A business owner walks into a bank with solid sales, a real need for capital, and confidence that the file will get approved. A week later, the answer is no. The banker points to documentation gaps, credit concerns, collateral issues, or cash flow that doesn't fit the bank's box. The owner hears rejection. A skilled broker hears opportunity.

That gap between what a bank wants and what a business can provide is where a commercial loan brokerage gets built. Anyone who understands the requirements for a commercial loan can stop treating denials like dead ends and start treating them like deal flow. The businesses are still fundable. They just need the right structure, the right lender, and the right packaging.

For aspiring brokers, this matters because the work isn't just about finding money. It's about diagnosing why a file won't clear one channel, then repositioning it for another. That skill creates repeat referrals from owners, CPAs, consultants, real estate professionals, and other local partners who all know businesses need funding but don't know how to get through underwriting.

Table of Contents

- Why Most Businesses Get Denied for Commercial Loans

- The Three Pillars of Commercial Loan Eligibility

- Decoding the Required Financial Paperwork

- The Truth About Collateral and Personal Guarantees

- Traditional Banks vs Alternative Lenders A Broker's View

- Your Broker Checklist for a Winning Loan Application

- Turn This Knowledge into a Thriving Broker Business

Why Most Businesses Get Denied for Commercial Loans

A common file looks good on the surface. The owner has been operating for years, customers are paying, and the business needs working capital, equipment financing, or a real estate loan. Then underwriting starts asking harder questions. The bank wants cleaner statements, stronger ratios, more collateral, or a guarantor profile that clears internal policy. The deal stalls.

This happens because banks don't lend on effort. They lend on documented risk. If the borrower can't fit the bank's model, the bank usually won't spend time trying to reshape the file. That leaves plenty of good businesses in the middle. They aren't fraudulent, distressed beyond repair, or unfundable. They just don't match a rigid credit box.

A trainee broker should understand one thing early. Most rejected borrowers still need capital, and many of them can still qualify somewhere else. That's why knowing how lenders evaluate repayment ability matters so much. A basic grasp of debt service coverage ratio standards helps a broker see what the bank saw, then decide whether the file needs restructuring, better documentation, or a different lending path.

Bank denial doesn't always mean bad business. It often means bad fit.

The funding gap is where brokerage businesses become valuable. A banker might only offer one product line. A broker can look at the same borrower and ask better questions.

- Was the deal denied for structure? A borrower may have requested the wrong product for the use of funds.

- Was it denied for timing? Some files fail because the owner applied before the numbers were organized.

- Was it denied for lender fit? A strict bank may decline a file that an alternative lender can evaluate more flexibly.

That's the practical opportunity. A broker who understands the requirements for a commercial loan stops reacting emotionally to denials and starts diagnosing them. That approach closes more deals and builds referral trust because clients remember who found a path forward after the bank said no.

The Three Pillars of Commercial Loan Eligibility

Commercial loan eligibility works like a three-legged stool. If one leg is weak, the deal may still stand, but the lender choice narrows. If two legs are weak, the broker needs a sharper strategy. If all three are weak, the file usually needs repair before it needs a lender.

The three pillars are time in business, annual revenue, and credit score. For alternative business loans, the primary qualification filters are often 12 to 24 months in business, annual revenue of $2 million or more, and credit scores commonly in the 600 to 680 range, while traditional bank loans often want 2 or more years in business, $5 million or more in revenue, and credit scores above 700, according to LendingTree's overview of alternative lending requirements.

Time in Business Tells Lenders How Much Uncertainty They Are Buying

A newer company might be healthy, but lenders still see less operating history. That means fewer statements, fewer trend lines, and less proof that management can handle pressure. Time in business is really a stability test.

A broker should ask early whether the business has enough operating history for the target product. That prevents wasted submissions and helps frame expectations. Some deals belong with traditional lenders. Others belong with lenders that can handle shorter histories if the rest of the file is strong.

