A lot of people who look into business lending are in the same spot. They want a business they can run from home, they want more control over their schedule, and they want work that still matters when the economy gets tight. They don't want a hype-driven sales job. They want a real service business with repeat demand.

Working capital leads sit in the middle of that opportunity. They connect everyday business owners with funding for payroll, inventory, vendor payments, repairs, and the short-term gaps that keep operations moving. For an aspiring broker, that makes lead generation the foundation of the business. If the lead flow is weak, everything feels random. If the lead flow is steady and well-qualified, the business becomes far more predictable.

Table of Contents

- The Hidden Market for Funding and How You Can Tap Into It

- Building Your Lead Generation Engine Without Cold Calling

- Qualifying Leads to Focus on Winnable Deals

- The Consultant's Approach to Converting Leads

- Automating Your Brokerage for Scalable Growth

- Your Path to Becoming a Six-Figure Funding Advisor

The Hidden Market for Funding and How You Can Tap Into It

The strongest reason to build a funding brokerage from home is simple. Businesses need cash before they need another sales pitch.

That need isn't small. S&P 1500 companies have trapped about $707 billion in working capital, a 40% increase from pre-pandemic levels, which shows how widespread liquidity pressure has become across industries, according to Resolve's working capital analysis. When large companies struggle to turn receivables and inventory into usable cash, smaller firms feel the strain even faster.

That creates a steady market for brokers who can help owners find practical funding options when timing matters more than theory.

Small business owners make up a huge share of the economy. The U.S. Chamber of Commerce says small businesses employ nearly half of the American workforce and represent 43.5% of America's GDP, while banks decline most small business loan applications, leaving a large gap in available capital, as shown in the U.S. Chamber small business data center. That gap is where working capital leads come from.

Businesses rarely wake up wanting debt. They wake up needing time, flexibility, and enough liquidity to keep moving.

This is why the opportunity works for aspiring entrepreneurs. A home-based brokerage doesn't need heavy overhead. It needs a repeatable way to identify owners with a real cash timing problem, a funding need that can be solved, and enough urgency to act.

Some leads need a line of credit. Others need short-term working capital, receivables-based funding, or options such as invoice factoring for small business. The broker's value isn't just finding a lender. It's recognizing the cash flow problem quickly and directing the owner toward a fitting solution.

