A lot of people looking at business loan brokering right now are in the same spot. They want a home-based business with low overhead, flexible hours, and work that solves a real problem. They also don't want to spend months learning products that banks already dominate.

That's why the hard money commercial loan niche matters.

When a borrower needs speed, a bank usually can't help. The file is too messy, the property isn't stabilized, the closing date is too tight, or the borrower's profile doesn't fit a conventional credit box. A broker who understands hard money can step into that gap, place a deal with the right private lender, and build strong referral relationships with investors, attorneys, real estate professionals, CPAs, and business owners who need answers fast.

For an aspiring broker, this isn't just another loan type. It's one of the clearest ways to become useful quickly, work remotely, and build a recession-resistant business around urgent funding needs.

Table of Contents

- The Hidden Opportunity in Speed

- Hard Money Versus Conventional Loans

- The Anatomy of a Hard Money Deal

- Spotting Opportunities for Your Clients

- Your Broker Playbook for Qualifying Deals

- Placing the Deal and Getting Paid

- Become the Go-To Broker for Fast Funding

The Hidden Opportunity in Speed

A commercial investor finds a distressed mixed-use property. The seller wants certainty and a fast close. The buyer has experience, some cash, and a plan to improve the building. What the buyer doesn't have is time for a conventional lender to review tax returns, committee the deal, ask for more documents, and miss the closing date.

That's where a broker becomes valuable.

A hard money commercial loan exists for situations where timing is the problem and collateral is the answer. The borrower isn't buying a perfect asset with a long runway. The borrower is trying to secure a property before someone else does, bridge a gap, fund a turnaround, or solve a financing problem that a bank won't touch on deadline.

Why urgency creates broker value

Banks usually win on price. Brokers in the hard money space win on usefulness.

When a client needs fast execution, the broker who can gather the right story, present the collateral clearly, and line up a lender quickly often becomes the person who saves the deal. That creates trust fast. It also creates repeat business because investors rarely have just one transaction.

Practical rule: The client rarely calls a hard money broker because the rate is attractive. The client calls because delay is more expensive than the loan.

This is why hard money lending is such an attractive niche for aspiring brokers. It lets them solve high-stakes problems without needing a giant staff, a storefront office, or a traditional banking platform. A laptop, a process, and a solid lender network can go a long way.

What this looks like in the real world

One client needs funding to close on a property that won't qualify for bank financing until repairs are complete. Another needs short-term capital while working on a refinance. Another is trying to move on an opportunity where the seller cares more about speed and certainty than squeezing out the last dollar.

Those are all brokerable situations.

For anyone learning the broader context of securing capital for property projects, it helps to see how different funding types fit different stages of a deal. Hard money sits in the part of the market where speed, asset strength, and execution matter most.

