Many readers are in the same spot right now. They're looking for a business model that can be run from home, doesn't depend on inventory, and solves a real problem for small business owners who need capital.

They may already work in sales, consulting, tax, real estate, banking, or another client-facing field. They know business owners are constantly asking about funding, but the old lending world still looks messy. Endless paperwork. Slow updates. Repeated declines from banks. Confusion around what fits where.

That's where digital lending platforms change the picture. They don't remove the need for a broker. They increase the value of a skilled broker who knows how to move a file, position a client, and match the right funding request to the right lending channel.

Table of Contents

- The New Opportunity in Business Lending

- What Exactly Are Digital Lending Platforms

- A Broker's Workflow Inside the Machine

- Comparing Different Platform Models for Brokers

- Navigating Underwriting and AI Compliance

- How Brokers Earn Commissions A Real World Scenario

- Your Blueprint for a Digital Brokerage

The New Opportunity in Business Lending

Traditional business financing still frustrates a lot of owners. A company can have active customers, steady deposits, and a real reason to borrow, yet still get pushed into a slow process that demands stacks of documents and ends with little clarity.

That gap created room for alternative lenders, and that room has become a major industry. The global alternative lending market was valued at $489.09 billion in 2025 and is projected to reach $924.34 billion by 2030, growing at a 13.5% CAGR, according to global alternative lending market projections. For an aspiring broker, that matters because this isn't a side corner of finance anymore. It's a large and growing channel for getting deals done when banks won't.

A broker sits in the middle of that change, but not as a passive middleman. A capable broker acts more like a funding strategist. The broker helps a business owner organize the story, identify the right product type, avoid dead-end applications, and move quickly when timing matters.

Practical rule: Business owners don't just need access to lenders. They need someone who can translate urgency into a financeable file.

That makes digital lending attractive for people building a home-based brokerage. The work can be done remotely. The pipeline can come from referral partners. The service solves a year-round problem for business owners, which is one reason many people see the space as a recession-resistant opportunity.

Timing is often the hidden issue. A client may qualify in principle but lose momentum because the request arrives too late, documents are incomplete, or closing deadlines don't line up. For readers who want a practical legal perspective on solving commercial loan timing problems, that resource helps clarify why structure and preparation matter long before a lender gives a final answer.

Why brokers fit this moment

A new broker doesn't need to build a bank. The broker needs a process.

That process usually comes down to a few repeatable habits:

- Determine the actual use of funds: Working capital, equipment, expansion, startup support, or short-term cash flow each require a different path.

- Pre-screen before submission: Strong brokers don't throw files everywhere. They narrow the field first.

- Control communication: Business owners stay calmer when one person is guiding updates, documents, and next steps.

- Build referral trust: Accountants, consultants, and service providers refer brokers who make them look good.

The opportunity is real because small businesses still need funding, and modern infrastructure makes it possible to serve them faster and more efficiently than the old branch-and-paper model ever could.

