A new broker usually sees the same scene in the first week. A business owner calls in a panic. Payroll is close. Inventory needs to be bought. A truck, oven, or key machine just went down. The owner already tried the bank and got nowhere. The problem isn't demand for funding. The problem is that most owners don't know where to go next, and most rookie brokers don't know how to guide them.

That gap is the business.

Fast approval business loans aren't just a product category. They're a practical entry point into a home-based, referral-driven brokerage business that solves urgent problems for small business owners. For aspiring entrepreneurs, consultants, sales professionals, CPAs, bankers, and anyone looking for a recession-resistant income stream, this niche offers something rare: clear client demand, remote flexibility, repeatable processes, and commissions tied directly to funded deals.

Table of Contents

- Why Fast Funding Is a Golden Ticket for Brokers

- Mapping the Fastest Funding Routes for Your Clients

- Your Client's Pre-Approval Document Checklist

- From Application to Cash The 72-Hour Funding Timeline

- Speed Up Approvals and Avoid Common Pitfalls

- Ready to Build Your Own Lending Business

Why Fast Funding Is a Golden Ticket for Brokers

The fastest path to becoming useful as a broker is learning how to solve urgent funding problems. Owners rarely shop for fast money because it sounds exciting. They shop for it because the usual channels failed them and time ran out.

That's where a professional broker becomes valuable. Instead of handing out a generic application and hoping for the best, a broker screens the situation, packages the file correctly, and routes the client to lenders built for speed. That service matters because the traditional system leaves a huge opening. Data shows only 13.8% of small company loans are approved by large banks, and a mere 44% of applicants receive full approval. This rejection chasm necessitates a pivot to non-bank lenders, which utilize AI to make decisions in hours and fund borrowers with credit scores as low as 500 according to Bankrate's review of fast business loan approval patterns.

Why urgency creates broker opportunity

A broker doesn't need to manufacture demand in this market. The demand already exists. The owner with a short cash window is already motivated. What's missing is guidance.

A skilled broker does three things that amateurs don't:

- Qualifies the problem: Is this a payroll gap, a repair issue, a seasonal slowdown, or a growth opportunity with a short deadline?

- Matches speed to structure: Not every urgent need should be solved with the same product.

- Protects the borrower: Fast money can fix a problem or create a worse one. The broker's value sits in knowing the difference.

Practical rule: The owner doesn't pay for information. The owner pays for speed, clarity, and access.

Why this business fits remote entrepreneurs

This model works well for people building from home because it's driven by conversations, document collection, lender matching, and referral relationships. It doesn't depend on a storefront. It doesn't require a giant staff to get started. It rewards consistency and judgment.

It also scales cleanly. One funded client can become a repeat borrower, a referral source, or both. That's why many recruits start by learning the funding side and later build broader relationships around accounting firms, consultants, insurance agents, real estate professionals, and local business communities. Anyone curious about the economics behind that model can review this breakdown of business loan broker salary.

Fast approval business loans give a new broker something even more important than speed. They create relevance on day one.

