A lot of new brokers are closer to this niche than they realize. They already know a CPA who serves physicians, an office realtor who handles medical space, a payroll contact with dental clients, or a consultant who hears the same sentence every month: “The practice is growing, but financing is the bottleneck.”

That's where many people miss a real business opportunity. They hear “doctor” and assume the deal belongs with a bank branch, a private banker, or a specialty lender. In practice, many healthcare borrowers still need someone who can identify the right product, pre-qualify the file, package it cleanly, and move it to a lender that understands the deal.

For an aspiring broker building a home-based business, medical practice loans are one of the most practical niches to learn. The clients are serious, the use cases are easy to understand, and the referral paths are strong once one funded deal turns into introductions to partners, specialists, accountants, and vendors.

Table of Contents

- The Untapped Goldmine in Your Network

- Understanding the Medical Practice Loan Landscape

- Your Broker Toolkit of Medical Financing Products

- Decoding Underwriting What Lenders Really Want

- How to Package and Place Deals Like a Pro

- Case Studies From Consultation to Commission

- Become the Go-To Funding Expert for Healthcare Professionals

The Untapped Goldmine in Your Network

A broker can lose a strong deal before it even starts. A physician mentions plans to expand, buy equipment, or bring in a partner. The broker nods, says they'll “look into options,” then never builds the confidence to guide the transaction. That usually doesn't happen because the borrower is unqualified. It happens because the broker doesn't yet understand the niche.

Why this niche pays attention to prepared brokers

Medical borrowers aren't casual shoppers. They usually come to the table with a defined purpose, a license, an established service model, and a clear reason for needing capital. That makes the conversation cleaner than many general small business deals.

Medical practice financing is also recognized as a specialized category with features such as longer repayment terms and lower down payment requirements than many other business loan types, and it supports a broad range of providers including doctors, dentists, chiropractors, and psychologists, as outlined in this overview of medical practice financing. For a broker, that matters because specialization creates room for advisory value.

Practical rule: The broker who can explain the difference between a cash flow request, an equipment request, and an acquisition request wins trust faster than the broker who just asks, “How much do you need?”

The opportunity isn't limited to one traffic source either. A broker can build this niche through professional referrals, targeted outreach, local networking, and simple authority-based content. For anyone building prospect flow, these top lead generation strategies are useful because they map well to professional-service niches where trust matters before speed.

Where brokers usually find the first deal

The first medical file rarely comes from a mass ad campaign. It often comes from an adjacent professional who already has the relationship.

A practical referral map looks like this:

- CPAs and tax preparers: They see expansion plans before lenders do.

- Medical office landlords and brokers: They hear about relocations, buildouts, and new lease deposits early.

- Vendors serving practices: Equipment reps, billing consultants, and software advisors hear when capital is holding up a purchase.

- General business owners in healthcare circles: One introduction inside a practice can lead to multiple specialists and partners.

A newer broker who wants more targeted conversations can also sharpen prospecting by studying how others source working capital leads for business funding conversations. The same principles transfer well when the borrower happens to wear a white coat.

Understanding the Medical Practice Loan Landscape

Medical practice loans aren't just “business loans for doctors.” A broker who treats them that way usually misses both the best-fit product and the best-fit borrower. The stronger approach is to look at the reason for the capital and the stage of the practice.

What makes this category different

Healthcare financing works on a different rhythm from many retail or service businesses. Revenue may be strong, but timing can be uneven. Growth can require expensive equipment, specialized space, staffing, software, and compliance-related overhead before the return shows up fully.

That's why brokers need to think in use cases, not generic categories. Common requests include practice acquisition, expansion, office buildouts, working capital, equipment purchases, partnership buy-ins, and short-term liquidity support. A lender reviewing a medical borrower also pays close attention to industry experience, licensing, stable income patterns, and the borrower's ability to operate in a regulated environment.

