A new broker usually meets this problem early. A business owner has real revenue, real customers, and a real need for capital, but the bank still says no because the owner's personal score is weak, the company is young, or the tax returns don't tell the full story.

That moment frustrates beginners because it looks like a dead deal. It isn't. It's the opening for a smarter kind of underwriting, and for a broker business built around serving the companies that traditional lending overlooks. Alternative data for credit scoring matters because it helps lenders evaluate what a business is doing now, not just what an old report says happened in the past.

For brokers, that changes the job completely. Instead of forwarding declines, they can reposition deals, present the right supporting data, and place business with lenders that care about cash movement, payment behavior, and operational consistency. That's how more files turn into approvals, more approvals turn into commissions, and more funded clients turn into repeat referrals.

Table of Contents

- Why Traditional Lending Fails Great Businesses

- What Is Alternative Data for Credit Scoring

- The Key Alternative Data Sources for Business Lending

- How Lenders Use Alternative Data to Say Yes

- Your Blueprint for Using Alternative Data as a Broker

- Start Your Broker Business with a Modern Edge

Why Traditional Lending Fails Great Businesses

Traditional lending misses good businesses because it often relies on narrow signals. A borrower can run a solid company, keep customers happy, and produce healthy deposits, yet still fall outside bank guidelines because the owner's profile doesn't fit a standard credit box.

That happens every day with contractors, restaurants, e-commerce sellers, service firms, seasonal businesses, and companies that mix personal and business finances while they grow. The business may be viable. The file just isn't bank-friendly.

The bank decline is often a model mismatch

Banks like clean files. They prefer long histories, strong bureau records, neat financial statements, and predictable documentation. Small businesses rarely grow in a neat, predictable way.

A strong operator might have:

- Recent momentum: Revenue has improved faster than the paperwork reflects.

- Messy structure: Deposits are consistent, but accounts aren't organized the way a bank wants.

- Thin traditional profile: The owner doesn't have the kind of bureau history that supports a conventional approval.

That's why a decline doesn't always mean the business is weak. It often means the lender is using the wrong lens.

Great businesses get rejected when underwriting focuses on what's easy to document instead of what actually predicts repayment.

For a broker, this is an important opportunity. The market isn't only made of pristine borrowers. It's full of business owners who need capital and can support it, but need a lender willing to evaluate live operating performance instead of static legacy criteria.

Why this creates room for brokers

Alternative lenders built their underwriting around that gap. They look deeper into cash flow, recurring deposits, account activity, and payment behavior. A broker who understands that process can rescue files that would otherwise disappear.

That's the practical difference between being an application taker and being an advisor. One forwards a decline. The other knows where the deal still fits.

A useful starting point is understanding how the alternative lending industry really works. Once that framework clicks, alternative data stops sounding technical and starts looking like what it really is: the evidence that helps a lender justify a yes.

