A broker takes an application on Monday, gets an approval by Thursday, and assumes the client experience was solid because the funding arrived. Then the client goes silent. No second deal. No referral to their accountant or attorney. No introduction to another owner in the same industry. The file closed, but the relationship never matured into an asset.

That pattern shows up in a lot of home-based and independent brokerage businesses. Revenue looks acceptable for a while, but growth stays inconsistent because service lives in the broker's memory instead of a repeatable process. Strong customer care best practices fix that. They reduce avoidable confusion, protect lender relationships, and give referral partners confidence that sending a business owner your way will not create extra work for them.

In business lending, customer care is not about sounding friendly on calls. It is about building systems for communication, discovery, education, documentation, and follow-up that hold up under pressure. That is especially true in a referral-driven model, where one missed update or vague expectation can cost far more than a single commission check.

Business loan brokerage fits a remote, flexible business model well, but only when service is deliberate and documented. This guide for superior customer experience supports that broader principle from a service operations perspective. Good intentions help. A process gets repeat business.

The framework below focuses on the practices that help brokers build trust, earn repeat clients, and turn funded deals into long-term referral relationships.

Table of Contents

- 1. Build a Referral-Driven Communication System

- 2. Develop a Needs-Based Discovery Process for Business Owners

- 3. Create a Transparent Communication Timeline with Clients

- 4. Implement a Multi-Product Education Strategy

- 5. Build a Compliance and Documentation Checklist System

- 6. Develop a Post-Funding Follow-Up and Relationship Maintenance Strategy

- 7. Create a Proactive Communication Protocol for Lender Updates and Changes

- 8. Establish Clear Communication Channels and Response Time Standards

- 9. Build a Client Success Stories and Testimonial Library

- 10. Design a Proactive Problem-Solving and Escalation Protocol

- 10-Point Customer Care Best Practices Comparison

- Build Your Business on a Foundation of Trust

1. Build a Referral-Driven Communication System

A broker who only reaches out when a deal is needed trains the network to ignore them. A broker who shares useful guidance all year becomes part of the referral ecosystem.

That system can be simple. A monthly lending update for accountants, a quarterly lunch-and-learn for consultants, and short check-ins with funded clients often do more than random prospecting bursts. For a home-based broker, this structure creates consistency without forcing constant outreach.

Build rhythm, not noise

The best communication systems are predictable and useful. They aren't daily messages or vague "checking in" emails. They deliver something a referral partner can use with clients right away.

- Segment the network: Separate past clients, CPAs, consultants, bankers, and strategic partners so each group gets relevant updates.

- Assign touchpoints: Put outreach on a yearly calendar with specific days for emails, calls, and review reminders.

- Lead with value: Share lender guideline changes, common funding mistakes, or product fit examples instead of asking for referrals every time.

Practical rule: Stay visible before someone needs capital, not after the problem has already turned urgent.

Many brokers secure their initial scalable advantage through this approach. Business Lending Blueprint teaches a referral-driven model for a reason. Warm relationships compound. Cold outreach usually burns time.

2. Develop a Needs-Based Discovery Process for Business Owners

Many brokers lose trust in the first conversation because they start matching products before they understand the problem. Business owners can feel that immediately.

A stronger approach uses a repeatable discovery process. The broker asks about timeline, use of funds, current cash flow pressure, business stage, credit profile, and what success looks like after funding. That keeps the conversation consultative instead of transactional.

Ask questions that change the recommendation

A restaurant owner needing seasonal working capital doesn't have the same need as a contractor replacing equipment or a retailer bridging inventory timing. A structured intake form helps uncover that difference early.

A broker might learn that the client asking for a term loan needs a line of credit, or that the owner chasing "funding" really needs a smaller facility with better payment flexibility. In tougher files, product education also matters. Borrowers with challenged profiles often need a realistic discussion around business loan options for bad credit before expectations get too far ahead of approvals.

- Start with use of funds: Expansion, payroll, equipment, inventory, and consolidation each point toward different lending paths.

- Qualify early: If the deal doesn't fit current lender appetite, say so quickly and redirect instead of dragging the file along.

- Document everything: Notes inside the CRM should capture business goals, objections, and personal details that matter in follow-up.

Good discovery lowers friction later because the client doesn't have to repeat the story every time a lender asks another question.

Strong customer care best practices aren't just about being responsive. They're about making fewer bad recommendations in the first place.