The underserved angle most brokers ignore

One of the most useful openings in this niche is the borrower who isn't fully “bank-ready” yet. Existing content often emphasizes that medical practice loans offer 100% financing and a standard 680+ FICO expectation, but it usually skips the funding gap for early-career physicians still in residency or with less than one year of practice history, even though SBA 7(a) loans typically require at least one year of business operation, as noted in this discussion of medical practice loans for physicians.

That gap creates a real broker role. A new physician may need capital for lease deposits, startup equipment, or setup costs before the practice has enough operating history for certain programs. Many guides aimed at doctors don't address that transition period well. A broker can.

The niche opens up when the broker stops asking, “Who already qualifies?” and starts asking, “Who has a financeable path with the right structure?”

How to spot the opportunity early

A clean way to classify a healthcare lead is by timing:

| Borrower stage | What they usually need | Broker angle |

|---|---|---|

| Pre-launch | Deposit money, equipment, startup positioning | Set expectations and identify nontraditional paths |

| Early operation | Working capital, stabilization, small upgrades | Focus on documentation and lender fit |

| Established practice | Expansion, acquisition, partner buy-in | Package a stronger story around growth and repayment |

| Mature operator | Real estate, large equipment, strategic restructuring | Match long-term assets to longer-term financing |

Cash flow support often shows up in this niche because reimbursement timing can create friction even in healthy practices. That's one reason operational partners who help boost healthcare cash flow can become valuable referral allies for a broker. They see pressure points before a loan inquiry ever reaches a lender.