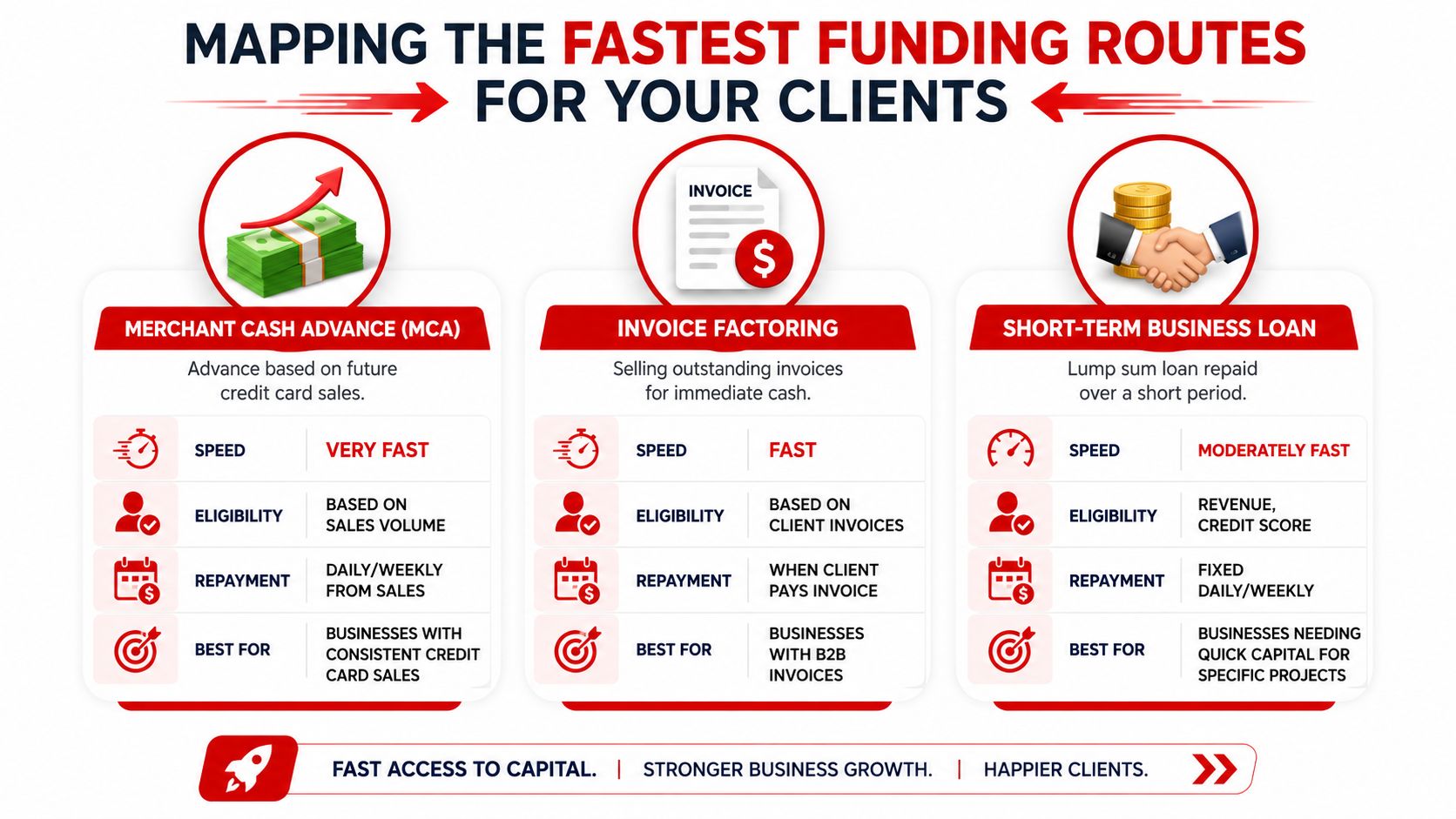

Mapping the Fastest Funding Routes for Your Clients

A rookie broker loses deals by treating every urgent borrower the same. A professional sorts the file by repayment source, deal purpose, and tolerance for payment frequency. That's the map.

The speed advantage sits with alternative lending. Online lenders approve 26–30% of small business loan applications, more than double the 13–15% rate of large banks. Their key advantage is speed, with funding delivered in 1–7 days, and often within 24–72 hours, compared to 30–90 days for traditional banks, based on small business lending statistics compiled by Crestmont Capital.

Merchant cash advance

This is usually the fastest route when the business has strong sales volume and needs money immediately. The advance is tied to future receivables rather than structured like a conventional loan.

Best fit:

- High card or steady sales businesses: Restaurants, retail, service businesses, and other operators with frequent incoming revenue.

- Short-window emergencies: Equipment repair, tax pressure, inventory shortages, or payroll timing issues.

- Borrowers with weak bank options: Especially when the owner won't pass traditional underwriting.

Weak point: repayment pressure. If the revenue stream is unstable, the product can become painful fast.

Invoice-based funding

This route makes sense when the borrower has unpaid business invoices and solid customers, but can't wait to collect. The underwriting focus shifts toward receivables quality rather than the owner's full credit profile.

Good fit:

- B2B firms with slow-paying clients

- Businesses growing faster than cash flow

- Owners who need working capital without waiting on net terms

A sharp broker asks one question early. Is the business cash-poor because it's weak, or cash-poor because customers pay slowly? That answer changes the product path.

Short-term business loan

This is often the cleanest middle ground. The client gets a lump sum and repays on a shorter schedule. It's still fast approval territory, but usually easier to explain than receivables-based products.

A short-term structure tends to work when the borrower needs money for a defined purpose:

- A one-time project such as a renovation or contract mobilization.

- A time-sensitive purchase like discounted inventory.

- A temporary operating gap that should normalize with incoming revenue.

The best fast funding route isn't the one that closes fastest. It's the one the client can survive after funding lands.