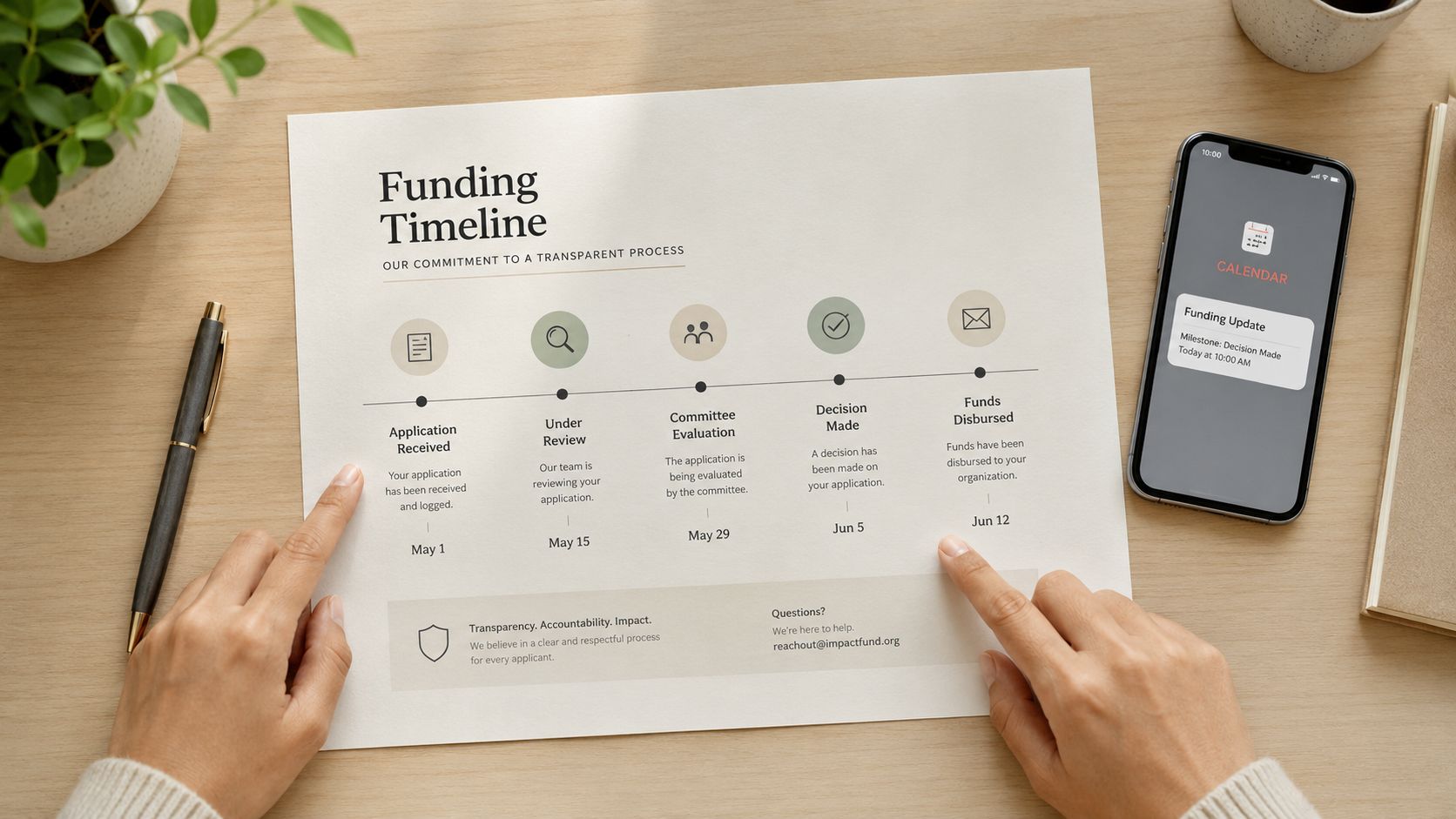

3. Create a Transparent Communication Timeline with Clients

A borrower submits documents on Monday, hears nothing by Thursday, and starts wondering whether the file is stalled, declined, or sitting in someone's inbox. By Friday, that uncertainty turns into extra calls, duplicate emails, and sometimes a conversation with another broker who appears to have a tighter process.

A transparent timeline prevents that drift. It gives the client a working view of the process, who owns each step, what usually triggers delays, and when the next update will arrive.