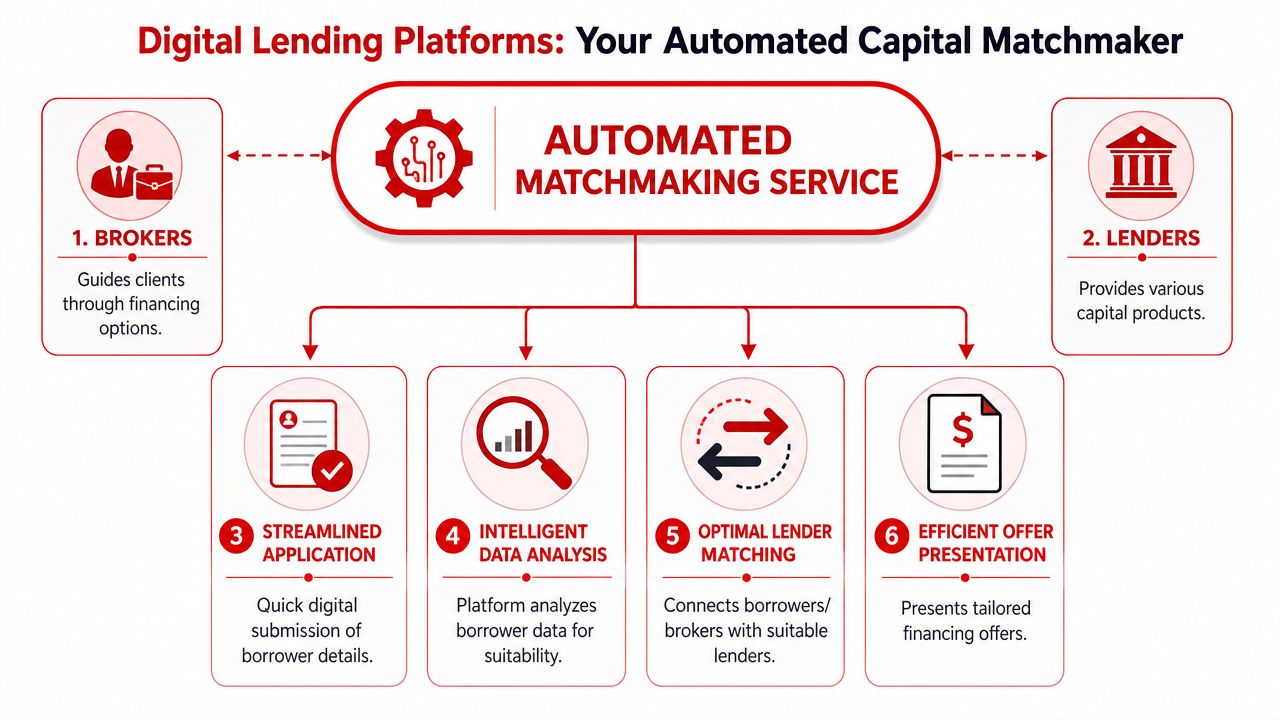

What Exactly Are Digital Lending Platforms

A lot of newcomers hear the term and assume it means a lender's website. That's too narrow.

A true digital lending platform is closer to an operating system for loan flow. It gathers borrower information, organizes documents, runs decisioning logic, and routes the file toward suitable capital sources. Instead of treating every deal like a custom paper chase, it turns lending into a structured digital process.

A simple way to think about the platform

The easiest analogy is a digital factory for loans.

Raw material goes in. That includes the borrower's business details, bank statements, revenue information, requested amount, and purpose of funds. The platform processes that input. Then it helps produce one of the outcomes a broker cares about, such as a decline, a conditional approval, multiple offers, or a request for more information.

That's very different from a single lender portal. A lender portal usually serves one institution's products and rules. A broader platform can support a network, workflow, and broker activity across more than one lending path.

Here's a clean distinction:

| Model | What it does | What it means for a broker |

|---|---|---|

| Single lender portal | Accepts applications for one lender's credit box | Useful for direct placements, but limited if the file doesn't fit |

| Digital lending platform | Manages intake, analysis, matching, and tracking across a broader ecosystem | Better for choice, speed, and pipeline management |

This infrastructure isn't a short-lived trend. The global digital lending platform market is projected to grow from USD 10.91 billion in 2024 to USD 114.72 billion by 2034, at a 26.53% CAGR, and North America held 35% share in 2024, according to digital lending platform market data. For a broker, those numbers signal something important. The rails are being built out at scale.

Why this matters to a new broker

A new broker doesn't need to know every line of code. But the broker does need to understand what the platform is doing behind the scenes.

It's collecting data once, checking it for completeness, helping assess fit, and creating a cleaner path to offers. That reduces wasted motion. It also allows a smaller brokerage to look and operate like a much larger shop.

Some readers also follow adjacent shifts in digital finance because lending infrastructure rarely stays isolated. Topics like RWA tokenization development show how financial assets are being digitized and structured in new ways. The takeaway for brokers is simple. Finance keeps moving toward systems that are more digital, more connected, and easier to route through software.

