A strong deal is sitting on the table. The business has a real path to revenue, the collateral is solid, and the timing matters. Then the bank shuts the door because the file doesn't fit its checklist. The owner leaves frustrated. The consultant, CPA, salesperson, or aspiring broker watching that happen sees something else too. A gap.

That gap is where alternative lending lives.

A hard money lender for business isn't the right answer for every deal, and anyone pretending otherwise shouldn't be trusted. But when a borrower needs speed, flexibility, and asset-based underwriting, hard money can move a transaction from stalled to funded. Better yet, for the person who learns how these deals work, this niche opens the door to a serious home-based business helping owners secure capital while earning lender-paid commissions.

Hard money is often considered a last resort. Smart operators look at it as a tool. Smarter ones learn how to broker it.

Table of Contents

- Why Your Bank Said No and What to Do Next

- Decoding Hard Money Loans for Business Deals

- How to Find and Vet a Reputable Hard Money Lender

- Structuring the Deal and Partnering for Success

- The Blueprint to a Six-Figure Business Loan Broker Career

- Your Next Step to Funding Deals and Earning Commissions

Why Your Bank Said No and What to Do Next

A common scene plays out every week. A business owner finds a warehouse, retail property, partner buyout opportunity, or expansion play that makes sense on paper. The owner has urgency, some collateral, and a plan. The bank still says no because tax returns don't show enough history, cash flow looks uneven, or the deal falls outside neat policy boxes.

That rejection doesn't always mean the deal is bad. It often means the deal is wrong for a bank.

Banks want predictability. They prefer borrowers with clean documentation, long operating history, and plenty of time. Hard money lenders care more about the asset, the exit, and whether the deal can hold together under pressure. That difference matters when a borrower needs a bridge, not a lecture.

Banks underwrite for policy. Alternative lenders underwrite for possibility, then price the risk.

This is also where skilled advisors separate themselves from order takers. Instead of telling a business owner to “try again later,” a sharp funding professional starts asking better questions:

- What asset supports the request: real estate, equipment, receivables, or another hard asset?

- What caused the bank decline: thin history, credit profile, debt load, or timing?

- What's the exit plan: sale, refinance, incoming revenue, or recapitalization?

- What's the immediate pressure: closing deadline, working capital gap, or acquisition window?

If credit issues are part of the problem, the borrower needs two tracks at once. One track is immediate funding strategy. The other is long-term borrower improvement. A practical starting point is this detailed guide for mortgage-ready credit, which helps borrowers understand how to strengthen their profile while pursuing the right funding fit now.

Some deals also don't need hard money at all. When invoices and customer payments are the stronger story, accounts receivable funding options may fit better than real-estate-backed capital.

The real lesson in a bank rejection

A bank decline can discourage a borrower. It should educate an aspiring broker.

The lending world isn't one lane. It's a network of products, risk models, and capital sources. The person who understands where hard money fits becomes useful fast. Useful people get referrals. Referrals turn into funded deals. That's how this business starts.