Replace uncertainty with milestones

A one-page funding timeline clears up more confusion than long email threads ever will. It should show intake, initial review, packaging, submission, lender response, conditional approval, final stipulations, and funding. It should also show what the client needs to do at each stage, because delays often come from missing documents, unsigned forms, or tax returns that arrive in pieces.

In a referral-based brokerage, this matters for more than convenience. Referral partners remember whether their client felt informed. A clean process earns confidence. A vague process creates cleanup work for everyone involved.

The timeline also needs honest ranges, not best-case promises. If underwriting usually takes two to four business days, say that. If lender feedback can pause while bank statements or ownership documents are reviewed, say that too. Clients handle bad news better than surprise.

For brokers who want a cleaner framework, this guide on how to manage client expectations is worth applying directly to the funding process.

- Send updates before the client asks: A scheduled weekly status note cuts down on check-in emails and shows the file is being managed.

- Name the reason for delays clearly: If the lender is waiting on clarification, if underwriting volume is heavy, or if a document was rejected, explain that directly.

- Assign ownership to each step: The client should know whether the next update is coming from your office, the processing team, or the lender.

- Set the next checkpoint every time: Each communication should end with a specific date or trigger for the next update.

There is a trade-off. Proactive communication takes discipline, CRM hygiene, and follow-through from the team. But it protects pull-through, reduces client stress, and makes your operation look structured enough to deserve repeat referrals.

4. Implement a Multi-Product Education Strategy

A broker limited to one or two familiar products will miss opportunities hiding in plain sight. Business owners often ask for the product name they know, not the solution that fits.

Education fixes that. Instead of reciting features, the broker teaches when a line of credit fits uneven cash flow, when equipment financing preserves working capital, and when revenue-based financing may be more practical than a rigid repayment structure.

Teach through decision paths

Short educational tools work better than long explanations. A one-page "Which funding option fits this situation?" guide, a webinar for accountants, or a product map for consultants gives referral partners language they can use.

This also strengthens customer care best practices because it reduces mismatch. When the client understands why a certain option fits the business, resistance usually drops and documentation gets easier.

The broker who explains trade-offs clearly becomes harder to replace than the broker who simply shops files.

A practical example is a manufacturer seeking growth capital. After education, the owner may realize that equipment financing for machinery and a separate working capital facility for operations is cleaner than forcing everything into one request. That kind of clarity creates trust and often opens future deals from the same relationship.

5. Build a Compliance and Documentation Checklist System

A deal can look strong on paper and still die in processing because the file is sloppy. One missing signature, an outdated bank statement, or unclear ownership structure is enough to slow underwriting and weaken lender confidence.

A checklist system prevents that. It gives the client a clear document path from day one and gives your team a repeatable review standard before the file ever leaves your office.

Standardization protects reputation

Strong brokers package files with the same care they use to structure the deal. They do not rely on memory, inbox searches, or whatever the borrower happened to send first. They use product-specific intake lists, internal review steps, and a submission standard that catches problems early.

That process also improves the client experience. A borrower who receives a focused document request tied to the actual loan scenario is far more cooperative than one who gets a generic list of twenty items with no explanation.

Three practices make this work:

- Create product-specific checklists: Equipment financing, SBA requests, and short-term working capital deals each require a different file structure.

- Track receipt and review status: Use a pipeline view or document workflow inside a CRM system for brokers so your team can see what is missing, what has been reviewed, and what still needs clarification.

- Run a pre-submission audit: Check signatures, dates, entity documents, explanations for credit issues, and lender forms before submission.

For smaller shops, Micro CRM solutions can help organize document collection without adding unnecessary complexity.

The trade-off is simple. Building the checklist takes time up front, but it saves far more time in rework, follow-up calls, and preventable lender declines. Clean files signal competence. In this business, that often determines whether a lender asks for your next deal or avoids it.

6. Develop a Post-Funding Follow-Up and Relationship Maintenance Strategy

A borrower gets funded on Friday. By Monday, the broker is chasing the next file, and the client hears nothing until renewal season. That gap costs deals.

Post-funding follow-up is where brokerage revenue becomes predictable. The goal is not to “check in” for the sake of politeness. The goal is to learn how the capital performed, spot the next financing need early, and stay close enough to earn the refinance, expansion request, and referral.

Build the next deal before the client is under pressure

Good brokers do not wait for a cash crunch to restart the conversation. They ask better operational questions while the outcome is still fresh. Did the inventory purchase fix the timing issue? Did the new truck increase capacity enough to justify a second unit? Is the business now hitting constraints in staffing, space, or equipment?