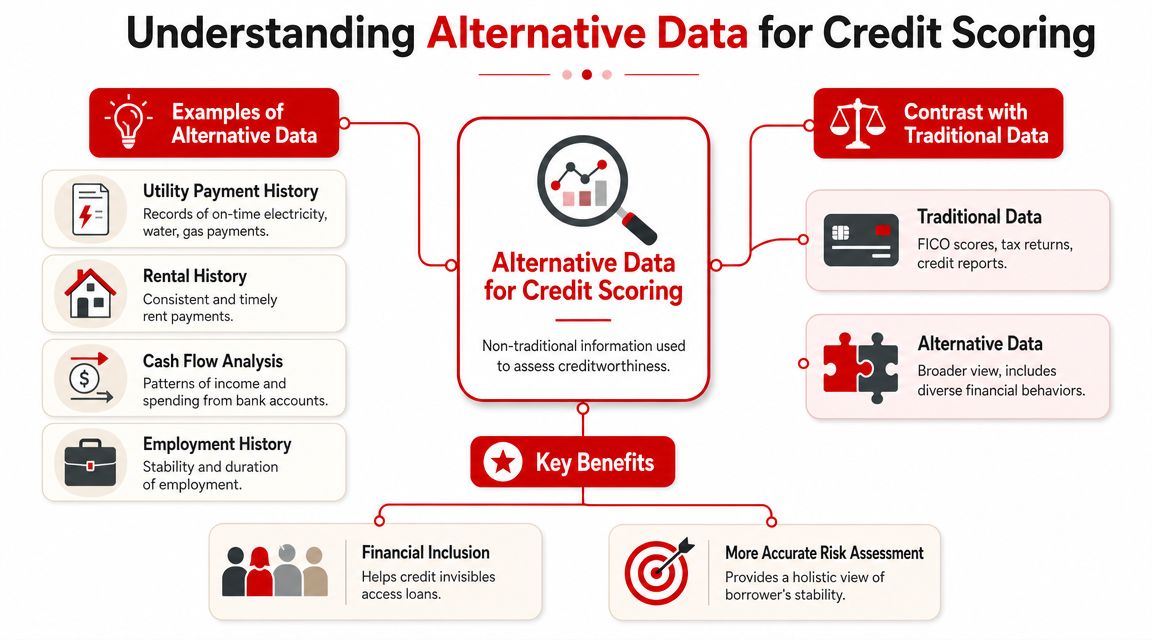

What Is Alternative Data for Credit Scoring

Alternative data for credit scoring is any nontraditional information a lender uses to assess creditworthiness beyond the standard mix of bureau files, tax returns, and conventional credit application data. In business lending, that usually means looking at how the company operates day to day.

Think of traditional data like an old report card. It shows a limited set of grades from the past. Alternative data looks more like a live digital portfolio. It shows current performance, patterns, consistency, and whether the business is functioning with discipline right now.

A static snapshot versus a live operating picture

Traditional underwriting still has value. Credit reports, tax filings, and financial statements can reveal history and structure. The problem is timing. Those records often lag behind the borrower's current condition.

Alternative data adds a more current and practical layer. It can include rent payments, utility payments, telecom history, and bank transaction behavior. Its importance became unmistakable when adoption of these methods made it possible to score more than 50 million U.S. consumers who had previously been unscoreable, while the World Bank reported that various combinations of alternative data can improve predictive power by 5% to 20%, and cited a FICO study showing that alternative data used alongside traditional data could accurately score more than 50% of previously unscorable applicants using signals such as rent and utility payments, as explained by the Urban Institute's discussion of alternative data in credit scoring.

For brokers, the consumer example matters because it proves the broader point. When the file is thin, incomplete, or misleading, nontraditional signals can fill the gap.

Why this matters for brokers

A broker doesn't need to become a data scientist. The practical job is simpler. The broker needs to recognize when standard paperwork is underselling a borrower and when alternative data can tell the stronger story.

That usually happens in cases like these:

- Young businesses with traction: The company lacks long operating history but shows healthy recent deposits.

- Owners with weak personal credit: The business is performing better than the owner's bureau file suggests.

- Businesses with irregular cycles: Revenue isn't smooth every month, but the inflows still support repayment over time.

Practical rule: If the business looks stronger in its bank activity than it does on paper, alternative data deserves attention.

This is why many modern lenders ask for account connectivity or recent statements early in the process. They're not being difficult. They're trying to see the business in motion.

For a broker, that's an advantage. The better the broker understands what alternative data reveals, the easier it becomes to prequalify deals, set owner expectations, and send files to lenders that can interpret real operating behavior instead of rejecting it.

The Key Alternative Data Sources for Business Lending

Not all alternative data is equally useful. Brokers close more deals when they understand which data sources help underwriting and what each one proves. The point isn't to collect everything. The point is to collect the right evidence for the right deal.

What lenders actually want to see

In small business lending, the most valuable nontraditional signals usually answer four questions. Does the business generate cash consistently? Does it pay core obligations reliably? Does the revenue source look stable? Can the lender verify the operating story without guessing?

Cash-flow and account activity are central because they're current. According to Plaid's overview of alternative credit data, traditional credit scores are often updated monthly, while account data can provide a near-real-time view of income, spending, and liquidity, which can help lenders distinguish risk more precisely, especially for thin-file or no-file applicants.

