A business owner says sales are strong. Bank statements show money coming in. The owner assumes funding should be easy, then gets declined or offered terms that don't match expectations. That gap confuses a lot of business owners, and it creates a real opportunity for anyone learning to become a business loan broker.

The reason is simple. Sales alone don't tell the full story, but they do tell an important one. A broker who understands what top line revenue is, which revenue counts, and how lenders interpret it can spot issues early, package deals better, and speak with far more authority than someone who only asks for statements and submits an application.

For aspiring brokers, this metric isn't just accounting vocabulary. It's one of the first filters that separates surface-level conversations from real financial analysis.

Table of Contents

- Why "Record Sales" Is Only Half the Story

- Defining Top Line Revenue The Right Way

- Top Line vs Bottom Line A Deeper Look

- What Lenders See That Others Miss in Revenue

- How to Grow Top Line Revenue and Secure Funding

- Your Path to Becoming a Business Finance Professional

Why "Record Sales" Is Only Half the Story

A contractor lands several large jobs in a short stretch. Revenue looks impressive on the surface. The owner feels confident walking into a bank because the business is busier than ever.

Then the financing conversation starts. The underwriter asks where the revenue came from, whether it repeats, how much was discounted, whether there were refunds, and how much cash the business retained after expenses. Suddenly, “record sales” stops sounding like a complete answer.

That's where many newer advisors get exposed. They hear strong sales and assume the business is healthy, fundable, and easy to place. Experienced brokers know better. They know sales can be real and still not be reliable enough to support the type of financing the owner wants.

Practical rule: A lender doesn't just want proof that money came in. A lender wants to understand how that money was generated, how often it shows up, and whether the pattern is likely to continue.

It's important to note that business owners often use sales, income, profit, and revenue as if they all mean the same thing. They don't. A broker who can separate those terms quickly becomes more useful in the first conversation.

The real issue behind the decline

In many deals, the business owner isn't lying and the bank isn't being irrational. They're just looking at different things.

- The owner sees momentum. More invoices, more customers, more deposits.

- The lender sees uncertainty. One-time jobs, uneven timing, margin pressure, or a weak cash cushion.

- The broker sees the bridge. A way to explain the numbers properly and match the deal to the right funding structure.

That bridge starts with one basic concept. Top line revenue tells a broker what the business is producing before costs enter the picture. It's not the whole analysis, but it is the first lens.

For aspiring loan brokers, understanding that lens is one of the fastest ways to sound credible. It changes the conversation from “How much did you make?” to “What kind of revenue is this, and how will a lender view it?”

Defining Top Line Revenue The Right Way

Top line revenue is the total sales or gross revenue a business generates before any deductions, and it appears as the first figure on an income statement. For a product business, a simple calculation is units sold × price per unit. For a service business, it can be calculated as customers × average service price, as explained in Ramp's overview of top line growth and revenue basics.

A useful way to think about it is a harvest. A farm can bring in a full harvest before paying for labor, equipment, transport, or storage. The harvest shows output. It doesn't show what was kept.

What the term actually means

A lot of confusion stems from this point. Business owners often hear “revenue” and think “profit.” That's a mistake, especially in lending.

Top line revenue answers a narrow question. How much did the business bring in before subtracting costs, taxes, and other expenses? It doesn't answer whether the business was efficient, well-managed, or highly profitable.

A simple interpretation looks like this:

| Business type | Basic top line formula | What it captures |

|---|---|---|

| Product business | Units sold × price per unit | Gross sales from goods sold |

| Service business | Customers × average service price | Gross revenue from services delivered |

For readers who want a stronger grasp of how revenue flows through financial statements, this guide to mastering business finances offers helpful context on reading profit and loss reports.

Why the first line matters

The phrase “top line” comes from placement. It sits at the top of the income statement for a reason. It's the starting point for almost every financial discussion that follows.

Strong top-line revenue can indicate demand and selling ability. It does not, by itself, prove the business is financially strong.

That distinction matters in funding. A broker reviewing a file needs to know whether the business has enough sales activity to support a financing request. But the broker also needs to know that this number is only the opening line, not the verdict.

When someone asks what is top line revenue, the right answer isn't just “sales before expenses.” The right answer is “the gross inflow a business creates before deductions, and the first figure a lender uses to start evaluating the deal.”