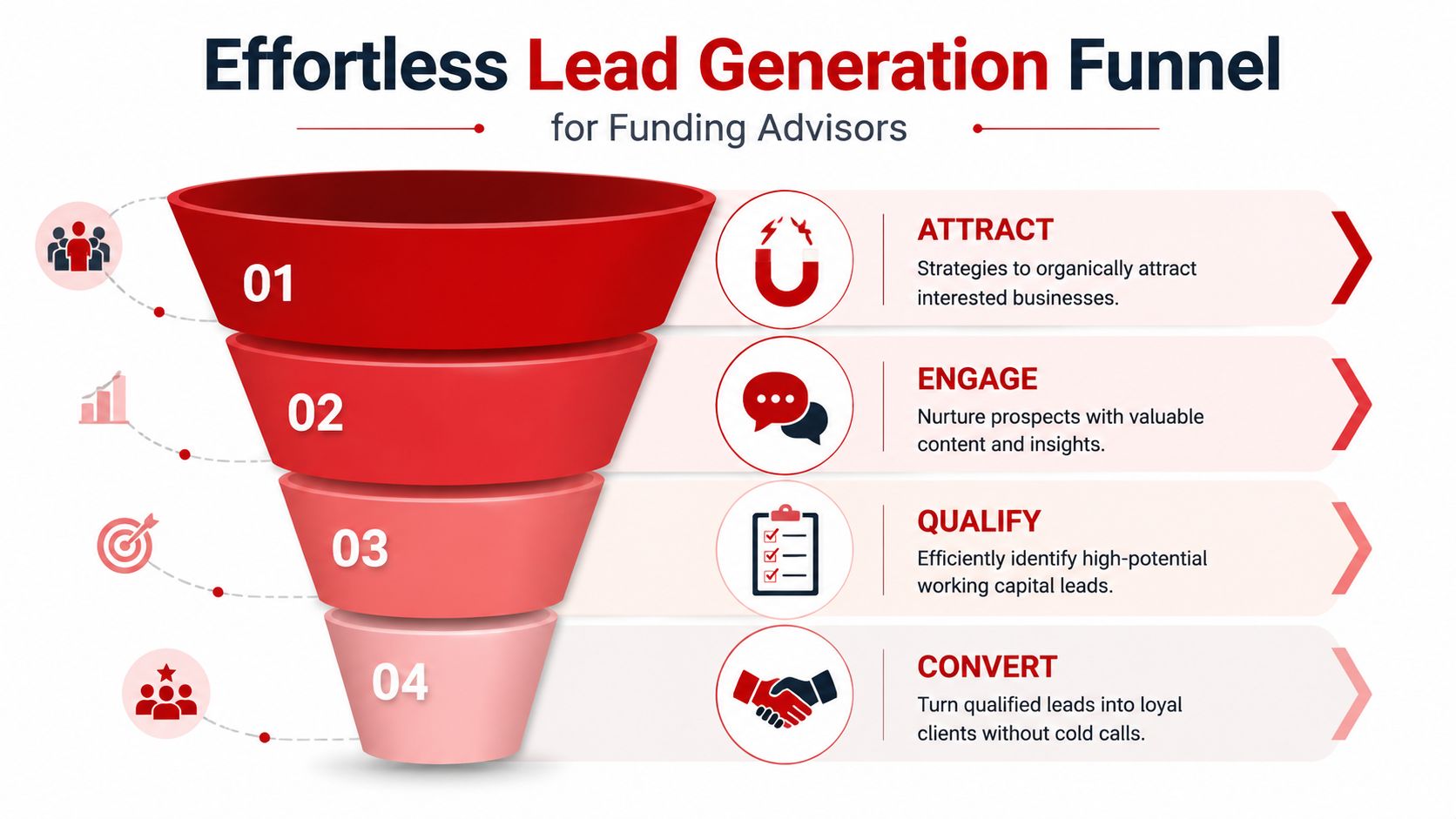

Building Your Lead Generation Engine Without Cold Calling

Cold calling isn't the only path to a brokerage pipeline, and for many people it shouldn't be the core path at all. Working capital leads respond better when the outreach is tied to timing, context, and trust.

A better model uses three channels at once. Referrals bring in warm deals. Content attracts owners who are already searching for help. Targeted outreach reaches businesses that are showing visible signs of cash flow friction.

Referral partners who already serve cash-strapped owners

The most reliable early pipeline usually comes from professionals who already hear about funding problems first.

That includes:

- CPAs and bookkeepers: They see tax pressure, uneven receivables, and seasonal slowdowns before most outsiders do.

- Attorneys: They often know when a business is restructuring, settling disputes, or navigating a partner change.

- Consultants and agencies: They hear owners say yes to growth plans, then admit cash is the constraint.

- Insurance and real estate professionals: They work with business owners during expansion, relocation, and equipment decisions.

The mistake new brokers make is asking for referrals too quickly. The better approach is to become useful first. Share a short funding intake checklist. Explain which clients are a fit, which aren't, and how the process works. That lowers the risk for the referral partner.

A relationship-driven brokerage also benefits from organized follow-up. A simple CRM helps track referral sources, stage notes, and follow-up dates. For brokers who want a practical view of how a pipeline system supports consistency, this piece on a CRM system for mortgage brokers maps out principles that transfer well to lending workflows.

Content that attracts owners before they apply anywhere else

Content works when it answers the questions owners are already typing into search bars and social platforms. It fails when it tries to sound clever.

Strong topics usually sound plain:

- What to do when payroll and receivables don't line up

- How to compare a short-term funding option with a line of credit

- What lenders look for when cash flow is tight

- When inventory growth creates a working capital problem

A broker doesn't need to publish every day. A small library of useful articles, email sequences, and short posts can keep bringing in inquiries over time. On the social side, brokers who use LinkedIn for relationship building can sharpen their outreach process by studying a master LinkedIn lead generation framework that focuses on message quality and targeting discipline.

Practical rule: Content should answer a funding question that an owner is already worried about this week, not a question the broker wishes they cared about.

Targeted outreach based on real cash flow friction

Targeted outreach is not cold calling with a nicer label. It starts with a reason.

The strongest signals often come from businesses dealing with collection delays, supplier pressure, inventory build-up, or rapid growth that hasn't translated into available cash. A short email or direct message works better when it references a likely problem pattern and offers a conversation, not a pitch deck.

