Mezzanine capital is a hybrid form of financing that blends debt and equity, sitting between senior bank debt and equity in a company's capital structure. It's commonly structured as subordinated debt or preferred equity, and because it takes more risk than senior debt, lenders often target returns in the 12% to 17% range, with some deals reaching 20% to 30% in faster, lightly collateralized situations.

A new broker usually runs into mezzanine capital definition searches at the same moment a deal stops fitting the bank box. The client has revenue, momentum, and a real use for funds, but the lender says no, or says yes to only part of the request.

That's where confusion starts. Most articles explain mezzanine capital like a finance textbook. They define the instrument, mention subordinated debt, and stop there. What they don't tell a broker is whether the average business owner in that pipeline is even a realistic fit.

That gap matters. A broker who understands mezzanine capital as a practical tool, not just a technical term, can save time, protect credibility, and move clients toward the right funding structure faster.

Table of Contents

- Your Client Has a Funding Gap What's Next

- The Official Mezzanine Capital Definition for Brokers

- Deconstructing the Deal Typical Terms and Structures

- Mezzanine Capital vs Senior Debt vs Equity

- When to Use Mezzanine Capital Real World Use Cases

- The Broker's Reality Check Sourcing Mezzanine Deals

- Become the Go-To Funding Expert in Your Market

Your Client Has a Funding Gap What's Next

A business owner wants to acquire a competitor, open another location, or buy out a partner. Cash flow looks solid. Management is competent. The expansion story makes sense. Then the bank declines the full request or offers an amount that leaves a hole in the capital stack.

That's a familiar moment for a broker. It's also where many newer brokers lose the deal by forcing a senior loan conversation when the client needs a layered solution.

Mezzanine capital exists for that gap. It isn't a first-stop product for every file, and it isn't a rescue tool for weak businesses. It's a specialty instrument used when a company is too strong to give up ownership cheaply, but not a clean fit for full conventional debt.

A broker who already understands repayment capacity through measures like debt service coverage ratio calculation will recognize why this matters. The borrower may be able to support a structured obligation, but not under the amortization and collateral rules a bank requires.

Practical rule: When a client has a real growth plan and the bank still leaves a funding gap, the next question isn't “Can this deal be forced into bank debt?” It's “What layer belongs between the bank and the owner's equity?”

That's the practical starting point for a usable mezzanine capital definition. It's not just a term from corporate finance. For a broker, it's a way to think about deals that are good businesses but imperfect bank loans.

The Official Mezzanine Capital Definition for Brokers

Most definitions are technically correct but operationally weak. The broker version needs to answer two questions fast. Where does mezzanine sit, and why does anyone use it?