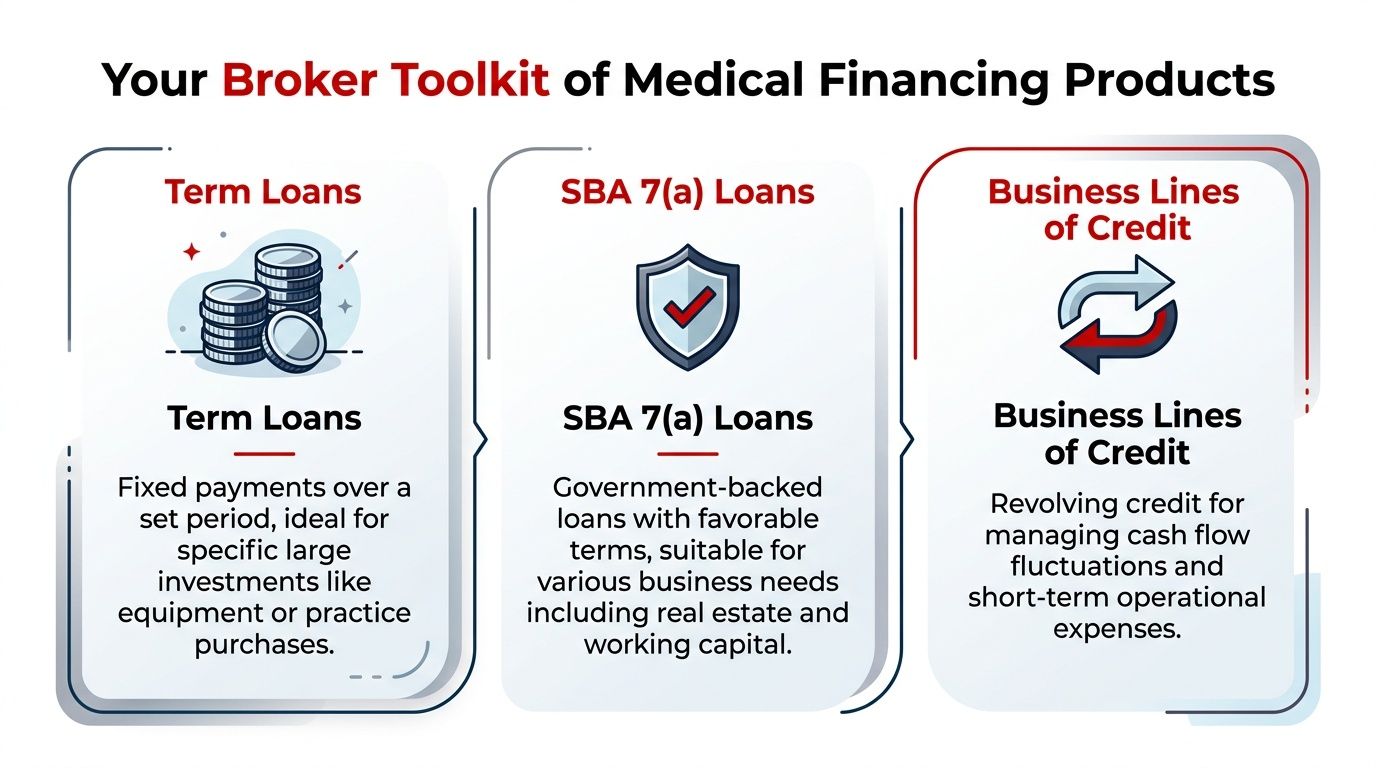

Your Broker Toolkit of Medical Financing Products

A broker doesn't need dozens of products to serve this niche well. A few well-understood options will cover most real conversations. The key is knowing which request belongs with which structure.

The three core products every broker should know

A practical way to think about medical practice loans is this:

| Product | Best use | Main advantage | Main caution |

|---|---|---|---|

| Term loan | One-time investment | Predictable repayment | Wrong term can squeeze cash flow |

| SBA 7(a) loan | Larger strategic needs | Lower down payment and longer runway | More documentation and tighter fit requirements |

| Business line of credit | Short-term operating gaps | Flexibility, borrow as needed | Not ideal for long-lived assets |

The broad category can include financing amounts up to $500,000 with repayment terms extending as long as 12 years, allowing providers to acquire or expand practices without mandatory down payments or collateral pledges in some cases. SBA 7(a) loans are also popular here and may require a down payment of only 10%, according to this medical practice loan overview.

When to use each one

Term loans

Term loans are often the cleanest fit for a defined project. Think software upgrades, office expansion, or a partnership buy-in. They remain a common option for major one-time investments, with typical terms ranging from 1 to 5 years in this category, as described in this guide to medical practice loans.

For the borrower, the upside is clarity. For the broker, term loans are straightforward to explain and package because the use of proceeds is specific.

SBA 7(a) loans

SBA 7(a) loans work well when the borrower needs a more flexible structure for a larger business objective. That can include acquisition, expansion, working capital, or owner-occupied real estate in the right scenario.

This product often appeals to medical borrowers because the government-backed structure can provide lower rates and extended repayment terms, but the file usually demands stronger documentation. Brokers who do well here don't oversell speed. They sell fit.

Business lines of credit

Lines of credit solve a different problem. They aren't built for a major permanent purchase. They're built for uneven timing. In this niche, that can mean short-term cash flow gaps, recurring costs, or unexpected operating needs. The borrower only pays interest on the amount used, which makes the product easier to position when the need is temporary rather than fixed.

Equipment financing deserves separate treatment

Equipment requests look simple from the outside, but structure matters. These loans are often aligned to the useful life of the asset, with term loans typically spanning 1 to 5 years for equipment and longer periods available for acquisitions and real estate in certain situations, as detailed in this lender-focused breakdown of medical financing structures.

A broker adds value when the financing term matches the life of the asset. That keeps the doctor from making payments on equipment long after the equipment has stopped helping the practice produce revenue.

That point helps close deals. It also helps build referral trust because the broker sounds like an advisor, not an order taker.