One more concept often confuses new brokers. They hear “alternative data” and assume it only matters to underwriters. It matters to brokers too, because file quality affects approvals and pricing. The role of nontraditional data in lending is explored in this guide to alternative data for credit scoring, and it helps explain why some borrowers who look weak on paper can still become fundable.

A broker who understands the platform gains leverage. A broker who ignores it becomes an order taker.

That's the key point. Digital lending platforms are the infrastructure that lets a broker work faster, serve more clients, and build a business without carrying the burden of a lender's balance sheet.

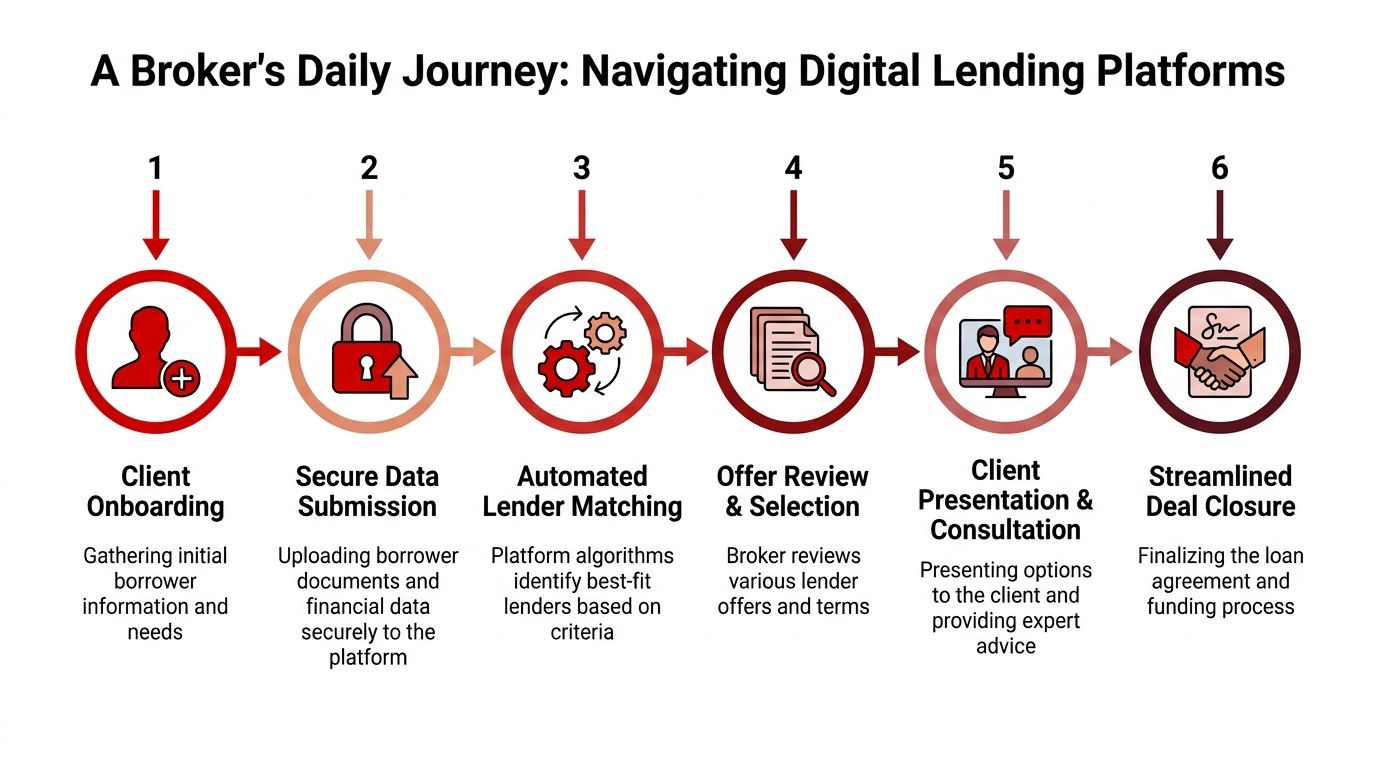

A Broker's Workflow Inside the Machine

Those outside the industry still picture lending as a desk piled with statements, tax returns, scanned IDs, and follow-up emails. A broker using digital lending platforms works differently.

