A lot of owners hit the same wall. The business is real, invoices are going out, customers are paying, and cash flow still gets squeezed. They apply for a business credit card to smooth out expenses, separate purchases, and protect working capital, then the application stalls because of personal credit.

That's frustrating, but it isn't random. Card issuers don't see a young business the same way the owner sees it. They see limited history, thin business credit, and a person behind the company whose personal habits may still be the clearest risk signal. For owners, that means the problem has to be solved in the right order. For brokers, it means this is one of the most practical entry points into a longer funding relationship.

A business credit card for bad credit is possible. It just usually won't come through the glamorous route often expected.

Table of Contents

- Why Your Personal Credit Haunts Your Business

- Laying the Proper Foundation for Business Credit

- Three Proven Pathways to a Business Card with Bad Credit

- Application Strategies and How to Rebuild Your Credit

- The Broker's Role in This Funding Scenario

- Start Building Your Blueprint for Funding Success

Why Your Personal Credit Haunts Your Business

A denial often sounds personal, but lenders usually treat it as procedural. A new or lightly established business doesn't yet have enough standalone borrowing history, so the owner's personal credit becomes the fallback screen.

That's why a person can run a legitimate company and still get turned down for a business card. Most standard business credit cards require a minimum FICO score of 670, and stronger rewards cards may want 700 or higher, while owners with personal FICO scores below 630 usually struggle to qualify for unsecured products and are often pushed toward secured business cards instead, according to Bankrate's breakdown of business credit card approval standards.

Why lenders lean on personal credit early

Lenders ask a simple question. If the business has limited credit history, who are they really extending trust to?

For many small businesses, the answer is still the owner. That's especially true when the company is new, has few reporting accounts, or hasn't established a clear borrowing pattern in its own name. Personal credit doesn't define the business forever, but it often shapes the first approvals.

Practical rule: Bad personal credit is a startup financing problem. It doesn't have to become a permanent business financing problem.

The useful shift is mental. A low score isn't just a rejection point. It's a signal that the file needs to be restructured before another application goes out.

What owners and brokers should take from this

Owners need to stop treating the next application as the solution. The setup behind the application usually matters more than the application itself.

Brokers can build trust quickly here because most clients don't need hype. They need a plain explanation of why the issuer looked through the business and back to the individual. A stronger understanding of business credit vs personal credit and how to build commercial credit helps clients see that separation is built over time, not created by filing paperwork once.

The good news is that credit challenges are usually workable when the business is prepared properly. The bad news is that many owners apply too soon, apply too often, and make the file weaker before they build it.

Laying the Proper Foundation for Business Credit

The fix starts before the card search. A lender wants evidence that the business is operating as a business, not just as an extension of the owner's personal wallet.

What lenders want to see before an application

A clean foundation does three things. It creates legitimacy, it improves documentation, and it gives the underwriter a clearer story.

That usually means:

- A separate legal entity: An LLC or corporation helps establish that the business is more than a side account attached to personal spending.

- An EIN in the business name: This is basic, but it matters because lenders expect a formal tax identity for the company.

- A dedicated business bank account: Mixing personal and business deposits creates confusion fast. A clean account history makes the file easier to evaluate.

- Consistent business information: The legal name, address, phone, and bank records should match across documents and applications.

Many owners also benefit from reviewing how they get business credit without using personal credit before they submit anything. That helps them stop chasing shortcuts and start building the file lenders want.

Separate records don't guarantee approval. They do make the business look real, organized, and easier to underwrite.

Operational discipline matters here too. Owners who control overhead, keep records tight, and maintain cleaner financial systems are easier to fund. For teams trying to streamline operations and reduce costs, that kind of cleanup often supports credit readiness as much as it supports day-to-day cash flow.

Why the EIN-only shortcut usually fails

A lot of owners hear the same promise online. Get an EIN, apply in the business name, and bypass personal credit. That sounds simple, but it usually isn't true for smaller firms.

According to Slash's analysis of EIN-only startup card approval, some EIN-only approvals do exist, but they typically require high monthly revenue of $50K to $100K+ and venture backing, which makes them inaccessible to 95% of small businesses with bad personal credit. That's the key distinction most content skips.

