Most advice about how to start a loan business is wrong from the first sentence. It pushes people toward direct lending, heavy compliance, large capital requirements, and a model that most beginners should avoid.

A smarter path is the business loan brokerage model. A broker doesn't lend personal money. A broker connects business owners to lenders, manages the process, and earns a commission when deals fund. That changes everything. It lowers startup friction, removes the need for large reserves, and creates a business that can run from home with referral partners instead of cold calling.

That matters because small business owners need funding right now, and traditional banks aren't meeting that need. The opportunity isn't in becoming a bank. The opportunity is in becoming the person who knows where capital is still available, how to package a deal correctly, and how to build trust with referral sources who already serve business owners every day.

Table of Contents

- The Trillion-Dollar Gap Banks Cannot Fill

- Establishing Your Lean Brokerage Foundation

- Building Your Network of Vetted Lenders

- Implementing a Referral-Driven Lead System

- Mastering Your Deal Flow and Underwriting Process

- Projecting Revenue and Scaling to Six Figures

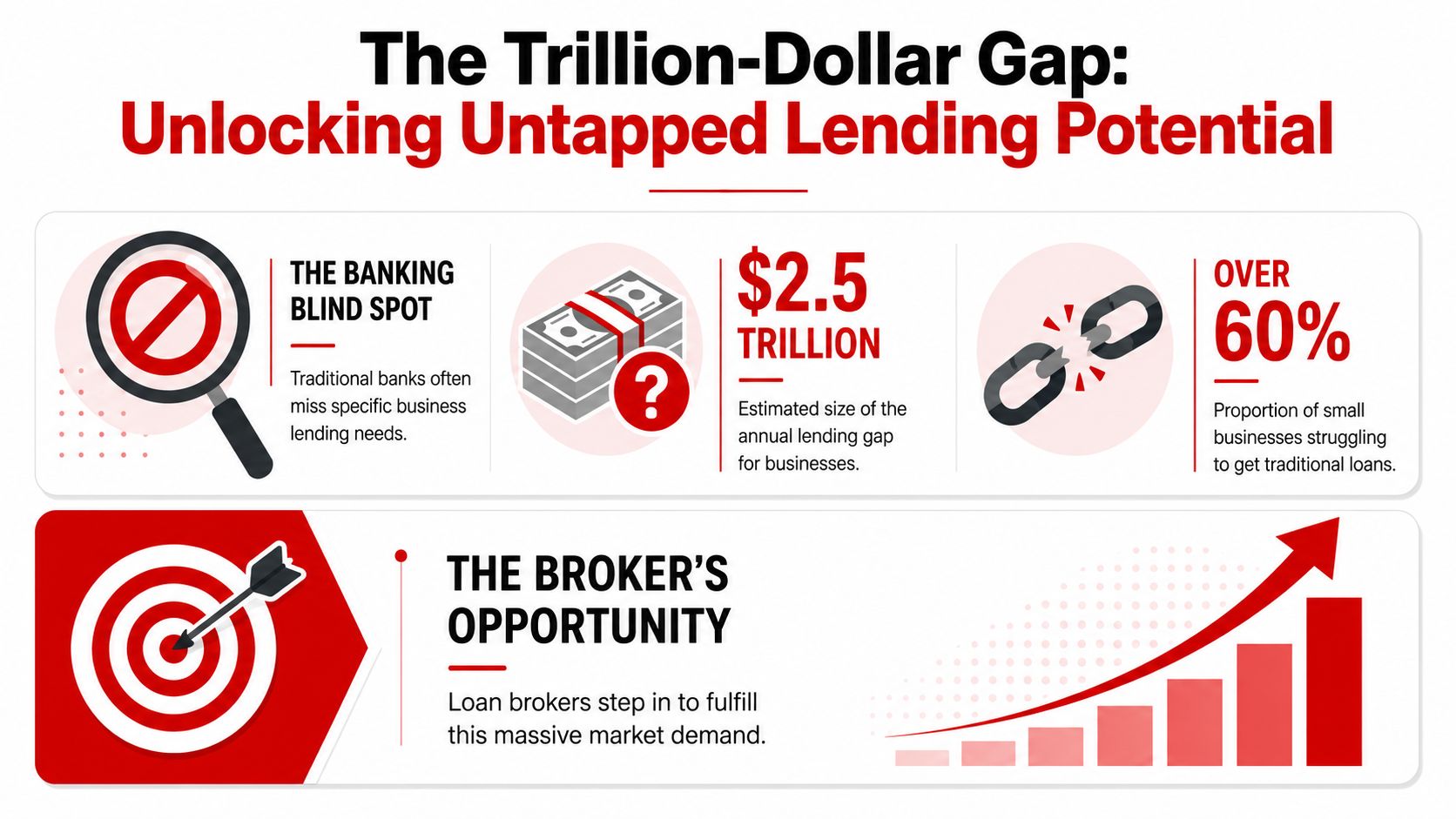

The Trillion-Dollar Gap Banks Cannot Fill

Starting a loan business does not require lending your own money. It requires sitting between real demand and the right capital source.

That distinction matters because too many articles blur brokerage and direct lending. They should not. A direct lender needs capital, tighter regulation, and balance-sheet risk. A business loan broker gets paid for matching deals, packaging files correctly, and sending them to lenders that fund. That is the low-overhead model worth building.

The opportunity is large. Abrigo's small business lending market overview summarizes a U.S. small business financing market of roughly $1.7 trillion in 2022, with strong growth from prior years. That is more than enough room for a broker who knows how to bring lenders qualified files through referral channels.

Why banks leave so much demand untouched

Banks miss a huge share of the market because their credit box is narrow, their process is slow, and many small business owners do not fit the clean profile a bank wants. The same Abrigo analysis shows low approval rates at both large and smaller banks, while non-bank lenders approve a higher share of applicants.

That creates the opening for a broker.

A restaurant owner with uneven deposits, a contractor with tax issues, or a growing company that needs money this week does not need a lecture about underwriting philosophy. They need options. A broker who understands lender appetite can place deals that a bank branch would decline, ignore, or drag out until the borrower gives up.

That is why I tell new brokers to stop trying to sound like bankers. Your job is not to protect a branch model. Your job is to solve funding problems that traditional channels leave behind.

Abrigo's summary also notes that many businesses get only part of the financing they asked for, or none at all. That shortfall keeps demand alive even when owners have already tried a bank once.