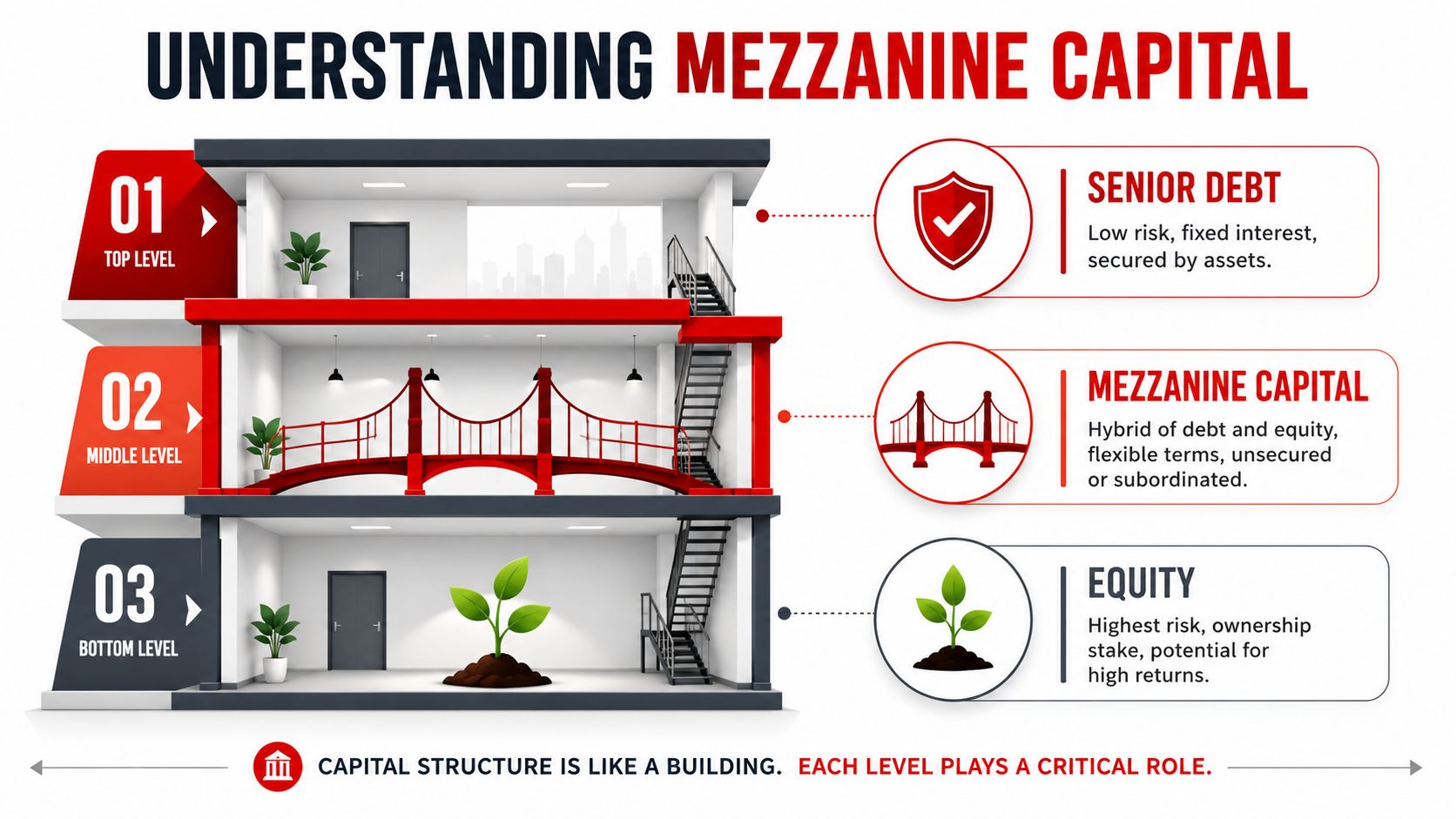

Mezzanine capital is a hybrid financing layer that sits between senior debt and equity in the capital structure. It's usually structured as subordinated debt or preferred equity, often with features like warrants or conversion rights that give the lender some upside participation while remaining below senior creditors and above common shareholders in repayment priority, as outlined in this overview of mezzanine capital.

Where mezzanine sits in the stack

The easiest way to teach the mezzanine capital definition is to borrow the building analogy. A mezzanine floor sits between main levels. In finance, mezzanine capital sits between the safer money above it and the riskier ownership below it.

A simple way to describe the stack in a client conversation:

- Senior debt is the cheapest money and usually has the strongest collateral protection.

- Mezzanine capital fills the space when senior debt won't cover the full need.

- Equity absorbs the most risk and gets paid last, but keeps the upside.

That middle position explains the name and the price. Because mezzanine is junior to bank lenders but senior to common equity, CAIA's discussion of mezzanine structures notes that mezzanine funds often target 12% to 17% total returns, with some lenders seeking 20% to 30% returns in faster, lightly collateralized deals.

For brokers who want another plain-English framing, Homebase's funding solutions offer a useful overview of how mezzanine is used to bridge a gap between senior financing and owner capital.

Why the pricing is higher

The lender isn't charging more because the structure is exotic. The lender is charging more because repayment priority is weaker and collateral is often limited.

That's why mezzanine behaves like debt in some ways and equity in others. The borrower usually makes contractual payments. The lender may also receive warrants, conversion rights, or preferred equity economics to compensate for risk.

A broker should never pitch mezzanine as “better than equity” or “better than debt.” It solves a specific structural problem and charges accordingly.

That distinction matters in client meetings. If the owner only hears “higher cost,” the deal sounds unattractive. If the owner understands that mezzanine can preserve control, avoid deeper dilution, and support a transaction senior debt alone can't fund, the economics become easier to evaluate.