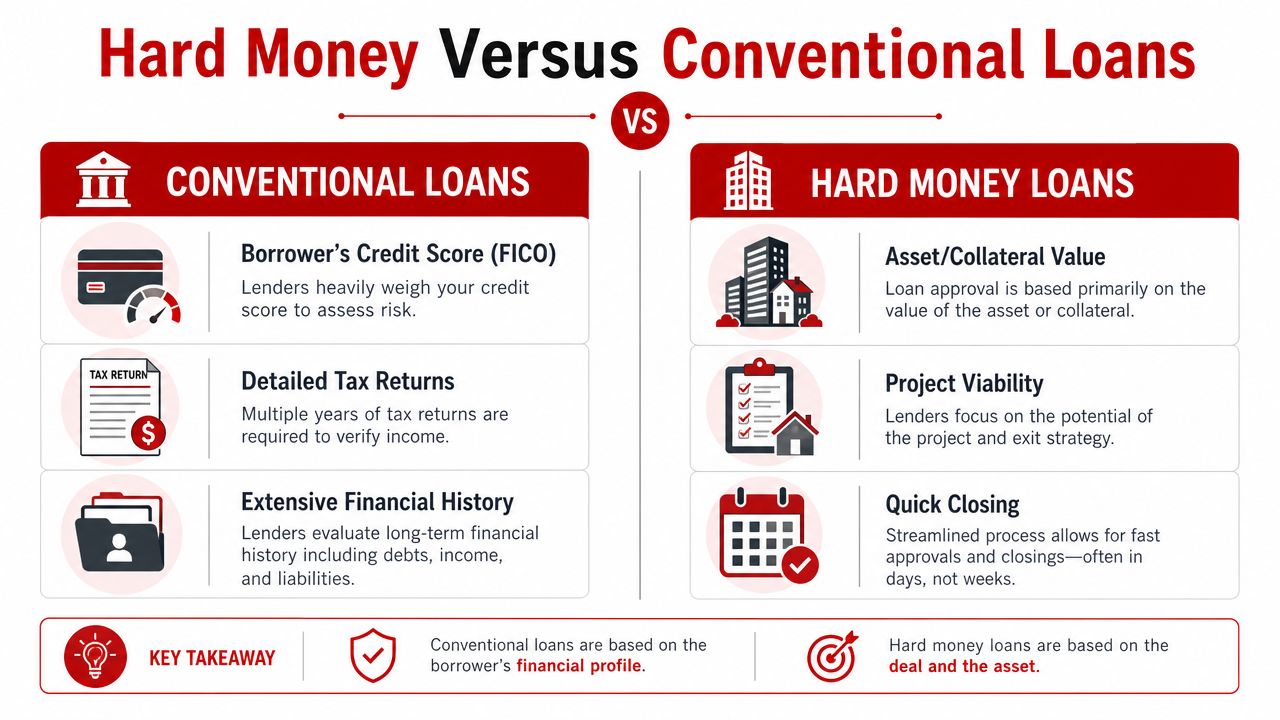

Hard Money Versus Conventional Loans

The simplest way to explain a hard money commercial loan to a new client is this. A conventional lender underwrites the borrower first and the property second. A hard money lender underwrites the property first and the borrower second.

That difference changes everything.

Two very different underwriting mindsets

A conventional commercial loan is like a formal job interview. The lender wants a full history. Credit quality, financial statements, tax returns, debt coverage, global cash flow, entity structure, tenant quality, lease history, and operating strength all matter.

A hard money deal is closer to a collateral-driven transaction. The lender still cares about the borrower and the exit, but the main question is whether the property gives enough protection if the plan doesn't go as expected.

That's why hard money often works when the borrower is not “bankable” on paper, even if the deal itself makes sense.

Side-by-side view

| Loan type | Main focus | Typical borrower fit | Best use case |

|---|---|---|---|

| Conventional commercial loan | Credit profile, income, financials, property performance | Stabilized borrower and stabilized asset | Long-term financing |

| Hard money commercial loan | Asset value, equity position, exit plan | Time-sensitive or transitional deals | Short-term bridge or opportunistic financing |

This distinction matters when talking to clients. A borrower who keeps saying, “My score is the issue,” may be framing the deal incorrectly. In hard money, the better question is, “What does the collateral look like, and how does the lender get repaid?”

A trainee broker who wants a stronger grasp of standard property financing structures can also review this guide to commercial property loans. It helps put hard money in context instead of treating it like a standalone product.

What conventional borrowers still need to understand

Hard money doesn't replace conventional lending. It fills the gap when conventional lending can't move fast enough or won't touch the deal in its current condition.

That's why many successful brokers learn to identify both the short-term need and the likely takeout path. If the client plans to refinance into cheaper debt later, the broker should understand the lender's future underwriting lens too. A basic understanding of debt service coverage ratio calculation helps with that conversation, especially when the borrower expects to transition into more traditional financing after stabilization.

The best brokers don't argue that hard money is better than a bank loan. They explain why it fits a specific moment in the life of a deal.