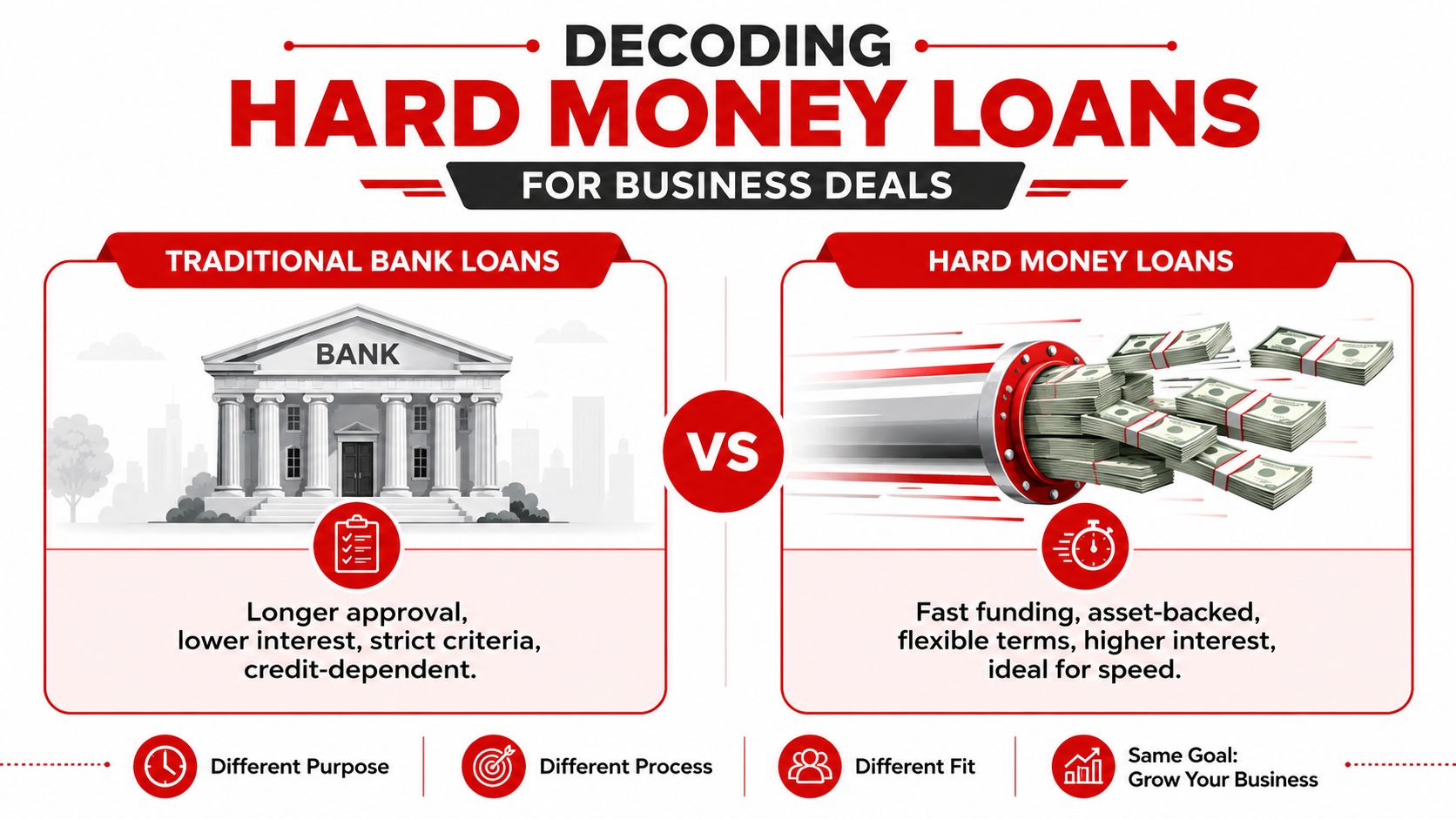

Decoding Hard Money Loans for Business Deals

A hard money lender for business makes decisions differently than a bank. The center of gravity is the collateral, not the borrower's polished financial package. That's why these loans can rescue good opportunities that conventional underwriting rejects.

The tradeoff is cost. According to Crestmont Capital's guide on hard money loans for business, hard money loans for business typically range from 8% to 15% per annum, and they can reach 45% or more in higher-risk scenarios. The same source notes that traditional commercial or SBA-backed loans often fall between 6% and 9%, while hard money lenders also commonly charge origination fees of 1% to 5%.

That's the first rule. Speed costs money.

What a hard money lender is really evaluating

A new borrower often thinks the lender is asking, “Is this owner bankable?” That's not the right question. The lender is really asking, “Is this asset strong enough, and is the path to repayment believable enough?”

That changes the conversation.

Instead of obsessing over whether the borrower looks perfect on paper, the file needs to answer practical deal questions:

| Focus area | What the lender wants to understand |

|---|---|

| Collateral | Is the asset valuable, marketable, and documented clearly? |

| Use of funds | Will the capital solve a real problem or support a near-term opportunity? |

| Exit strategy | How does the lender get repaid without wishful thinking? |

| Borrower discipline | Does the borrower present the deal clearly and respond quickly? |

A borrower who understands this gains an advantage. A broker who understands it becomes valuable to both sides.

For a broader beginner-friendly foundation, this introduction to hard money lending basics helps frame the terminology and deal flow.

Where hard money fits and where it doesn't

Hard money works best when speed matters and the asset is strong. Common examples include bridge situations, acquisition gaps, commercial property opportunities, and deals where the borrower needs fast execution more than low-cost capital.

It doesn't fit every business need. If the borrower wants cheap long-term money, hard money is the wrong product. If there's no clean collateral story and no credible exit, it's also the wrong product.

Practical rule: Use hard money for short-term leverage, not long-term comfort.

A disciplined advisor doesn't sell the product. A disciplined advisor solves the problem. Sometimes that solution is hard money. Sometimes it isn't. That honesty is what builds a durable book of business.

How to Find and Vet a Reputable Hard Money Lender

Finding a lender isn't hard. Finding one worth sending deals to is where real professionals separate themselves.