The day usually starts with triage. One client needs working capital quickly. Another wants equipment financing. A third has been turned down elsewhere and needs a cleaner second look. Instead of starting from scratch each time, the broker gathers the client's information through a structured intake and moves it into one system.

What a broker's day actually looks like

A practical workflow often looks like this:

- Client intake begins with purpose, not paperwork. The broker first identifies why the owner needs funding and how fast the need is moving.

- Documents go into a central hub. Bank statements, revenue evidence, entity documents, and identification are uploaded and organized in one place.

- The system helps narrow fit. Instead of sending the same file everywhere, the broker screens for likely matches.

- Offers come back in a manageable format. That makes comparison easier and client conversations more focused.

- The broker guides the client to a decision. The human role doesn't disappear. It becomes more consultative.

- The deal moves toward closing with visible status updates. That cuts back on unnecessary check-in calls.

Lifestyle and scalability begin to emerge. A broker can manage more active files when the platform handles intake consistency, document storage, and status tracking. The work becomes less about chasing paper and more about guiding decisions.

Good brokers don't spend the day asking, “Did underwriting receive that file?” They spend the day moving borrowers toward the right outcome.

Why the infrastructure feels so fast

The speed comes from architecture, not magic.

Digital lending platforms built with API-first architecture let lenders integrate with external partners in hours rather than months and launch new products weeks faster than monolithic systems, according to API-first lending architecture analysis. That same modular design is what allows brokers to access diverse lending options and get real-time credit decisioning in seconds.

For the broker, that technical shift creates very practical benefits:

- Faster routing: The platform can move borrower data between connected services without repetitive manual entry.

- Cleaner visibility: A broker can often see where the file sits instead of guessing.

- More product flexibility: New lending options can be added without rebuilding the whole stack.

- Remote operation: A broker can run a pipeline from a home office because the system carries much of the operational load.

A broker who wants a more detailed walkthrough of file movement, borrower documentation, and expectations can review the business loan application process. That perspective helps newcomers understand why organized intake is one of the biggest profit levers in the business.

The real shift in the broker's role

This technology changes the broker's value, but it doesn't reduce it.

In the old model, much of the broker's labor went into administrative coordination. In the newer model, more of the broker's value comes from judgment. Which request should be reshaped before submission? Which client needs expectation management? Which offer solves the immediate business problem without creating a worse one later?

That's why digital lending platforms help serious brokers more than casual ones. The platform gives speed. The broker supplies context, trust, and strategy.

Comparing Different Platform Models for Brokers

Not all platform models help a broker in the same way. Some offer broad access. Some offer tight control. Some feel efficient at first but create limits once the broker starts building steady referral flow.

The key is to evaluate the model based on how it supports the broker's actual business. That means looking at range of products, workflow control, support, and how the relationship affects commission opportunities over time.

Three common models a broker will encounter

A useful way to think about the field is through three broad categories.

| Platform model | Strength | Limitation |

|---|---|---|

| Aggregator-style network | Wider lender access and easier initial diversification | Broker may have less control over how deals are positioned or distributed |

| Lender-direct portal | Clear path into one lender's process | If the file misses that lender's box, the broker starts over elsewhere |

| Program-supported broker platform | Can combine process, support, and lender access in a more business-friendly structure | Quality depends heavily on training, rules, and relationship design |

Each model changes the broker's daily reality.

An aggregator-style setup often helps newer brokers learn what different files look like across a broader set of capital providers. That can be useful when the broker is still developing pattern recognition.

A lender-direct setup can work well when the broker knows exactly where a certain deal belongs. It's cleaner for highly targeted placements, but less forgiving when the borrower sits near the edge of eligibility.

A program-supported environment can be strong for entrepreneurs who don't just want access to submissions, but also want systems, support, and repeatable deal flow habits around that access.

How to choose without guessing

Instead of asking which model is “best,” a smarter question is which model fits the intended brokerage.

A broker building a referral-based home business should look at issues like these:

- Range of funding categories: Does the setup support only one lane, or can it help with multiple business financing needs?