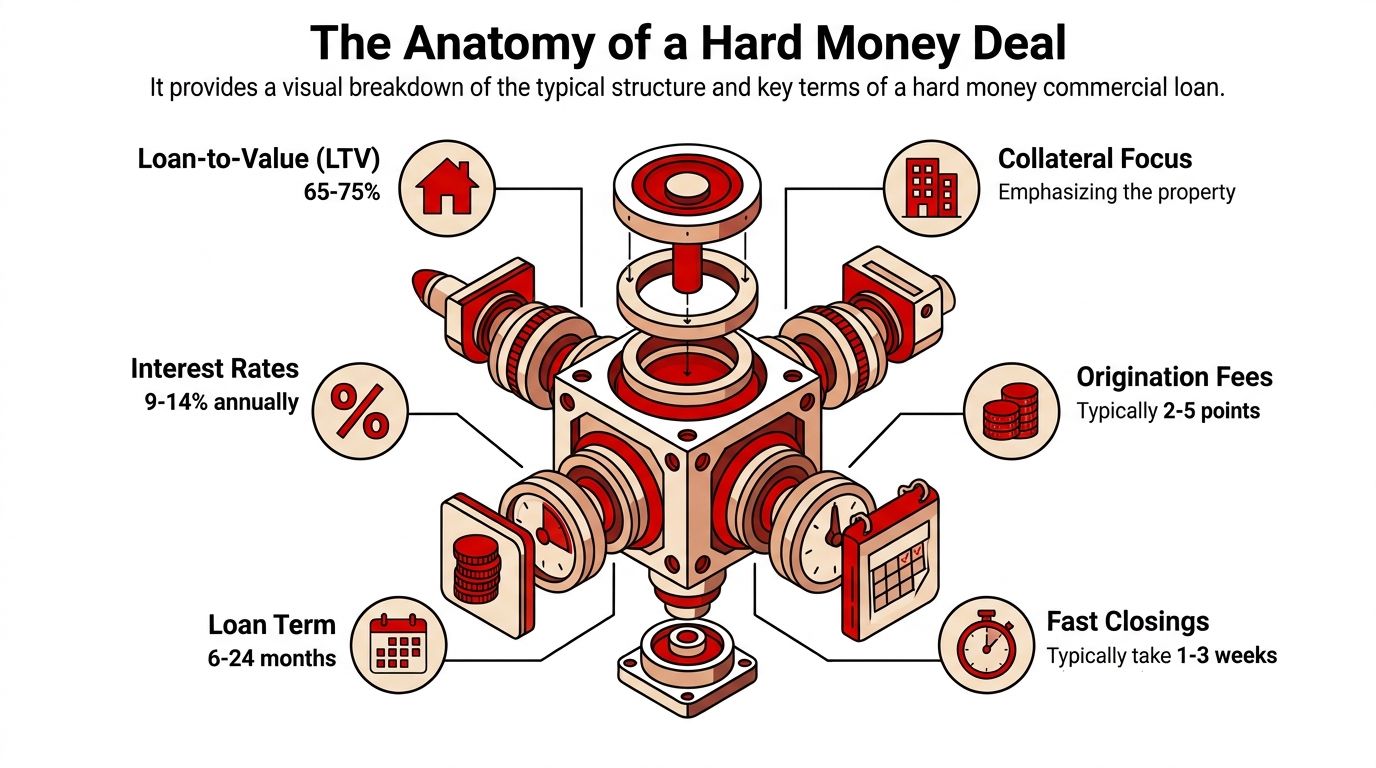

The Anatomy of a Hard Money Deal

A trainee broker usually loses the deal in one of two places. Either the numbers were never framed clearly, or the exit was never tested hard enough. Hard money files move fast, but they still break for predictable reasons.

The three numbers that drive the file

Start with rate, points, and loan-to-value ratio. If you cannot explain those three items in plain English, you will struggle to control the borrower conversation and you will send weak submissions to lenders.

As outlined in one commercial hard money overview, these loans often price higher than bank debt, commonly include upfront points, and usually stay in a moderate loan-to-value range. The same source also notes that lenders in this space may put more weight on collateral than on borrower credit, with some flexibility on credit score when the asset and exit are strong.

Rate is the monthly pain.

Points are the cash hit at closing.

Loan-to-value decides how much room the lender has if the borrower misses the plan.

A new broker should learn to read those numbers together, not one at a time. A file with a higher rate may still close if the financing is conservative and the borrower has a clean payoff path. A file with a lower rate can still be dead if the borrower is asking for too much against a troubled property.

What those numbers mean at the deal desk

Borrowers fixate on rate because it is easy to compare. Brokers get paid for seeing the whole structure.

If the lender is charging heavy points, confirm who is bringing that cash and whether it comes from the borrower, the seller, or another source. If borrowing capacity is tight, ask for proof of down payment early. Do not wait until underwriting to learn the borrower is short on equity.

This is also where commissions are protected. A broker who surfaces the cash requirement, the reserve expectation, and the lender's maximum financing threshold on day one creates fewer late-stage surprises. Fewer surprises means fewer blown closings.

Broker mindset: The loan terms matter, but the real question is whether the structure gives the lender a believable way out.

How lenders size up risk

Hard money lenders usually underwrite the property first and the borrower second. That does not mean the borrower is irrelevant. It means the asset, the basis, and the exit plan carry more weight than they would in a conventional file.

Focus your review on these pressure points:

- As-is value versus stabilized value: Know whether the lender is lending against today's condition or a post-rehab story.

- Borrower cash in: Verify the equity injection, not just the claimed liquidity.