A serious borrower or broker starts with channels that tend to surface active dealmakers. Referrals from attorneys, CPAs, commercial real estate contacts, and experienced funding professionals usually beat random internet searches. Local investor communities can also expose who closes and who talks big but disappears when paperwork starts.

Then the work begins. Vetting.

What a real underwriting process looks like

A reputable lender has a process. Not a vague promise. A process.

According to Perfect Alliance Capital's breakdown of business acquisition hard money underwriting, a hard money lender for business often uses a five-step underwriting approach centered on collateral value. The same source explains that the key metric is loan-to-value, typically 60% to 75% of after-repair value, and that approval often closes in 5 to 15 business days based on property value rather than credit.

That tells a broker what to look for. A legitimate lender should be able to explain, in plain language, how the file moves from inquiry to funding.

A useful vetting checklist looks like this:

Ask how the lender sizes risk

A real lender can explain collateral standards, what documentation matters, and how repayment is evaluated.Test timeline credibility

Fast funding is possible, but only if the borrower can deliver documents quickly and the lender can move decisively.Review fee transparency

Good lenders spell out costs early. Confusing charges and shifting terms signal trouble.Check communication quality

If a lender can't answer straightforward questions before the file is submitted, the closing process won't improve later.

Red flags that should end the conversation

Not every lender deserves a second call. Some should be ruled out immediately.

- Pressure before review: If someone pushes for commitment before understanding the deal, that's a bad sign.

- Foggy explanations: If terms are vague and answers keep changing, trust the pattern.

- No discussion of exit: A lender who doesn't care how repayment happens is not being flexible. That lender is being reckless.

- Sloppy presence: Poor documentation habits, broken processes, and amateur communication usually show up again at closing.

A clean term sheet from the wrong lender can still become a dirty closing.

Strong brokers keep a short list of dependable funding partners and update it constantly. They know who handles real estate well, who likes bridge situations, who gets nervous around complicated ownership structures, and who needs hand-holding on every file. That knowledge turns guesswork into placement strategy.

Structuring the Deal and Partnering for Success

A weak deal package gets ignored. A tight package gets reviewed.

That's why many borrowers fail before underwriting even starts. They send fragments. The lender receives partial financials, vague use-of-funds language, and an exit strategy that sounds more like hope than planning. Then the borrower wonders why nobody calls back.

A professional package does three jobs. It makes the opportunity understandable, it reduces perceived chaos, and it shows that the person submitting the deal respects the lender's time.

What the submission package must do

The package doesn't need to be fancy. It needs to be clear.

A strong submission usually includes the business purpose, collateral details, relevant financial documentation, and a blunt explanation of repayment. If the deal involves acquisition, bridge financing, or a turnaround, the file should explain what changes after funding. Lenders don't finance mystery.

The most overlooked piece is the exit strategy. Here, many otherwise promising deals fall apart. If repayment depends on perfect execution, the lender will hesitate. If repayment depends on a realistic sale, refinance, or revenue event, the conversation gets easier.

A quick underwriting prep checklist helps:

- State the request cleanly: loan amount, use of funds, collateral, and timing.

- Show the asset clearly: ownership, condition, value story, and supporting documents.

- Explain the business case: why this transaction matters and what funding enables.

- Define the exit: refinance, sale, improved cash flow, recapitalization, or another credible path.

One newer challenge deserves attention. A projected trend for 2025 to 2026 cited by Credibly's minority business lending guide says 45% of online lenders now require API-linked bank statements for digital cash flow verification. That matters because many borrowers still expect to upload PDFs and move on. Brokers who know how to guide clients through digital verification remove friction that less prepared advisors don't even see.

Scripts that sound professional because they are

A good first message to a lender isn't long. It's sharp.

Borrower seeks asset-backed financing for a time-sensitive business purpose. Collateral details, requested amount, and exit strategy are organized. If this fits current appetite, term guidance is requested before full file submission.

That message works because it respects the lender's filter.

A good borrower-facing script matters too:

This isn't about sending more paperwork blindly. This is about presenting the lender with a deal they can understand, price, and close.

For borrowers who need help pressure-testing costs before submitting, a business funding payment calculator can help frame whether the projected repayment fits the actual business plan.

The brokers who win in this space don't act like hype-driven salespeople. They act like translators between capital and opportunity. That's why lenders keep taking their calls.

The Blueprint to a Six-Figure Business Loan Broker Career

Once someone understands how a hard money lender for business thinks, a bigger opportunity becomes obvious. The true value isn't just using the product. The value is becoming the person who knows when to use it, how to package it, and where to place it.

