From Chaos to Commissions: Why Process Is Your Secret Weapon

Are you drowning in paperwork, chasing down clients for documents, and watching promising deals stall for weeks? That's the normal starting point for a lot of new business loan brokers. They get interested in helping business owners secure funding, they find real demand in the alternative lending space, and then the backend of the business starts breaking down.

The brokers who stay stuck usually blame lead quality, lenders, or timing. The brokers who build a durable business fix the machine behind the deal. Process is what turns scattered activity into repeatable revenue, especially in a home-based brokerage where every missed follow-up, missing bank statement, or unclear handoff can cost a commission.

That matters because the opportunity is real. The U.S. Small Business Administration reports that about 50% of small business loan applications are denied by traditional banks, which leaves a large group of business owners looking for non-bank funding options. For independent brokers, that creates room to serve clients through alternative lenders while building a referral-driven business from home.

This article is a practical blueprint, not a corporate theory lesson. These are 8 process improvement examples designed for the independent business loan broker who wants better control, cleaner submissions, stronger referral relationships, and a business that can grow beyond part-time hustle.

Table of Contents

- 1. Lean Process Mapping

- 2. Six Sigma DMAIC Framework

- 3. Referral System Optimization

- 4. Technology Integration and Automation

- 5. Deal Flow Pipeline Management

- 6. Lender Relationship Management and Partner Optimization

- 7. Compliance and Documentation Standardization

- 8. Performance Metrics and Key Performance Indicator KPI Tracking

- 8-Point Process Improvement Comparison

- Your Blueprint for a Scalable Loan Broker Business

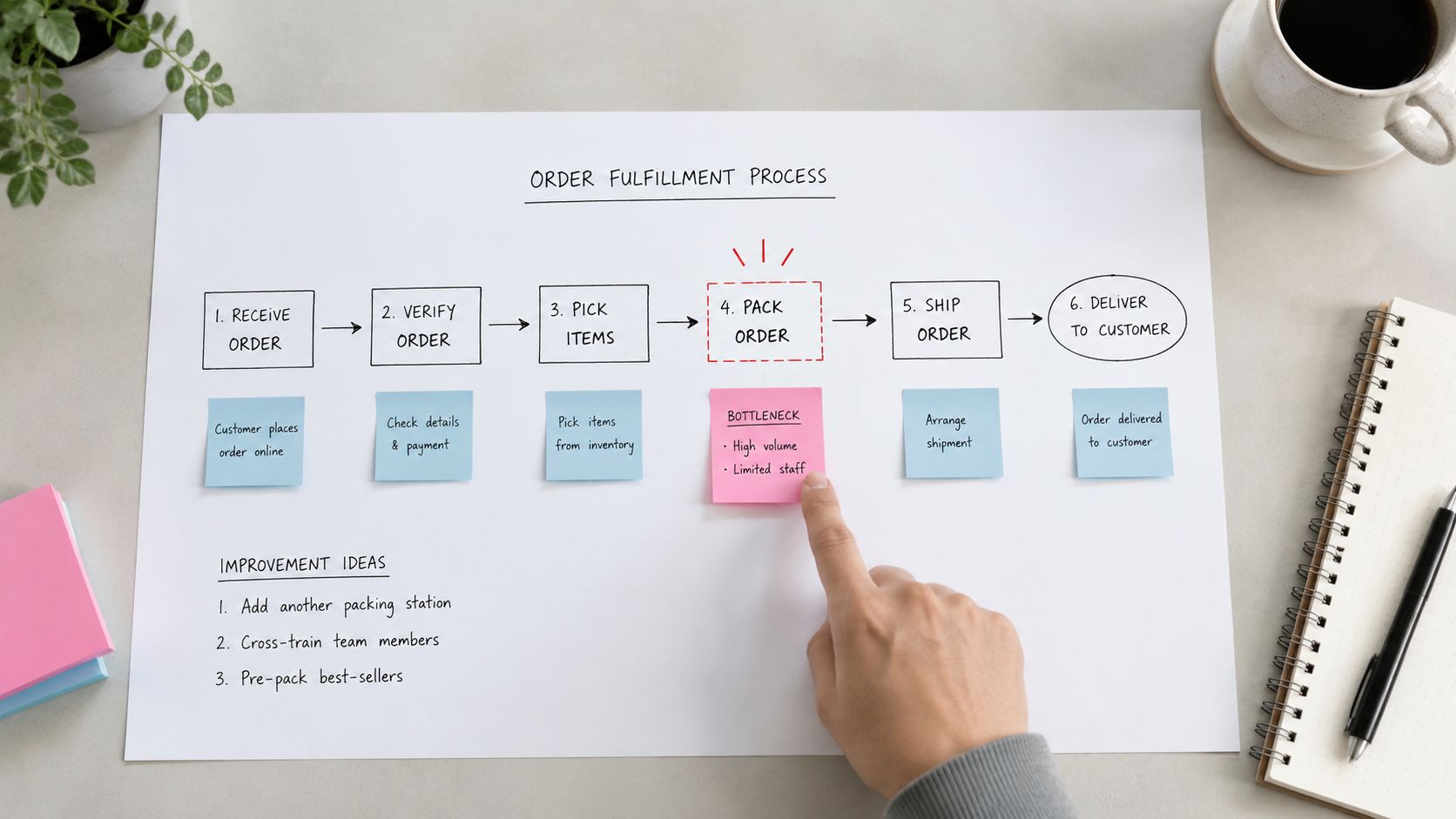

1. Lean Process Mapping

Most brokers think they know their workflow until they map it. Then they see the truth. Leads come in from three places, intake happens in two different ways, documents live across email and cloud folders, and nobody can clearly say what happens between “interested prospect” and “funded deal.”

That's why lean process mapping is one of the strongest process improvement example methods for a loan brokerage. It forces every step into view, including the waste. In brokering, waste usually looks like duplicate outreach, unclear responsibility, missing documents, and avoidable status-check emails.

Where brokers usually lose time

A practical map starts with one lane only. Lead to application is usually the best starting point because that's where most deals either gain momentum or stall.

A broker can sketch this on a whiteboard, in flowchart software, or inside a CRM notes field. The tool matters less than the visibility.

- Start with one workflow: Map the path from referral received to complete submission.

- Name each owner: Who sends the intake form, who checks documents, who updates the client, who submits to lenders.