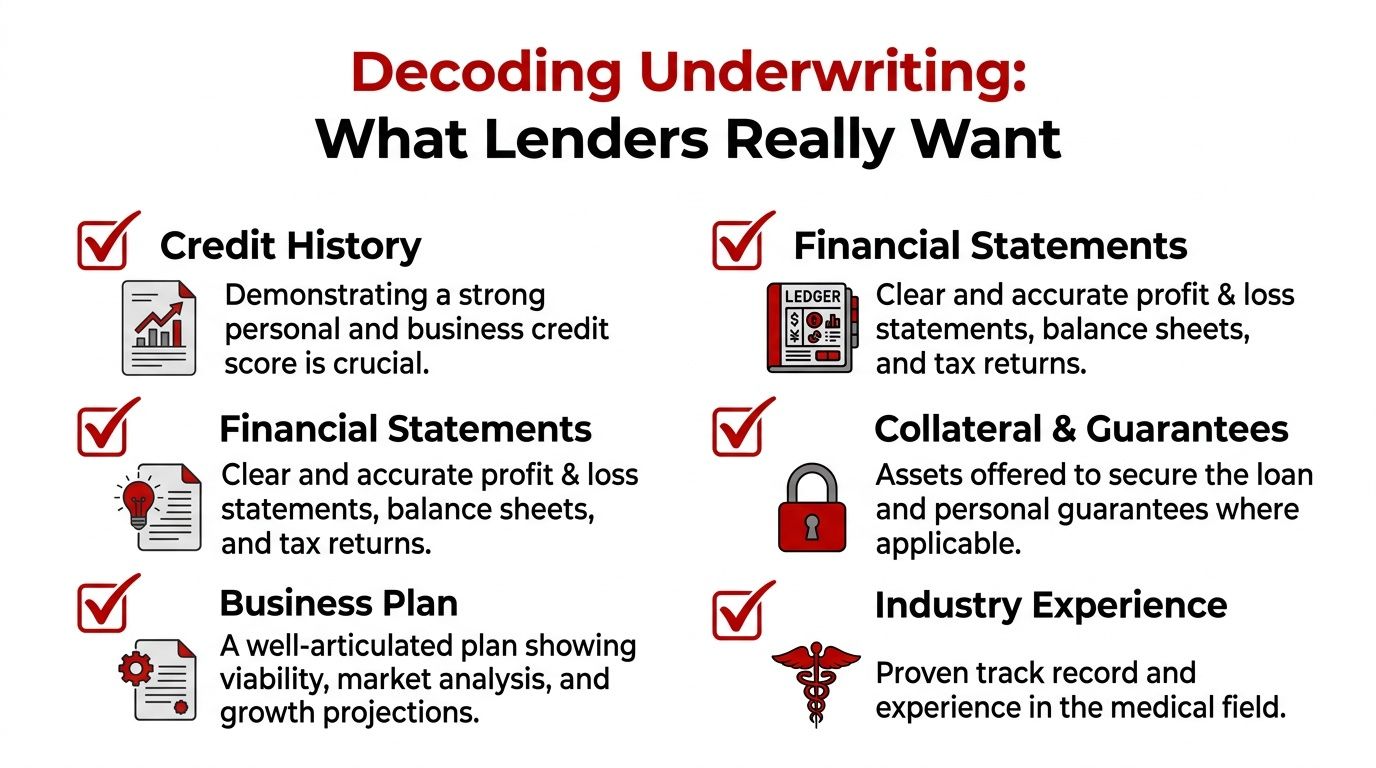

Decoding Underwriting What Lenders Really Want

A broker who understands underwriting can reject weak files before the lender does. That saves time, protects lender relationships, and makes the broker look far more experienced than their years in the business might suggest.

The baseline numbers matter, but they aren't the whole story

For medical practice financing, lenders often want the practice to generate at least $40,000 in monthly revenue (about $480,000 annually) and the borrower to maintain a personal FICO score of 625 or higher, with many stronger lenders looking for 660 or above, according to this underwriting snapshot for medical practice financing.

Those numbers are useful because they create a fast screen. They aren't useful if the broker stops there.