That is a business.

For aspiring entrepreneurs, consultants, sales professionals, former bankers, CPAs, and service providers, this niche has real appeal because it can be built from home, run remotely, and expanded through relationships instead of expensive infrastructure. Business owners need funding in every economy. Banks still say no to deals that deserve another look. Someone has to bridge that gap.

Why this niche works as a home-based business

This business rewards people who can listen well, qualify quickly, and match deals to the right funding source. It doesn't require a massive office, a giant payroll, or a complicated inventory model. It requires judgment, process, and consistency.

That makes it attractive for people who want:

- Remote flexibility: deals can be sourced, packaged, and managed from a home office.

- Referral power: accountants, real estate contacts, credit professionals, consultants, and local business networks can become recurring lead sources.

- Scalability: one funded client can refer others if the experience was honest and effective.

- Recession resistance: when traditional lending tightens, alternative funding conversations often increase.

Professionals who already advise business owners can strengthen their positioning by studying broader relationship-building material, including these resources for financial advisors, then adapting the client communication principles to funding conversations.

How commission economics actually work

Many newcomers get confused, either underestimating the value of brokering or becoming unrealistic and fantasizing. Both mistakes are costly.

According to SoFi's explanation of business loan broker compensation, business loan brokers typically earn 1% to 3% of the total loan amount paid directly by the lender upon closing, and some agreements allow up to 5% depending on complexity and negotiation.

That structure matters because it aligns the broker's role with outcomes. No funded deal, no commission.

A responsible way to think about the business is this:

| Broker activity | Why it matters |

|---|---|

| Pre-qualifying deals | Saves time and protects lender relationships |

| Packaging files properly | Improves lender confidence and speed |

| Managing communication | Keeps deals from dying in avoidable confusion |

| Building referral channels | Creates repeatable, low-overhead lead flow |

This isn't a get-rich-quick lane. It's a professional services business with strong upside for disciplined operators. The people who last don't chase random deals. They build systems, maintain lender relationships, and become known as the person who can solve funding problems.

For anyone evaluating the career side more closely, this breakdown of business loan broker income realities adds useful context around how the model works over time.

The broker who lasts is the one who becomes dependable, not flashy.

That's the blueprint. Learn the products. Learn the lenders. Learn the borrower psychology. Then build a repeatable process around trust.

Your Next Step to Funding Deals and Earning Commissions

Many individuals stop at product knowledge. They learn what hard money is, maybe talk to a few borrowers, and then stall. The bigger move is turning that knowledge into a repeatable service.

That service solves two problems at once. Business owners get access to funding pathways banks often ignore. The broker gets paid for bringing clarity, structure, and lender access to deals that would otherwise stay stuck.

The real opportunity most people miss

A lot of people assume commission businesses require endless cold outreach and aggressive selling. This niche doesn't have to work that way. A smart operator builds around relationships, referrals, and visible expertise.

That means practical lead generation matters. For example, service providers exploring targeted outreach can study approaches for extracting Instagram data for leads and adapt the lesson that organized prospecting beats random activity every time.

The economics become very real when commission is understood in points. According to this explanation of broker compensation in points, one point equals exactly 1% of the loan amount, and a $150,000 working capital deal funded at 4 points generates a $6,000 commission for the broker.

That example matters because it removes fantasy and replaces it with simple math. A broker doesn't need hype. A broker needs funded files.

What to do next if this path fits

The right next move is not consuming endless content. It's building a real blueprint.

Start with the fundamentals:

- Learn deal triage: know which files fit hard money and which need another funding path.

- Build lender awareness: understand appetite, documentation standards, and communication expectations.

- Create referral conversations: position as a resource for business owners, advisors, and local professionals.

- Practice packaging: the cleaner the file, the faster the decision.

A funded deal changes a borrower's options. A funded deal also proves a broker can create value in the market.

This niche rewards people who can stay calm around urgency, communicate clearly, and keep learning. That's why it suits motivated entrepreneurs, side-hustlers, career changers, and professionals who want a flexible business with real demand behind it.

The opportunity is already there. Banks create it every time they reject a file that still has a path forward. The only question is who will step in and become the bridge.

Business Lending Blueprint shows everyday people how to build a real business loan brokerage from home, connect business owners with funding solutions, and earn commissions by brokering deals the right way. For anyone ready to stop circling the opportunity and start building a recession-resistant business with a proven process, the next step is simple. Watch the free training at Business Lending Blueprint or schedule a strategy session and see how this business can be built with clarity, structure, and the right support.