A newer lead category has emerged around failed forecasting. Brex reports that 80% of top suppliers now require quarterly financial reviews and 60% of businesses still lack accurate cash flow models, which opens the door for brokers to find owners after internal forecasting breaks down, as outlined in Brex's working capital guidance. These aren't abstract prospects. They're businesses that thought they had visibility and then hit a cash shortfall anyway.

That changes how outreach should sound:

- Reference the pressure point: supplier reviews, missed forecast assumptions, or a cash gap tied to growth.

- Offer a brief diagnostic call: not a full application request.

- Ask timing questions: when payroll, inventory purchases, or vendor obligations hit.

- Move quickly: owners who reach this stage are usually trying to solve a near-term issue.

This system is why no-cold-calling models hold up. Instead of chasing random business owners, the broker builds a lead engine around people who already have motive, context, and a reason to respond.

Qualifying Leads to Focus on Winnable Deals

A full pipeline can still be a weak pipeline if too many leads are unqualified. New brokers often lose time on businesses that are curious but not committed, urgent but unfundable, or active but pointed toward the wrong product.

The fix is a qualification process that screens for movement, not just interest.

What strong working capital leads usually signal early

One useful sign is operational behavior. Companies that implement electronic workflows for payables and digitize invoices for collections see a 25% faster cash collection cycle, and businesses pursuing those efficiencies are often strong working capital candidates because they're actively trying to solve a timing issue instead of ignoring it, based on Eagle Business Credit's working capital discussion.

That kind of lead is usually easier to work with than the owner who says cash flow is tight but hasn't cleaned up invoicing, collections, or payment practices.

Another screening improvement comes from separating a true lead from a true prospect. A useful primer on lead and prospect qualification helps clarify the mindset. In brokerage terms, a lead has shown interest. A prospect has a real funding need, a plausible path to approval, and a reason to act now.

Working Capital Lead Scoring Criteria

A simple scoring model keeps the pipeline clean.

| Criteria | Points | Notes |

|---|---|---|

| Clear use of funds | High | The owner can explain whether the money is for payroll, inventory, vendor obligations, repairs, or another short-term operating need. |

| Timing pressure | High | An upcoming cash gap creates urgency. Vague future plans score lower. |

| Operational discipline | Medium | Digitized invoicing, active collections, and attention to payables suggest a business that's trying to improve, not just borrow blindly. |

| Financial awareness | Medium | The owner knows basic revenue patterns, major expenses, and where the cash squeeze is happening. |

| Responsiveness | Medium | Fast replies and completed document requests usually signal a real deal. |

| Product fit | High | The lead's situation matches a realistic funding option instead of forcing the wrong structure onto the business. |

| Referral source quality | Medium | A trusted referral partner often sends cleaner deals than broad, unfiltered inbound traffic. |

| Growth versus distress balance | Medium | Growth-related working capital needs can be very fundable. Deep unmanaged distress often requires a different conversation. |

This doesn't need to be complicated. A broker can use simple labels such as high, medium, and low to sort the pipeline daily.

A calculator can also help frame conversations around need and payment structure before a submission goes out. A practical example appears in this business building loan calculator, which shows how a structured estimate helps qualify fit and expectation.

When negative working capital is not a deal killer

Experienced brokers separate themselves from script readers.

Negative working capital can signal trouble, but it can also reflect an efficient operating model in certain industries. High-volume retail businesses, for example, may collect cash quickly and pay suppliers later. That doesn't automatically mean the business is weak. It may mean the owner runs a fast-turn model with strong cash discipline.

A number on a balance sheet doesn't tell the whole story. The operating rhythm behind that number matters more.

The right question isn't, "Is working capital negative?" The right question is, "Why?" If the answer points to strong turnover and disciplined payables, the lead may be better than it first appears. If the answer points to chronic collection issues, stale inventory, or unpaid obligations piling up, caution is warranted.

The Consultant's Approach to Converting Leads

The conversion phase works best when the broker stops acting like a marketer and starts acting like a guide. Business owners don't need pressure once they've raised their hand. They need clarity.

A typical lead conversation often begins with tension. The owner wants funding, but doesn't want to feel judged. They may have applied elsewhere, been told no, or received terms they didn't understand. A strong broker lowers that friction by making the first conversation orderly and specific.