For owners preparing to raise capital, good preparation matters before any application is submitted. Practical operators often benefit from essential capital raising advice that forces them to clarify the funding purpose, cash needs, and investor or lender narrative.

Revenue and Credit Shape Lender Options

Revenue tells the lender whether the business has enough commercial scale to support debt. Credit tells the lender how the owner or business has handled obligations in the past. Neither one stands alone.

A broker should never look at top-line sales in isolation. Gross revenue may look strong while margins are weak, debt load is heavy, or cash management is sloppy. That's why understanding top-line revenue in lending context helps new brokers avoid overestimating file strength.

A quick screen can keep the process efficient:

| Pillar | What a broker wants to know | Why it matters |

|---|---|---|

| Time in business | Is there enough operating history for the target lender? | It affects risk tolerance and documentation depth |

| Annual revenue | Are sales consistent and large enough for the request? | It shapes repayment capacity and lender appetite |

| Credit score | Is the borrower profile bankable or better suited for alternative funding? | It affects pricing, structure, and available products |

Practical rule: Prequalify on these three pillars before requesting a full document package. It saves time, protects relationships, and makes a broker look disciplined.

This is one reason structured training matters. A program like Business Lending Blueprint teaches new brokers how to screen deals, match borrower profiles to lender categories, and avoid wasting submissions on files that never had a realistic fit.