Deconstructing the Deal Typical Terms and Structures

A broker doesn't need to draft documents to be effective, but that broker does need to translate the term sheet into plain business language. Owners rarely struggle with the concept of mezzanine. They struggle with the mechanics.

The first thing to understand is cost versus cash flow. According to the UN ESCWA reference on mezzanine capital, mezzanine capital is typically more expensive than senior debt, with target returns around 15%–20%. In exchange, it often carries interest-only or bullet maturity structures with terms up to 7–8 years and no amortization until maturity, which helps borrowers preserve operating cash flow.

What the borrower actually pays attention to

In practice, four features drive most conversations.

- Interest structure matters because it affects monthly pressure. A borrower may tolerate a higher overall cost if near-term payments are manageable.

- Equity kicker matters because it affects upside. Warrants or conversion features give the lender a way to participate if the business performs well.

- Subordination matters because it defines who gets paid first in a stress scenario.

- Covenants matter because they shape borrower behavior after closing.

Newer brokers often miss the trade-off. They focus on the stated rate and ignore amortization. For many borrowers, preserving cash during growth matters more than securing the lowest nominal price.

A client looking at expansion, acquisition, or recapitalization should be shown both sides of the equation. Higher pricing can still be workable if the structure reduces monthly drag while the business integrates a purchase, ramps production, or opens a new facility.

How brokers should read the structure

A practical review process helps. Before discussing a mezzanine proposal with a client, the broker should check:

- Cash burden now. Is the payment structure light enough to support the business plan?

- Refinance path later. If principal comes due at maturity, what's the likely exit?

- Control risk. Do warrants or conversion rights create future friction?

- Default consequences. What rights does the mezz lender gain if performance slips?

A strong broker also maps this against the client's full liability picture. That's why understanding a company's debt schedule and repayment obligations is essential before discussing subordinated capital.

For property-backed and mixed-use transactions, broader underwriting context also helps. A concise review of key metrics for CRE loan approval can sharpen how a broker thinks about the capital structure, debt coverage, and sponsor strength before mezzanine is introduced.

Advisor note: A mezzanine term sheet should be read backward from the exit. If the borrower can't explain how the balance gets taken out at maturity, the structure isn't ready.

That's what works in the field. Translate the legal language into business outcomes. Monthly payment. Ownership impact. Refinance risk. Control rights. Once those are clear, the client can make a rational decision.

Mezzanine Capital vs Senior Debt vs Equity

A borrower usually doesn't ask for mezzanine first. The borrower asks for capital. The broker's job is to compare the available layers clearly enough that the owner can see the trade-offs.

Senior debt is usually the least expensive option, but it tends to come with tighter collateral requirements, stronger lender protections, and less tolerance for imperfect deals. Equity gives the business the most payment flexibility, but the owner gives up part of the company and future upside. Mezzanine sits between those two choices.

For a borrower weighing a structured growth plan, this comparison often matters more than the formal mezzanine capital definition.

Funding options at a glance

| Feature | Senior Debt | Mezzanine Capital | Equity |

|---|---|---|---|

| Position in capital stack | Highest repayment priority | Below senior debt, above common equity | Last in repayment priority |

| Typical cost profile | Lower than mezzanine | Higher than senior debt | No contractual interest, but ownership dilution |

| Collateral expectation | Usually strongest | Often subordinated or unsecured | Ownership investment rather than loan collateral |

| Cash flow impact | Often tighter payment structure | Can be structured to preserve near-term cash flow | Usually light on required periodic payments |

| Control impact | Limited ownership dilution | May include warrants or conversion features | Direct dilution of ownership and control |

| Best fit | Stable, bankable deals | Funding gaps in larger strategic transactions | Businesses prioritizing flexibility over ownership retention |

A helpful way to frame this for clients is through strategy, not labels. Articles on funding business growth can be useful because they show why many companies don't rely on a single capital source.

How to position each option

Use senior debt when the deal is clean, collateral is strong, and the business can live with the lender's repayment structure.

Use equity when the owner values flexibility more than ownership retention, or when debt capacity is too limited to support the plan.

Use mezzanine when the company needs additional capital without going straight to a larger equity give-up, and when the business can support a higher-cost layer that may still be easier on near-term cash flow than a fully amortizing loan.

For smaller operating businesses, many files won't justify this middle layer at all. In those cases, a broker is often better served comparing standard products such as term loans versus lines of credit rather than forcing a capital-stack solution onto a simple working capital need.