- Time to payoff: Sale, refinance, partner buyout, or another documented exit should make sense inside the loan term.

- Property problems: Vacancy, deferred maintenance, title issues, and legal messes all affect proceeds and timing.

I tell new brokers to write the deal summary the way a lender thinks. What is the collateral? What is the basis? What is the ask? How does this loan get repaid? That habit alone improves submissions and raises close rates.

For brokers trying to sharpen sourcing judgment as well as placement, outside examples of how professionals find commercial lending deals can help. Internal training on hard money lenders for beginners is also useful if you want a clearer feel for how different lender types assess risk.

Spotting Opportunities for Your Clients

Hard money isn't a product that gets sold well through generic advertising. It gets placed when a broker recognizes a funding problem inside a real transaction.

The easiest way to learn this niche is to notice the patterns.

The bridge situation

A buyer has one property under contract and another property that hasn't sold yet. The long-term plan may be fine, but the timing doesn't line up. A hard money commercial loan can bridge that gap and keep the acquisition alive.

In this scenario, the broker's job is to keep the conversation centered on collateral, timeline, and payoff. If the borrower spends the entire call explaining old tax returns, the broker should redirect the discussion to the actual bottleneck.

The rehab play

An investor buys a building that needs work before a bank will touch it. Maybe occupancy is weak. Maybe deferred maintenance is obvious. Maybe the property is functional but far from financeable under conventional standards.

That's a classic hard money fit.

The borrower isn't trying to hold expensive debt forever. The borrower is trying to buy, improve, stabilize, and refinance or sell. A broker who understands this sequence can structure the conversation more intelligently than someone who treats every deal like a permanent loan request.

The problem asset

Some properties lose financing options because the story is messy. Partner disputes, partial vacancy, nonstandard conditions, title cleanup, deferred repairs, or a short closing date can all push a deal out of the bank lane and into the private lane.

That doesn't make it a bad deal. It makes it a different deal.

A broker who also understands capital stack conversations can be more useful here. Some transitional transactions involve layers beyond first-position debt, and familiarity with concepts like mezzanine capital definition helps when a client's structure gets more complex.

Many borrowers don't know they need hard money. They only know the bank said no, the seller won't wait, and the deal still makes sense.

The repeat-referral client

This niche becomes profitable when the broker stops chasing one-off leads and starts building referral channels around recurring deal flow.

Good referral sources include professionals who regularly encounter urgency, asset issues, or financing gaps. Those relationships matter because hard money borrowers often come back. A successful bridge borrower may need a refinance path later. A repeat investor may need another acquisition loan. A professional referral partner may bring several files over time.

That's how a remote broker turns one useful transaction into a durable business.

Your Broker Playbook for Qualifying Deals

A hard money file can look exciting and still be unfundable. New brokers lose time when they chase every urgent lead instead of screening for lender logic.

The fastest way to improve close rates is to qualify in the right order.

Start with the property

Before asking for a full borrower life story, get the basics on the collateral.

Ask questions like:

- What is the property type? Office, retail, industrial, mixed-use, multifamily, land, or special use all trigger different lender reactions.

- What is the purchase price or current value? The broker needs a rough baseline immediately.

- What condition is the property in? Deferred maintenance, vacancy, code issues, and unfinished work matter.

- What is the requested loan amount? If the financing sought is unrealistic, it's better to know now.

- What is the timing? A deal closing fast needs a lender that can perform under pressure.

If a borrower can't answer these clearly, the broker usually doesn't have a placement-ready deal yet.

Then test the borrower's capacity

Hard money is asset-driven, but weak sponsors still create risk. The broker should understand whether the borrower has experience, liquidity, and enough reserves to get through the business plan.

A useful supporting document in this stage is the borrower's debt schedule. It helps reveal whether the sponsor is overloaded, disorganized, or carrying obligations that could interfere with execution.

The exit strategy is not optional

At this point, many new brokers get lazy, and it costs them deals.

A common blind spot for new investors is what happens if the exit strategy fails. With rising commercial vacancy in 2024, brokers need to stress-test the borrower's plan because many hard money lenders offer limited grace periods before moving toward foreclosure if the property isn't sold or refinanced on time, as discussed by Agora Real on commercial hard money lending risks.

That means the broker should ask direct questions:

- If the sale takes longer, what changes?

- If the refinance doesn't get approved on schedule, what is the backup?

- Who is providing additional cash if the budget expands?

- What milestones must happen before payoff becomes realistic?