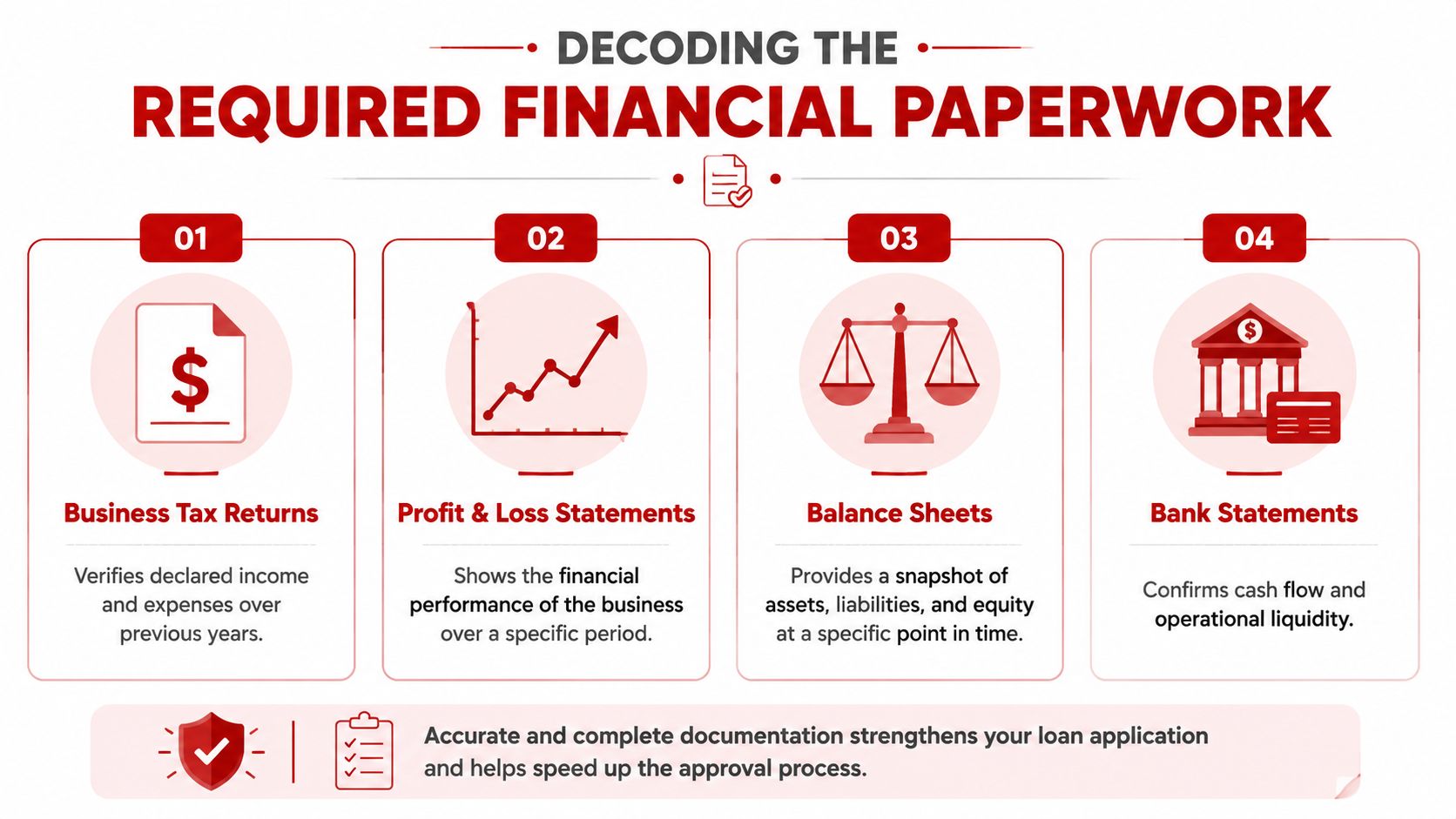

Decoding the Required Financial Paperwork

Most business owners think paperwork is the painful part of the loan process. Underwriters think it's the decision-making part. A broker should think the same way. Financial documents aren't just forms to collect. They are evidence, and they tell the lender whether the borrower's story holds up.

Lenders prefer steady net income that is at least 20% greater than total debt, and approval relies on three years of year-end balance sheets and income statements. If those statements are unaudited, business tax returns are mandatory, and personal financial statements are required because owners typically guarantee the debt, as explained in Woodsboro Bank's breakdown of commercial loan requirements.

What Lenders Want and Why They Want It

Three years of year-end statements give the lender trend lines. A single strong month can be staged. Multi-year performance is harder to fake. Underwriters use those statements to see whether revenue is stable, margins are holding, and operating expenses are creeping in the wrong direction.

Tax returns matter because they anchor the file in documents submitted to taxing authorities. If the borrower's internal financials look better than the returns, the broker should expect questions. Personal financial statements matter because many privately held business loans still depend on personal support behind the business entity.

A broker should review each document with a specific purpose:

- Income statements: Look for consistency, unusual swings, and whether earnings support the debt request.

- Balance sheets: Check debt levels, liquidity, and whether assets appear strong enough to support the structure.

- Tax returns: Confirm that the core financial story matches what was officially reported.

- Bank statements: Use them to test whether deposits and operating activity support the borrower's claims.

For owners cleaning up records before any financing event, even adjacent guides can be useful if they reinforce clean presentation. A concise example is Bizbe's guide for selling FedEx routes, which is helpful because it stresses clear, organized financial statements that hold up under buyer and lender review.

How a Broker Turns Paperwork Into an Approval Story

Good brokers don't dump files into underwriting. They package them. That means reading the numbers before the lender does and identifying what will raise concerns.

A debt summary is one of the fastest ways to reduce confusion. If a borrower doesn't know current obligations, maturity dates, and payment load, the application will wobble. Reviewing a business debt schedule helps a broker line up the existing debt picture before the lender has to ask twice.

Red flags usually show up in patterns, not isolated details.

If the business says cash flow is strong but statements show frequent cash squeezes, the issue isn't the paperwork. The issue is credibility.

A broker should look for these problems before submission:

- Mismatch problems such as internal statements that don't line up with tax returns.

- Timing problems such as stale statements or missing year-end reports.

- Story problems such as a large request with no clear use of funds or repayment logic.

When the file is clean, the broker's job gets easier. When the file is messy, the broker still adds value by identifying what needs repair before the lender sees it. That's how paperwork stops being a chore and starts becoming an advantage.