Why this business holds up when credit gets tighter

Tighter credit does not kill demand. It increases the value of a broker who can move fast and match the file to the right lender the first time.

Business owners still need working capital, equipment financing, lines of credit, and short-term cash solutions. They still need payroll covered, inventory purchased, trucks repaired, and opportunities funded. The same source notes that access to financing is a top growth issue for owners, and speed matters heavily in lender selection. Those conditions favor brokers because brokers win on access and packaging, not on holding capital.

That is the core reason the brokerage model works so well for a referral-based business. You do not need to cold call all day. You need accountants, consultants, tax professionals, insurance agents, real estate professionals, and other local connectors who already hear, “I need funding.” If you become the reliable person who gets those files placed, the market will keep feeding you opportunities.

If you want a clearer picture of where brokers fit, read this explanation of how the alternative lending industry really works. For the legal setup side, the California business incorporation guide is a useful reference.

| Market reality | Why it matters to a broker |

|---|---|

| Bank approval rates are low | More borrowers need alternative funding sources |

| Non-bank lenders approve more applicants | Access to lender relationships has direct value |

| Owners care about speed | Fast packaging and quick placement win deals |

| Many businesses get partial funding or no funding | Repeat demand keeps showing up through referrals |

Establishing Your Lean Brokerage Foundation

Start simple. A business loan brokerage is a fee-based service business, not a lending company, and that distinction decides whether you stay lean or bury yourself in overhead before the first commission hits.

New brokers waste time acting bigger than they are. They buy branding packages, hunt for office space, and obsess over business cards. None of that gets a file approved. A clean entity, a compliant setup, and a tight operating process do.

The reason this model works is straightforward. You are not using your own capital to fund deals. You are matching business borrowers to lenders, packaging the file correctly, and earning a commission when the deal closes. That means you can start from home, keep fixed costs low, and build around referrals instead of cold outreach.

Build the business entity first

Set up the company before you chase leads. An LLC or corporation gives you a legal shell for contracts, commissions, taxes, and banking. It also forces you to treat this like a real operation instead of a side hustle with a Gmail inbox.

Get the EIN. Open a business bank account. Use a business email domain. Put your intake documents, lender agreements, and client records in one secure system from day one. Sloppy admin kills trust fast, especially when referral partners are deciding whether to send you another client.