The primary issue isn't whether an EIN exists. It's whether the business profile is strong enough for an issuer to ignore the person behind it.

For most startups and owner-operated businesses, an EIN is necessary but not sufficient. It's part of the file, not a magic bypass. Brokers who explain that clearly save clients from wasting applications on products they were never likely to qualify for.

A strong readiness checklist usually includes the entity, EIN, bank account, basic financial organization, and a plan for how the business will begin generating its own credit references. Without that, the application is just exposing weak spots sooner.

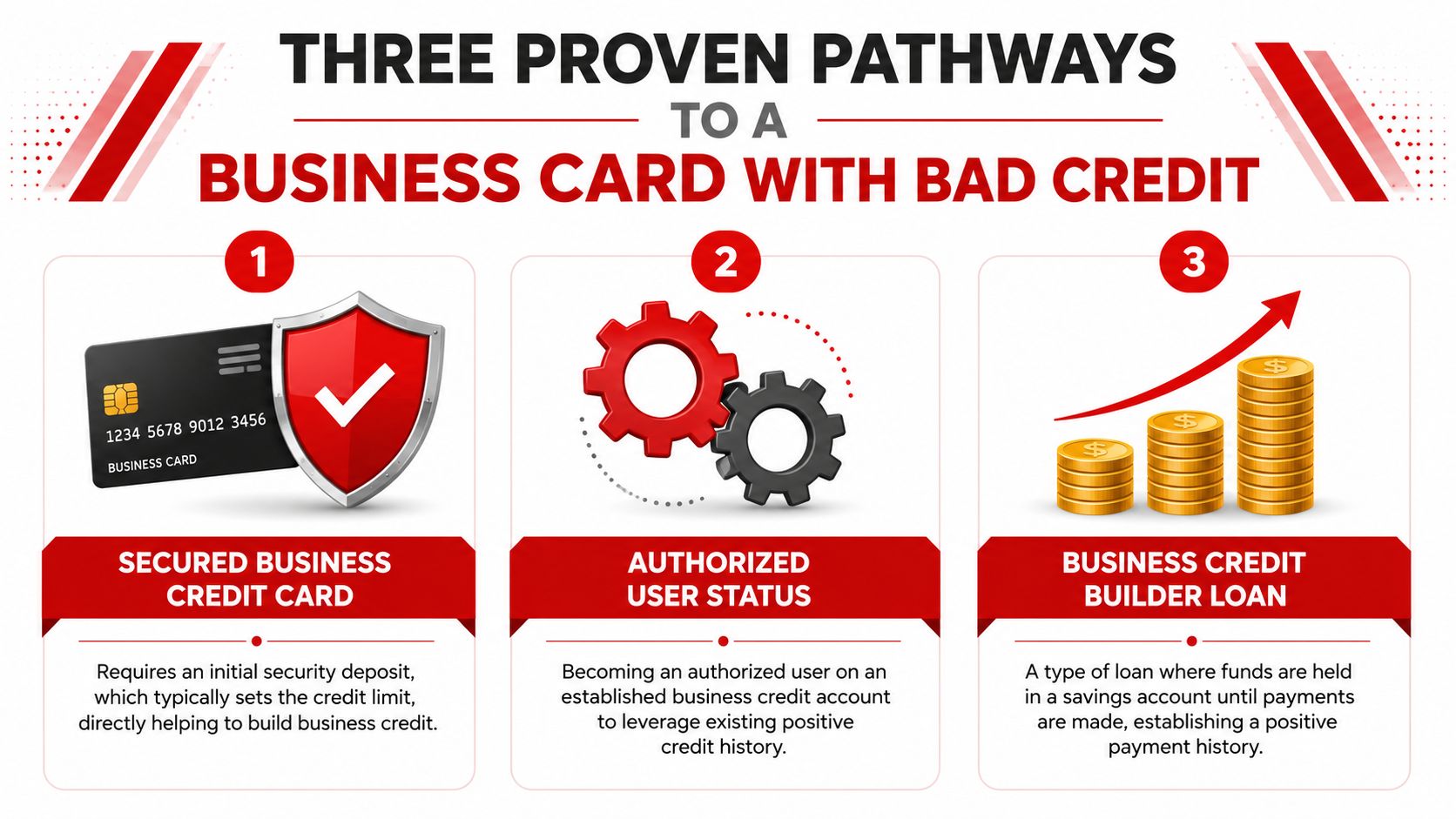

Three Proven Pathways to a Business Card with Bad Credit

There isn't one universal route to a business credit card for bad credit. There are several, and each one solves a different problem. The strongest strategy depends on whether the business needs immediate spending capacity, credit-building history, or a bridge to better approvals later.