Traditional routes aren't built for urgency

Banks and SBA-style financing have a place. They're often better when the borrower has time, stronger documentation, and a need for longer-term structure. They are not built for a business owner who needs capital right away.

That's why a broker should keep product selection practical. Fast approval business loans are often the right move for urgency. Long-term products are the right move for stability. Confusing those two is how bad placements happen.

For brokers who want broader context on asset-backed and speed-driven financing paths, this overview of hard money commercial loan structures adds another useful lens.

Your Client's Pre-Approval Document Checklist

Most funding delays start before underwriting ever touches the file. The broker submitted a half-built package, the lender asked for cleanup, and the client disappeared for a day chasing paperwork. That's amateur work.

A professional broker gathers the file first, then shops it.

The documents that matter most

Fast lenders move quickly when the application is complete and credible. Missing paperwork slows everything down and makes the borrower look disorganized. The basic package should be assembled before any serious submission goes out.

| Document | Why It's Needed | Broker's Tip |

|---|---|---|

| Bank statements | Underwriters use them to verify cash flow trends and deposit activity. | Check consistency: Make sure the statements cover at least one year and match the business entity applying. |

| Tax returns | They help confirm historical business performance. | Review before sending: Watch for missing pages, unsigned returns, or numbers that conflict with the bank activity. |

| Current P&L statement | It shows how the business is performing now, not just in past tax years. | Keep it recent: If the P&L is stale, the lender may question whether the business has changed. |

| Budget | It gives context for how the business manages expenses and upcoming obligations. | Tie it to reality: The budget should support the stated use of funds. |

| Cash flow projections | Lenders want to see how repayment fits future business activity. | Don't overcomplicate it: Clear and believable beats fancy. |

| Basic business information | Ownership details, legal entity data, and operating background help validate the file. | Match all records: Business name, address, and entity details should be identical across documents. |

| Voided business check or bank verification item | It helps confirm where funds should be deposited. | Get it early: Waiting until approval to collect this creates unnecessary friction. |

Why complete files move faster

Funding delays of 72 hours or more are statistically common when an application is incomplete. Fast-approval lenders, who typically fund within 24 to 72 hours, prioritize verified cash flow and will only move quickly on applications that have all necessary documents, like bank statements and tax returns, submitted correctly from the start, according to Fora Financial's guidance on instant approval business loans.

That one fact should shape a broker's entire intake process.

Broker move: Don't ask, “Can this client apply?” Ask, “Is this file submission-ready?”

What underwriters are really checking

New brokers tend to focus too heavily on the owner's verbal story. Underwriters don't lend on stories alone. They compare the story to the documents.

A clean intake call should verify:

- Use of funds: The stated need should make business sense.

- Revenue behavior: Deposits should support the requested payment burden.

- Document alignment: Tax returns, P&L, and statements shouldn't tell three different stories.

- Bankability: The business account should reflect operating activity, not chaos.

If a debt picture needs to be organized before packaging the deal, this breakdown of what is a debt schedule helps frame liabilities clearly for underwriting.

A broker's reputation with lenders is built on file quality. Send junk files and the lender stops taking the broker seriously. Send organized, complete packages and the lender starts responding faster.