What lenders are really testing

Lenders are trying to answer a handful of questions:

- Can the practice carry debt after fixed overhead? Medical offices usually carry meaningful payroll, rent, insurance, and administrative costs.

- Is income stable enough to support repayment? Consistent patient volume and insurer relationships matter.

- Does the borrower run a disciplined business? Personal credit often serves as a proxy for how carefully the owner manages obligations.

- Has the practice moved beyond the volatile startup phase? For some products, time in business is a major filter.

A line of credit application may also require the entity to be in business for at least two years in some cases, which gives the lender more confidence that the operation has stabilized. That's one reason a broker needs to ask better questions before collecting paperwork.

Field note: Underwriters don't just read numbers. They read patterns. Erratic deposits, weak explanations, and unrealistic projections create friction even when a borrower hits the minimums.

How a broker should pre-screen a file

Use a practical checklist before submission:

- Review credit first. If the personal profile is below the likely lender range, the broker should reset expectations immediately.

- Study the financials for consistency. Clean statements matter. This short guide on preparing financial statements is a helpful reference when a borrower's package is sloppy.

- Check debt capacity, not just revenue. A borrower can have solid gross revenue and still be too tight after expenses. A broker who understands debt service coverage ratio calculation will screen deals far better.

- Read the story behind the numbers. A temporary dip can be explainable. Ongoing instability usually isn't.

- Confirm licenses, experience, and business purpose. Lenders want confidence that the borrower can execute.

The broker's edge comes from doing lender thinking before lender submission.