The Truth About Collateral and Personal Guarantees

Many borrowers assume commercial financing is impossible without strong collateral and a personal guarantee. Many new brokers assume the same thing. That assumption leaves deals on the table.

Traditional lenders like collateral because it gives them a secondary source of repayment if the business fails. They like personal guarantees because they want another party legally responsible if the company defaults. That structure makes sense from the lender's side. It doesn't mean every borrower must fit it.

What Traditional Lenders Are Protecting Against

Collateral and guarantees exist because lenders are trying to control loss severity, not just default risk. A profitable business with limited hard assets can still make a traditional lender uncomfortable if there isn't enough fallback protection.

That's why guarantee language matters so much. Brokers who want to understand the legal side of personal support should review how attorneys describe managing financial obligations with guaranty. The key lesson is simple. A guarantee is not a casual signature. It carries real personal exposure.

When the deal involves real estate, borrowers also run into down payment requirements and stricter collateral standards. Those files often demand more equity from the borrower and more documentation around the business structure and property use.

Where Brokers Create Value When Assets Are Thin

Brokers earn trust. According to Third Way's report on underserved business financing, 73% of small business loans are denied due to insufficient collateral or poor credit. That same report points to non-traditional routes such as CDFI-backed loans, SBA 504 loans requiring only 10% down, and revenue-based factoring that bypasses collateral entirely.

That changes the conversation. Instead of telling a borrower, “come back when you own more assets,” a broker can ask better questions.

- Is the borrower asset-light but revenue-producing? Revenue-based products may fit better than collateral-heavy loans.

- Is the down payment the obstacle? A different program may reduce the cash injection burden.

- Did the bank object to both collateral and speed? Short-term bridge solutions may keep the business moving while a stronger file is built.

Some borrowers will still need a guarantee. Some won't qualify without one. Some may fit products with far less emphasis on hard collateral than they expected. Brokers who understand options like hard money commercial loan structures can often keep a deal alive when a conventional lender would shut it down immediately.

Borrowers don't need false reassurance. They need an accurate map of which lenders care most about assets, which care most about cash flow, and which can work around both.