That information shapes the next recommendation and strengthens retention. Research from Salesforce's State of the Connected Customer found that customers expect companies to understand their needs and expectations. In a brokerage context, that means documenting what the capital was supposed to accomplish, then following up against that plan instead of sending a generic “just checking in” email.

Use a broker CRM system that tracks follow-up milestones so no funded client disappears into a closed-deal folder. Smaller shops can keep the same discipline with Micro CRM solutions if they need a lighter setup.

Three habits make this process profitable:

- Book the first review before funding is complete: A 30-day or 45-day follow-up scheduled in advance gets far better completion rates than an email sent later.

- Track business events, not just loan dates: Hiring plans, seasonal ramps, new contracts, equipment wear, and location expansion often reveal the next lending opportunity before the owner asks.

- Stay useful between transactions: An introduction to an accountant, insurance contact, or operations resource gives the client another reason to remember your name and mention you to other owners.

There is a trade-off here. Frequent outreach can feel forced if every message asks for another deal. A structured cadence solves that. One early implementation check, one later performance review, and periodic milestone-based outreach usually keeps the relationship active without becoming noise.

Brokers who treat funding as the midpoint of the client relationship build a stronger book of repeat business. Brokers who treat it as the finish line start every month from zero.

7. Create a Proactive Communication Protocol for Lender Updates and Changes

Lender appetite changes. Programs tighten. New products open. Documentation standards shift. Referral partners rarely track those changes closely, but they value the broker who does.

A proactive communication protocol turns market movement into relationship equity. Instead of waiting for a CPA or consultant to ask, the broker sends a short note when a lender changes credit expectations, adjusts product availability, or becomes more active in a niche.

Turn updates into usable guidance

The mistake is sending vague market commentary. The stronger move is sharing what changed and what it means for the business owner.

For example, if a lender starts leaning away from lower-credit files, the broker can alert referral partners to prepare stronger documentation or consider different product paths earlier. If equipment financing becomes more attractive for a certain profile, the broker can explain which clients may benefit now.

Referral partners don't need a market report. They need a clear answer to "Which clients should I send today?"

This is also where accessibility matters. Service guidance often overlooks disabled customers even though 1.3 billion people globally experience vision loss, and 87% of websites fail basic accessibility checks. Brokers who share updates through accessible formats, readable PDFs, clean emails, and screen-reader-friendly portals make communication easier for clients and partners who are frequently ignored by generic service systems.

8. Establish Clear Communication Channels and Response Time Standards

A borrower submits bank statements at 8:40 p.m., sends a text at 9:05, then follows up by email the next morning because they are not sure which channel you monitor. By noon, confidence is already slipping. In brokerage, confusion about communication feels like confusion about the file.

Clear channel rules prevent that slide. Set one primary channel for documents, one for scheduled strategy calls, and one for quick status coordination. Then publish response standards that fit the way you work. A broker who promises a two-hour response and misses it trains clients to worry. A broker who promises same-business-day replies and meets that standard builds trust.

This protects client experience and your own capacity. Business owners want access, but they also want consistency. Constant availability sounds helpful until it slows underwriting work, causes missed details, and turns every notification into a priority.

Use a simple service framework:

- Email for documents and file-specific instructions: It creates a record and reduces lost details.

- Phone or scheduled meetings for complex conversations: Product fit, lender concerns, and expectation-setting are handled better live.

- Text for short coordination only: Confirm receipt, request a callback, or flag a time-sensitive item.

- Published response windows: State them in your signature, intake email, and voicemail so clients do not have to guess.

The trade-off is real. More channels can make you look accessible, but too many channels usually create fragmented conversations and slower follow-through. Strong brokers do not offer every option. They offer the options they can manage well.

Automation has a place here, but only as support. The National University notes that 70% of consumers prefer interacting with a human over a chatbot when they need customer support, which is a useful reminder to keep live judgment at the center of client communication: research on customer preferences for human support. Auto-replies, scheduling confirmations, and document reminders help. Sensitive file updates, lender friction, and approval setbacks still need a real person.

One practical standard works well in a referral-based brokerage. Acknowledge every meaningful client message within one business block, even if the full answer comes later. That tells the borrower the file is active and gives referral partners confidence that their client did not disappear into a queue. You can see that same system-first discipline in these Business Lending Blueprint success stories, where clear process supports repeat business and referrals.