Payment history outside the banking system also carries weight. Utility, telecom, and rental data are highly predictive because they act as proxies for financial discipline outside traditional credit files, and telecommunication payment history in particular has been highlighted as high-quality and predictive in FICO's guidance on alternative data in credit risk analytics.

That matters in business lending because many owners don't present clean bureau-driven profiles, but they still keep the lights on, the internet active, and the rent paid.

Alternative Data Sources for Small Business Lending

| Data Category | Examples | What It Proves to a Lender |

|---|---|---|

| Bank transaction data | Deposits, withdrawals, balance patterns, recurring expenses | The business has active cash movement, liquidity patterns, and observable operating rhythm |

| Utility and telecom payments | Electric, water, gas, phone, internet bills | The company maintains essential obligations consistently and shows operational discipline |

| Rental payment history | Office, warehouse, storefront, equipment space rent | The business can handle recurring fixed commitments tied to ongoing operations |

| Platform and processor records | Marketplace payouts, merchant processing activity, subscription receipts | Revenue is tied to real commercial activity that can be tracked and verified |

| Administrative and business records | Licensing, registrations, invoicing patterns, bookkeeping consistency | The business is functioning as an ongoing enterprise rather than a one-off application |

A newer broker should read that table like an underwriter. Every data type tells a story.

A steady pattern of deposits suggests repeat customer demand. Utility history suggests the company manages routine obligations. Platform records can validate revenue when tax returns lag behind current performance. Rental history can show consistency even when bureau data is thin.

For files built around bank activity, clean transaction labeling matters more than many brokers realize. When categories are messy, lenders spend time interpreting noise instead of assessing strength. Resources such as a transaction identification API are useful for understanding how transaction streams can be classified into something more readable and decision-friendly.

A lender says yes faster when the file answers basic questions without forcing the underwriter to reconstruct the business by hand.

This is also where product fit matters. A company with reliable receivables but uneven owner credit may belong in a different lane than a company funded on daily card volume. Brokers working those files should understand how accounts receivable lenders evaluate underlying payment sources, because receivables quality can matter as much as the borrower's headline profile.