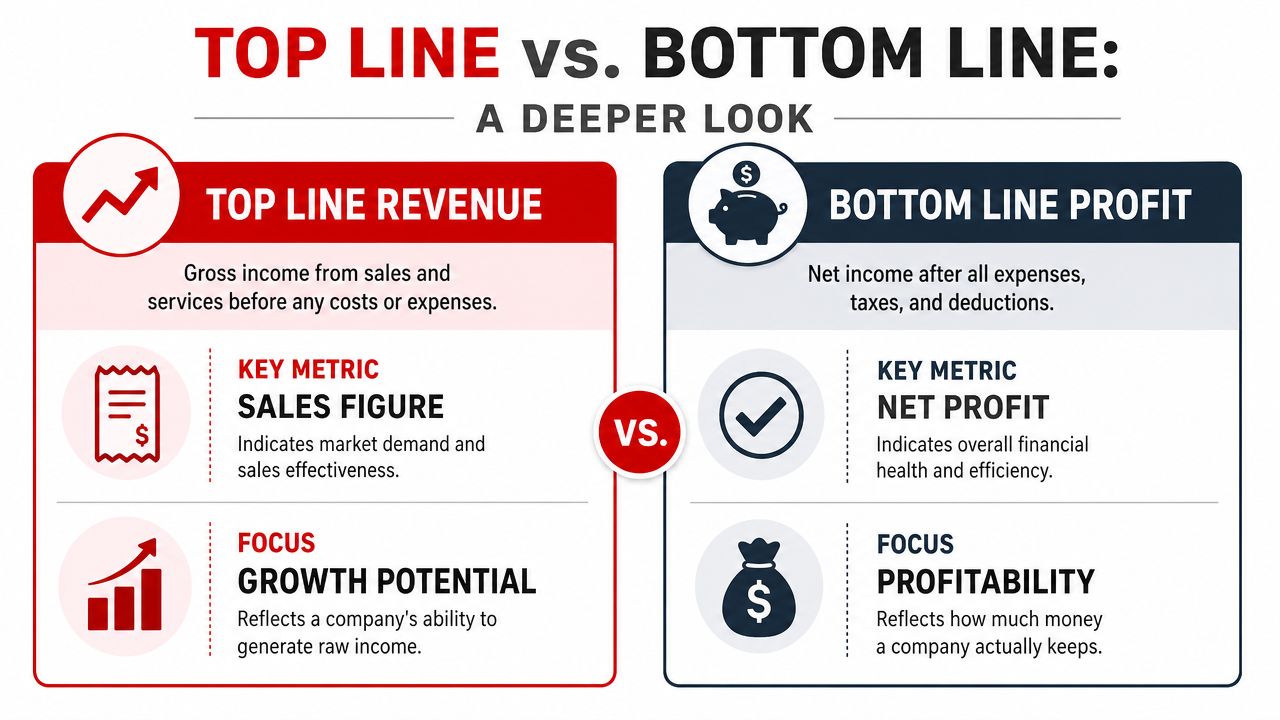

Top Line vs Bottom Line A Deeper Look

A business can produce healthy sales and still struggle financially. That's the core difference between the top line and the bottom line.

The top line shows sales activity. The bottom line shows what remains after costs, taxes, and other expenses have been removed. Those are two different stories. One speaks to market demand and revenue generation. The other speaks to profit.

A simple business example

Take a local café. Its sales look strong because the register stays busy, catering orders come in, and weekend traffic is solid. On the surface, the business appears fundable because the top line is active.

But then the owner's expense structure comes into view.

- Occupancy costs can absorb a large share of monthly inflow.

- Payroll may stay high because service businesses need coverage every day.

- Inventory and waste can erode profit, especially when pricing hasn't kept pace.

- Debt payments and taxes can squeeze whatever remains.

The result is common. The café has enough demand to generate visible sales, but not enough operating discipline to retain much profit. A traditional lender may hesitate. An alternative lender may still look at the file, but the structure and pricing will reflect the risk.

Why brokers need both views

Many new brokers improve quickly when they stop treating revenue as the answer and start treating it as the start of underwriting.

A useful comparison looks like this:

| Metric | What it tells a broker | What it does not tell a broker |

|---|---|---|

| Top line revenue | Whether the business is generating gross sales | Whether the business keeps enough of that revenue |

| Bottom line profit | Whether operations leave money after expenses | Whether the business has broad market demand |

A broker who only studies revenue can overestimate deal quality. A broker who only studies profit can miss growth potential.

A lender wants context around both. Revenue may support the narrative that demand exists. Profit and cash flow help support the narrative that repayment is realistic. That's also why ratios matter in credit analysis. Readers who want to connect sales performance to repayment strength should review this explanation of debt service coverage ratio calculation.

For practical deal structuring, the lesson is straightforward. Top line opens the conversation. Bottom line and cash flow determine how strong that conversation really is.

What Lenders See That Others Miss in Revenue

The textbook definition of top line revenue is useful, but it's incomplete for real lending work. One of the biggest gaps in common explanations is that they stop at gross sales and never address which revenue counts when a business has multiple streams, returns, discounts, refunds, add-ons, or non-core income. TGG Accounting highlights that problem in its discussion of top line versus bottom line.

That issue matters because lenders don't treat every dollar of revenue the same way.

Not all revenue carries the same weight

A lender wants to know whether revenue is stable, core to the business, and likely to continue. That's very different from merely checking whether deposits exist.