For readers who need a plain-English walkthrough on forming an entity, this California business incorporation guide is a useful reference for understanding the setup process and common formation considerations.

Verify the rules before you market

A lot of beginners assume every loan-related business requires the same licensing burden as direct lending or consumer finance. That assumption keeps people stuck for no reason.

Business loan brokerage is often lighter. In many states, you can broker commercial funding without the same setup required to make loans yourself. The point is not to guess. The point is to confirm the rules in your state, for the exact products you plan to broker, before you take an application or advertise services.

Do that once, document it, and move on.

Define your lane early

Generalists stay confused. Specialists get traction.

Pick the funding categories you want to handle first. Working capital, term loans, equipment financing, merchant cash advances, and invoice-based products all have different documentation standards and borrower profiles. A new broker should start with a narrow offer and get good at packaging those deals before expanding. If you plan to serve companies with receivables-based needs, study how accounts receivable lenders evaluate funding requests so you know what a financeable file looks like.

A clear offer also makes referrals easier. Accountants and consultants do not want a vague pitch. They want to know who you help, what problems you solve, and how quickly you can tell them whether a file has a real shot.

Use a lean operating stack

Your foundation should fit on one checklist:

- Form the entity. Use an LLC or corporation so contracts and commissions run through the business.

- Get the EIN and bank account. Keep revenue and expenses separate from personal finances.

- Confirm state requirements. Verify what applies to your brokerage activities before marketing.

- Set up core communication tools. Business email, dedicated phone, calendar, e-signature, and secure document storage.

- Choose one CRM. Every lead, referral source, follow-up, and status update should live in one place.

- Create a basic intake process. Decide what documents you require, how files are reviewed, and how quickly you respond.

That is enough to launch.

Stay home-based until revenue earns the upgrade

A lean brokerage should look boring at first. Good. Boring makes money. Expensive vanity purchases do not.

Skip the office. Skip paid ads. Skip the polished image campaign. Put your time into referral relationships, lender communication, follow-up discipline, and file quality. Those four things create commissions. Once the business produces steady monthly revenue, then you can decide what to improve. Until then, protect cash and build a process that works without you carrying unnecessary overhead.

Building Your Network of Vetted Lenders

A broker's primary product is access.

Clients do not pay you for a logo, a polished site, or a stack of generic financing options. They pay you because you know which lender can fund their deal, which one will waste their time, and which file needs to be packaged differently before it goes out. That is the whole business model.

Start with a small lender bench. One to three strong partners is enough at the beginning. More than that usually hurts a new broker because every lender has different submission rules, appetite, stipulations, and sales pressure. If you do not know those differences cold, you submit sloppy files, create delays, and look inexperienced to both the client and the funding source.

Use a simple structure:

- One core working capital lender for fast-turn requests and straightforward files

- One flexible lender that can handle tougher credit profiles or unusual scenarios

- One specialist for a niche you expect to see often

That last category matters more than beginners think. If your referral partners work with B2B companies, invoice financing may come up early. Learn how accounts receivable lenders review aging reports, customer concentration, and payor strength before you promise anything.

Do not sign up with lenders just because they approve your broker application. Vet them like your reputation depends on it, because it does.

Here is what to check before you send a single deal:

| Lender factor | What the broker should look for |

|---|---|

| Process clarity | Clear submission requirements, fast answers, and no mystery steps |

| Product fit | Financing options that match the types of borrowers you plan to serve |

| Commission structure | Written payout terms, timing, and fee transparency |

| Speed | Reliable turnaround from submission to decision to funding |

| Reliability | Consistent communication and fewer last-minute surprises |

A lender with vague instructions will create the same mess on every file. Missing documents, repeated follow-ups, and changing stipulations do not just slow down funding. They make your referral partners question whether sending clients to you was a mistake.

Your lender network should get sharper over time. You should know each partner's appetite, common decline reasons, preferred documents, and how they handle edge cases. That knowledge is what lets a small brokerage compete without cold calling or using personal capital. Precision beats volume.

Business Lending Blueprint trains brokers on lender placement and gives access to a vetted lender network. That matters because trial and error is expensive when your business runs on trust. A bad first few submissions can damage referral relationships before they ever become consistent.

You should also pay attention to how lenders and brokers present themselves publicly. A clear LinkedIn posting strategy can help you stay visible to referral partners while reinforcing the markets and deal types you handle well.