A weak exit strategy can sink an otherwise attractive asset. Hard money lenders know that, and brokers need to know it first.

A quick qualification screen

| Question | Why it matters |

|---|---|

| Is the collateral clear and understandable? | Lenders fund what they can evaluate quickly |

| Is the leverage request reasonable? | Overleveraged requests waste time |

| Does the borrower have a believable payoff plan? | Every hard money deal is temporary |

| Can the sponsor carry the project if timing slips? | Short-term loans leave little room for denial |

When brokers ask sharper questions up front, they don't just protect lenders. They protect clients from walking into a structure they can't survive.

Placing the Deal and Getting Paid

Qualifying the deal is only half the job. The broker still has to present it in a way that makes a lender want to issue terms.

Many beginners leave money on the table. They find a real borrower with a real need, then submit a sloppy package and blame the lender when the file stalls.

Build a clean lender package

A strong package makes the underwriter's job easier. It should tell the story fast and answer the obvious questions before anyone asks them.

That usually includes:

- A concise deal summary: Property, borrower, use of funds, timeline, and exit plan.

- Collateral documents: Purchase contract, rent roll if applicable, rehab scope if applicable, photos, and any available valuation material.

- Entity documents: Borrowing entity information and ownership details.

- Sponsor information: Experience summary, liquidity support, and relevant background.

- Closing needs: Title issues, timing pressure, and any special circumstances.

A broker's credibility rises when the package is organized. Lenders notice who submits financeable files and who sends chaos.

Match the file to the lender, not the other way around

Not every private lender likes every property type, borrower profile, or deal structure. One lender may like transitional retail. Another may avoid it. One may tolerate heavy rehab. Another may only want cleaner bridge scenarios.

That's why lender matching matters so much. A broker who understands appetite saves everyone time.

Market conditions also change lender behavior. In a volatile market, some private lenders moved from 70% LTV to 60% to 65% LTV in mid-2025 due to yield compression, according to Ignite Funding's discussion of hard money loan shifts. That single change affects how much cash the borrower needs, whether the deal still works, and which lenders are even realistic options.

Field note: When terms tighten, the broker who explains the shift clearly keeps the client. The broker who acts surprised loses trust.

Protect the closing and the commission

Once terms come in, the broker's role becomes part translator and part traffic manager. The borrower needs to understand what the lender is offering. The lender needs prompt responses and complete conditions. The title and closing process needs attention so the deal doesn't die in the final stretch.

A disciplined workflow helps:

- Review the term sheet carefully

- Confirm the borrower still agrees with the economics

- Collect closing conditions quickly

- Stay in contact with all parties

- Follow up after funding for the next opportunity

Broker compensation is paid when deals close, so the skill isn't just finding leads. The skill is moving a file from conversation to funded transaction without confusion, surprises, or broken communication.

This is one reason the niche works so well for home-based brokers. The core value isn't office space. It's process, lender relationships, and responsiveness.

Become the Go-To Broker for Fast Funding

A hard money commercial loan gives a broker access to a very specific kind of client need. It shows up when timing is tight, property condition is imperfect, borrowing capacity needs reassessment, or a borrower needs a bridge that conventional lenders won't provide.

That makes this niche practical for new brokers.

It doesn't require pretending every business owner is a fit. It requires learning how to recognize urgency, qualify collateral, pressure-test exits, package a file properly, and place it with the right lender. That skill set is valuable in any market because borrowers will always face deals that don't fit a bank's timeline or box.

There's also a business model advantage here. A broker can build this from home, work remotely, keep overhead low, and grow through referral relationships instead of relying on random one-off leads. Attorneys, CPAs, real estate professionals, investors, and business advisors all run into funding problems they can't solve alone. The broker who becomes known for fast, credible solutions can build a pipeline that compounds over time.

For aspiring entrepreneurs, consultants, sales professionals, bankers, and career changers, this is one of the more practical ways to enter financial services without creating a traditional office-bound career. The work is flexible, scalable, and tied to real client outcomes. That's what makes it durable.

The brokers who do best in this space don't try to sound clever. They get good at asking the right questions, explaining trade-offs transparently, and moving files efficiently.

Business Lending Blueprint shows aspiring brokers how to build a profitable, home-based business helping clients secure funding through alternative lenders. If the goal is to create flexible income, work remotely, and build recurring referral relationships in a recession-resistant niche, the next step is to watch the free training at Business Lending Blueprint or schedule a strategy session.