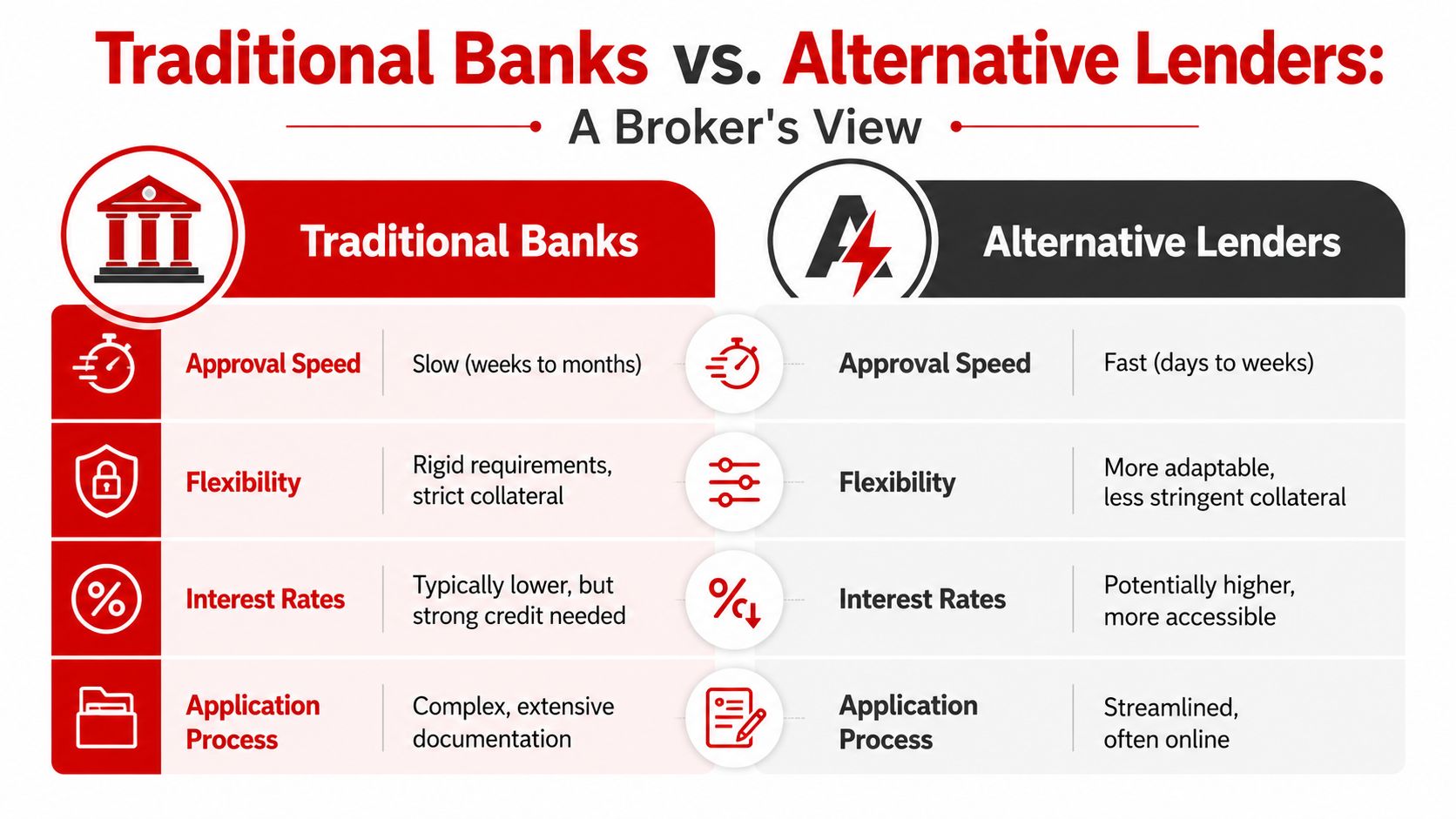

Traditional Banks vs Alternative Lenders A Broker's View

The strongest brokers don't argue that one lender category is always better. They learn where each category works, where each one fails, and how to place deals accordingly. That judgment is what clients pay for.

Large banks approve only about 13.8% of small company loans, while smaller banks approve 19% and non-bank lenders approve nearly 25%, according to Capital Bank's summary of business loan statistics. For brokers, that approval gap explains why so many business owners need help beyond the branch office.

Where Banks Work Well

Banks are a strong fit for clean borrowers. That usually means stronger credit, cleaner financials, better documentation, and a request that fits standard policy. When a client qualifies, bank capital can be attractive and stable.

But banks are slow by design. They document more, escalate more, and stay inside policy. That's not a flaw. It's the model. A trainee broker should learn not to send a time-sensitive or imperfect file into a bank channel and hope personality will overcome policy.

A bank file tends to work best when:

| Situation | Bank fit |

|---|---|

| Clean financial statements | Strong |

| Well-documented business history | Strong |

| Need for speed | Weak |

| Limited collateral or uneven credit | Often weak |

Where Alternative Lenders Win Deals

Alternative lenders fill the gap banks leave behind. They often move faster, they may tolerate more complexity, and they can evaluate borrowers with different risk models. That matters when the business is viable but the file isn't conventionally clean.

Alternative financing also gives brokers more room to solve specific borrower problems. One client needs speed. Another needs flexibility around collateral. Another has credit issues but solid revenue. Another needs capital while waiting for a cleaner tax year to support a future bank application.

A broker's judgment matters because alternative products are not automatic solutions. They come with trade-offs.

- Speed versus price: Faster money can cost more.