A quick comparison of the three routes

| Pathway | Primary Requirement | Key Advantage | Key Disadvantage |

|---|---|---|---|

| Secured business credit card | Cash deposit | Most direct path to an account in the business name | Ties up cash and may come with expensive terms |

| Authorized user or strong credit support | Access to a well-managed existing account | Can help establish history without starting from zero | Depends on another person or business relationship |

| Business credit builder accounts | Separate entity and reporting vendor activity | Builds commercial profile more independently | Takes patience before stronger card options open |

Pathway one secured business credit cards

This is the path most owners with weak personal credit see first. It's straightforward. The applicant puts down a cash deposit, and that deposit usually determines the starting limit.

The upside is access. Secured cards are often the first realistic option for an owner who can't qualify for a standard unsecured product. They can also help create separation between personal and business spending if used carefully.

The downside is cost. According to Nav's review of secured business cards for bad credit, secured cards are often tied to 3 to 5 times higher APRs, with an average of 29.99% versus 14.99%, and cardholders with bad credit can incur $1,200+ in annual fees and interest on average, compared with $350 for unsecured peers. That's why a secured card should be treated as a stepping stone, not a long-term home.

Pathway two authorized user or strong credit support

Some owners can gain traction by attaching themselves to an existing well-managed business account through authorized user status or another form of strong credit support. This doesn't fix the entire profile, but it can reduce the “blank file” problem and help the owner demonstrate access to responsible account behavior.

This route works best when the supporting account is healthy and the arrangement is handled transparently. It works poorly when people assume association alone will replace the need for documentation, discipline, and separate business setup.

A supported file can open a door. It won't keep the door open unless the business starts producing its own track record.

For brokers, this route is less about pushing a tactic and more about screening carefully. If the support relationship is shaky, temporary, or undocumented, the client often does better with a slower but cleaner credit-building path.

Pathway three business credit builder accounts

This is the route many owners should start earlier than they do. Instead of forcing a card approval first, they build commercial payment history through reporting vendor tradelines and similar business credit builder activity.

According to Nav's guidance on establishing business credit, the most effective method for owners with bad personal credit is to create a fully separate business entity, secure an EIN and a D-U-N-S® number, then open reporting Tier 1 vendor accounts. With on-time or early payments over 3 to 6 months, over 70% of small businesses successfully build their first business credit score within 9 months using that path.

That matters because it changes the story lenders see. Instead of one owner with weak personal credit, the underwriter starts seeing a business with its own payment behavior.

Owners who want a practical starting point often benefit from reviewing vendors that report business credit. That's where many files begin to gain traction.

What works best in the real world

Different situations call for different sequencing:

- Need a card soon and have available cash: A secured card may be the fastest starter option.

- Have access to a strong supporting account: Authorized user status may help establish momentum.

- Need durable separation from personal credit: Reporting vendor accounts usually offer the cleanest long-term foundation.

The mistake is treating these routes as competing ideologies. In practice, they often work best when staged properly. An owner may start with one route, use it carefully, then graduate to stronger products after the business develops a profile of its own.

Application Strategies and How to Rebuild Your Credit

Getting approved is only half the job. The other half is making sure the new account actually improves the file instead of becoming another expensive problem.

How to apply without sabotaging approval odds

Owners with bad credit often make the same move after a denial. They submit more applications. That usually makes the profile look more desperate, not more qualified.

A tighter approach works better:

- Wait until the business setup is complete. The entity, EIN, and bank account should already be in place.

- Match the application to the file. If the business is still early and personal credit is weak, a starter product usually makes more sense than chasing premium unsecured cards.