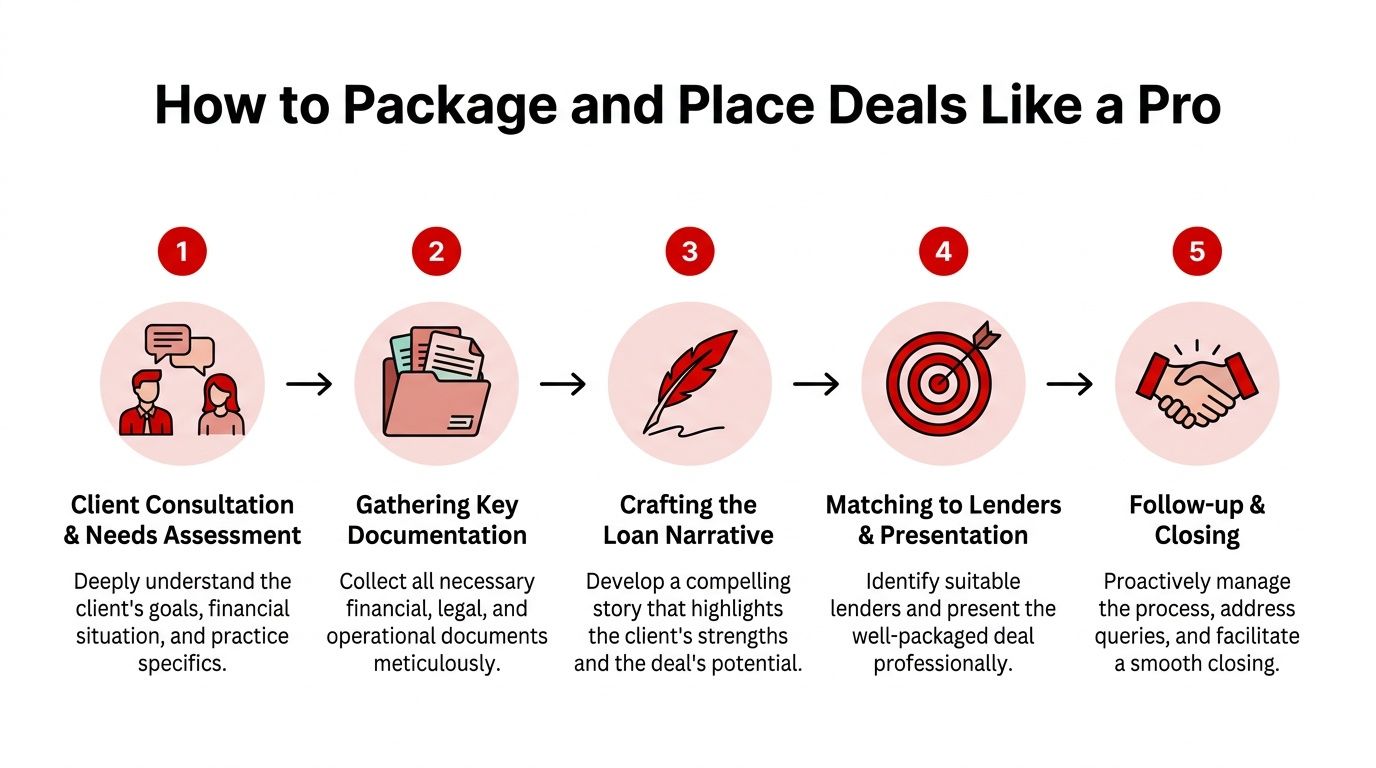

How to Package and Place Deals Like a Pro

A medical practice file doesn't get approved because the borrower is impressive. It gets approved because the broker turns the file into a coherent lending story. That's packaging.

Start with the business reason, not the loan request

When a physician says, “Need capital,” that isn't enough. The broker needs to know what the money is supposed to accomplish, how fast the need is developing, and what repayment will depend on.

A strong discovery call usually answers these questions:

- What's being funded? Equipment, expansion, buy-in, acquisition, or short-term operating need.

- Why now? The timeline reveals urgency and product fit.

- What will the capital change? More capacity, stronger margins, smoother operations, or a transition in ownership.

- What could block approval? Credit, time in business, thin liquidity, or weak documentation.

Gather documents with a purpose

Too many brokers collect paperwork like a checklist and dump it into underwriting. Good packaging is selective and intentional. Every document should support a point.

A clean package often includes financial statements, tax returns, bank statements, licensing information, ownership details, lease or purchase information when relevant, and a business plan when the deal depends on future performance. If the practice has meaningful overhead, the broker should also understand expense structure. This primer on how to calculate overhead cost helps newer brokers interpret what they're seeing instead of just forwarding reports.

Write the narrative lenders need

The cover summary is where many deals are won or weakened. The broker should explain the request in plain language, address obvious questions before the lender asks them, and highlight the strengths that support repayment.

A simple narrative framework works well:

| Narrative element | What to include |

|---|---|

| Borrower profile | Specialty, experience, ownership structure |

| Loan purpose | Exact use of proceeds and why it matters |

| Repayment logic | How the practice supports or will support debt |

| Risk explanation | Any issue that needs context |

| Strength factors | Stability, licensing, history, contracts, growth plan |

The best submission memo sounds like a credit analyst wrote it after meeting the borrower, not like a salesperson copied notes from an intake form.

Match the file to the right lender lane

Not every lender likes startup-adjacent healthcare files. Not every lender likes acquisition deals. Not every lender wants to finance specialized equipment. Placement matters as much as packaging.

A disciplined broker asks:

- Does this lender like the borrower's stage?

- Does the lender support this use of proceeds?

- Will this lender tolerate any weakness in the file if the overall story is strong?

- Is the timeline realistic for this credit box?

Manage the close professionally

Once the package is out, the broker's work shifts to coordination. That means answering conditions quickly, keeping the borrower calm, clarifying any underwriting questions, and preventing the file from going stale.

Here, referral relationships are built. A physician remembers the broker who made a complex process feel organized. So does the lender.

Case Studies From Consultation to Commission

Theory matters, but stories close the loop. Medical practice loans become much easier to sell when a broker can recognize the pattern inside a real borrower conversation.