How a discovery call should feel

A productive call usually moves in this order:

Start with the operating issue

Ask what created the need. Was it seasonality, growth, receivables timing, supplier pressure, or an unexpected expense?Clarify the use of funds

The broker needs a practical answer. Payroll, inventory, vendor catch-up, repairs, marketing, or short-term operating cushion all lead to different conversations.Establish timing

The most important deals often have a real calendar attached to them. If the owner needs funds before a vendor deadline or payroll run, that shapes the next steps.Set expectations on documentation

Many deals either tighten up or drift away during documentation. A clean list beats a vague request.

A broker might say something like this during the call:

“The first step is understanding what created the cash gap and how quickly the business needs a solution. Once that's clear, the funding path becomes much easier to narrow down.”

That language calms the conversation because it tells the owner there is a process. It also positions the broker as someone who solves fit problems, not someone who chases signatures.

A follow-up email that moves the deal forward

The best follow-up message is short, direct, and built around next actions.

Sample email

Subject: Next steps for working capital options

Hi [Owner Name],

Thank you for the conversation today. Based on what was shared, the main issue appears to be a short-term cash timing gap tied to [use of funds].

The next step is to review the documents needed to determine which funding options are the most realistic fit. Once those items are in, the broker can assess timing, structure, and what lenders are most likely to consider.

Please send:

- recent business bank statements

- a brief note confirming use of funds

- any updated revenue or receivables information that helps explain the current cash flow situation

Once received, the broker will review everything and respond with the clearest path forward.

Best,

[Broker Name]

This works because it avoids hype. It doesn't promise approval. It doesn't oversell access. It gives the owner a clean checklist and keeps momentum alive.

Another useful habit is documenting the emotional context of the call. Did the owner sound embarrassed, defensive, confident, rushed, or highly organized? Those details often predict how the deal will move more accurately than enthusiasm alone.