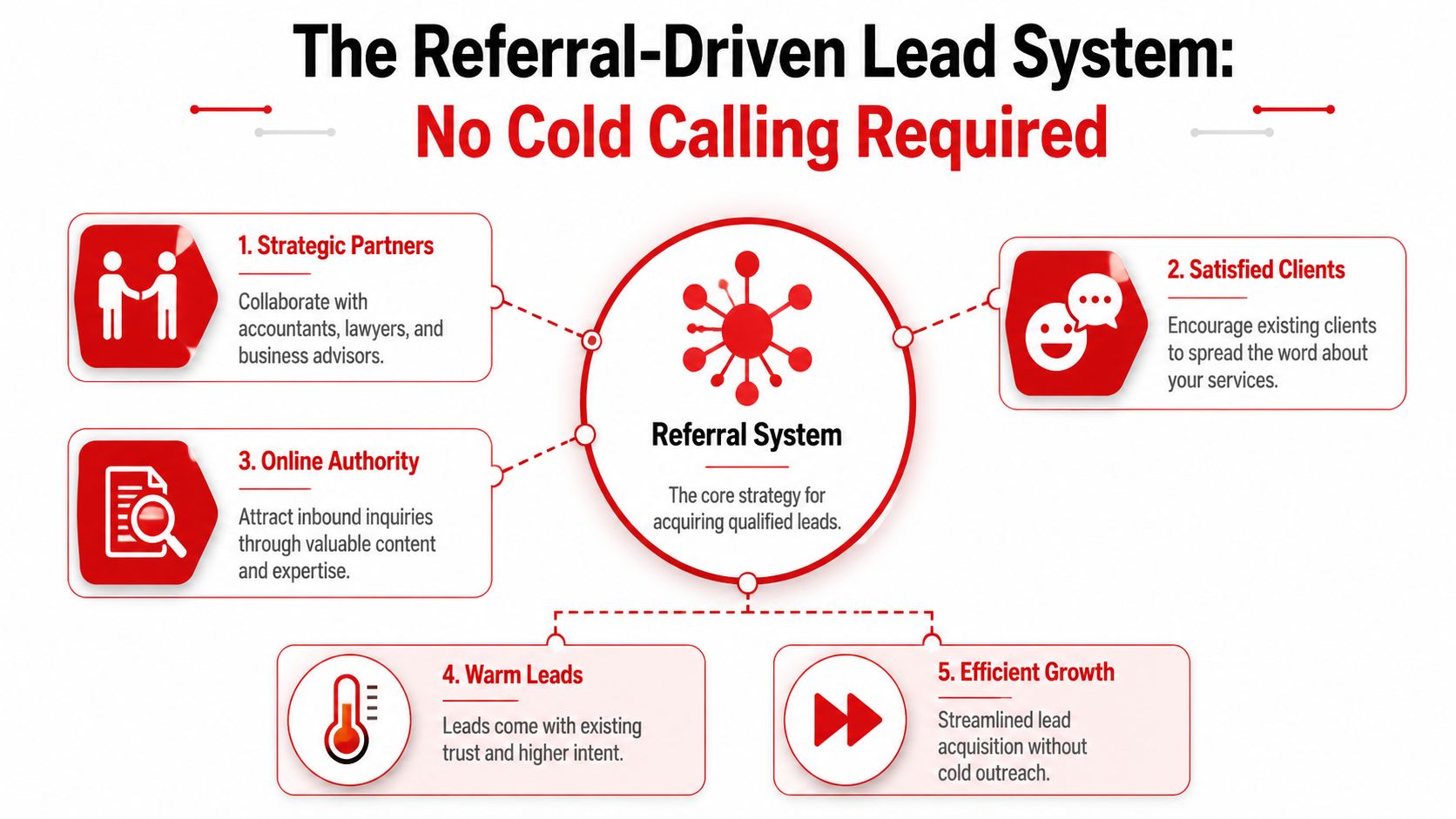

Implementing a Referral-Driven Lead System

If you want to know how to start a loan business without burning months on rejection, stop chasing strangers. Build a referral engine instead.

A brokerage wins on trust, speed, and placement. Referrals solve the trust problem before you ever get on the phone. They also fit the low-overhead model this guide is built around. You do not need ad spend, a call center, or your own capital to fund deals. You need a small group of professionals who already serve business owners and who need a reliable funding resource for the clients they cannot help themselves.