9. Build a Client Success Stories and Testimonial Library

A borrower gets funded, solves the immediate cash problem, and goes back to running the business. If no one captures what happened next, the brokerage loses one of its best referral assets.

Strong client care includes documenting outcomes after the deal closes. That work belongs in operations, not just marketing, because the best stories come from disciplined follow-up. Brokers who stay in touch hear the tangible result. Inventory pressure eased. Payroll stayed on track. A piece of equipment started producing revenue. Those details make future conversations with prospects and referral partners far more credible.

Document outcomes while they're fresh

Wait until the client has had enough time to put the capital to work, then ask focused questions. A vague request usually gets a vague quote. A structured prompt gets usable proof.

Ask for three things:

- the business problem before funding

- the product or structure that solved it

- the business result after funding

That format gives you a library you can use. Some stories fit a written testimonial. Others work better as a short video, a case summary, or a before-and-after snapshot with the client's approval. The goal is not volume. The goal is a set of specific examples that help the next borrower see what a well-run process can produce.

Use this library across the brokerage. Give referral partners examples that match their client base. Share relevant stories during sales conversations. Train team members on what strong outcomes look like in different industries and loan scenarios. The Business Lending Blueprint success stories show the kind of practical, outcome-based proof that supports a systemized, referral-driven brokerage.

A useful success story focuses on the business problem, the funding path, and the result. It should read like a real business case, not ad copy.

10. Design a Proactive Problem-Solving and Escalation Protocol

A borrower sends tax returns on Friday. By Monday, the debt service coverage is weaker than expected, one bank statement does not match the application, and the product discussed on the first call no longer fits the file. That is the point where a broker either protects trust or starts losing it.

Strong customer care in lending is not just fast replies. It is a clear protocol for spotting issues early, deciding who owns the fix, and giving the client a realistic path forward before the file stalls.

Solve the problem while options still exist

The best time to handle friction is before submission, not after an underwriter declines the deal. Review the file with an escalation mindset. Look for revenue inconsistencies, recent NSF activity, collateral gaps, ownership questions, and loan requests that are oversized for the business profile. Then decide what happens next.

In practice, that usually means one of four moves. Adjust the request. Gather support that closes the gap. Shift to a lender or product that fits the actual risk profile. Pause the file until the borrower can correct the issue.

High-friction moments need human communication. As noted earlier, borrowers may tolerate automation early in the process, but they expect direct access to a person when the stakes rise. In a brokerage, that means no vague status update and no silent handoff. The client should know what the issue is, what it affects, and what the next best option looks like.

A simple escalation protocol should cover:

- Pre-submission review: Catch obvious weaknesses before the lender does.

- Issue categories: Define common problems such as credit, cash flow, documentation, time in business, collateral, or use of funds.

- Owner and deadline: Assign who is responsible for the fix and when the follow-up happens.

- Alternative paths: Match each issue type to a backup product, revised structure, or supporting document set.

- Client communication standard: Explain the problem plainly, without blame or false reassurance.

Newer brokers often lose deals because they treat every problem as a one-off event. Experienced brokers build a repeatable decision tree. If coverage is short, they know whether to reduce the request, add a co-borrower, present stronger deposits, or move the file. If documentation conflicts, they know what must be clarified before the package reaches underwriting.

Underwriter relationships matter here too. A credible broker does not send messy files and hope for mercy. A credible broker submits a file with the weakness identified, the context explained, and the compensating factors organized. That approach gives the lender something useful to review and gives the client a better chance of getting to approval.

Handled well, a tough conversation often increases confidence. Business owners do not expect every deal to be perfect. They do expect their broker to see problems early, tell the truth, and bring solutions.

10-Point Customer Care Best Practices Comparison

| Strategy | Implementation Complexity | Resource Requirements | Expected Outcomes | Ideal Use Cases | Key Advantages |

|---|---|---|---|---|---|

| Build a Referral-Driven Communication System | Medium, process design and automation setup | CRM, email automation, content, time for regular touchpoints | Consistent warm lead flow and predictable recurring income over time | Brokers with existing networks aiming for steady growth | Lower acquisition cost, trust-building, works in varied markets |

| Develop a Needs-Based Discovery Process for Business Owners | Medium, training and scripted frameworks | Discovery forms, call guides, CRM documentation, practice | Higher close rates and better product-to-client matches | Consultative brokers handling diverse funding needs | Reduces mismatches, increases credibility and conversion |