- Add delays, not just steps: The bottleneck is often the waiting period between actions.

- Mark rework loops: If a file gets returned for missing statements or unsigned forms, that should appear on the map.

Brokers don't usually have a lead problem first. They have a handoff problem.

The strongest reason to map the process is that standardized inputs reduce rework. At Piraeus Bank, process mining of the consumer loan approval workflow used over 1 million event logs and found that lack of standardized data input caused 40% of rework loops. After standardization and automation, average processing time dropped from 35 minutes to 5 minutes, an 86% reduction in total lead time. That case shows what happens when process discipline replaces ad hoc intake and review.

For a solo or small brokerage, the takeaway is straightforward. If the same document issues keep showing up, the process isn't failing at underwriting. It's failing at intake.

2. Six Sigma DMAIC Framework

DMAIC sounds corporate, but the method fits brokering well because it solves one painful issue at a time. Define, Measure, Analyze, Improve, Control. That sequence stops a broker from guessing and pushing random fixes into the workflow.

A useful place to apply it is stalled submissions. If files sit too long in review, the broker needs more than motivation. The broker needs a method.

A tighter way to solve one problem at a time

Define the exact issue. “Deals take too long” is weak. “Qualified files sit in review because lenders receive inconsistent supporting documents” is a real problem statement.

Then measure what's happening now. Time from intake to submission, time from submission to lender response, and time from approval to funding are all workable internal metrics. Once the timeline is visible, patterns emerge.

Walmart's operational overhaul is a good example of why DMAIC works when it's applied seriously. Using Six Sigma and RFID-enabled inventory visibility, Walmart increased inventory turnover by 25%, reduced out-of-stock incidents by 40%, lowered logistics expenses by 15%, and generated $33 million in annual savings and avoided costs. The structure mattered because Define, Measure, Analyze, Improve, and Control were tied to real operating decisions.

Practical rule: Don't run DMAIC on your whole business. Run it on one leak in the pipeline.

For a loan broker, that often leads to changes like tighter pre-screening, clearer lender-specific document lists, and a submission review step before files go out. Those are simple moves, but they create consistency. Teams that want to boost efficiency with lean methods usually find that discipline beats complexity.

What doesn't work is jumping straight to software before the problem is defined. If the submission process is sloppy, a CRM just helps the broker track sloppy faster.

3. Referral System Optimization

A new broker often spends too much time trying to market everywhere. That usually leads to weak relationships and unpredictable lead flow. Referral system optimization fixes that by narrowing attention to the people who already serve the same business owner.

