script lines sound like this:

- For the first call: “The first step is to map every current obligation and see whether restructuring improves cash flow or just moves the pressure.”

- When the client asks for a guarantee: “Approval depends on the account profile and current lender positions, so the review has to come first.”

- When the deal may not reduce total debt: “This may improve payment structure without reducing what's owed. The documents will show whether the trade-off makes sense.”

- When the client is already under severe strain: “If the account is too damaged for consolidation, other resolution paths may be more realistic.”

That language protects everyone. It also increases credibility. Business owners under stress can tell when a broker is selling fantasy.

Where brokers get into trouble

Compliance mistakes usually come from one of three habits.

First, brokers promise savings before reviewing the full stack. Second, they describe a receivables-based product as if it were a standard term loan. Third, they avoid difficult conversations about account health because they don't want to lose the deal.

“Let's see if this can improve payment stability” is compliant and useful. “This will wipe out the problem” is neither.

Ethical communication is part of professional survival. A broker who wants longevity should study fair lending practices for business finance professionals and apply that discipline to every distressed file.

When a file doesn't fit, the broker should say so. That doesn't kill the relationship. In many cases, it creates the referral because the client finally spoke with someone who told the truth.

Become the Go-To Expert in MCA Restructuring

Brokers who understand MCA restructuring operate at a different level. They don't just pass applications around. They identify whether the client has a payment problem, a pricing problem, a documentation problem, or a business model problem.

That skill compounds. It improves close rates because submissions are cleaner. It improves commissions because the broker solves more complex financing cases. It improves referrals because accountants, consultants, and other professionals prefer sending clients to someone who can handle messy files without creating more damage.

For aspiring entrepreneurs, sales professionals, bankers, CPAs, consultants, and career changers, this is one of the clearest paths to building a flexible, home-based, recession-resistant brokerage business. The work can be done remotely. The relationships can scale. The expertise creates repeat business because funding needs don't disappear after one deal.

A broker doesn't need hype to make this model attractive. The opportunity is strong enough on its own. Small business owners need funding guidance. Alternative lenders need qualified submissions. Skilled brokers sit in the middle and create value by making good matches, protecting clients from bad structures, and managing deals with discipline.

Business Lending Blueprint teaches people how to build a profitable, home-based business by becoming a business loan broker. It doesn't provide loans. It provides the training, mentorship, systems, and industry guidance to help people launch and grow a lending business that serves real business owners. To learn how to build referral relationships, work remotely, and create a scalable income opportunity in business finance, watch the free training from Business Lending Blueprint or schedule a strategy session.