When to Use Mezzanine Capital Real World Use Cases

Mezzanine doesn't belong in everyday funding conversations. It belongs in transactions where the company has a meaningful strategic objective and a clear reason senior debt alone won't do the job.

Situations where mezzanine fits

A common example is a management buyout. A leadership team wants to acquire ownership from a retiring founder. The bank may support part of the transaction, but not all of it. Equity may feel too dilutive or politically difficult. Mezzanine can fill that middle layer so the deal closes without forcing management to give away more of the company than necessary.

Another fit is growth and expansion capital. A manufacturer needs funds to add capacity after winning larger contracts. The business has operating momentum, but the expansion requires more capital than senior lenders are comfortable advancing. In that setup, mezzanine can support the growth plan while preserving cash for execution.

A third use case is acquisition financing. One company is buying another and expects the combined business to be stronger after integration. Senior debt may cover a base amount, but the full purchase price requires additional capital. Mezzanine can bridge the shortfall without immediately turning the transaction into a larger equity raise.

When the story supports the structure

The best mezzanine candidates usually share a few traits:

- Clear strategic use. The money funds an acquisition, buyout, recapitalization, or expansion with an identifiable business purpose.

- Credible repayment path. The borrower can explain how the mezzanine layer gets refinanced, repaid from earnings, or taken out through a later event.

- Operating strength. The company has enough stability that a subordinated lender can underwrite the story with confidence.

A broker should also look at alternatives before bringing mezzanine into the discussion. If the client's real issue is slow collections, uneven working capital, or receivables timing, a product tied to accounts receivable financing and lender fit may solve the problem more directly.

“Good mezzanine use cases are rarely emergency deals. They're usually deliberate transactions where the company needs one more capital layer to complete a smart move.”

That's the practical pattern to remember. Mezzanine works best when the business is doing something important, not when it's trying to survive the month.