| Create a Transparent Communication Timeline with Clients | Low–Medium, templates and coordination with lenders | Timeline templates, CRM reminders, lender coordination | Reduced client anxiety, fewer dropouts and complaints | High-touch deals or clients sensitive to process timing | Clear expectations, improved client satisfaction |

| Implement a Multi-Product Education Strategy | Medium–High, ongoing content creation and updates | Content library (blogs, videos), webinars, product charts | Expanded deal flow and referral opportunities from educated partners | Markets with many product options; referral partner education | Positions you as expert, scalable marketing asset |

| Build a Compliance and Documentation Checklist System | Medium, initial setup and training | Checklists, CRM tracking, document templates, review process | Faster approvals, fewer lender rejections and delays | Volume operations or lenders with strict documentation needs | Reduces processing time, improves lender relationships |

| Develop a Post-Funding Follow-Up and Relationship Maintenance Strategy | Low–Medium, scheduling and routine processes | CRM, scheduled check-ins, review templates, time for follow-up | Repeat business, referrals, higher lifetime client value | Brokers focused on retention and recurring commissions | Generates repeat commissions, strengthens referrals |

| Create a Proactive Communication Protocol for Lender Updates and Changes | Medium, monitoring and verification workflow | News/alert feeds, curated newsletters, verified lender contacts | Early opportunity capture and maintained market credibility | Fast-changing lending environments and referral networks | First-mover advantage, positions you as market expert |

| Establish Clear Communication Channels and Response Time Standards | Low, policy, templates and discipline | Scheduling tools, autoresponders, documented policies | Better professionalism, predictable response expectations | Home-based brokers and teams managing availability | Protects work-life balance, sets professional boundaries |

| Build a Client Success Stories and Testimonial Library | Medium, collection, editing, and permissions | Recording tools, consent forms, content editing, storage | Strong social proof and improved conversion rates | New brokers needing credibility; marketing campaigns | Persuasive proof, reusable marketing content |

| Design a Proactive Problem-Solving and Escalation Protocol | Medium–High, decision trees and lender relationships | Underwriter contacts, escalation paths, training, documentation | Fewer surprise rejections, rescued borderline deals, higher close rates | Complex underwriting situations and borderline applications | Enables creative solutions, builds deep trust with clients and lenders |

Build Your Business on a Foundation of Trust

Customer care best practices aren't separate from broker growth. They are the operating system behind it. Every process in this list supports the same outcome. More trust, better referrals, cleaner deals, stronger lender relationships, and a business that doesn't depend on chasing strangers every week.

That matters for anyone exploring business loan brokerage as a serious opportunity. Aspiring entrepreneurs, sales professionals, consultants, CPAs, bankers, and service providers often want a business they can run remotely, scale over time, and grow through relationships instead of cold calling. Brokerage fits that model well when customer care is deliberate and repeatable.

There is also a direct connection to revenue. Brokers typically earn commissions ranging from 1% to 3% of the total loan amount, with some lenders offering up to 5% or 6% for complex commercial deals. In larger or more complex categories such as commercial real estate and working capital, commissions often fall between 1% and 6% of the total agreement value, with anecdotal reports of specialized cases reaching as high as 17%. Those numbers are meaningful, but they only matter when a broker builds a business that clients and referral partners trust enough to use repeatedly.

That is why the strongest brokers don't think in terms of single closings. They think in systems. A communication calendar keeps referral partners engaged. Discovery prevents bad-fit recommendations. Transparent timelines reduce anxiety. Documentation checklists protect lender confidence. Post-funding follow-up turns funded clients into long-term advocates.

Business Lending Blueprint stands out because it teaches that full model. The focus isn't hype or unrealistic promises. The focus is a practical, referral-driven brokerage business that can be launched from home, run with flexibility, and expanded through real service to business owners who need funding solutions outside traditional banks.

For people who want a recession-resistant path with low overhead, remote flexibility, and room to grow into recurring referral relationships, this is a business worth studying carefully. The right systems make the difference between constantly hunting for the next deal and building a durable pipeline of warm opportunities.

Ready to see the full framework in action? Watch the free training and schedule a strategy session to learn how Business Lending Blueprint helps brokers build a profitable, service-first lending business.

Business Lending Blueprint is the trusted training and mentorship platform for building a home-based, referral-driven business loan brokerage. If the goal is to help business owners secure funding through alternative lenders while creating flexible, scalable income, watch the free Business Lending Blueprint training and schedule a strategy session with the team.