That's especially important in a brokerage model because referral trust compounds. A CPA, consultant, insurance advisor, or business services professional doesn't keep referring based on one good conversation. They refer based on a clean process, clear communication, and confidence that their client won't be mishandled.

Build a referral machine instead of chasing random leads

The first move is simple. Track every referral source and connect it to outcome. Not vanity activity. Outcome.

A broker should know which sources send complete prospects, which ones send tire-kickers, and which ones send owners who are ready to move. That's the difference between a network and a system.

- Tier the partners: Frequent, high-quality referrers get regular updates and real attention.

- Close the loop fast: When a referred client submits, gets approved, or needs more documents, the partner should know.

- Use one-page tools: A short partner guide, funding options summary, or intake explainer makes referral easier.

- Protect the relationship: Brokers should never make the partner chase for updates.

The economics make this worth refining. Alternative lending products such as merchant cash advances, term loans, and lines of credit can generate broker commissions ranging from $1,000 to $15,000 per funded deal, with typical commissions often in the 3% to 5% range. That means one good referral relationship can be materially more valuable than broad but inconsistent outreach.

A strong process improvement example here is replacing generic “checking in” messages with a referral cadence. Monthly market updates, lender appetite changes, and short educational notes give partners a reason to remember the broker. What doesn't work is asking for referrals repeatedly without giving visibility or value back.