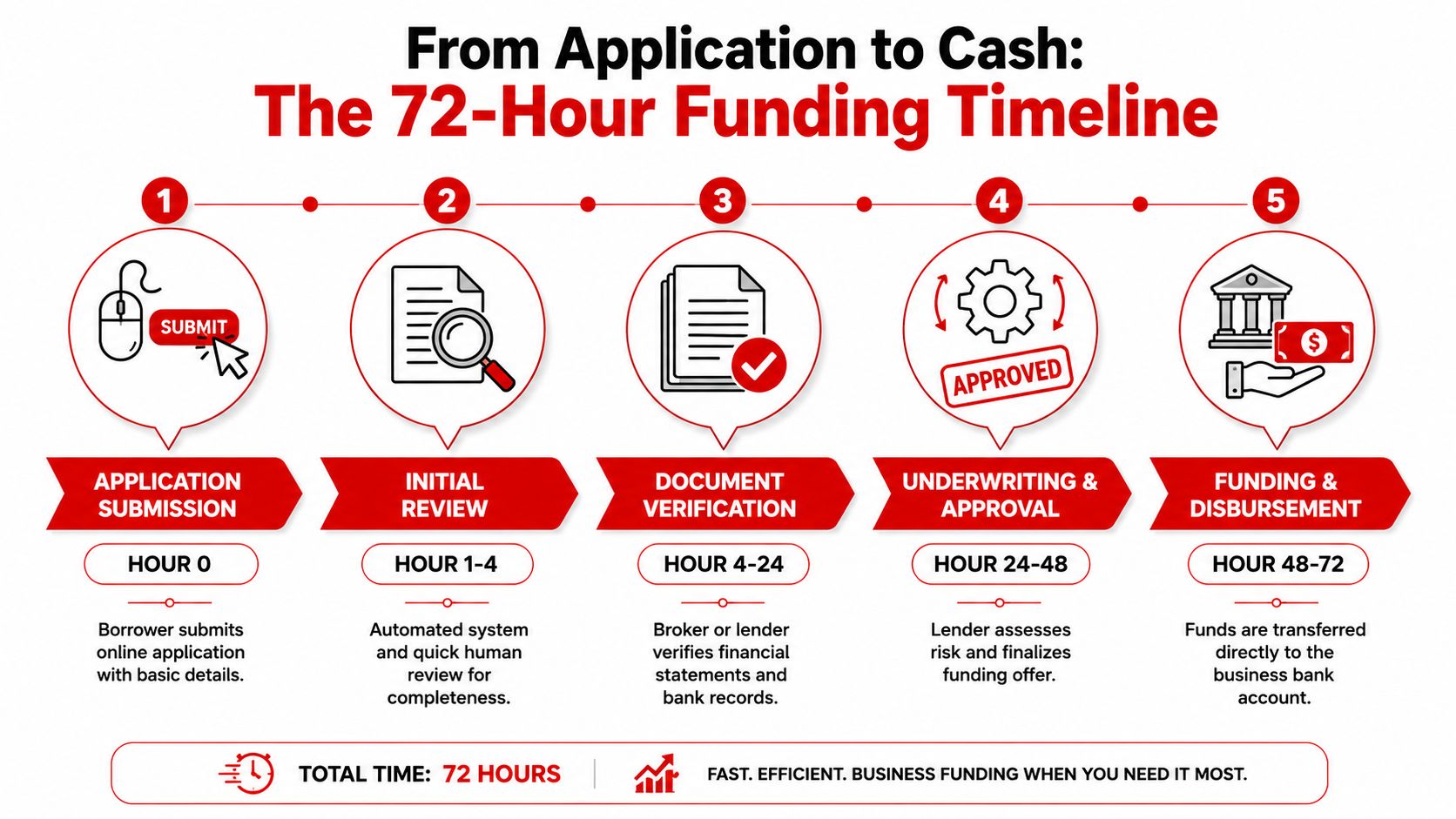

From Application to Cash The 72-Hour Funding Timeline

Once the file is clean, the funding process becomes very predictable. Not guaranteed. Predictable. A disciplined broker knows what should happen next, what can go wrong, and where to step in before momentum dies.

Hour 0 to initial review

The client submits the application, or the broker submits on the client's behalf using a complete package. In the first pass, the lender checks whether the file is usable. That means identity, business basics, cash flow visibility, and document completeness.

At this stage, the broker's real job is quality control. If the numbers don't line up or a statement is missing pages, the broker should catch it before the lender does.

Hour 4 to document verification

Weak files start to wobble as the lender verifies statements, tax documents, and operating details. Some files move quickly because the paperwork is clean. Others stall because the borrower uploaded screenshots, partial PDFs, or mismatched business records.

A strong broker stays close during this window and keeps the borrower responsive. Silence kills speed.

Hour 24 to approval decision

The lender weighs risk, sets terms, and decides whether to issue an offer. If the file supports repayment and the business story makes sense, an offer can arrive quickly. If questions show up, the broker has to answer them fast and cleanly.

The best brokers don't just forward the offer. They translate it.

- Confirm the structure so the client understands what's being offered.

- Check payment frequency against the client's real cash cycle.

- Re-state the purpose so the client doesn't take expensive money for the wrong reason.

Borrowers don't panic because underwriting is complicated. They panic because nobody explains what happens next.

Hour 48 to cash in bank

After acceptance, the final stage usually involves signing, funding verification, and disbursement to the business bank account. During this stage, small mistakes still cause large delays. A wrong account detail or an unsigned item can push funding back.

The timeline only works when the broker manages expectations correctly. A fast lender can move in a day or two, but only if the borrower behaves like someone who wants fast money. That means answering calls, reviewing documents, and signing quickly.

A recruit who understands this timeline can control the client conversation better. Instead of saying “it depends” all day, the broker can explain the sequence, set deadlines, and keep the borrower engaged from submission to funding.