How Lenders Use Alternative Data to Say Yes

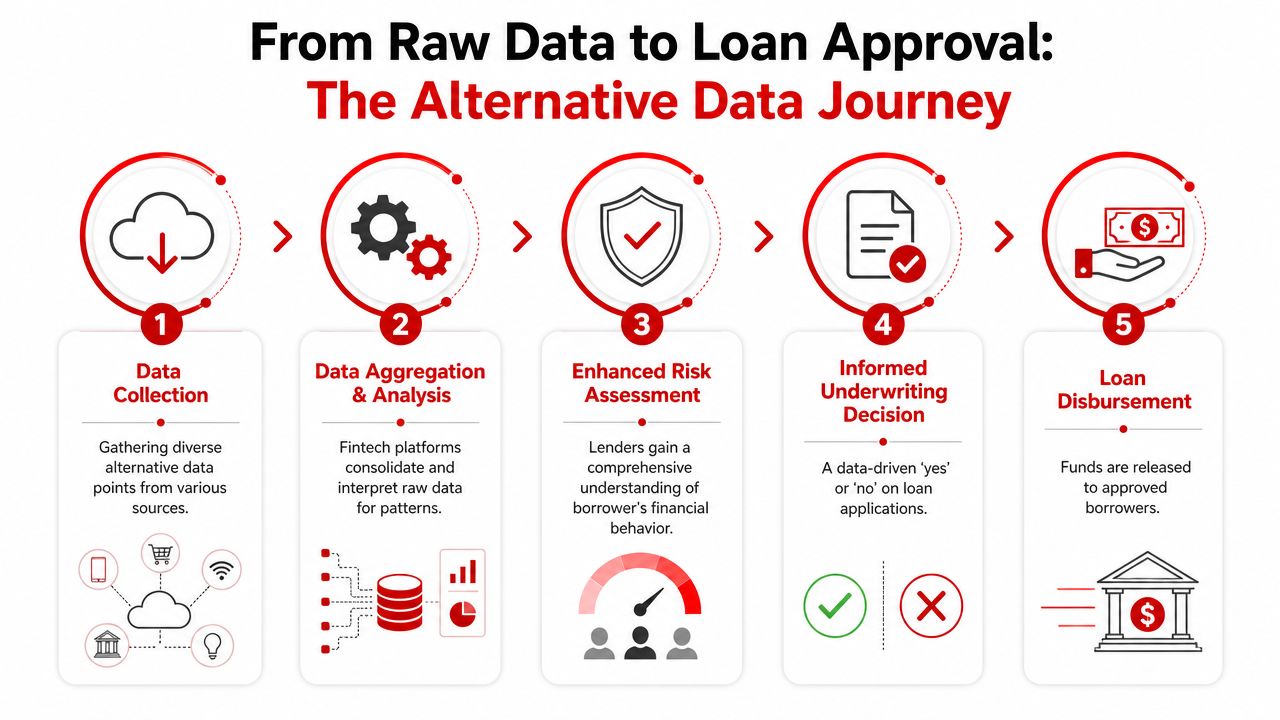

Lenders don't approve deals because raw data exists. They approve deals because the data forms a repayment story they can trust. The underwriting process turns activity into patterns, patterns into risk signals, and risk signals into a decision.

From account connection to underwriting decision

A typical file starts with permissioned access to account data or submission of recent bank statements. The lender reviews inflows, outflows, balances, recurring expenses, and irregularities. Then the lender compares those patterns with the requested payment structure.

Alternative data changes outcomes. In a Peru study using retail transaction data and administrative records, adding the alternative dataset increased simulated credit-card approval rates for applicants with no credit history from 16% to between 31% and 48%, while approval rates for borrowers with established credit stayed near 88%, according to the published research on transaction-based alternative data and access to credit. The lesson for brokers is direct. Better operating data can widen access without broadly rewriting decisions for already clear-cut borrowers.

A lender reviewing a small business file may ask questions like these:

- Deposit behavior: Are revenues recurring or random?

- Expense stability: Do normal operating obligations appear manageable?

- Liquidity pattern: Does the account routinely crash near zero, or does it maintain some cushion?

- Business reality: Do the transactions match the story presented in the application?

A business can fail a traditional screen and still pass this kind of review. That's where “invisible prime” borrowers come from. On paper, they look weaker than they are. In motion, they look fundable.

Why clean data matters

Alternative underwriting isn't magic. It still breaks when the data is incomplete, mislabeled, or inconsistent with the application. That's why disciplined brokers package files carefully.

If a business uses several accounts, the broker should identify the primary operating account. If personal and business expenses are mixed, the broker should explain the pattern instead of hoping underwriters ignore it. If deposits are seasonal, the broker should say so before the lender assumes volatility means distress.

Teams that work with structured data pipelines often use formal rules to ensure reliable data for your team, and the same principle applies here. Clear definitions, consistent fields, and fewer surprises produce faster decisions.

Clean presentation doesn't create borrower quality. It reveals it.

A broker who understands repayment coverage also gives the lender a stronger narrative. Reviewing debt service coverage ratio calculation helps connect raw cash-flow evidence to the lender's core question: can this business realistically support the new obligation?

Your Blueprint for Using Alternative Data as a Broker

The biggest mistake new brokers make is treating alternative data like a backup plan. It's better viewed as a placement strategy. Some files should go to alternative-data-driven lenders first because that approach matches the borrower's reality better than conventional underwriting ever will.

The opportunity is especially strong in small business lending. The Federal Reserve notes that cash-flow data improves underwriting speed, accuracy, and access for underserved borrowers, and that lens helps lenders identify “invisible prime” borrowers who may appear subprime under traditional reports but stronger when cash-flow is included, as discussed in the Federal Reserve's consumer and community context publication.

Which clients fit this model best

Some borrowers wave a clear signal that alternative underwriting is the right fit.

- A business with strong deposits but weak owner credit. The personal score may scare a bank, but the company's operating account may support a different decision.