- Submit one targeted application at a time. Spray-and-pray rarely helps.

- Prepare documents before applying. Inconsistent business details can cause preventable delays or denials.

For owners building through reporting accounts first, tradeline reporting that helps build business credit can make later card applications look more credible and less speculative.

How to use starter credit without getting trapped

A starter card is supposed to lead somewhere better. If it only creates fees, interest, and balance pressure, it isn't solving the problem.

That's why usage discipline matters more than card ownership. The owner should treat the account like a credit-building tool, not extra income.

- Keep balances modest: A smaller revolving balance is easier to manage and easier to pay down predictably.

- Pay on time without exception: Payment reliability is the habit that gives the account value.

- Use the card for planned business expenses only: Recurring, budgeted expenses are safer than emotional or emergency swipes.

- Review fees and reporting details: Some products cost too much relative to the benefit they provide.

Watch-out: The wrong secured card can become a credit trap. If the terms are expensive and the usage is loose, the account may cost more than it helps.

The goal is graduation. A business owner should use the starter phase to strengthen personal discipline, create cleaner business records, and make the next financing conversation easier. Brokers who stay involved after approval become more than placement agents. They become trusted advisors who help the client move from survival credit to strategic credit.

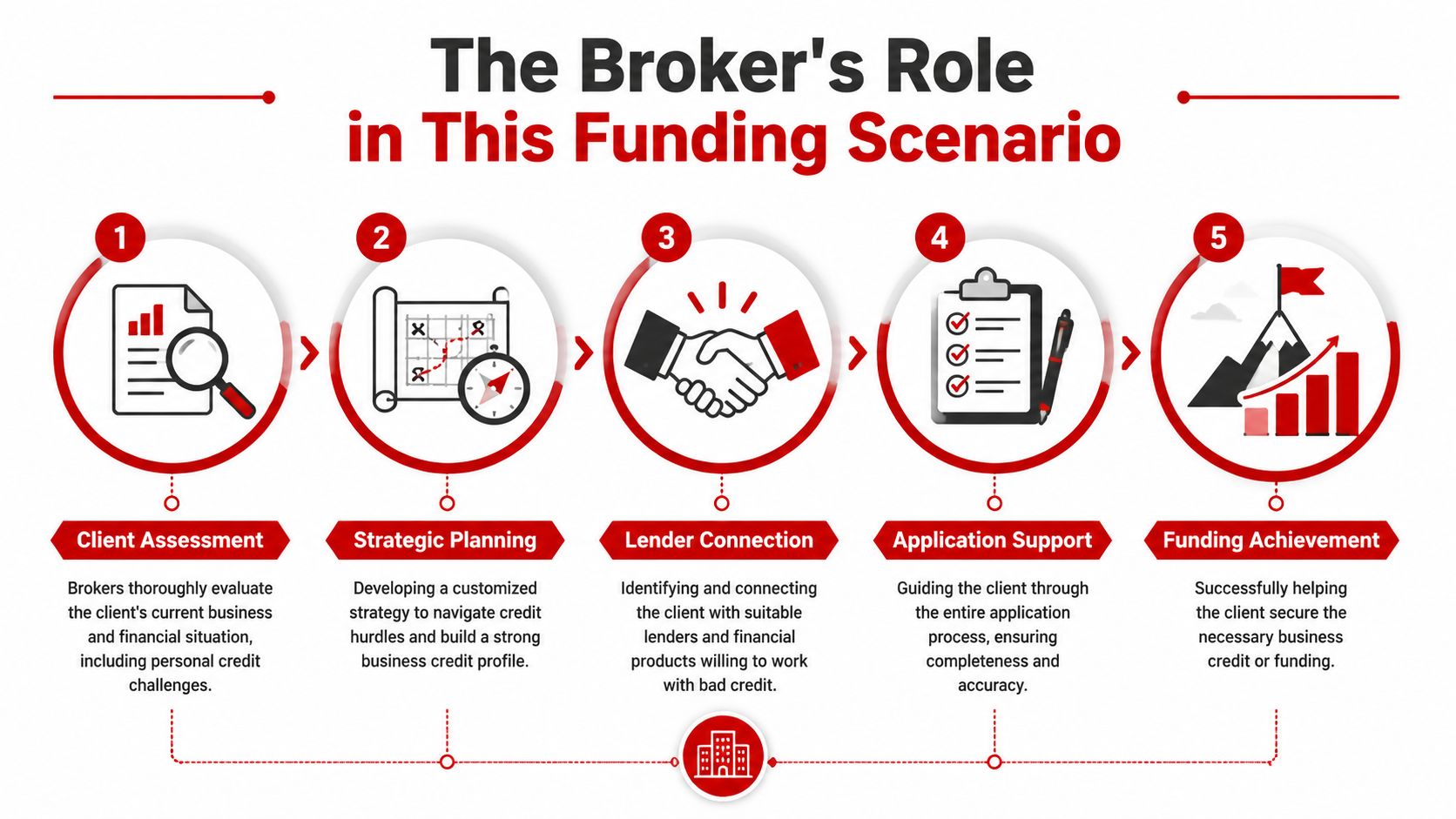

The Broker's Role in This Funding Scenario

Owners with bad credit rarely need another generic rejection. They need someone who can look at the full file, identify what's blocking approval, and map out the next workable step.

That's where a broker creates real value. Not by forcing a product, but by translating credit problems into funding strategy.

Why this problem creates a valuable advisory service

A business owner with poor personal credit often arrives confused. They may think the issue is the lender, the EIN, the industry, or timing. A broker can identify whether the actual blockage is weak personal credit, an incomplete entity setup, missing banking separation, or unrealistic product selection.

That kind of guidance is valuable because it leads to more than one transaction. If the broker helps the client establish business credibility, organize documents, choose the right starter product, and avoid unnecessary denials, the relationship usually deepens.

This is why credit-challenged clients can become strong long-term clients. Today they may need a basic card strategy. Later they may need a line of credit, a term loan, equipment financing, or growth capital through alternative lenders.

The first win is often small. The trust built from solving it can lead to much larger funding opportunities later.