Case one, the dentist with a defined expansion plan

A dentist wanted financing for an office improvement project tied to additional production capacity. The first conversation sounded simple, but the file had a common problem: the borrower focused on the project details, not on the repayment story.

The broker reframed the request around business function. Why the space changes mattered, how the practice expected to use the upgraded space, and what operational stability already existed. That changed the file from “doctor wants capital” to “established operator funding a practical growth move.”

What worked:

- Clear use of proceeds: The request was specific.

- Strong documentation: Financials supported stability.

- Tight narrative: The broker explained the business reason, not just the construction details.

What didn't work at first:

- Too much borrower jargon: Clinical language doesn't help underwriting.

- No summary memo: Without context, the lender had to guess.

Case two, the chiropractor with an equipment purchase

This borrower needed financing for equipment expected to support service delivery and operational capacity. The mistake many new brokers make here is treating equipment like generic working capital.

A better structure tied the financing to the useful life of the asset and kept the loan purpose clean. The package highlighted why the equipment mattered to the practice, how it fit current operations, and why the request wasn't speculative.

When a broker can explain why an asset should be financed on terms that make sense for that asset, the conversation gets easier for both the lender and the borrower.

This kind of deal also helps build referral momentum. Equipment vendors, office consultants, and even practice managers often know who is planning the next purchase before the doctor starts shopping for financing.

Case three, the commission math that makes the niche tangible

The broker side of this business needs to stay practical. Compensation is usually deal-driven. Brokers often get paid in points, where one point equals 1% of the loan amount, and a $150,000 funded loan at 3 points yields $4,500, with payment issued when the deal funds, as explained in this broker commission example.

That example matters because it strips away hype. The business isn't about vague “high ticket” language. It's about learning to source, pre-qualify, package, and close financeable transactions.

A few practical takeaways from these scenarios:

- Defined purpose closes faster: Lenders respond better when the request is tied to a specific outcome.

- Narrative creates value: Packaging is where the broker earns trust.

- Healthcare referrals compound: One funded deal can lead to partners, office managers, accountants, and specialists in the same network.

- Commission follows execution: A broker doesn't get paid for enthusiasm. The deal has to fund.

Become the Go-To Funding Expert for Healthcare Professionals

This niche is attractive because it rewards competence more than noise. A broker doesn't need to become a clinician, a banker, or a healthcare consultant. The broker needs to understand how to identify the need, match the structure, pre-screen the file, and package the story in a way lenders can approve.

That's why medical practice loans fit so well inside a home-based brokerage model. The work is advisory, repeatable, and relationship-driven. The borrowers tend to have real business purposes. The referral partners tend to be professionals. And the broker who handles one file well often earns trust beyond a single transaction.

What separates average brokers from trusted specialists

The average broker reacts to inquiries. The stronger broker builds a lane.

That lane includes:

- A referral network: CPAs, landlords, consultants, and vendors serving healthcare operators.

- A product framework: Knowing when to use term loans, lines of credit, SBA options, or equipment financing.

- An underwriting mindset: Screening for quality before submission.

- A packaging system: Turning scattered documents into a lender-ready deal.

The fastest way to stand out in a crowded brokerage market is to become easy to refer. Healthcare professionals refer the broker who understands their world and doesn't waste their time.

This is also a learnable business. Someone coming from sales, consulting, banking, real estate, tax, insurance, or even a completely different field can build a serious operation here by mastering process and staying consistent. That's one reason the business loan broker model continues to appeal to people who want remote work, flexible schedules, recurring referral relationships, and a recession-resistant service.

The opportunity in medical practice loans isn't hidden. It's just under-served by brokers who haven't learned how to speak to the niche. The ones who do become valuable quickly.

Business Lending Blueprint shows aspiring brokers how to build a profitable, home-based business by helping companies secure funding across products like term loans, lines of credit, equipment financing, and more. For readers who want a practical, referral-driven path into this industry without hype, the next step is to watch the free training or schedule a strategy session at Business Lending Blueprint.