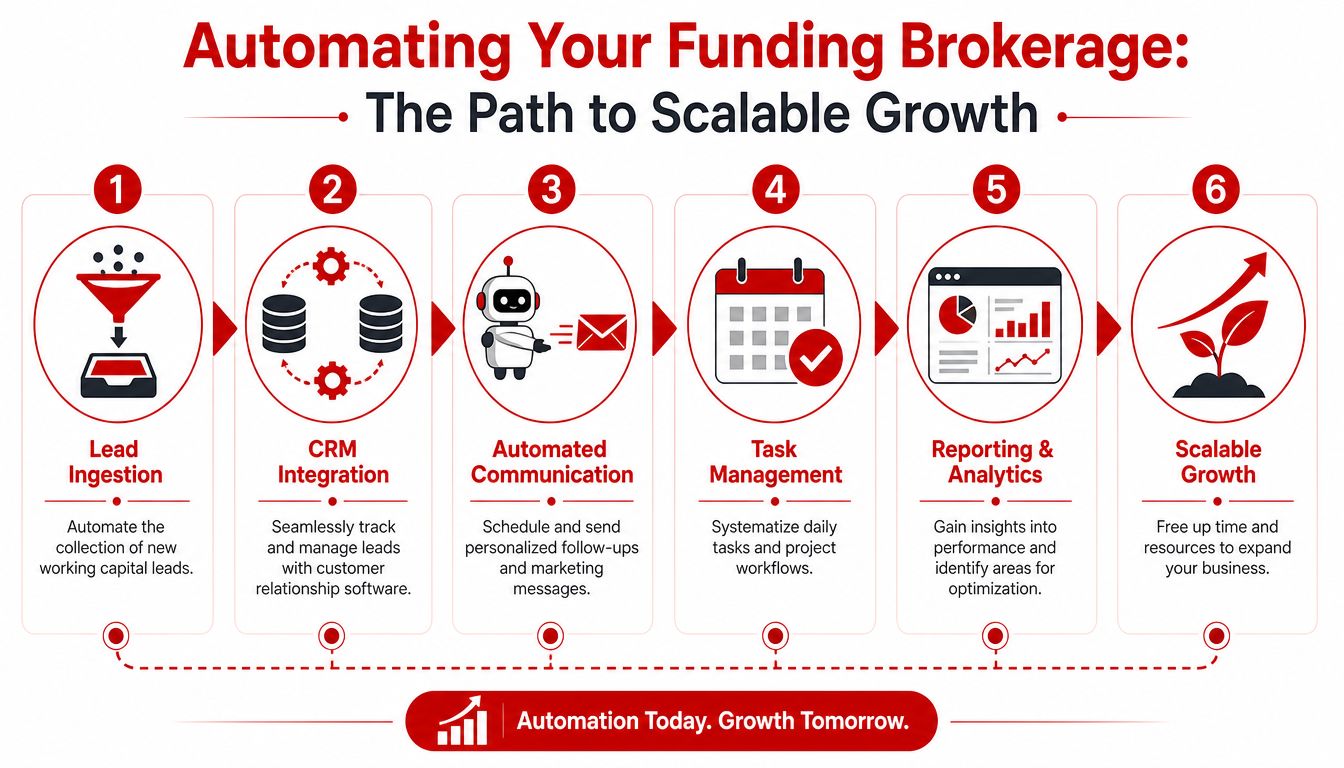

Automating Your Brokerage for Scalable Growth

A brokerage stops feeling like a job and starts feeling like a business when the back end becomes repeatable. Manual follow-up, scattered notes, and inbox-only lead tracking create bottlenecks fast.

The better model is borrowed from working capital discipline itself. Taulia outlines a four-step framework that starts with defining objectives, reviewing current strategies, identifying improvement areas, and implementing solutions, and that same structure works well for a broker building internal systems, as described in Taulia's working capital strategy guide.

Use a simple four-part system

Define objectives.

Decide what the system must do. For most brokers, that means capturing inbound leads, tracking referral sources, following up automatically, and keeping document requests organized.

Review current workflow.

Look at how leads enter the pipeline now. Some arrive through referrals, some through content, some through outreach. If each one gets handled differently, consistency disappears.

Identify improvement areas.

The usual weak spots are response time, missed follow-ups, and poor visibility into which lead sources convert.

Implement solutions.

Start small. A basic CRM, a short email nurture sequence, and task reminders cover a lot of ground. For brokers exploring process design more broadly, this process improvement example shows how documenting steps can tighten operations.

What to automate first

Not everything should be automated. Relationship building and deal diagnosis still need human judgment. Administrative repetition doesn't.

A practical starting list looks like this:

- Lead capture: Route referral forms, website inquiries, and direct messages into one place.

- Follow-up reminders: Create automatic tasks so older leads don't disappear.

- Email sequencing: Send polite check-ins to leads who need time before re-engaging.

- Pipeline tagging: Mark leads by source, industry, urgency, and funding need.

- Weekly review: Look at stalled deals, active submissions, and referral partner activity.

For readers interested in broader workflow design, a practical guide to AI automation offers useful ideas for reducing repetitive admin work without overcomplicating the business.

One structured option in this category is Business Lending Blueprint, which provides training, scripts, and systems for building a referral-driven loan brokerage from home. The value of any such program comes down to whether it helps the broker create a repeatable process, not just generate short bursts of activity.

Your Path to Becoming a Six-Figure Funding Advisor

The appeal of this business isn't just that it can be run remotely. It's that the model connects effort to value in a direct way. A broker builds referral relationships, generates qualified working capital leads, solves funding problems, and gets paid when deals close.

That compensation structure is clear. Business loan brokers typically earn commissions ranging from 1% to 5% of the total loan amount, and a $150,000 working capital deal at 4% pays $6,000, according to NerdWallet's business loan broker overview. That doesn't guarantee earnings, but it does show why a focused pipeline matters so much.

This is also why sustainable systems beat random hustle. Referral partners create repeat business. Useful content compounds over time. Clean qualification protects the calendar. Automation keeps follow-up from slipping. The result is a business that can start part-time and grow into a serious advisory practice.

For professionals leaving a traditional job, adding a new income stream to an existing service business, or looking for a more flexible path, funding advisory offers something practical. Business owners need help finding capital. A broker who learns how to bring in the right leads and guide them responsibly can build a durable, home-based business around that need.

Business Lending Blueprint shows aspiring brokers how to build that kind of business with a referral-driven model, practical systems, and real-world funding workflows. To see how the model works, watch the free training at Business Lending Blueprint or schedule a strategy session to evaluate whether this path fits your goals.