The Broker's Reality Check Sourcing Mezzanine Deals

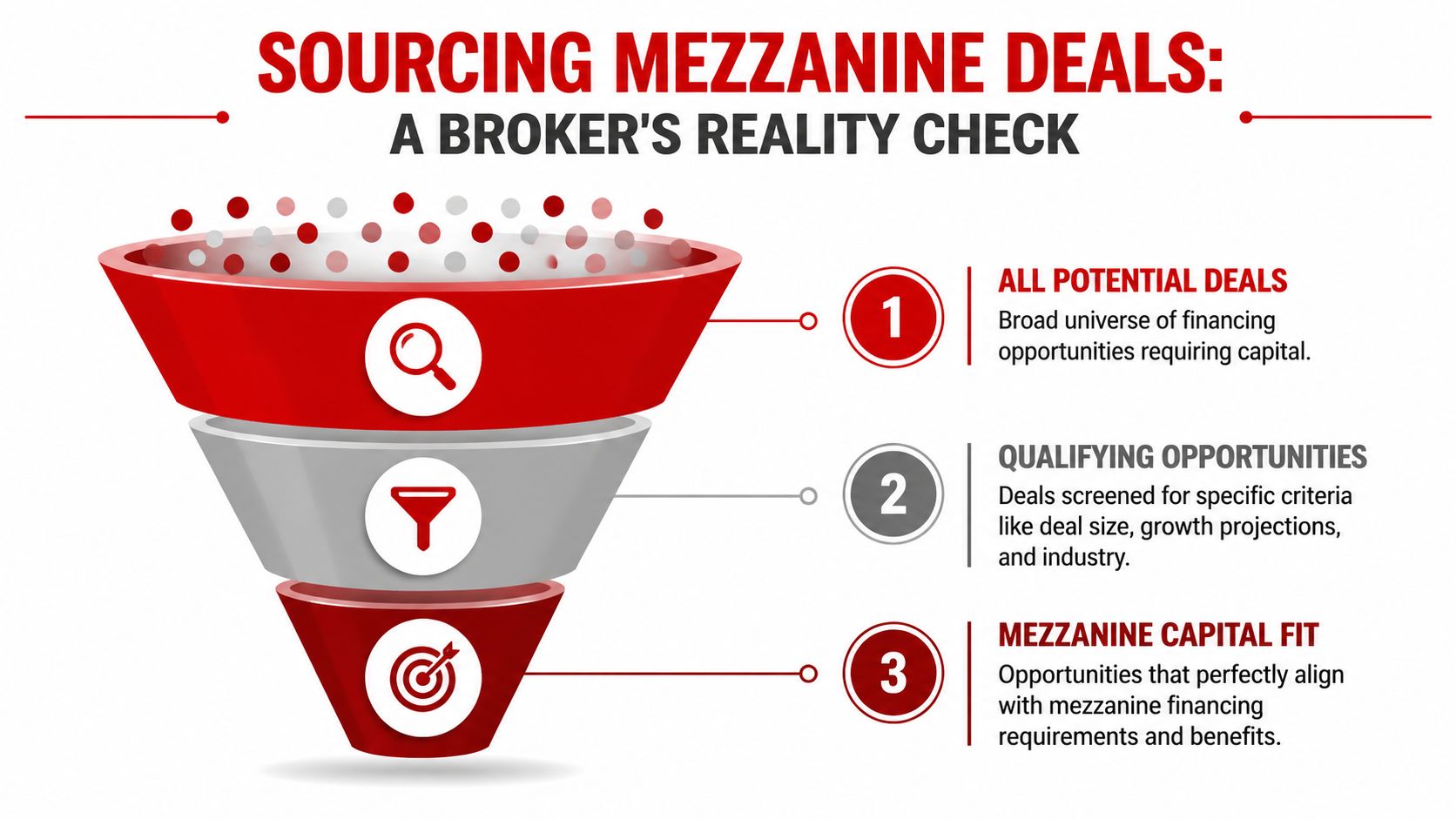

Many new brokers burn time. They learn the mezzanine capital definition, hear the word “flexible,” and assume it can be offered broadly to small business owners who didn't qualify for a bank loan.

That's not how the market works.

Why most broker leads won't qualify

Most definitions leave out the operational barrier. According to Prudential Private Capital's discussion of what mezzanine financing is, over 85% of small businesses are ineligible for traditional mezzanine products due to revenue thresholds, typically above $5M annual revenue.

That single fact changes how a broker should source deals. If the pipeline is filled with main street requests, startup asks, and modest working capital files, mezzanine usually isn't the answer. A broker who keeps pitching it anyway starts sounding uninformed.

A better qualification screen is simple:

- Transaction purpose. Is there a meaningful acquisition, recap, buyout, or expansion event?

- Business profile. Does the company look like a lower-middle-market or mid-market borrower rather than a small-ticket funding applicant?

- Capital stack need. Is there a gap between what senior debt will provide and what ownership wants to contribute?

Field reality: Mezzanine is a niche product. Treating it like a general small-business fallback usually leads to wasted calls, weak submissions, and frustrated clients.

What to do with the rest of the pipeline

The good news is that this reality makes a broker more valuable, not less. When a client isn't a mezzanine fit, the broker can pivot instead of stalling.

That means saying, in effect, “This isn't the right capital layer for your deal. Here's what is.”

For most smaller businesses, the right answer is usually a simpler structure. It may be a line of credit, a term product, receivables financing, equipment financing, or another non-mezzanine option that matches the business need more precisely.

That's how strong brokers build trust. They don't force every client into the most advanced-sounding product. They identify the rare deals that belong in a mezzanine conversation and move everything else toward a better-fit solution.

Become the Go-To Funding Expert in Your Market

A broker doesn't become valuable by memorizing definitions. Value comes from knowing when a product fits, when it doesn't, and how to redirect a client before time gets wasted.

That's the main point behind any serious mezzanine capital definition. It's a specialized layer of capital for the right company, the right transaction, and the right capital stack problem. It's not a universal solution for bank declines.

A broker who understands that difference stands out quickly. Business owners remember the advisor who explained the trade-offs clearly, protected their cash flow thinking, and recommended the right path instead of the flashy one.

That kind of judgment is what builds a durable brokerage. It also creates better referral relationships with owners, accountants, consultants, and other professionals who need a funding resource they can trust.

If this article clarified how mezzanine fits into the world of business funding, the next step is learning the full product map that successful brokers use every day. Watch the free training from Business Lending Blueprint to see how to build a remote, referral-driven loan brokerage, understand which funding products fit which clients, and turn that knowledge into a serious business.