- A young company with fast traction. Time in business is short, yet recent revenue activity shows momentum.

- An operator with mixed accounts. The file is messy, not necessarily weak. Good explanation and documentation can still make it workable.

- A platform-based seller or service business. Revenue may flow through processors, marketplaces, or recurring subscriptions rather than a traditional invoicing model.

The common thread is simple. The business looks better in live operations than in legacy paperwork.

How to position the process with business owners

Many owners hesitate when asked for account connectivity or detailed statements. They assume the lender is invading privacy or looking for a reason to decline. The broker's job is to reframe that request properly.

Good talking points sound like this:

- This helps the lender see current performance. Old returns don't always reflect what the business is doing now.

- This can help a thin or messy file. If the business is stronger than the credit report suggests, this gives underwriting more to work with.

- This can reduce back-and-forth. Cleaner access to operating data often means fewer document chases.

The broker who explains why the lender wants the data usually keeps the client calm. The broker who just forwards a checklist usually creates resistance.

It also helps to organize the file before submission. A current business debt snapshot, recurring obligations, and any unusual account behavior should be explained early. A simple review of what a debt schedule is often gives brokers the structure they need to present the borrower's obligations clearly.

How a broker turns data into funded deals

Consider two common examples.

A food truck owner gets declined by a bank because personal credit is bruised and tax returns don't fully capture current momentum. But recent account activity shows steady deposits from regular operating days, recurring inventory purchases, and consistent core bill payments. That file may still fit with a lender that underwrites recent operating behavior.

An online seller has limited conventional borrowing history, but processor payouts and account inflows show active commerce. The business may not look strong through a bureau-first lens, yet it can look much stronger when underwriting follows revenue flow.

The broker's practical playbook is straightforward:

- Spot the mismatch early. If the traditional file looks weaker than the operating reality, don't force it into a bank box.

- Collect decision-grade data. Statements, account context, payment patterns, and a clean explanation matter.

- Match the lender to the evidence. Use the lender whose model fits the file, not the lender that sounds most familiar.

- Set expectations clearly. Alternative data can improve access and pricing quality in the right cases, but it doesn't fix a business with unstable fundamentals.

- Protect trust. Work with reputable funding sources, explain disclosures, and avoid overselling approvals.

That last point matters. Alternative data is powerful, but it doesn't replace judgment. A broker still has to separate a temporary cash crunch from a structurally weak business. The best brokers don't push every file. They identify the deals where better data reveals a borrower worth funding.

Start Your Broker Business with a Modern Edge

A broker who understands alternative data isn't just learning a technical trend. That broker is learning how modern lending works for the businesses banks leave behind.

That creates a sharper business model. More deals become salvageable. More business owners see real options after a decline. More referral partners trust the broker who can find funding paths for files that looked dead a day earlier.

Why this creates a durable advantage

Traditional-only brokers are limited by traditional outcomes. If the bank says no, their pipeline shrinks. A broker who understands cash-flow-based underwriting, nontraditional payment signals, and lender fit can keep working the file.

That matters for anyone building a home-based, referral-driven brokerage. The work can be done remotely. The client need is constant. Small businesses always need capital for inventory, payroll, equipment, expansion, and working capital gaps. A broker with a broader underwriting lens can serve more of that demand.

The business case for learning this now

Alternative data for credit scoring gives newer brokers a real edge because it rewards understanding, not just contacts. A broker who knows how to read the borrower's operating story can compete without coming from a banking background.

That's good for the client and good for the broker's long-term business. Better placement skill leads to more funded deals, stronger referral relationships, and a reputation for solving difficult files instead of recycling obvious ones.

The industry doesn't need more order takers. It needs brokers who can interpret what lenders are really buying: repayment ability, demonstrated through the clearest evidence available.

Business Lending Blueprint shows aspiring and growing brokers how to build that kind of business from home with practical training, lender insight, and a repeatable system for helping business owners secure funding. To learn how to build a modern, flexible, referral-driven broker business, watch the free training from Business Lending Blueprint or schedule a strategy session.