How referrals happen in the real world

A CPA sees cash flow pressure before the client asks for funding. An attorney sees a partner buyout, dispute, or acquisition coming. A marketing consultant sees a client that needs working capital to push inventory or ad spend. A banker has a customer who does not fit bank credit but still needs a solution.

Those are the people who feed a brokerage.

Your pitch to them should be simple. Send me the business owner who needs capital. I will handle the options, communicate clearly, and protect your relationship. That message works because it answers the only question referral partners care about. "Will you make me look smart or make me regret the introduction?"

Start with referral partners who already hear funding problems

Go after professionals who are close to revenue, risk, and growth decisions:

- CPAs and tax professionals who spot cash crunches, tax debt, and uneven receivables

- Business attorneys involved in transactions, disputes, restructures, and ownership changes

- Consultants and agencies working with companies trying to grow faster than cash flow allows

- Insurance, credit, and commercial real estate professionals serving the same owner base

- Local business networking groups where advisors and operators meet consistently

One good partner can send multiple deals a year. Ten weak partners who barely know what you do will waste your time.

That is why I recommend depth over breadth early on. Pick a few referral categories, learn their client pain points, and give them a clean reason to send business your way.

Give partners a reason to refer, not just a reminder

Referral partners do not need a speech about your ambition. They need clarity.

Tell them who you help, what situations fit, what documents are usually needed, and how fast you respond. If you serve businesses with consistent revenue that need working capital, equipment financing, or short-term cash flow solutions, say that plainly. If you can help clients declined by traditional banks, say that too. Specificity gets referrals. Generic "I can help anyone" messaging gets ignored.

You should also make the handoff easy. Ask for a simple email introduction, reply fast, and keep the partner updated without creating extra work for them.

Add online authority so referrals compound

Offline trust gets the first referral. Online credibility helps get the second and third.

A referral partner wants somewhere to send people that looks professional and current. That means a clear website, a sharp LinkedIn profile, and short educational content that explains the borrower problems you solve. For brokers using content to stay visible with professional contacts, this LinkedIn posting strategy gives a practical framework for staying consistent without sounding like every other finance account.

Service quality keeps the system alive. Referral sources keep sending clients when you respond quickly, explain the process clearly, and treat every introduction like it matters. These customer care best practices matter because a referral business grows on reputation, not volume.

Mastering Your Deal Flow and Underwriting Process

Loan brokerage margins are won in processing, not prospecting.

A referral partner can send you a solid borrower, but if your intake is sloppy, your document collection drags, or you submit the file to the wrong lender, that referral dies fast. This business does not reward brokers who spray applications and hope something sticks. It rewards brokers who pre-screen hard, package cleanly, and move files with speed.

Run every deal through a fixed workflow

If your process changes with every borrower, you do not have a business. You have a guessing habit.

Use the same sequence on every file:

- Initial intake. Capture the funding request, business model, monthly revenue, time in business, and urgency.

- Borrower interview. Find out why they need capital, how they plan to use it, and what payment they can realistically handle.

- Pre-qualification. Screen for clear fit issues before you ask lenders to review anything.

- Document collection. Gather the statements and supporting records needed to present a credible file.

- Internal review. Check for inconsistencies, weak explanations, and missing items before submission.

- Lender placement. Send the deal to the lender profile that matches the file.

- Stipulations and closing. Manage follow-up, keep the borrower on task, and get the deal funded.

That structure protects your time. It also protects your reputation with referral partners, because they care about one thing. Whether you make them look smart for introducing you.

Track every file in one place

Memory is not a system.

Once referrals start coming in, you need a clear pipeline for contact history, document status, lender submissions, follow-ups, and funding outcomes. A broker who wants a cleaner way to organize that pipeline should spend time understanding sales funnel strategies. The lesson is simple. Every lead needs a visible stage and a defined next action.

This also gives you better control over conversion. You can see where files stall, which referral sources send fundable borrowers, and which lender matches produce the highest close rates. That kind of visibility matters if you care about building income you can predict. If you want to see how that turns into real commissions, review this breakdown of business loan broker salary ranges and earning potential.

Underwrite the file before a lender sees it

A profitable broker does not act like a messenger. A profitable broker acts like the first line of underwriting.

Ask questions that expose the actual risk fast:

- Why does this business need money right now?

- Will the proposed use of funds produce a clear return or solve a cash flow problem?