For someone building a home-based brokerage, this creates a practical service model. It can be done remotely, it fits referral-based business development, and it naturally leads to recurring relationships with accountants, consultants, bankers, real estate professionals, and other service providers who see business owners struggle with financing.

How brokers monetize the relationship

Brokers typically earn money when funding closes, rather than when advice is given. According to this explanation of broker compensation in funded deals, brokers often get paid in points, where one point equals 1% of the loan amount. The example given is a $150,000 loan producing $1,500 in broker compensation.

That matters for two reasons. First, it aligns the broker's incentive with the client's outcome. Second, it shows how a broker can build a scalable business by solving financing problems that traditional banks often leave unresolved.

A broker who understands business credit card scenarios for bad credit isn't just helping with cards. That broker is learning how to diagnose fundability, coach clients through readiness, and create referral-driven income from real business problems.

Start Building Your Blueprint for Funding Success

Bad personal credit can delay a business, but it doesn't have to define it. The owners who make progress usually do three things well. They separate the business properly, choose a realistic starting path, and use early credit with discipline.

That same process also creates a strong opportunity for aspiring brokers. Business owners need help navigating denials, understanding trade-offs, and finding practical options outside the usual bank conversation. A broker who can guide that process becomes useful fast, especially in a market where many owners need funding but don't know how to become fundable first.

A business credit card for bad credit isn't really about finding one magical issuer. It's about building a file that deserves better options over time. For owners, that means patience and structure. For brokers, it means there's a repeatable, high-value service to offer clients who have been told no and need a smarter path forward.

The strongest funding businesses aren't built on hype. They're built on solving everyday money problems for business owners, doing it consistently, and becoming the person referral partners trust when a client needs financing guidance.

Business owners who need a clearer funding path, and entrepreneurs who want to build a flexible, home-based brokerage around solving these problems, can start with the free training from Business Lending Blueprint. It breaks down how to work remotely, help business owners access funding through alternative lenders, build recurring referral relationships, and create a practical brokerage business without relying on hype. Those who want a deeper look can also schedule a strategy session and see whether this model fits their goals.