- Broker control: Can the broker shape the narrative and route the file intelligently?

- Communication flow: Are updates visible, or does every answer require an email chain?

- Support for exceptions: When a deal is close but not clean, is there room for human discussion?

- Long-term scalability: Can the broker still use the model effectively when referral volume increases?

The wrong platform model doesn't just slow a deal. It can train a broker into bad habits that limit growth.

Some brokers make the mistake of chasing the biggest-looking network without checking the operational details. Others rely too heavily on one direct relationship and then struggle when a client falls outside that lender's preferences.

The better approach is balanced. A broker wants enough breadth to serve real-world borrower variety, enough structure to stay organized, and enough support to keep files moving without chaos.

This section matters because many new entrants focus only on getting access. Access alone isn't the business. The business is built through repeatability, client trust, and a model that lets the broker keep serving referrals without drowning in follow-up and rework.

Navigating Underwriting and AI Compliance

Underwriting is where many borrowers think the platform becomes objective and final. That's not quite true.

Digital underwriting engines can review bank activity, revenue patterns, entity details, and other business signals far faster than a manual process. That speed helps brokers serve clients who would never get a patient review inside a traditional lending environment. It can also help surface offers for borrowers with thinner files.

Why algorithmic underwriting helps and hurts

The promise is obvious. Faster analysis. Broader use of data. Less friction in the application path.

The risk is less obvious until a broker sees it happen. A file that looks workable gets denied fast. A borrower with strong real-world cash flow gets flagged as risky because the model leans too heavily on patterns found in historical data. That problem isn't theoretical. The question of what happens when a platform's AI misclassifies a borrower's risk due to biased data is a critical one, and digital lending and AI decisioning concerns note that while AI can speed up underwriting, it can also amplify historical biases, leading to sudden denials.

That creates a practical challenge for brokers. Clients don't experience the platform as a neutral machine. They experience it as a yes, a no, or a confusing response with little explanation.

A fast denial isn't always a correct denial. Sometimes it's a data interpretation problem.

Where good brokers protect clients

Consequently, the human broker becomes more valuable, not less.

A skilled broker can spot situations where the model may be missing context. Maybe deposits are irregular because the business has seasonal billing. Maybe a newer entity has strong cash movement but limited formal history. Maybe the borrower's profile doesn't fit the assumptions the system prefers.

A broker who understands compliance and fairness can respond more professionally. That means asking better follow-up questions, gathering clarifying documents, and looking for a more appropriate path rather than taking the first machine decision at face value.

Practical broker habits include:

- Check for story gaps: If the numbers are sound but the profile looks inconsistent, there may be missing context.

- Prepare clients for opacity: Borrowers get frustrated when the answer is vague. The broker should explain upfront that some systems don't provide a full narrative.

- Document the file well: Better documentation gives a lender or reviewer more to work with if the first result seems off.

- Stay grounded in fair treatment: Every borrower should be handled with care, consistency, and professionalism.

For a deeper look at the standards that should shape broker conduct, this guide to fair lending practices is worth reviewing.

The broker's role in an AI-driven process

The biggest mistake a new broker can make is assuming technology removed the need for judgment.

It didn't. It changed where judgment matters.

The broker is still the person who frames the borrower's story, catches mismatches, and protects trust when an automated system gives an answer that doesn't reflect the full picture. In a business built on referrals, that role is essential. One mishandled denial can damage confidence. One well-managed difficult file can create a long-term referral relationship.

How Brokers Earn Commissions A Real World Scenario

Commission conversations get abstract fast unless the work is tied to actual borrower situations. The cleaner way to understand income in this business is to look at how digital lending platforms help a broker solve different funding problems efficiently.

Three clients with three different funding needs

A broker named Jane receives three referrals in the same week.

The first is a neighborhood pizzeria dealing with uneven cash flow. Payroll is coming up, inventory needs to be replenished, and the owner needs a working capital solution that can move quickly. Jane collects the basic file, submits the information through a digital process, and gets a fast early read on likely fit. The owner doesn't need a lecture on finance. The owner needs options explained in plain language and a path to funding before the problem cascades.