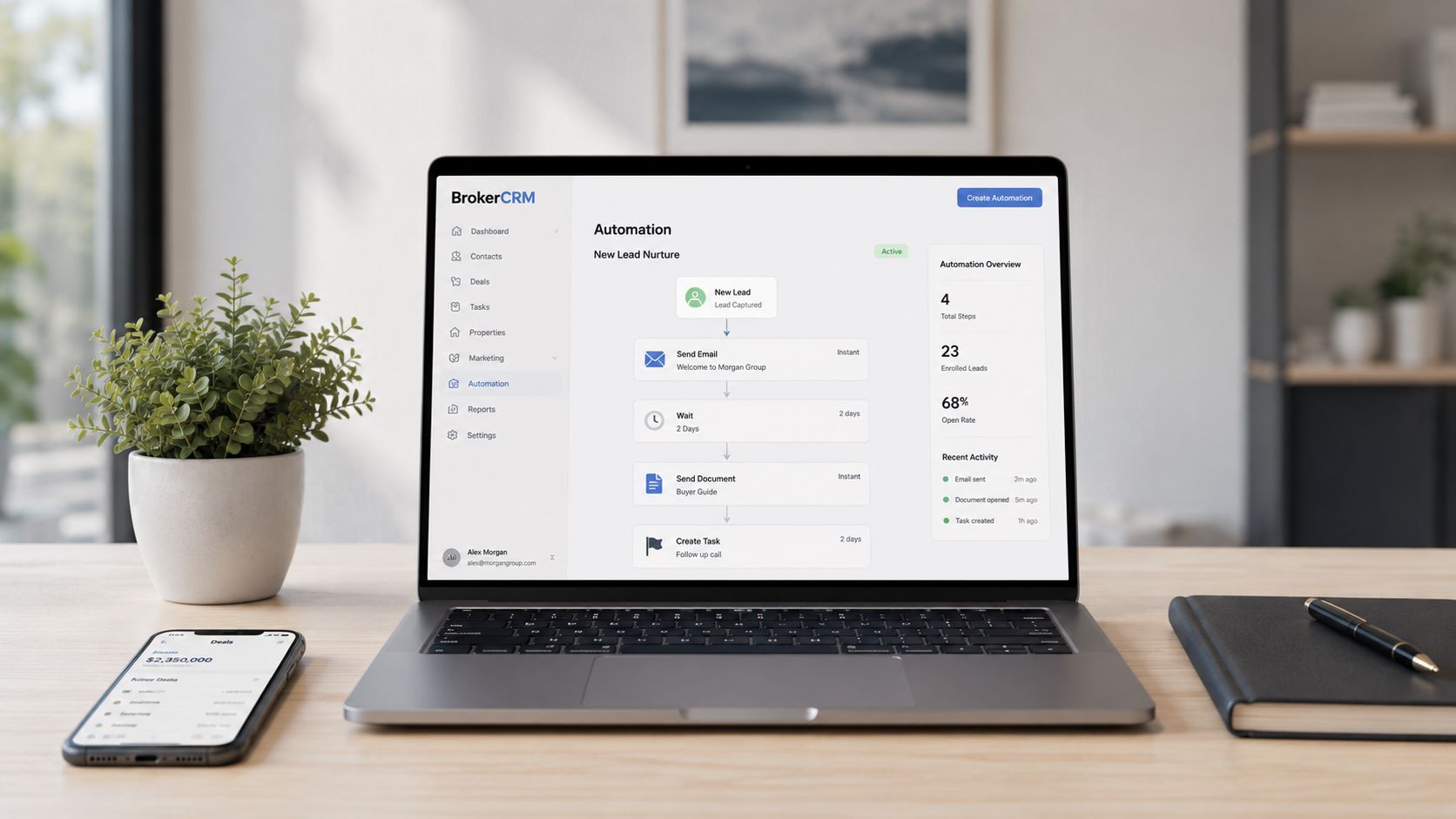

4. Technology Integration and Automation

Technology should remove friction, not create another side project. A lot of brokers buy software too early, set up half the features, and end up doing the same work with more tabs open. The better approach is narrower. Automate the repetitive pieces that drain selling time.

The data supports that direction. In a 2023 Pipefy survey, 59.4% of business and IT leaders in the United States identified automation as the primary benefit of adopting process improvement methodologies. That fits the brokerage model well because repetitive admin work is what usually crowds out relationship building.

Automate the repeatable parts

The highest-value automation points are usually intake, document reminders, milestone emails, and task triggers. A broker doesn't need a huge stack to make that work. One CRM, one document storage system, and one simple automation layer is enough for many home-based operations.

For brokers evaluating systems, this guide to a CRM system for mortgage brokers is useful because the operational principles carry over well to business lending. The categories may differ, but the workflow discipline is similar.

A practical setup often includes:

- CRM tracking: HubSpot, Pipedrive, or Zoho for stage management and communication logs.

- Document organization: Shared folders with lender-specific naming conventions.

- Email sequences: Status updates triggered when a deal changes stage.

- Compliance records: Every major touchpoint logged automatically.

Automation should handle reminders, routing, and recordkeeping. It shouldn't replace judgment on deal fit.

Brokers who rely on better systems also tend to improve responsiveness. That matters for both clients and referral partners. Stronger operational follow-up supports data-driven mortgage lead strategies because leads convert better when the process behind them is timely and organized.

What doesn't work is automating messy language and messy files. If the intake form is unclear, automating it just scales confusion.

5. Deal Flow Pipeline Management

A broker can't manage what isn't staged. If every lead lives in the same inbox and every active file feels equally urgent, the pipeline turns into emotional decision-making. That's where commissions get delayed.

Pipeline management gives every deal a visible position. New lead, qualified, docs requested, complete file, submitted, under review, approved, funded, paid. The exact labels can vary, but the movement must be clear.

Every deal needs a defined stage

The point isn't cosmetic organization. The point is control. When a broker reviews the pipeline weekly, the bottleneck becomes obvious. Maybe too many leads are qualified but never submit documents. Maybe lender reviews drag because the files weren't packaged correctly. Maybe approvals happen, but commission collection lags because final documentation wasn't tracked.

For clients, defined stages also reduce anxiety. They know where the deal stands and what's needed next. For brokers, the process exposes where time is leaking.

A practical process improvement example is adding stage-exit rules. A deal doesn't move from “qualified” to “docs requested” without a documented funding purpose. It doesn't move from “complete” to “submitted” without a lender-fit review. It doesn't stay in “under review” without a scheduled follow-up date.

- Set movement criteria: Every stage should have a clear entry and exit condition.

- Review aging deals weekly: Old files usually reveal either weak follow-up or poor qualification.

- Prioritize by probability and urgency: Not every file deserves the same attention.

- Record drop-off reasons: Lost deals teach more than won deals if they're documented.

Client communication matters here too. This resource on how to manage client expectations is directly useful because many stalled deals are really expectation failures dressed up as processing issues.

What doesn't work is an overcomplicated pipeline with too many statuses. If a broker needs a legend to understand the board, the board is too complex.

6. Lender Relationship Management and Partner Optimization

A broker's lender list is not just a directory. It's an operating asset. The strongest brokers don't blast every file to everyone. They know which partners move quickly, which ones handle edge cases better, and which ones communicate clearly during the review process.