Speed Up Approvals and Avoid Common Pitfalls

Closing a fast deal is good. Closing a deal that helps the client and preserves the relationship is what separates a pro broker from a commission chaser.

This is also where the business gets profitable. Business loan brokers typically earn commissions from 1% to 5% of the total loan amount. On a $150,000 funded deal, a 1-point commission (1%) would generate $1,500, while a 4-point commission would generate $6,000 for the broker, as outlined in SoFi's explanation of business loan broker compensation. Those numbers are meaningful, but they only matter if the broker keeps getting referrals instead of complaints.

The fastest way to slow a deal down

The biggest mistake is sending a file to the wrong lender category. A borrower with unstable revenue shouldn't be pushed into a structure that demands relentless payment pressure. A borrower with receivables shouldn't be treated like a generic term-loan applicant. Product mismatch creates denials, confusion, and wasted time.

The next mistake is a weak use-of-funds explanation. Underwriters don't need a novel. They need a clean business reason that connects directly to repayment capacity.

Good summaries usually include:

- Specific purpose: equipment repair, inventory purchase, payroll bridge, contract mobilization

- Clear timing: why the funds are needed now

- Plausible repayment story: how cash flow supports the obligation

- Clean amount logic: why the request size makes sense

The trap hidden inside speed

Fast approval business loans can become destructive when the repayment structure is ignored. Some products collect frequently enough to squeeze the client's operating cash before the business has time to breathe. A rookie broker sees the approval and celebrates. A professional asks whether the business can live with the payment cadence.

That's where judgment matters most with bad-credit files. Some fast lenders consider borrowers with lower credit profiles, but lower credit should never be treated as permission to ignore affordability. The right move is often to pursue the safest workable option, not the first one willing to send paper.

Hard truth: A funded deal that hurts the client destroys more long-term income than a declined deal handled honestly.

How pros protect both the client and the pipeline

A disciplined broker does a few things every time:

- Pre-frames cost clearly: Fast money usually costs more. Clients can handle that if the use of funds justifies it.

- Screens repayment rhythm: Daily or frequent payments can work for some revenue models and wreck others.

- Keeps alternatives alive: One lender path is rarely enough on a tougher file.

- Documents the story well: Good packaging speeds underwriting and builds lender trust.

This is why training matters. A structured system helps recruits identify what lenders care about, how to present revenue correctly, and how to read the difference between a workable approval and a future default. For brokers learning how nontraditional underwriting interprets borrower quality, alternative data for credit scoring is a useful concept to understand early.

The broker who wins long term

The best broker in this field isn't the one who talks the most. It's the one who filters noise, protects the client from bad fit products, and gets legitimate deals funded quickly. That creates referrals from borrowers, accountants, consultants, and local professionals who see that the broker solves problems instead of creating them.

That's how a home-based brokerage grows into a real business. One funded deal brings revenue. One well-handled deal brings a pipeline.

Ready to Build Your Own Lending Business

A person doesn't need decades in banking to build a brokerage around fast approval business loans. What's needed is process discipline, lender-fit judgment, and the ability to communicate clearly with business owners under pressure. Those are learnable skills.

This niche appeals to a wide range of people for a reason. Salespeople like it because it rewards responsiveness. Consultants and CPAs like it because clients already trust them with financial conversations. Career changers like it because the model can be run remotely with low overhead. Entrepreneurs like it because the business can scale through referrals instead of depending on constant cold outreach.

Why the model has staying power

Small businesses will keep needing capital outside the bank channel. Some need speed. Some need flexibility. Some need a guide who knows how to present their file properly. That creates a durable opening for brokers who can serve borrowers well and maintain strong lender relationships.

A disciplined broker also learns when not to force a fast product. Some clients are better served by preparing for a stronger long-term option later. For borrowers working toward that path, it helps to understand ways to improve SBA loan approval odds before they apply.

A practical next step

For someone entering the industry, a training platform should provide more than theory. It should show the intake process, file packaging, lender submission flow, referral strategies, and compliance basics in plain language. Business Lending Blueprint teaches people how to launch and grow a business loan brokerage, including how to work with alternative lenders, build referral-driven deal flow, and operate remotely around real client needs.

That matters because this business rewards execution, not random effort. The brokers who last are the ones who build repeatable habits, protect clients from bad fits, and turn each funded deal into another relationship.

The next move is simple. Watch the free training at Business Lending Blueprint or schedule a strategy session to see how a home-based business loan brokerage can be built around real demand, flexible work, and referral-driven growth.