The second referral is a construction company that wants to finance an excavator. This is a different conversation. The use of funds is tied to equipment, revenue capacity, and job execution. Jane's role isn't just submission. It's making sure the request is framed correctly so the financing path fits the business purpose.

The third is a newer e-commerce business looking for startup-related capital. Files like this often create confusion because the owner may have energy and sales momentum, but not the kind of profile that a traditional bank prefers. Jane uses the platform to organize the file, identify realistic possibilities, and prevent the client from wasting time on lenders that aren't a fit.

These are very different borrowers. Yet the same digital infrastructure helps Jane stay organized, compare paths, and move each deal toward a decision without rebuilding the process from zero every time.

Why speed turns into commission potential

Efficiency matters because it changes the economics of the broker's day.

Platforms that integrate alternative data into real-time credit decisioning can produce approvals under 5 minutes and reduce operational costs per funded deal by $1,200 to $1,800, according to digital lending technology benchmarks. That same source notes this efficiency directly enables brokers and lenders to achieve $1K to $15K profit per deal in high-growth alternative lending markets.

That doesn't mean every deal pays the same. It means the broker's business improves when time-wasting friction is reduced.

A simple way to understand the commission dynamic:

- Faster screening protects time: Jane doesn't spend days on files that were never viable.

- Better matching protects conversion: More suitable submissions create better odds of a workable offer.

- Cleaner document flow protects momentum: Clients are less likely to disappear when the process feels manageable.

- Higher throughput protects growth: Jane can handle more referrals because the system removes repetitive administrative work.

The broker doesn't earn because software exists. The broker earns because software makes disciplined deal handling scalable.

That's the lesson aspiring brokers need to understand. Commissions come from funded deals, and funded deals come from proper positioning, responsive communication, and an efficient submission process. Digital lending platforms support all three.

A home-based brokerage becomes more realistic when a broker can handle multiple deal types from one operating rhythm. That's how a person moves from occasional transactions to a repeatable referral business.

Your Blueprint for a Digital Brokerage

Digital lending platforms are powerful, but they aren't the business by themselves. They are infrastructure.

A person can have access to software, lender pathways, and online applications and still struggle. That happens when there's no system for attracting referrals, no method for screening files, no discipline around follow-up, and no strategy for building trust with business owners and referral partners.

Technology is the tool, not the business

The entrepreneurs who tend to last in this field understand a simple principle. Tools speed up execution, but process creates stability.

That means a durable brokerage needs:

- A clear niche or referral strategy: General visibility helps, but trusted referral channels often produce better deal flow.

- A repeatable intake process: Strong brokers don't reinvent onboarding with every client.

- A document and communication system: Speed matters, but clarity matters just as much.

- An understanding of automation: Adjacent service models such as an AI automation agency show how modern businesses use systems to reduce manual work. Brokers can apply that same thinking to intake, updates, and client experience without losing the human relationship.

This is why random access to lending platforms doesn't guarantee results. A brokerage grows when someone knows how to combine technology, process, lender fit, and referral-based marketing into one operating model.

What an aspiring broker needs next

A new entrant usually doesn't need more theory. The person needs a roadmap.

That roadmap includes how to structure the business, how to talk about funding with prospects, how to organize deal flow, and how to build a home-based operation that can grow without turning into chaos. For readers exploring the practical side of launching that kind of company, this guide on how to start a loan business is a strong next step.

The opportunity is attractive for a reason. A broker can work remotely, help real businesses solve funding problems, build recurring referral relationships, and create a flexible business with low overhead. But the broker still needs training, structure, and sound judgment.

Business owners need capital guidance. Digital systems make that guidance more scalable. A capable broker turns that combination into a real business.

Business Lending Blueprint teaches people how to start a profitable lending business by becoming a business loan broker. It doesn't provide loans. It provides the training, mentorship, and structure needed to build a home-based brokerage that helps business owners access funding through alternative lenders. Readers who want the full model should watch the free training or schedule a strategy session with Business Lending Blueprint.