That knowledge gets built through deliberate tracking and regular contact. Without it, lenders become interchangeable in the broker's mind, and that creates poor submissions and slower funding.

Match the deal to the right lender faster

This process starts with a lender scorecard. Nothing fancy. Product fit, document burden, speed, communication quality, and commission reliability are enough to begin.

As volume grows, lender optimization affects both service quality and income. The U.S. alternative lending market was valued at more than $240 billion in 2024 and is projected to reach $450 billion by 2028. That projected growth matters because brokers who organize lender relationships now will be in a stronger position to serve a larger base of business owners who don't fit traditional bank credit boxes.

A practical scorecard can include:

- Approval fit: Which lender handles weaker files, seasonal businesses, or urgent capital needs.

- Processing behavior: Which lender asks for clean, predictable follow-ups versus constant backtracking.

- Commission handling: Which partner is easy to reconcile after funding.

- Communication quality: Which account reps help structure a deal.

The right lender relationship shortens the path from application to answer. The wrong one creates unnecessary loops.

What doesn't work is treating every lender like a primary channel. Brokers need core partners, secondary partners, and backups. That structure improves submission quality because the broker stops guessing where a deal belongs.

7. Compliance and Documentation Standardization

At this stage, many part-time brokers get exposed. They can sell, they can network, and they can get a prospect interested. Then the file gets messy. Missing statements, inconsistent naming, unsigned disclosures, wrong lender requirements, no audit trail.

Standardization fixes that. It also protects trust. Business owners may tolerate a tough underwriting process, but they won't tolerate a disorganized broker handling sensitive financial records.

Standardization protects both speed and trust

A landmark 2018 case study by Maury, Donnelly & Parr showed that a rigorous business process improvement initiative reduced human errors by 75% when generating complex financial proposals. The firm used software-driven process improvements to standardize data entry and validation steps, which reduced manual calculation mistakes and improved operational reliability. That lesson translates well to brokerage work, where document handling errors can slow deals and damage credibility.

A broker doesn't need enterprise systems to apply the same principle. The essentials are simple.

- Use lender-specific checklists: Each top lender should have its own required-doc list and submission format.

- Create standard client instructions: Tell applicants exactly what to send, how to send it, and what delays approval.

- Add a pre-submission review: One last check catches omissions before the lender does.

- Store templates centrally: Disclosures, email scripts, status updates, and invoices should live in one place.

Brokers who also help clients strengthen their funding profile can connect documentation discipline with education. This overview of business credit building program building corporate credit fits naturally into that process because clients who understand credit and documentation standards tend to move through funding more cleanly.

What doesn't work is using one generic checklist for every lender. Standardization is not sameness. It's consistent execution against the right requirements.

8. Performance Metrics and Key Performance Indicator KPI Tracking

Many brokers avoid metrics because income is uneven. One month closes strong, the next month feels quiet, and that unpredictability makes the business seem hard to measure. But uneven income is exactly why metrics matter.

A brokerage doesn't run on effort alone. It runs on conversion. If the broker can't see where referrals turn into applications, where applications turn into approvals, and where approvals turn into paid commissions, growth stays guesswork.

Track what actually drives broker income

The best KPI dashboard for a broker is not complicated. Active referrals, completed applications, submission count, approval count, funded deals, commissions received, and average days in each stage are enough to make better decisions.

This matters in a remote model because low overhead gives brokers room to build carefully. Brokers in the business loan industry can often operate with less than $5,000 in annual overhead when working remotely, since they usually don't need office space, inventory, or licensed staff. When fixed costs are lean, performance tracking becomes even more important because small process gains can materially improve owner income without adding heavy expense.

A useful KPI habit looks like this:

- Review monthly, not randomly: Same day each month, same scorecard.

- Separate leading and lagging indicators: New referrals and complete files lead. Paid commissions lag.

- Track by referral source: Some relationships create volume. Others create funded deals.

- Watch aging: Deals sitting too long in one stage usually signal a process fault.

For brokers serving clients with more complex approval profiles, understanding alternative data for credit scoring can sharpen tracking as well. It helps connect file quality, lender fit, and outcome quality in a more disciplined way.

A dashboard doesn't need to impress anyone. It needs to tell the broker what to fix next.

What doesn't work is tracking vanity numbers. Social engagement, open rates, and random activity counts are secondary. The core question is simple. Which actions are producing submitted deals, funded deals, and paid commissions?