For example, these revenue types often create different reactions in underwriting:

- Recurring revenue tends to read better because it's tied to repeat behavior, contracts, subscriptions, maintenance plans, or ongoing client relationships.

- One-time project revenue can still be valuable, but it usually needs explanation. If the work is large and irregular, lenders may question predictability.

- Add-on and ancillary revenue may count, but underwriters often want to know whether it's core to operations or occasional.

- Refunds, returns, and discount-heavy sales can distort the headline number. Gross sales might look strong while realized revenue quality is weaker.

- Non-core income raises a flag when it inflates the picture without reflecting the company's normal operating engine.

A helpful outside perspective on this broader review process appears in Stewart Accounting's article on what banks examine during a small business loan application.

How a broker can pre-underwrite revenue

A good broker can clean up confusion before the file reaches a lender. That alone improves credibility.

The review should include questions like these:

- Where does most revenue come from? One product line, several services, subscriptions, seasonal contracts, or a few large customers.

- Is the revenue repeatable? Repeatable revenue usually creates a stronger funding narrative than sporadic spikes.

- What gets reversed or discounted? Refunds and concessions can change how healthy the top line really is.

- Is any revenue non-operating? If so, it shouldn't carry the same weight as core business activity.

Revenue quality often matters as much as revenue size.

This is also where document review becomes practical. A broker who compares statements, receivables, and obligations can identify whether reported sales are translating into usable cash. That's why understanding a client's liabilities matters alongside revenue review. This overview of what is a debt schedule fits naturally into that analysis.

A broker who learns to think this way stops acting like a lead generator and starts acting like a financial professional. That shift is where long-term referral relationships usually begin.

How to Grow Top Line Revenue and Secure Funding

Business owners don't need vague advice about “getting more sales.” They need growth moves that are visible in financials and understandable to lenders. The best brokers help clients connect revenue growth plans to a funding strategy.

That's where brokering becomes valuable. A business owner may know the goal, but not how to finance the inventory build, marketing push, hiring plan, or receivables gap required to get there.

Growth moves that lenders can understand

Some revenue growth strategies are easier to support with financing because the use of funds is clear.

- Expand into a new market. A business may need capital for inventory, staff, or outreach before new sales arrive.

- Adjust pricing carefully. If the company has strong demand but weak margins, a pricing review can improve revenue quality without changing the core model.

- Bundle products or services. Bundling can raise average ticket size and make customer value easier to defend.

- Strengthen retention. Repeat customers often produce cleaner revenue patterns than constant new-customer chasing.

- Tighten the sales process. Better follow-up, clearer offers, and stronger collections can improve the top line without major operational changes.

Funding works best when the use of proceeds connects directly to a believable revenue plan.

How brokers turn growth plans into fundable requests

A broker's job isn't just to ask what the client wants. It's to translate the request into lender language.

If a business wants to grow revenue, the broker should ask:

| Growth objective | Likely funding need | Broker angle |

|---|---|---|

| Enter a new territory | Working capital | Show how capital supports expansion activity |

| Carry more inventory | Short-term or revolving capital | Tie inventory timing to expected sales cycles |

| Improve collections | Receivables-based financing | Match financing to outstanding invoices |

| Add marketing capacity | Growth capital | Explain how spend supports customer acquisition |

Niche knowledge proves valuable. If a client is waiting on customer payments while trying to grow, a broker may need to understand options tied to invoices and payment timing. This resource on accounts receivable lenders is one example of how funding structure can align with revenue strategy.

In practice, the broker who wins trust is usually the one who can say, “Here's how the business can improve top-line performance, and here's the funding structure that supports that plan.”

Your Path to Becoming a Business Finance Professional

Knowing what top line revenue is won't make someone a skilled broker by itself. But it does mark the shift from casual sales talk to real financial thinking.

A strong broker understands how revenue is generated, what kind of revenue lenders trust, how expenses change the story, and how funding can support growth without ignoring risk. That knowledge makes conversations sharper. It also makes referrals more likely, because business owners remember advisors who explain the numbers clearly.

The opportunity in learning the language of lending

This field fits people who want a home-based business built around analysis, communication, and relationship-driven work. It also fits professionals who already serve business owners and want to add a funding capability without becoming a banker.

For those who want structured training, lender access, and a system for packaging deals, becoming a business loan broker is the next practical step to explore. Business Lending Blueprint is one training option that teaches people how to build a brokerage around business funding, remote operations, and referral-based client acquisition.

The broker who understands financial fundamentals creates more value than the broker who only forwards applications.

That's the takeaway. Learning metrics like top line revenue gives a person better judgment, better conversations, and a better chance of building a serious business around helping owners secure capital.

If this article clarified how lenders really look at revenue, the next step is simple. Watch the free training from Business Lending Blueprint to see how a business loan brokerage works, how deals are structured, and how to build a remote, referral-driven funding business with practical guidance.