- What does the revenue pattern say about repayment ability?

- Which documents support the story, and which ones create concern?

- Which lender box does this borrower fit into?

Weak files usually fail for obvious reasons. The revenue story is unclear. The request amount makes no sense. Bank statements conflict with what the borrower said on the phone. Documents come in half-complete. Then the lender asks for more, the borrower gets annoyed, and the referral source stops sending deals.

Fix that before submission.

Package the deal like an advisor, not an order taker

Borrowers often do a poor job explaining their own file. That is your job.

Your submission should tell a tight, credible story. What the business does. Why it needs capital. How much it needs. What the cash flow supports. Why this lender is the right fit. Clean packaging gets faster decisions because the underwriter does not have to guess.

One well-built file beats five rushed submissions every time.

Projecting Revenue and Scaling to Six Figures

Six figures in this business does not come from a huge team, paid ads, or personal lending capital. It comes from simple brokerage math repeated every month through referrals.

A business loan brokerage gets attractive once you know your numbers. Brokers are paid a percentage of funded deals. In plain English, that means one solid month of funded volume can produce more income than many service businesses make with far more overhead. That is the advantage of the brokerage model. You arrange capital. You do not lend your own money, carry the risk, or tie up cash in inventory.

Revenue follows funded volume and payout discipline

If you want predictable income, stop thinking in vague goals and start thinking in funded deals, average commission per deal, and referral partner output.

The model is straightforward:

- referral partners send qualified business owners

- you review the opportunity fast

- you place the file with the right lender

- the lender funds

- you get paid

That system scales well because it does not depend on cold calling. It depends on trust. A referral partner who sends good-fit borrowers month after month is far more valuable than a pile of random leads that never close.

A practical growth path usually looks like this:

| Stage | Focus |

|---|---|

| Early stage | Learn submission standards, fund first deals, build trust with referral sources |

| Stable stage | Increase referral consistency, tighten follow-up, improve close rate |

| Growth stage | Expand placement options, raise average commission, protect turnaround time |

| Scale stage | Add support, standardize intake, track every step from lead to funding |

Six figures usually come from consistency, not complexity

New brokers often overcomplicate the path. They chase websites, logos, CRMs, automations, and social content before they have a steady referral engine. That is backwards.

A six-figure brokerage is usually built on a smaller set of repeatable actions done well:

- Bring in referral partners who already talk to business owners. Accountants, consultants, brokers, and other trusted advisors can send better opportunities than cold outreach ever will.

- Track funded volume by source. You need to know which relationships produce funded deals, not just conversations.

- Protect your average payout. Low-quality files waste time and drag down revenue even if they create activity.

- Increase placement accuracy. Better lender matching leads to more approvals and faster funding.

- Respond fast. Referral partners keep sending deals to the broker who makes them look good.

That is the true scaling engine.

Product range protects revenue

A broker with only one solution has a fragile business. A broker who can place several types of business funding keeps more deals in-house and gives referral partners a reason to keep sending clients.

Business owners do not arrive pre-sorted. One needs working capital. Another needs equipment financing. Another belongs in a longer-term product. If you only know how to place one type of deal, your income ceiling stays low because your decline pile gets too large.

The fix is simple. Build enough product knowledge to route each file to a realistic option, then get sharper over time. Breadth improves revenue because it improves retention of opportunities.

Better volume gives you better economics

Payouts improve when lenders trust your files and expect usable submissions from you. That trust is earned. It comes from clean packaging, realistic expectations, and funded volume over time.

Focus on the inputs that change your income:

- funded deals per month

- average commission per funded deal

- referral partners producing active opportunities

- approval rate by lender and product

- time from intake to submission

- time from submission to funding

Watch those numbers every month. If funded volume is flat, the problem is usually lead quality, weak referral activity, poor matching, or slow follow-up. It is rarely a motivation problem.

For a closer look at how commissions stack across deal flow, read this breakdown of business loan broker salary and earnings potential.

The big advantage here is hard to ignore. You can build this from home, start without lending your own capital, and grow through referral relationships instead of cold calling. That is why the brokerage model is such a strong play for operators who want a lean business with real upside.

Business Lending Blueprint shows aspiring brokers how to launch and grow a business loan brokerage using a referral-based model, a vetted lender network, and a step-by-step operating system. Readers who want the full blueprint can watch the free training or schedule a strategy session through Business Lending Blueprint.