8-Point Process Improvement Comparison

| Approach | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Lean Process Mapping | Low–Medium, straightforward mapping work | Low, team time, basic flowchart tools | Clear bottlenecks; faster workflows; baseline metrics | High-volume processes, onboarding, follow-up optimization | Quick visibility, team alignment, foundation for improvements |

| Six Sigma DMAIC Framework | High, structured phases and analysis required | Medium–High, data collection, analytics tools, training | Reduced variation; measurable ROI; improved approval rates | Specific quality problems, reducing variability, process-critical issues | Data-driven decisions, root-cause fixes, sustainable control |

| Referral System Optimization | Medium, relationship programs and segmentation | Medium, time to nurture, tracking tools, incentives | More warm leads; higher conversion; predictable pipeline over months | Brokers seeking recurring deal flow and lower CAC | Compounding referral network, higher conversion, lower acquisition cost |

| Technology Integration and Automation | Medium–High, integrations and setup work | Medium, CRM/subscriptions, integrations, implementation time | Large time savings; scalability; improved accuracy and compliance | Scaling operations, delegating tasks, increasing deal volume | Automates repetitive work, increases capacity and consistency |

| Deal Flow Pipeline Management | Low–Medium, process discipline and stage definitions | Low, CRM or spreadsheet, regular review time | Visibility into revenue; better prioritization; improved forecasting | Managing multiple active deals, revenue forecasting | Forecasting, deal prioritization, prevents lost opportunities |

| Lender Relationship Management & Partner Optimization | Medium, ongoing outreach and profiling | Medium, time for calls, tracking, analysis | Better lender matches; faster funding; higher commissions | Improving approval rates, negotiating better terms, high-value deals | Preferential access, improved match-making, negotiating leverage |

| Compliance & Documentation Standardization | Medium, create templates and QC steps | Low–Medium, templates, document storage, review process | Fewer rejections; faster lender processing; audit readiness | High-rejection environments, regulated markets, team onboarding | Reduces errors, protects compliance, enables delegation |

| Performance Metrics & KPI Tracking | Low–Medium, define KPIs and reporting cadence | Low, dashboard/spreadsheet, monthly update time | Objective business health; data-driven growth decisions | Scaling firms, goal-oriented brokers, performance improvement | Accountability, early warning signs, clear growth roadmap |

Your Blueprint for a Scalable Loan Broker Business

The brokers who build stable income from home usually aren't doing exotic things. They're doing ordinary things in a disciplined sequence. They map the workflow, tighten one bottleneck at a time, organize referral sources, automate repeatable tasks, manage the pipeline by stage, build lender relationships intentionally, standardize documentation, and track the numbers that matter.

That combination provides an advantage. It also creates flexibility. A broker can work remotely, build around family or a full-time job at the start, and still operate like a professional business instead of a side hustle held together by memory and inbox searches.

The broader opportunity is strong. Business owners continue to need capital outside traditional banking channels, and brokers sit in the middle of that need. The model is also attractive for people who want a home-based business with relatively lean operating costs and room to scale through referrals rather than constant cold outreach. For those who execute well, the economics can be meaningful because funded deals in alternative lending can generate commissions, and repeat referral relationships can create recurring opportunity over time.

The mistake is thinking growth starts with more leads. Usually, it starts with a better process. More leads poured into a weak intake system just creates more confusion. More lender relationships without tracking creates more mismatches. More referral partners without a follow-up process creates more disappointment. The process has to come first.

That's why each process improvement example in this guide matters. None of them are complicated on their own. Together, they build a brokerage that's easier to run, easier to scale, and easier for referral partners to trust. That's the foundation of a six-figure business in this space. Not hype. Not luck. Consistent execution.

Business Lending Blueprint is one relevant option for people who want a structured path into this industry. Its training focuses on the operational side of building a business loan brokerage, including referral systems, lender access, workflow discipline, and practical deal flow processes. For aspiring entrepreneurs, professionals, consultants, salespeople, bankers, and CPAs who want to add a recession-resistant income stream, that kind of framework can shorten the learning curve.

The next step should be practical. Learn the model, see the workflow, and understand how the pieces fit together before trying to assemble them alone. Watch the training, study the process, and build the business the right way from day one.

Business Lending Blueprint helps aspiring entrepreneurs build a profitable, home-based business as a business loan broker by using proven referral systems, lender relationships, and optimized operational workflows. To see how the full model works, watch the free training at Business Lending Blueprint or schedule a strategy session to explore whether this business fits your goals.