- Flexibility versus documentation depth: Some lenders streamline the process, but they still want enough evidence to support repayment.

- Accessibility versus structure: A borrower may qualify, but only for a product that fits short-term needs rather than permanent financing.

The broker's job isn't to push every client into alternative lending. The job is to place each file where it has the highest chance of closing without creating the wrong kind of debt.

That's why this business can be resilient and home-based. Owners will keep needing capital in expansion cycles, tight credit cycles, and uncertain markets. Banks will keep declining borrowers who fall outside policy. Brokers who understand requirements for a commercial loan, and who know how to route files to the right funding channel, build referral relationships that keep producing deals remotely over time.

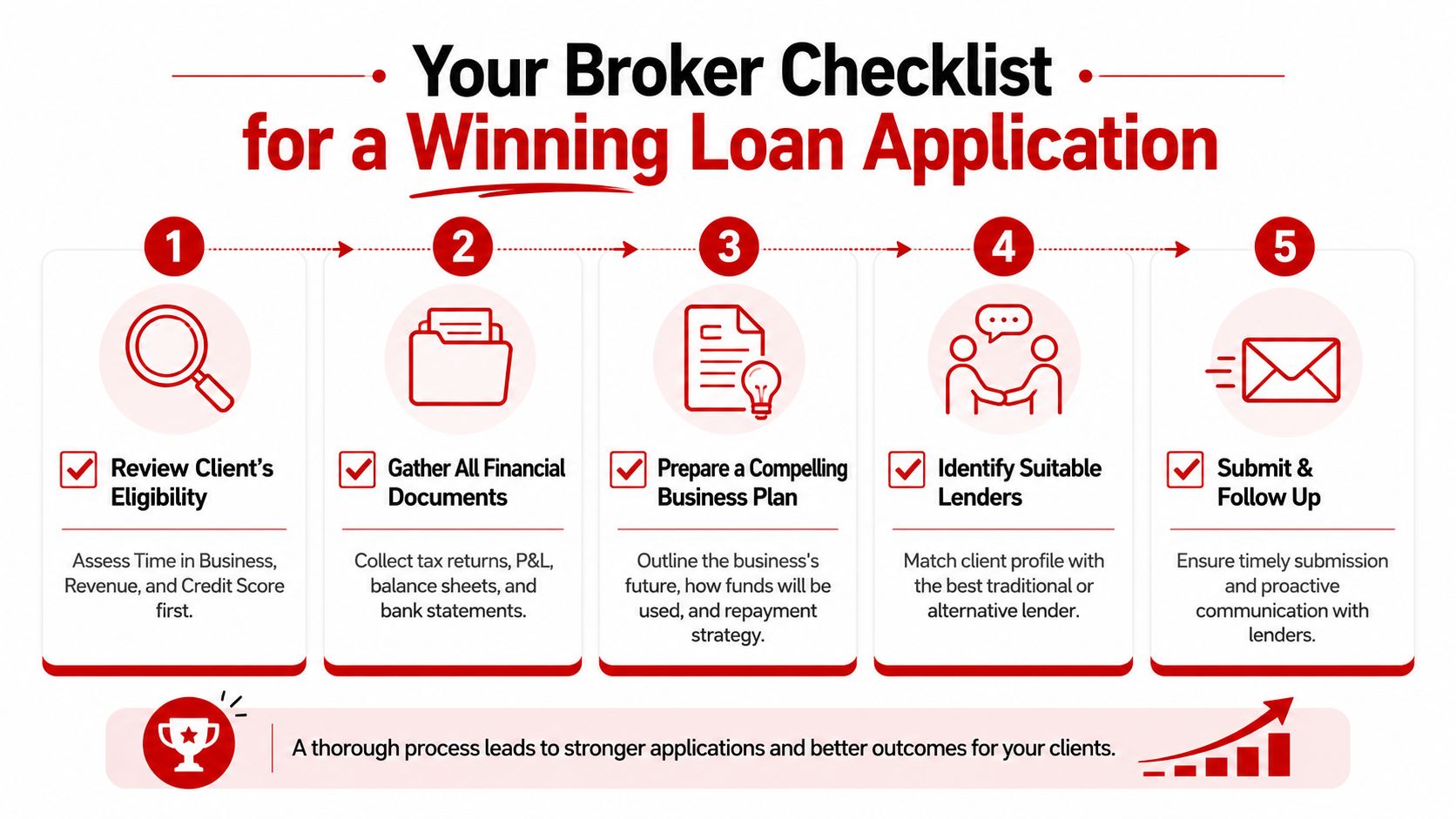

Your Broker Checklist for a Winning Loan Application

A winning loan application starts before the application. Brokers who wait until documents arrive to start thinking usually miss preventable problems. Brokers who run a repeatable process look more professional, move faster, and waste less time.

Prequalify Before Collecting a Stack of Documents

Start with the borrower interview. Clarify the use of funds, the urgency, the rough business profile, and whether the entity is properly formed. For commercial real estate loans, a key prerequisite is that the business is legally structured as an S corporation or LLC, and those loans typically require down payments ranging from 15% to 35%, based on NCUA commercial lending guidance.

That early screen saves embarrassment later. A borrower with the wrong entity setup, unclear ownership, or unrealistic down payment expectations isn't ready for submission.

Use a simple first-pass checklist:

- Confirm entity readiness: Verify that the borrower is operating through the correct legal structure.

- Clarify loan purpose: Expansion, equipment, working capital, acquisition, refinance, and real estate each lead to different lender types.

- Test expectation fit: If the borrower expects bank terms on a file that looks like an alternative deal, reset expectations early.

Package the File So an Underwriter Can Say Yes

Once the deal survives prequalification, build a file that answers lender questions before they ask them. That means the financials are organized, the purpose of funds is clear, and the weaknesses are addressed directly rather than hidden.

A clean broker workflow usually looks like this:

- Review eligibility first. Time in business, revenue quality, and credit profile still drive lender matching.

- Gather supporting documents. Tax returns, statements, and bank activity should support one coherent story.

- Write a clear narrative. Explain what the business does, why the capital is needed, and how repayment makes sense.

- Match lender type carefully. Don't force a conventional file into an aggressive product or vice versa.

- Follow up actively. Good brokers manage the process instead of merely waiting after submission.

A weak file gets weaker when the broker is vague. A fair file gets stronger when the broker is organized.

This checklist matters because brokerage is an operations business as much as a sales business. Anyone can take an inquiry. The brokers who close deals are the ones who can prequalify accurately, collect the right information, and present it in a way lenders can approve.

Turn This Knowledge into a Thriving Broker Business

Knowing the requirements for a commercial loan does more than help a borrower get approved. It gives a broker a marketable skill that businesses need in every economy. Owners need capital to buy property, smooth cash flow, expand operations, bridge shortfalls, and solve timing problems. Many won't fit a bank box. That doesn't mean they won't fund.

That's the business model. A broker learns how to read the file, spot the obstacle, and route the deal to the right capital source. Some files belong with banks. Some belong with alternative lenders. Some need cleanup first. That judgment is what creates commissions, repeat referrals, and long-term relationships with professionals who serve business owners.

It also fits the kind of business many people want to build now. This work can be done remotely, from home, with flexible scheduling and scalable referral channels. It appeals to consultants, bankers, CPAs, sales professionals, and entrepreneurs because it combines real client value with a practical path to recurring deal flow. There's no need for hype. The opportunity is strong enough on its own when the broker knows how to solve financing problems that others can't.

Business owners will keep getting declined, delayed, and misunderstood by traditional channels. Brokers who know how to step into that gap can build a serious, recession-resistant business around real funding solutions. To see how that model works in practice, watch the free training from Business Lending Blueprint or schedule a strategy session to map out the steps for launching a home-based business loan brokerage.